ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

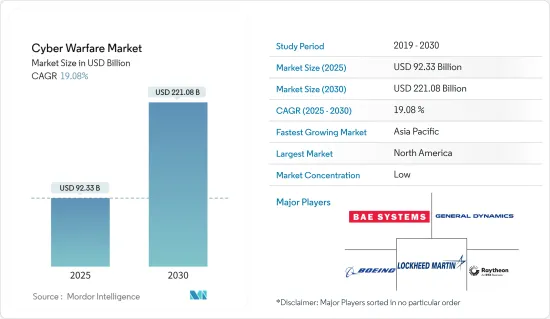

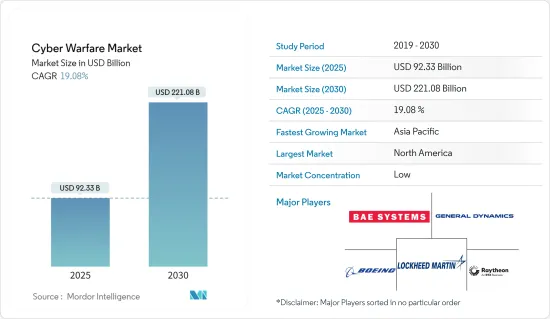

사이버 전쟁 시장 규모는 2025년에 923억 3,000만 달러, 2030년에는 2,210억 8,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 19.08%를 나타낼 전망입니다.

사이버 전쟁에는 사이버 공격, 스파이 활동, 파괴 공작 등의 공방이 포함됩니다. 전 세계적으로 사이버 공격의 수가 현저하게 증가하고 있습니다. 사이버 전쟁은 바이러스, 전자 메일 첨부 파일, 팝업 창, 인스턴트 메시지, 인터넷의 다른 형태의 사기 등 사이버 범죄자가 액세스할 수있는 모든 벡터를 사용합니다.

세계 사이버 공격 증가는 다양한 정부 및 민간 기업의 인터넷에 연결된 디지털 인프라에 손상을 줄 수 있으며, 사이버 전쟁 솔루션의 공격적 및 방어적 용도 모두에 대한 필요성을 높이고 시장 성장 기회를 창출하게 됩니다.

국제기구와 각국 정부는 미국과 인도 등 다양한 국가의 사이버 보안 능력을 향상시켜 국가 안보를 강화하는 것을 우선하고 있습니다. Center for Internet Security의 조사에 따르면 주정부와 지방정부에 대한 사이버 공격은 2022년에서 2023년에 걸쳐 증가했습니다. 이 센터에 따르면 악성코드 공격은 148% 증가했으며 랜섬웨어 사고는 2023년 첫 8개월 동안 51% 증가했습니다.

게다가 중국과 인도와 같은 신흥 국가들은 자국의 사이버 방어 능력을 높이는 전략을 취하고 있으며 시장의 성장을 지원하고 있습니다. 예를 들어, 인도는 2023년 2월, 2013년 이전 전략을 업데이트하여 '국가 사이버 보안 전략 2023'을 발표했습니다. 이 나라는 재무 및 법무 양성과 공동으로 국제 랜섬웨어 대책 태스크 포스를 설치했습니다.

그러나 사이버 전쟁 솔루션에 대한 수요 증가는 세계적으로 사이버 보안 전문가에 대한 수요를 높이고 있으며, 수요의 급격한 증가로 숙련된 사이버 보안 인력에 공백이 생겨 시장 성장에 과제가 되고 있습니다.

COVID-19는 세계적으로 기업에 큰 혼란을 가져왔습니다. COVID-19는 업무, 소매, 엔터테인먼트, 교육을 위한 인터넷 이용 증가로 인한 디지털 변혁에 힘입어 민간 기업 및 정부 기관에서 사이버 범죄 활동의 성장을 가속화하고 온라인 트래픽 급증을 촉진했습니다. 팬데믹 중 및 팬데믹 후 사이버 공격과 부정 행위 증가는 사이버 위험을 최소화하는 데 적용 할 수있는 사이버 전쟁 솔루션의 기회를 창출하고 팬데믹 후 시장을 활성화했습니다.

사이버 전쟁 시장 동향

방위가 최대의 최종 사용자 산업이 될 전망

사이버 전쟁 시장에서는 방위 분야가 큰 시장 점유율을 차지할 것으로 예상됩니다. 방위 산업은 국가 및 국가 프로그래머의 잠재적 위험을 완화하고 차단하기 위해 디지털 보안 단위에 많은 투자를 하고 있습니다. 저항 기술 혁신과 사물 인터넷(IoT)의 상승은 방위 산업에서 디지털 전투 프레임워크의 사용을 촉진하는 요소가 될 것으로 예상됩니다.

