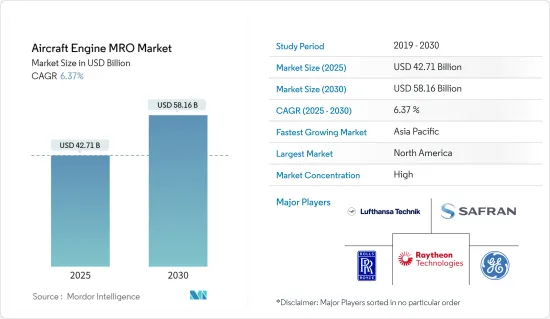

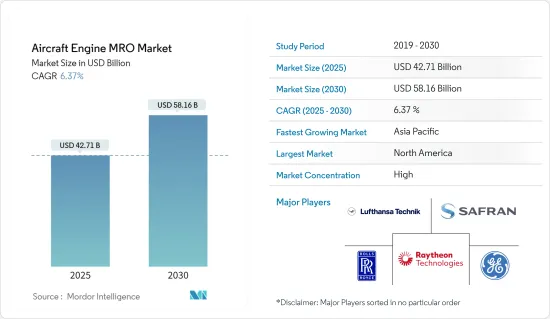

항공기 엔진 MRO 시장 규모는 2025년에 427억 1,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 6.37%로 성장할 전망이며, 2030년에는 581억 6,000만 달러에 달할 것으로 예측됩니다.

COVID-19 팬데믹이 항공기 엔진 MRO 시장에 미치는 영향은 큽니다. 대량의 항공기가 보관되고 가동률이 저하된 결과 항공기 엔진 MRO 수요는 2020년에 크게 떨어졌습니다. 그러나 2021년에는 항공 산업은 완만한 회복을 보이기 시작했고 여객 수와 항공기 이동이 증가했습니다. 이로 인해 항공기의 정비, 수리, 오버홀 활동의 수요가 증가했습니다.

항공사와 군의 급속한 기체 확대 계획은 예측 기간 동안 항공기 엔진 MRO 시장의 성장을 더욱 밀어올릴 것으로 예상됩니다.

일부 국가에서는 방위비 부족으로 노후화된 군용기의 서비스 수명을 연장할 계획이 있기 때문에 군용기의 노후화가 큰 수요를 초래할 수 있습니다.

새로운 항공기에 새로운 세대 엔진을 도입하면 항공기 엔진의 추가 MRO 수요가 증가할 것으로 예상됩니다. 신형 엔진은 구형기보다 더 비싼 재료가 필요합니다.

엔진 MRO의 진출기업별로, 전반적인 유지보수 프로세스의 효율성을 높이고, 전체적인 턴어라운드 시간을 단축하며, 안전성을 향상시키기 위해서, 유지관리 활동을 디지털화 및 자동화하는 첨단 기술의 도입은 향후 수년간 시장 성장을 뒷받침할 것으로 예상됩니다.

민간 항공 부문은 현재 가장 높은 시장 점유율을 차지하고 있으며 예측 기간 동안에도 그 우위성은 계속될 것으로 예상됩니다. 이것은, 군용 항공에 비해 민간 항공은 보유기수가 많은 것, 일반 항공에 비해 엔진의 유지 보수 비용이 비싼 것이 주요 이유입니다. 최근 항공사와 MRO 서비스 프로바이더 간에 항공기 엔진 유지 보수에 관한 몇 가지 새로운 계약이 체결되었습니다. 예를 들어 2021년 11월 SR Technics는 Vietjet Air와 Vietjet의 Airbus A320과 Airbus A321에 탑재된 CFM56-5B 엔진의 MRO 서비스를 제공하는 각서를 체결했습니다. 이 계약은 1억 5,000만 달러에 체결되었습니다. 이 계약에서는 이 회사는 엔진 유지 보수, 부품 요건, 수리, 기술, 훈련 서비스를 제공할 예정입니다. 이 회사는 Vietjet와 SR Technics의 합작 사업으로 새로운 항공 훈련 센터를 설립할 예정입니다.

마찬가지로 MRO 서비스 제공 업체는 비즈니스 엔진 MRO 서비스에 대한 수요 증가에 대응하기 위해 다양한 국가에서의 존재감을 확대하고 있습니다. 이 점에 관해서, S7 Technics는 2021년 9월, 쉐레메치예보 공항(모스크바)에 CFM56-5B와 -7B 엔진과 Honeywell131-9A/9B 보조 동력 장치(APU)의 오버홀을 실시하는 새로운 엔진 정비 공장을 개설할 계획을 발표했습니다. 새 공장의 정비 능력은 연간 최대 100대의 APU와 최대 42대의 엔진에 이를 전망입니다.

