India Contract Manufacturing Organization (CMO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1689696

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

인도의 수탁 제조 기관(CMO) 시장 규모는 2024년에 225억 1,000만 달러에 이르고 시장 추정·예측 기간(2024-2029년)의 CAGR은 14.67%를 나타내 2029년에는 446억 3,000만 달러에 달할 것으로 전망됩니다.

수탁 제조 기관(CMO)은 계약에 근거하여 의약품 개발·제조 서비스를 제약산업에 기재하고 있습니다.

주요 하이라이트

CMO는 엄격한 규제를 준수하며, 숙련된 노동력, 최첨단 제조시설, 비용대비 효과가 높은 서비스 포트폴리오를 자랑합니다. 위치를 구축하는 것이 요구되고 있습니다.그 결과, 제품 출시의 조기화, 가격 압력의 증가, CMO가 제공하는 이점(타임라인의 단축, 경쟁 코스트로 고품질의 제품)등이, 주요 시장 성장 촉진요인이 되고 있습니다.

인도의 제약 산업은 제네릭 의약품, OTC 의약품, 백신, API, 연구·제조 수탁, 바이오시밀러, 생물 제제 등의 중요한 부문을 포함하고 있습니다.

세계 백신 생산량의 60%를 차지하는 인도는 세계보건기구(WHO)의 디프테리아·백일해·파상풍(DPT) 백신과 카르메트·게린균(BCG) 백신 수요 40-70%를 채우고, 홍역 백신의 점유율도 90%로 압도적입니다.

2023년 인도 정부는 중앙의약품 표준관리기구(Central Drugs Standard Control) Organization)은 다양한 유전성 질환을 대상으로 하는 21가지 신약을 허가했습니다.

그러나 과제도 산적하고 있습니다.정부의 규제가 엄격하고, 특정 지역에 있어서의 저분자 의약품이나 생물 제제의 승인이 감소하고 있기 때문에 시장의 성장이 저해될 가능성이 있습니다. 또한, 소규모의 CDMO는 첨단 기술이 없기 때문에 에러 리스크의 고조에 직면합니다.

인도의 수탁 제조 기관(CMO) 시장 동향

주요 제약 기업에 의한 아웃소싱량 증가

인도 제약 공업 협회(IDMA)는 신흥국 시장에서의 비용 상승과 규제 강화의 압력으로 세계 제약 기업은 연구 개발·제조의 사내 능력을 삭감할 수밖에 없습니다고 지적했습니다., 수탁 제조, 연구 서비스, 개발 도상국에서의 연구나 임상 검사의 아웃소싱에 점점 눈을 돌리게 되어 있습니다. 또한, 유럽의 제조 시설의 노후화에 의해 기업은 연구·제조 업무를 인도에 변화하고 있습니다.

생물 제제 API(API)의 개발은 기술적으로 어렵고 자본 집약적이기 때문에 제조 비용은 기존의 의약품보다 크게 높아집니다. 산에 유래하는 것입니다 생물 제제의 높은 가치와 이익을 인식해, 의약품 수탁 제조 기관(CMO)은 능력의 확대에 다액의 투자를 실시했습니다.그러나, 제약 회사는 제조에의 직접 투자보다 공급의 확보를 우선하고 있습니다.

제약 섹터에서의 아웃소싱 증가 동향은 제조 수탁이 밸류체인의 중요한 구성 요소가 됨으로써 성공하는 파트너십에 대한 길을 열고 있습니다.

인도 연방 예산에 따르면 2020년 제약 산업의 예산 배분은 33억 4,000만 루피(약 4,000만 달러)였습니다.

미국 FDA 인가의 제조 시설이 100 이상 있어, 그 수는 증가의 일도를 추적하고 있습니다.

API(API)·중간체 부문이 성장을 이룬다.

API의 제조는 최근 몇 년간 일관되게 증가하고 있습니다. 앞으로도 특허 만료이 예상되고 세계 제약 생산 능력의 대폭적인 증가가 예상되므로 API는 꾸준히 증가할 것으로 예상됩니다.

