ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

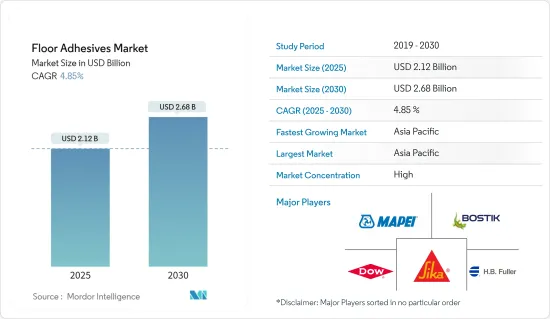

세계의 바닥용 접착제 시장 규모는 2025년 21억 2,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 4.85%로 확대되어, 2030년에는 26억 8,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

급속하게 성장하는 세계의 건설 업계와 바닥용 접착제의 범용성, 안전성, 도포의 용이성이 시장 성장을 견인할 것으로 보입니다.

반면, VOC 배출로 인한 건강에 부정적인 영향이 시장 성장을 방해할 수 있습니다.

바이오의 바닥용 접착제에 대한 수요 증가는 아마 기회로 작용할 것으로 보입니다.

아시아태평양은 세계 시장을 독점하고 있으며, 가장 큰 소비는 중국, 인도, 일본 때문입니다.

바닥용 접착제 시장 동향

주택 최종 사용자 산업 부문에서 수요 증가

타일 및 석재용 접착제는 주택 최종 사용자 산업 부문에서 가장 일반적으로 사용되는 접착제 유형입니다. 또한 주택 부문은 조사한 시장에서 가장 크고 가장 빠르게 성장하는 부문입니다.

가처분 소득 증가와 함께, 중류 계급 인구 증가는 중류 계급의 주택 부문의 확대를 촉진하여 바닥용 접착제의 사용을 증가시킵니다.

세계은행에 따르면 세계 건설산업의 가치는 2020년 22조 3,600억 달러에서 2021년 27조 1,800억 달러로 증가하고 있습니다.

중국과 인도의 주택 건설 시장 확대로 아시아태평양에서 가장 높은 성장이 예상됩니다. 이 두 지역은 2030년까지 세계 중간층의 43.3% 이상을 차지할 것으로 예상됩니다. 인도 정부는 주택에 과세되는 GST세를 12%에서 5%로 인하했습니다. 이 세금 감소로 인해 중간층 주택 건설 시장이 확대될 수 있습니다.

또한 2021년 10월 상파울루 주택 조합(Secovi-SP)은 브라질 상파울루에서 5,555호의 신규 주택 판매를 기록했습니다. 이 수는 주택에 대한 개인 소비가 증가함에 따라 증가할 가능성이 높습니다. 게다가 브라질의 단독 주택 동향은 향후 주택 건설 업계를 지원할 것으로 보입니다.

멕시코의 주택 착공 건수와 재고 수준은 연방 주택 보조금 제도의 대폭 삭감과 심각한 불황의 방아쇠가 된 팬데믹에 의해 10년 만의 저수준에 이르렀습니다. 사회적 주택 프로그램(Programa de Vivienda Social)은 2021년 예산이 179% 증가한 2억 달러로 건설 지출을 지원하게 되었습니다. 또한, 사용하기 쉬운 대출 제도와 유리한 주택 융자 제도는 이 나라의 주택 건설에 혜택을 줄 것으로 예상됩니다.

저가 주택 분야는 주로 도시 지역과 농촌 지역의 빈곤층에 저렴한 주택을 제공하는 정부의 이니셔티브으로 꾸준히 증가하고 있습니다.

저가 주택 건설에서 바닥용 접착제의 소비량은 다른 유형의 주택에 비해 상대적으로 적습니다. 세계 여러 나라들이 기타 국가의 난민들에게 대피소를 제공합니다. 따라서 정부는 난민들에게 일시적 또는 영구적인 저비용 주택을 제공합니다.

시장을 독점하는 아시아태평양

아시아태평양은 바닥용 접착제 세계 시장 점유율을 독점하고 있습니다. 중국, 인도, ASEAN 국가와 같은 국가에서 건설 활동이 증가함에 따라 바닥 접착제 소비량은이 지역에서 증가하고 있습니다.

중국 정부는 경제를 보다 서비스 지향 형태로 재조정하려는 노력에도 불구하고 향후 10년간 2억 5천만 명이 새로운 거대 도시로 이동할 준비를 포함한 대규모 건설 계획을 개발하고 있습니다.

중국국가통계국에 따르면 중국 건설공사 시장은 2020년 23조 2,700억 위안(3조 3,400억 달러)에서 2021년에는 25조 9,200억 위안(3조 7,200억 달러)으로 증가했습니다.