이러한 민간 항공사와의 여러 서비스 제공업체와의 제휴는 항공기 엔진의 내공성과 비행의 안전성을 유지하기 위한 지속적인 서비스로 인해 예측 기간 중에도 오랫동안 지속되고 있습니다. 이러한 파트너십을 통해 예측 기간 동안 민간 부문이 가장 높은 시장 점유율로 시장을 선도할 것으로 예상됩니다.

아시아태평양은 지난 10년간 항공기 보유 대수가 크게 증가하여 엔진 MRO 서비스에 대한 수요가 높아지고 예측 기간 동안 시장을 선도할 것으로 예상됩니다. 그 결과 미국과 유럽의 여러 MRO 서비스 프로바이더가 이 지역에 유지보수 시설을 설치하게 되었습니다. 게다가 몇몇 항공사는 해외 유지 보수 비용을 절감하기 위해 엔진 MRO 서비스 제공 업체와 제휴하여 사내 능력을 개발하고 있습니다. 예를 들면

중국국제항공은 2022년 9월 중국에 합작투자(JV)의 정비, 수리 및 오버홀(MRO) 시설을 설립한다고 발표했습니다. 새로운 시설인 Beijing Aero Engine Services Company Limited는 Rolls-Royce의 트렌트 700, 트렌트 XWB-84, 트렌트 1,000 항공 엔진의 MRO 지원을 기재하고 있습니다. 중국 국제 항공과 Rolls-Royce는, 각각 50%의 주식을 보유해, 약 26억 1,000만 위안(약 3억 7,820만 달러)의 계약을 맺었습니다.

이 지역에 대한 제조업체의 투자도 이 지역에서의 고수익, 나아가 시장의 성장을 견인하고 있습니다. 국제적인 대형 항공기 엔진 제조업체인 사프란은 2022년 2월 중국 쑤저우에 새로운 MRO 시설을 개설한다고 발표했습니다. 이 시설은 현재 설립 중이며 2022년 말까지 가동될 예정입니다. 이 회사가 소유한 5,200평방미터의 수리 스테이션은, 전략적인 약속에 도움이 되어, 중동과 인도에 걸쳐 있는 이 회사의 MRO 시설과 링크해, 이 회사를 세계의 주요 항공사의 MRO 서비스의 최적의 선택사항으로 만듭니다.

2022년 7월 Safran은 인도의 하이데라바드에 최대 2억 달러를 투자하여 회사 최대 MRO 시설을 설립하는 것도 발표했습니다. 이 시설은 연간 300건의 엔진 공장 방문에 대응할 수 있으며, 특히 인도 시장을 독점하는 CFM56, Leap 1A, Leap 1B 엔진을 지원합니다. 이 대규모 시설은 Safran의 아시아 엔진 고객을 위한 MRO 시설로도 사용될 예정입니다. 이러한 몇 가지 투자, 정부의 장려, 여객 유입의 잠재적인 증가로 예측 기간 동안 아시아 태평양에서 시장은 큰 성장률을 보일 것으로 기대되고 있습니다.

항공기 엔진 MRO 시장의 주요 기업은 Lufthansa Technik, Rolls-Royce Holding PLC, Raytheon Technologies Corporation, General Electric Company, Safran SA입니다. 주요 엔진 MRO 공급자들은 엔진 MRO 고객을 늘리기 위해 장기적인 파트너십을 맺거나 조인트 벤처를 형성하고 있습니다. 예를 들어, 2022년 6월, ST Engineering은 이 회사의 상용 항공 우주 사업이, 세계 유수의 항공 우주 엔진 메이커인 Safran Aircraft Engines와, ST Engineering이 CFM56-5B와 -7B 엔진의 엔진 유지보수(공장 방문) 오프로드를 제공하기 위한 5년 계약을 체결했다고 발표했습니다. 이 다년 계약으로 ST Engineering과 Safran Aircraft Engines는 항공 여행이 팬데믹에서 점차 회복됨에 따라 예측되는 엔진 MRO 활동 증가에 대응할 수 있게 될 수 있습니다. 경제적 안정성이라는 점에서는 시장 내의 참가 기업에 있어서 헤아릴 수 없는 이점이 있음에도 불구하고, 군이나 민간 항공사와의 기존 참가 기업의 장기 계약은, 신규 참가 기업의 장벽이 될 가능성이 있습니다.

The Aircraft Engine MRO Market size is estimated at USD 42.71 billion in 2025, and is expected to reach USD 58.16 billion by 2030, at a CAGR of 6.37% during the forecast period (2025-2030).

The impact of the COVID-19 pandemic on the aircraft engine MRO market has been significant. As a result of a large number of stored aircraft and lower utilization, the aircraft engine MRO demand significantly dropped in 2020. However, in 2021, aviation began to witness a gradual recovery, leading to increased passenger traffic and aircraft movements. This has led to an increase in demand for aircraft maintenance, repair, and overhaul activities.