게다가 의료부문에 있어서의 인도 정부에 의한 이니셔티브 증가, 생물 제제의 기술 혁신, 암이나 노화 관련 질환 증가는 API 제조 산업의 확대를 뒷받침하는 중요한 이유의 일부에 지나지 않습니다.또, 의약품의 연구 개발의 확대, 만성 질환률의 상승, 제네릭 의약품의 관련성 증가, 바이오의약품의 사용량

인도의 제약산업은 제제의 기초원료가 되는 의약품 유효성분인 다양한 API을 생산하고 있습니다. 또한 인도는 500개 이상의 API을 제조하고 60개의 치료 카테고리에서 6만개의 제약을 제조하고 있기 때문에 의약품 API(API)의 전문 지식도 가지고 있습니다.

인도는 또한 제약 기업에 대한 투자를 장려하고 완전 소유 또는 합작 시설을 설립함으로써 국내 수탁 제조 기관(CMO) 시장 확대로 이익을 얻고 있습니다. 2023년 4월 기준 인도의 의약품 수출 분포에 대한 인베스트 인디아의 데이터에 따르면 제제 및 생물학적 제제가 73.31%로 1위를 차지했고, 벌크 의약품, 중간체 및 기타 성분이 그 뒤를 이었습니다.

제네릭 의약품 생산과 수출에 중요한 역할을 담당하는 인도는 중국에 대한 의존에 경계감을 강화하고 있습니다. 국내 생산을 강화하기 위해 인도 정부는 몇 가지 시책을 시작했습니다. Medicare, Gujarat Themis, Solara Active Pharma 등 주요 API 제조업체의 주가를 크게 상승 시켰습니다.

인도의 수탁 제조 기관(CMO) 산업 개요

수탁 제조 기관(CMO)은 제약회사와 바이오테크놀러지 기업을 위한 제조서비스를 제공합니다.

인도의 의약품 수탁 제조 기관(CMO) 시장은 세분화되어 있으며 주요 공급업체가 큰 시장 점유율을 차지하고 있습니다. Limited, Cipla Ltd. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

생태계 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁의 강도

제5장 시장 역학

시장 성장 촉진요인

상대적으로 저렴한 비용으로 숙련된 노동력 이용 가능

대기업 제약 기업에 의한 아웃소싱량의 지속적 증가

아시아태평양의 대규모 시장에 대한 접근이라는 지리적 우위

시장 성장 억제요인

정부의 엄격한 규제와, 국내의 특정 지역에 있어서 다수의 저분자 화합물과 생물 제제 승인 감소

세계의 의약품 CMO 산업 개요와 인도 시장에서 확인된 주요 단서

아시아태평양의 주요 시장 개요

마하라슈트라주와 테랑가나주 CMO 시설의 주요 핫스팟

인도의 CMO 산업에서 최근 개인 자금 투자

제6장 시장 세분화

서비스 유형별

API 및 중간체

완성된 용량

고체

액체

반고체 및 주사제

제7장 인도의 CMO 산업에 대한 전략적 제안

인도는 특히 주사제 부문에서 CMO 시설의 설립을 계획하는 신규 공급업체에게 주로 국내 수요와 제네릭 의약품의 성장에 의해 계속 높은 제안력을 유지

비용 우위성과 인재 풀 액세스

약사 승인 파이프라인과 베이스 케이스 시나리오

인도에서의 잠재적 M&A 대상의 분석

제8장 경쟁 구도

기업 프로파일

Dr. Reddy's Laboratories

Cadila Healthcare Limited

MSN Laboratories Pvt Ltd

Viatris Inc(Mylan Laboratories Ltd)

Medipaams India Pvt Ltd

Cipla Ltd.