중국은 세계 최대 건설 시장이며 세계 건설 투자의 20%를 차지합니다. 중국은 2030년까지 약 13조 달러를 건축물에 투자할 것으로 예상됩니다. 중국은 지속적인 도시화 과정을 추진하고 진행 중이며 2030년 목표율은 70%입니다.

인프라 프로젝트에 대한 정부의 관심 증가와 주택 및 상업 부문에 대한 수요의 급속한 회복이 예측되기 때문에 건설 부문은 2022년도에 10.7%의 성장이 전망되고 있습니다. 따라서 이 나라의 건설 활동 확대는 바닥용 접착제 수요를 증가시킬 것으로 예상됩니다.

스마트 시티 프로젝트와 2022년까지의 만인주택건설 등 인도 정부가 실시하는 다양한 정책은 침체하는 건설 업계에 필요한 자극을 가져올 것으로 기대되고 있습니다. 또한 부동산법, GST, REIT와 같은 최근 정책 개혁은 승인 지연을 줄이고 향후 몇 년동안 건설 부문을 강화할 것으로 기대됩니다.

통계청 데이터에 따르면 한국의 건설업체가 2021년에 획득한 건설수주는 견조한 국제 수요로 2자리 증가했습니다. 한국통계청에 따르면 2021년 한국 내외 건설업체가 모은 건설수주는 총액 2,459억 달러로 2020년보다 31조원 증가했습니다.

바닥용 접착제 산업 개요

세계의 바닥용 접착제 시장은 부분적으로 통합되어 있습니다. 주요 기업은 Seika AG, MAPEI SpA, Arkema Group(Bostik SA), HB Fuller Company, Dow 등입니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

급성장하는 세계 건설 업계

바닥용 접착제의 범용성, 안전성, 도포 용이성

억제요인

VOC 배출에 의한 건강에 대한 악영향

기타 억제요인

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

수지 유형

에폭시

폴리우레탄

아크릴

비닐

기타 수지 유형

기술

수성

용제형

기타 기술

용도

타일&석재

카펫

목재

라미네이트

탄성 바닥재

기타 용도

최종 사용자 산업

주택

상업

공업용

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

3M

Arkema Group(Bostik SA)

Ashland

Dow

Forbo Holding AG

HB Fuller Company

Henkel AG & Co. KGaA

Jowat SE

LATICRETE International Inc.

MAPEI SpA

Pidilite Industries Limited

Sika AG

Tesa SE

제7장 시장 기회와 앞으로의 동향

바이오 바닥용 접착제에 대한 수요 증가

JHS

영문 목차

영문목차

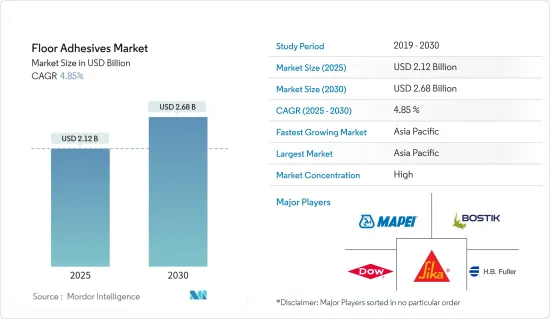

The Floor Adhesives Market size is estimated at USD 2.12 billion in 2025, and is expected to reach USD 2.68 billion by 2030, at a CAGR of 4.85% during the forecast period (2025-2030).

Key Highlights

The rapidly growing global construction industry and the versatility, safety, and ease of application of floor adhesives, are likely to drive market growth.

On the flip side, hazardous health effects due to VOC emissions may hinder the market's growth.

Increasing demand for bio-based floor adhesives will likely act as an opportunity.

Asia-Pacific dominates the global market, with the largest consumption coming from China, India, and Japan.

Floor Adhesives Market Trends

Increasing Demand from Residential End-user Industry Segment

Tile and stone adhesives are the most commonly used adhesive type in the residential end-user segment. Additionally, the residential segment is the largest and fastest-growing segment in the market studied.

The rising middle-class population, coupled with the increasing disposable incomes, has facilitated an expansion in the middle-class housing segment, thereby increasing the use of flooring adhesives.

According to the World Bank, the value of the global construction industry has increased from USD 22.36 trillion in 2020 to USD 27.18 in 2021.

The highest growth is expected to be registered in the Asia-Pacific region, owing to China and India's expanding housing construction markets. These two regions are expected to represent over 43.3% of the global middle class by 2030. The Government of India reduced the GST taxes for housing from 12% to 5%. This tax redemption may increase the construction market for middle-class housing.