지적 재산의 도난이나 국가의 방어 시스템이나 능력의 감시 및 제어에 사용되는 시스템의 침해를 피하기 위해 사이버 보안 솔루션에 대한 투자가 크게 늘어나고 있습니다. 각국은 현대 방어의 진보에 대응하기 위해 무인 차량이나 극초음속 무기 등의 신기술을 개발해 왔습니다.

이러한 진보는 데이터와 연결성에 크게 의존하기 때문에 침해나 공격의 영향을 받기 쉽습니다. 방위 산업에서의 기술 발전은 국제 평화와 안보에 대한 기회이자 위험입니다. 따라서 각국은 중요한 정보를 보호하기 위해 사이버 전쟁 솔루션을 채택하고 대책 개발에 주력 할 필요성이 커지고 있습니다.

또한, 방어적 사이버 작전은 네트워크를 보호하기 위해 필요하지만, 세계 각국 정부는 군사 계획에서 공격적 사이버 작전(OCO)도 중시하고 있습니다. 2023년 4월 영국 정부는 국민 국가의 적대자의 위협 증가에 대한 사이버 대응을 조정했습니다. 이것은 2022년 12월에 발표된 최신 국가 사이버 전략(NCS)에 따른 것이었습니다. 국가 보호 보안 당국을 도입한 후, 정부는 공격적인 사이버 능력에 대해 발신하기로 결정했습니다. 이 나라의 국가 사이버군(NCF)은 비밀리에 공격적 사이버 작전을 실시하는 원칙을 공유했습니다.

게다가 지난 몇 년동안 각국의 방위비 증가는 사이버 전쟁 솔루션을 채택하기 위한 성장 가능성을 창출하고 있습니다. 예를 들어 SIPRI 데이터에 따르면 세계 군사비는 2017년 18억 달러에서 2023년 24억 4,000만 달러로 크게 증가했습니다.

북미는 향후 수년간 사이버 전쟁 솔루션을 채택하는 현저한 시장이 될 것으로 예상됩니다. 지난 수년간의 군사비의 대폭적인 상승과 함께, 주요 시장 벤더의 존재감이 크고, 이 지역의 방위 산업에 있어서의 사이버 전쟁 솔루션 채용의 성장 가능성을 나타내고 있습니다.

북미가 큰 시장 점유율을 차지할 전망

미국과 캐나다의 민간 조직에서의 디지털화 동향은 디지털 서비스를 사이버 공격에 노출시켜 이 지역의 디지털 인프라 취약성을 높여줍니다. 이 시나리오는 사이버 위협을 보호, 감지 및 방지하는 능력으로 북미에서 사이버 전쟁 솔루션을 채택하는 데 박차를 가할 것으로 보입니다.

지정학적 이유로 미국, 러시아, 중국의 세계 갈등은 사이버 전쟁 동향으로 미국의 IT 인프라와 기능에 대한 사이버 공격을 증가시키고 있습니다. 예를 들어, 2023년 6월 미국 정부 기관인 사이버 보안 인프라 보안청은 미국 연방 정부 기관이 러시아 사이버 범죄자에 의한 세계의 사이버 공격을 받고 해킹 캠페인으로 침입된 여러 연방 정부 기관 중 미국 에너지부가 피해를 입었습니다고 발표했습니다.

미국과 캐나다 정부는 사이버 공간에서 경쟁력을 높이기 위해 사이버 보안 방어와 공격을 강화하는 전략적 우선 순위에 투자하고 있습니다. 이는 사이버 전쟁 솔루션을 제공하는 전문 지식을 갖춘 제너럴 다이내믹스와 보잉과 같은 시장 역학 공급업체에게 북미 시장에서 비즈니스 기회를 창출할 수 있습니다.

캐나다 혁신과학경제개발부는 캐나다 사이버 보안 혁신 네트워크를 구축하기 위해 선정된 신청자들과 무상환 기여 협약을 체결하여 4년간(2021-22-2024-25) 8,000만 달러를 지원했습니다. 캐나다 정부는 이 나라의 고등교육기관, 민간기업 및 기타 파트너와 협력하여 캐나다의 사이버 보안 분야에서 R&D를 지원하고 혁신적인 사이버 보안 제품과 서비스의 성장을 가속화하고 예측 기간 동안 이 나라에서 사이버 전쟁 솔루션의 상업화를 촉진한다는 비전을 내세워 이 네트워크를 도입했습니다.