Eisai Pharmaceuticals India Pvt Ltd

Delwis Healthcare Pvt Ltd

Maxheal Pharmaceuticals India Ltd

Rhydburg Pharmaceuticals Ltd

Theon Pharmaceuticals Limited

BDR Pharmaceuticals International

Akums Drugs and Pharmaceuticals Limited

Wockhardt Limited

Unichem Laboratories Ltd

Ciron Drugs & Pharmaceuticals Pvt Ltd

제9장 시장 전망

KTH

영문 목차

영문목차

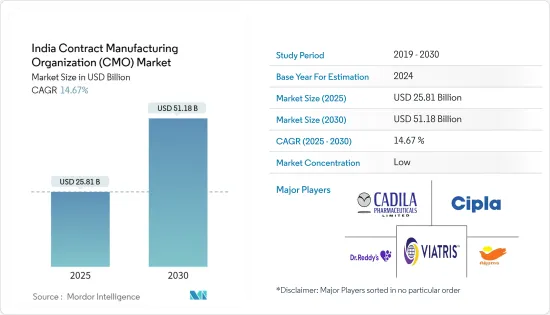

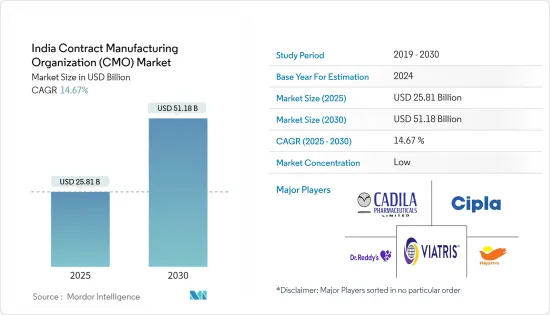

The India CMO Market size is estimated at USD 22.51 billion in 2024, and is expected to reach USD 44.63 billion by 2029, at a CAGR of 14.67% during the forecast period (2024-2029).

Contract manufacturing organizations (CMOs) provide drug development and manufacturing services to the pharmaceutical industry under contractual agreements. With a rising demand for injectable drugs, especially in cancer research, the contract manufacturing market is set to expand. Injectable drugs promise higher returns than other formulations and demonstrate superior therapeutic efficiency.

Key Highlights

CMOs adhere to stringent regulations and boast a skilled workforce, cutting-edge manufacturing facilities, and a cost-effective service portfolio. Heightened competition in the pharmaceutical sector underscores the urgency of swiftly launching products, aiming for a pioneering market position. Consequently, the push for earlier product launches, mounting pricing pressures, and the advantages offered by CMOs-like reduced timelines and high-quality products at competitive costs-serve as primary market drivers.

The Indian pharmaceutical landscape encompasses significant segments, including generic drugs, OTC medicines, vaccines, bulk drugs, contract research and manufacturing, biosimilars, and biologics. Notably, India stands out as a leading supplier of affordable vaccines.

Boasting 60% of the global vaccine production, India meets 40-70% of the World Health Organization's (WHO) demand for diphtheria, pertussis, and tetanus (DPT) and Bacillus Calmette-Guerin (BCG) vaccines, alongside a dominant 90% share for the measles vaccine. Such vast production capabilities position India as a potential growth driver for the studied market.

In 2023, the Indian government, as per the Central Drugs Standard Control Organization, greenlit 21 new drugs targeting various genetic diseases. This move paves the way for local players to establish new facilities, addressing the surging medicine demand. Additionally, India plays a pivotal role as a pharmaceutical exporter, with the U.S. notably relying on Indian imports and establishing plants there.

However, challenges loom on the horizon. Stringent government regulations and declining approvals for small molecules and biologics in specific regions could stifle market growth. Moreover, smaller CDMOs face heightened error risks due to a lack of advanced technology. Concerns over subpar quality and pricing challenges further complicate market expansion efforts.

India CMO Market Trends

Rise in Outsourcing Volume by Big Pharma Companies

The Indian Drug Manufacturers Association (IDMA) highlighted that rising costs and regulatory pressures in developed markets are compelling global pharmaceutical companies to reduce their internal capacities in research, development, and manufacturing. Instead, these companies are increasingly turning to contract manufacturing, research services, and outsourcing of research and clinical trials in developing nations. Additionally, ageing manufacturing facilities in Europe have led companies to shift their research and manufacturing operations to India.

Developing a biological Active Pharmaceutical Ingredient (API) is a technically challenging and capital-intensive, making its production cost significantly higher than conventional drugs. Notably, around 75% of the revenue from outsourcing biologics is derived from API production. Recognizing the high value and margins associated with biologic drugs, Contract Manufacturing Organizations (CMOs) heavily invest in expanding their capacities. However, pharmaceutical companies prioritize supply security over direct investments in manufacturing.

The trend of rising outsourcing in the pharmaceutical sector is paving the way for successful partnerships, with contract manufacturing becoming a vital component of their value chains. The market is witnessing substantial growth, driven by an increasing number of large pharmaceutical companies in India seeking to outsource products domestically.

As per the Union Budget of India, the pharmaceutical industry's budget allocation in 2020 was INR 3.34 billion (approximately USD 0.04 billion). This allocation was projected to surge to INR 40.9 billion (around USD 0.49 billion) by 2024. The global market is expanding, largely due to the cost-effective resources available in developing nations like India.