Furthermore, in October 2021, Sao Paulo State Housing Union (Secovi-SP) recorded 5,555 new residential units sold in Sao Paulo, Brazil. The number is likely to rise, owing to the increase in consumer spending on residential housing units. Moreover, the growing trend for single-family housing in Brazil is likely support the residential construction industry in the upcoming period.

Mexico's housing starts and inventory levels reached a 10-year low due to a sharp cut in the federal housing subsidy program and the pandemic that triggered a severe recession. The Programa de Vivienda Social, or social housing program, had a budget increase of 179% to USD 200 million in 2021, thus, supporting construction spending. Moreover, accessible loan facilities and favorable mortgage schemes are expected to benefit residential construction in the country.

The low-cost housing segment is rising steadily, primarily due to government initiatives to provide affordable housing to the poor in urban and rural regions.

The consumption of flooring adhesives in constructing low-cost houses is comparatively less than other types of houses. Various countries across the world are providing shelter to refugees from other countries. Hence, governments offer temporary or permanent low-cost housing to refugees.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region dominates the global floor adhesives market share. With growing construction activities in countries such as China, India, and ASEAN Countries, the consumption of floor adhesives is increasing in the region.

The Chinese government has rolled out massive construction plans, including making provisions for the movement of 250 million people to its new megacities, over the next ten years, despite efforts to rebalance its economy to a more service-oriented form.

The National Bureau of Statistics of China reports that the market for construction works in China increased from CNY 23.27 trillion (USD 3.34 trillion) in 2020 to CNY 25.92 trillion (USD 3.72 trillion) in 2021.

The country has the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030.

Because of the government's increased attention to infrastructure projects and the predicted rapid rebound in demand for both residential and commercial segments, the construction sector was expected to grow by 10.7% in FY22. Hence, the growing construction activities in the country are expected to increase the demand for floor adhesives.

Various policies implemented by the Indian government, such as Smart City projects, Housing for All by 2022, etc., are expected to bring the needed impetus to the slowing construction industry. Moreover, recent policy reforms, such as the Real Estate Act, GST, and REITs, are expected to reduce approval delays and strengthen the construction sector over the next few years.

According to statistical office data, construction orders won by South Korean builders in 2021 increased by double digits due to robust international demand. According to Statistics Korea, construction orders collected by local builders both at home and overseas totaled USD 245.9 billion in 2021, up by 31 trillion won from 2020.

Floor Adhesives Industry Overview

The global floor adhesives market is partially consolidated. The major players include Sika AG, MAPEI S.p.A, Arkema Group (Bostik SA), HB Fuller Company, and Dow.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Rapidly Growing Global Construction Industry

4.1.2 Versatility, Safety, and Ease of Application of Floor Adhesives

4.2 Restraints

4.2.1 Hazardous Health Effects Due to VOC Emissions

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION

5.1 Resin Type

5.1.1 Epoxy

5.1.2 Polyurethane

5.1.3 Acrylic

5.1.4 Vinyl

5.1.5 Other Resin Types

5.2 Technology

5.2.1 Water-borne

5.2.2 Solvent-borne

5.2.3 Other Technologies

5.3 Application

5.3.1 Tile & Stone

5.3.2 Carpet

5.3.3 Wood

5.3.4 Laminate

5.3.5 Resilent Flooring

5.3.6 Other Applications

5.4 End-user Industry

5.4.1 Residential

5.4.2 Commercial

5.4.3 Industrial

5.5 Geography

5.5.1 Asia-Pacific

5.5.1.1 China

5.5.1.2 India

5.5.1.3 Japan

5.5.1.4 South Korea

5.5.1.5 Rest of Asia-Pacific

5.5.2 North America

5.5.2.1 United States

5.5.2.2 Canada

5.5.2.3 Mexico

5.5.3 Europe

5.5.3.1 Germany

5.5.3.2 United Kingdom

5.5.3.3 France

5.5.3.4 Italy

5.5.3.5 Rest of Europe

5.5.4 South America

5.5.4.1 Brazil

5.5.4.2 Argentina

5.5.4.3 Rest of South America

5.5.5 Middle-East and Africa

5.5.5.1 Saudi Arabia

5.5.5.2 South Africa

5.5.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3M

6.4.2 Arkema Group (Bostik SA)

6.4.3 Ashland

6.4.4 Dow

6.4.5 Forbo Holding AG

6.4.6 H.B. Fuller Company

6.4.7 Henkel AG & Co. KGaA

6.4.8 Jowat SE

6.4.9 LATICRETE International Inc.

6.4.10 MAPEI SpA

6.4.11 Pidilite Industries Limited

6.4.12 Sika AG

6.4.13 Tesa SE

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Demand for Bio-based Floor Adhesives