The rapid fleet expansion plans of the airlines and military forces are anticipated to boost further the aircraft engine MRO market growth during the forecast period.

The aging military aircraft fleet in some countries may generate significant demand, as some have plans to extend the service life of these aging aircraft due to a lack of defense funding.

The introduction of newer generation engines in new aircraft is anticipated to increase the aircraft engine further MRO demand. The new engines will have more expensive material requirements than the older aircraft.

The introduction of advanced technologies that will digitize and automate maintenance activities to increase overall maintenance process efficiency, reduce the overall turnaround time, and improve safety by the engine MRO players is anticipated to boost the market's growth in the coming years.

The commercial aviation segment currently has the highest market share, and it is expected to continue its dominance during the forecast period. This is majorly due to the large fleet of commercial aviation compared to military aviation and the high cost of engine maintenance cost compared to general aviation. In recent years, several new contracts have been signed for the maintenance of aircraft engines between airlines and MRO service providers. For instance, in November 2021, SR Technics signed a Memorandum of Understanding (MoU) with Vietjet Air to provide MRO services for CFM56-5B engines onboard Vietjet's Airbus A320 and Airbus A321 aircraft fleet. The agreement was signed worth USD 150 million. Under the contract, the company is expected to provide engine maintenance, component requirements, repair, technical, and training services. It will set up a new Aviation training center as a joint venture between Vietjet and SR Technics.

Similarly, MRO service providers are expanding their presence in various countries to cater to the growing demand for commercial engine MRO services. In this regard, in September 2021, S7 Technics announced its plan to open a new engine maintenance facility at Sheremetyevo airport (Moscow) to overhaul CFM56-5B and -7B engines and Honeywell 131-9A/9B auxiliary power units (APU). The maintenance capacity of the new shop is expected to reach up to 100 APUs and up to 42 engines per year.

Multiple such service provider partnerships with commercial carriers are extending long into the forecast period for continued service of aircraft engines to be airworthy and safe for flight. Due to these partnerships, the commercial segment of the market is expected to lead the market with the highest market share during the forecast period.

Asia-Pacific has experienced significant growth in the total aircraft fleet over the past decade, which has increased the demand for engine MRO services and is expected to lead the market during the forecast period. This has resulted in several MRO service providers from the United States and Europe establishing their maintenance facilities in this region. Furthermore, several airlines have partnered with engine MRO service providers to reduce overseas maintenance costs to develop in-house capabilities. For instance,

Air China, in September 2022, announced that they are entering a Joint Venture (JV) maintenance, repair, and overhaul (MRO) facility in China. The new facility, Beijing Aero Engine Services Company Limited, will provide MRO support on the Rolls-Royce Trent 700, Trent XWB-84, and Trent 1000 aero engines. Air China and Rolls-Royce each hold 50% of the shares in the joint venture with a contract, accounting for about 2.61 billion yuan (about USD 378.2 million).

Manufacturer investments in the region are also driving high revenues and, consequently, market growth in the region. Safran - a large international aircraft engine manufacturer, in February 2022 announced the opening of a new MRO facility in Suzhou, China. The facility is being set up and is expected to be operational by the end of 2022. The company-owned 5,200 sq meter repair station helps it in strategic commitments, linking it to the company's MRO facilities across the Middle-Eastern and Indian facilities, making the company an optimal choice for MRO services for major airlines globally.

In July 2022, Safran also announced that it would invest up to USD 200 Million to set up its biggest MRO facility in Hyderabad, India. The facility would be capable of handling up to 300 engine shop visits annually, especially catering to the CFM56, Leap 1A, and Leap 1B engines that dominate the Indian market. This large facility is also expected to be used as an MRO facility for Safran's Asian engine customers. Due to several such investments, government incentivization, and the potential increase in passenger influx, the market is expected to witness significant growth rates in the Asian-Pacific region during the forecast period.

The prominent players in the aircraft engine MRO market are Lufthansa Technik, Rolls-Royce Holding PLC, Raytheon Technologies Corporation, General Electric Company, and Safran SA. The major engine MRO providers are entering into long-term partnerships or forming joint ventures to grow their engine MRO customers. For instance, in June 2022, ST Engineering announced that their Commercial Aerospace business had signed a five-year agreement with Safran Aircraft Engines, a global-leading aerospace engine manufacturer, for ST Engineering to provide engine maintenance (shop visit) offload for the CFM56-5B and -7B engines. This multi-year agreement may allow ST Engineering and Safran Aircraft Engines to meet the forecasted rise of engine MRO activities as air travel gradually recovers from the pandemic. Despite being an immense advantage for the players within the market in terms of economic stability, the long-term contracts of the established players with the armed forces and commercial airlines may act as a barrier for new players to enter the market.