India stands out as a favored destination for CMOs, boasting over 100 US FDA-approved manufacturing facilities, a number that's on the rise. The robust presence of major players like Zydus Cadila and LUPIN further strengthens the country's pharmaceutical landscape.

The Active Pharmaceutical Ingredient (API) and Intermediates Segment to Witness Growth

The manufacturing of APIs has consistently increased over the past few years. This will continue to rise steadily, with further patent expiries expected in the future and a significant increase in global generic production capacities. Most businesses in the industry emphasize creating biological APIs and boosting API production.

Furthermore, increased initiatives by the Indian government in the healthcare field, biologics innovation, and an increase in cancer and age-related disorders are just a few of the vital reasons propelling the expansion of the API manufacturing industry. The expansion could also be due to expanding R&D on medication, rising chronic illness rates, growing generic relevance, and rising biopharmaceutical usage.

The Indian pharmaceutical industry produces a variety of bulk pharmaceuticals, which are active pharmaceutical ingredients that serve as the basic raw materials for formulations. Formulations comprise the remaining four-fifths of the industry's output, with bulk pharmaceuticals making up about one-fifth. The nation also possesses expertise in active pharmaceutical ingredients (APIs), as it is the manufacturer of more than 500 APIs and the source of 60,000 generic brands in 60 therapeutic categories.

India also benefits from expanding the domestic CMO market by encouraging investments in pharmaceutical businesses to establish wholly-owned or joint venture facilities. According to the data by Invest India on the distribution of pharmaceutical exports from India as of April 2023, formulations and biologicals took the top position with 73.31%, followed by bulk drugs, intermediates, and other components. The cost structure in China and India has also diverged as China has become a more expensive outsourcing destination. Also, companies from the United States and Europe aim to diversify their supply chains, benefiting India.

India, a significant player in the production and export of generic medications, has grown wary of its reliance on China. To bolster domestic production, the Indian government has initiated several measures. Responding to the stark realization of India's heavy dependence on Chinese imports, the government unveiled a substantial USD 400 million grant to bolster the country's API production. This move triggered a significant surge in the stock prices of key API players, including Lasa Supergenerics, Shilpa Medicare, Gujarat Themis, and Solara Active Pharma.

India CMO Industry Overview

Contract manufacturing organizations (CMOs) offer production services tailored for pharmaceutical and biotechnology firms. Acting on behalf of these entities, CMOs produce drugs, medicines, and therapies. They take a developed drug formula and scale production based on the client's demand. CMOs prioritize safety, consistency, and adherence to regulatory standards in their production processes.

The Indian contract manufacturing organization (CMO) market is fragmented, with the top vendors accounting for a significant market share. Apart from these major players, several players in the market are investing in innovations and partnerships to gain an increased market share. Therefore, the intensity of competitive rivalry is high. The key players are Dr Reddy's Laboratories, Cadila Pharmaceuticals Limited, and Cipla Ltd.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Ecosystem Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Availability of Skilled Labor at Relatively Lower Cost

5.1.2 Sustained Increase in Outsourcing Volumes by Big Pharma Companies

5.1.3 Geographical Advantage in the Form of Access to Large Markets in the APAC Region

5.2 Market Restraint

5.2.1 The Existence of Stringent Government Restrictions and a Decrease in the Approval of Numerous Small Molecules and Biologics in Specific Regions of the Nation

5.3 Overview of the Global Pharmaceutical CMO Industry and Major Cues Identified in the Indian Market

5.4 Overview of Major Markets in Asia-Pacific

5.5 Major Hotspots for CMO Facilities in Maharashtra and Telangana

5.6 Recent Private Equity Investments in the CMO Industry in India

6 MARKET SEGMENTATION

6.1 By Service Type

6.1.1 API and Intermediates

6.1.2 Finished Dose

6.1.2.1 Solids

6.1.2.2 Liquids

6.1.2.3 Semi-solids and Injectables

7 STRATEGIC RECOMMENDATIONS ON INDIA CMO INDUSTRY

7.1 India Remains a High Proposition for New Vendors Planning to Set Up Their CMO Facilities, Specifically in the Injectables Domain, Mainly Due to Growth in Domestic Demand and Generic Drugs

7.2 Cost Advantages and Access to Talent Pool

7.3 Regulatory Approval Pipeline and Base Case Scenarios