이 지역의 금융 부문은 증가하는 사이버 공격에 대항하기 위해 사이버 보안 강화 전략을 우선하고 있기 때문에 이 지역의 BFSI 부문은 북미 사이버 전쟁 시장 점유율에 크게 기여하고 있습니다. 게다가 미국 뉴욕주 금융서비스국(NYDFS)이 2023년에 제안한 4개의 사이버 보안법은 이 지역 금융 부문의 사이버 방어 메커니즘을 강화하는 것을 목표로 하며 시장 성장 기회를 창출할 것으로 보입니다.

사이버 전쟁 산업 개요

사이버 전쟁 시장은 매우 세분화되어 있으며 BAE Systems PLC, The Boeing Company, General Dynamic Corporation, Lockheed Martin Corporation, Raytheon Technologies Corporation 등 대기업이 존재합니다. 시장 업체는 제품 제공을 강화하고 경쟁 우위를 얻기 위하여 제휴 및 인수와 같은 전략을 채택합니다.

2023년 11월, BAE Systems Detica는 방어 등급의 사이버 보안 제품인 CyberReveal을 기업이 사내에서 사용할 수 있도록 상용 시장에 처음 투입했습니다. CyberReveal은 분석 및 조사 제품으로 기업의 귀중한 재산과 상업상의 기밀 정보를 사이버 범죄자에 의한 도난이나 침해로부터 보호하기 위한 인텔리전스를 제공합니다.

2023년 4월, 지멘스와 레오나르도는 산업, 석유, 가스 및 에너지 분야의 인프라에 사이버 보안 솔루션을 제공하는 MoU를 체결했습니다. 양사는 중요한 인프라의 자산, 기계, 절차를 감시 및 감독하는 인시던트나 사이버 공격에 대한 자동화·접속 시스템의 회복력에 주안을 둔 개입이 될 것이라고 말합니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 및 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

밸류체인 분석

시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

시장 성장 촉진요인

국가 안보에 대한 우려 증가

국방비 증가

시장의 과제

사이버전쟁 전문가 부족

제6장 시장 세분화

최종 사용자 산업별

방어

항공우주

BFSI

기업

전력 및 유틸리티

정부기관

기타 최종 사용자 산업

지역별

북미

유럽

아시아

호주 및 뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

BAE Systems PLC

The Boeing Company

General Dynamic Corporation

Lockheed Martin Corporation

Raytheon Technologies Corporation

Mandiant Inc.(fireeye Inc.)

Leonardo SpA

Booz Allen Hamilton Inc.

DXC Technology Company

Airbus SE

제8장 투자 분석

제9장 시장의 미래

SHW

영문 목차

영문목차

The Cyber Warfare Market size is estimated at USD 92.33 billion in 2025, and is expected to reach USD 221.08 billion by 2030, at a CAGR of 19.08% during the forecast period (2025-2030).

Cyberwarfare involves offensive and defensive operations, such as cyberattacks, espionage, and sabotage. The number of cyberattacks worldwide is increasing significantly. Cyberwarfare uses all vectors accessible to cybercriminals, including viruses, email attachments, pop-up windows, instant messages, and other forms of deception on the internet.

The growth in the number of cyberattacks worldwide has the potential to damage the internet-linked digital infrastructure of various government or private sector enterprises, raising the need for both offensive and defensive applications of cyber warfare solutions, which would create an opportunity for market growth.

International organizations and governments prioritize strengthening national security by increasing the cyber security capabilities of various countries, such as the United States and India, due to increased security challenges within cyberspace in recent years. According to a survey by the Center for Internet Security, cyberattacks on state and local governments increased from 2022 to 2023. The center found that malware attacks increased by 148%, while ransomware incidents were 51% more prominent during the first eight months of 2023.

Additionally, developing countries, such as China and India, have been strategizing to increase their countries' capabilities in cyber defense, supporting market growth. For instance, in February 2023, India planned to launch the National Cyber Security Strategy 2023 by updating the old strategy of 2013. The country has created an International Counter Ransomware Taskforce in collaboration with its finance and legal affairs ministries.

However, the increasing demand for cyber warfare solutions has increased the demand for cyber security professionals worldwide, which has created a gap in the skilled cyber security workforce due to the sudden rise in demand, challenging the market growth.

COVID-19 caused significant disruption to businesses on a global scale. It accelerated the growth of cyber criminal activities in private and government enterprises supported by digital transformation with the increase in internet use for work, retail, recreation, and education, driving a surge in online traffic. The increase in cyberattacks and fraud during and after the pandemic has created an opportunity for cyber warfare solutions due to their application in minimizing the cyber risks and fueled the market during the post-pandemic period.

Cyber Warfare Market Trends

Defense is Expected to be the Largest End-user Industry

The defense segment is expected to hold a significant market share in the cyber warfare market. The defense industry is investing heavily in digital security units to moderate and discourage potential risks from country and state programmers. The rise of innovations and the Internet of Things (IoT) in the resistance are expected to be the driving components for the use of the digital fighting framework in the defense industry.

There has been significant growth in investment in cybersecurity solutions to avoid theft of intellectual property and compromising systems that are used to monitor and control the country's defense systems and capabilities. Countries have developed new technologies, such as unmanned vehicles and hypersonic weapons, to keep pace with modern defense advancements.

These advancements are highly dependent on data and connectivity, making them susceptible to breaches and attacks. Technological advancements in the defense industry may present opportunities as well as risks for international peace and security. Thus, there is a growing necessity for countries to focus on developing countermeasures by adopting cyber warfare solutions to safeguard critical information.

Moreover, while defensive cyber operations are necessary to protect a network, governments worldwide also focus on offensive cyber operations (OCOs) in military planning. In April 2023, the UK government adjusted its cyber response to the growing threat of nation-state adversaries. This was in line with its latest National Cyber Strategy (NCS) published in December 2022. After introducing the National Protective Security Authority, the government decided to communicate about its offensive cyber capabilities. The National Cyber Force (NCF) of the country shared the principles under which it conducts covert offensive cyber operations.

Additionally, the increasing defense expenditure of various countries in the past few years has created growth potential for adopting cyber warfare solutions. For instance, according to the data from SIPRI, military spending worldwide significantly rose from USD 1.80 billion in 2017 to USD 2.44 billion in 2023.

North America is expected to be a prominent market for adopting cyber warfare solutions in the coming years. The significant presence of major market vendors, coupled with a substantial rise in military expenditure in the past few years, indicates growth potential for adopting cyber warfare solutions in the region's defense industry.

North America is Expected to Hold Significant Market Share

The digitalization trends in the public and private sector organizations of the United States and Canada are raising the vulnerability of the region's digital infrastructures by exposing digital services to cyberattacks. This scenario would fuel the adoption of cyber warfare solutions in North America due to their capability to protect, detect, and prevent cyber threats.

The global rivalry between the United States, Russia, and China for geo-political reasons has led to increased cyberattacks on the IT infrastructures and functions of the United States due to the trend of cyber wars. For instance, in June 2023, the Cybersecurity and Infrastructure Security Agency, a government-owned agency of the United States, stated that US federal government agencies were hit in a global cyberattack by Russian cybercriminals, and the US Department of Energy was victimized among the multiple federal agencies breached in the hacking campaign.

The governments of the United States and Canada are investing in their strategic priorities to strengthen their cyber security defense and offense to be competitive in cyberspace. This may create an opportunity for market vendors, such as General Dynamics and Boeing, in the North American market due to their expertise in providing cyber warfare solutions.

Innovation, Science and Economic Development Canada established a non-repayable contribution agreement with selected applicants to form a Cyber Security Innovation Network in Canada with USD 80 million over four years (2021-22 to 2024-25). The Canadian government introduced this network with a vision to support research and development in the Canadian cybersecurity space by collaborating with the country's post-secondary institutions, the private sector, and other partners to accelerate the growth of innovative cybersecurity products and services, fueling the commercialization of cyber warfare solutions in the country during the forecast period.

The BFSI sector of the region is significantly contributing to the market share of the North American cyber warfare market because financial sectors of the region have prioritized their strategy in strengthening cyber security to fight against the increasing number of cyber attacks. In addition, the four cyber security laws proposed in 2023 in the United States by the New York State Department of Financial Services (NYDFS) aim to strengthen the cyber defense mechanism of the region's financial sector, which would create an opportunity for market growth.

Cyber Warfare Industry Overview

The cyber warfare market is highly fragmented, with the presence of major players like BAE Systems PLC, The Boeing Company, General Dynamic Corporation, Lockheed Martin Corporation, and Raytheon Technologies Corporation. The players in the market are adopting strategies, such as partnerships and acquisitions, to enhance their product offerings and gain a competitive advantage.

In November 2023, BAE Systems Detica launched CyberReveal, its defense-grade cyber security product, to the commercial market for companies to use in-house for the first time. CyberReveal is an analytics and investigation product that provides companies with intelligence to protect their valuable property and sensitive commercial information from being stolen or compromised by cybercriminals.

In April 2023, Siemens and Leonardo signed an MoU to provide cybersecurity solutions for infrastructures in the industrial, oil and gas, and energy sectors. The companies stated that the intervention's primary focus would be on the resilience of the automation and connectivity systems against incidents and cyberattacks that monitor and oversee critical infrastructures' assets, machinery, and procedures.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Value Chain Analysis

4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Concerns Regarding National Security