북미의 HVAC 장비 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

North America HVAC Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1687783

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

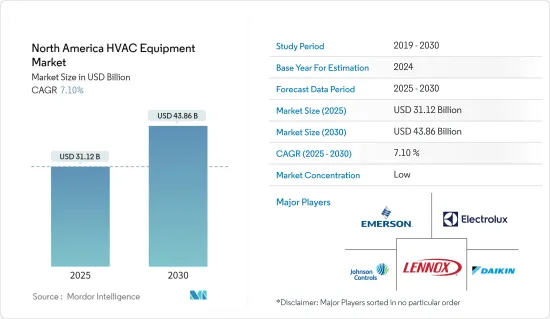

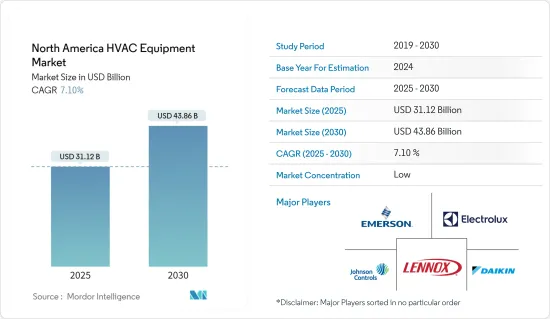

북미의 HVAC 장비 시장 규모는 2025년에 311억 2,000만 달러, 2030년에는 438억 6,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 7.1%를 나타낼 전망입니다.

가처분 소득 증가, 건설 활동의 급속한 확대, 기상 패턴의 변화가 조사 대상 시장의 성장을 이끌고 있습니다. 북미에서는 스마트홈과 스마트시티 프로그램의 도입이 크게 증가하고 있어 시장의 성장을 견인하고 있습니다.

주요 하이라이트

지속가능한 지역사회의 발전을 목적으로 하는 예산배분 증가라는 형태로 정부지원의 고조가 상업 및 공업건설 부문의 지속적인 성장에 기여하고 있을 가능성이 있습니다. 또한 건설 활동 증가, 급속한 도시화, 인프라 개혁은 HVAC 유닛 교체의 급증을 가져오고 HVAC 장비 시장을 견인하고 있습니다.

북미의 HVAC 장비 시장의 성장은 스마트 시스템에 대한 수요 증가와 사물 인터넷(IoT), 산업 자동화 시스템, 스마트 제조 및 인더스트리 4.0의 통합으로 이어집니다. 시장의 평균을 초과하는 성장의 대부분은 그린 빌딩 건설 활동의 활성화로 예측됩니다. 빠르게 성장하는 스마트 홈 시장은 HVAC 시스템 시장의 성장을 뒷받침할 것으로 예측됩니다.

그린 빌딩 건설 프로젝트는 이 지역의 HVAC 장비 시장 확대를 더욱 강화할 것입니다. 예를 들어, 2022년 2월 캐나다 그린빌딩 협의회(CAGBC)는 세계에서 사용되는 그린빌딩 인증 프로그램인 LEED(Leadership in Energy and Environmental Design)의 연간 상위 10개국가, 지역 목록에서 2021년에 이 나라가 세계 2위를 차지했다고 발표했습니다. 거주자의 건강과 에너지 소비에 대한 의식이 높아지면서 정부기관이 부과하는 기준을 충족시키는 공조장비의 설치는 그린빌딩 설계에서 중요한 기준이 되고 있습니다.

그러나 IEA와 미국 에너지부에 의하면, 전력 소비의 약 25-35%는 HVAC 시스템에 의한 것입니다. 이 출처에 따르면, 이 에너지 소비의 대부분(20%-60%)은 기생적 에너지 사용(냉난방의 이송에 사용되는 팬이나 펌프의 동력원으로 사용되는 에너지)이 기여하고 있습니다. 따라서, 집중형 공조 시스템은 유닛형 시스템보다(공조되는 공간의 단위 면적당 에너지 소비량이라는 점에서) 효율적임에도 불구하고 에너지 요금이 부담이 되고 있습니다.

제조업 전체의 고용이 부족합니다. 안타깝게도 냉난방 공조 업계도 예외는 아닙니다. 현재의 노동력 부족으로 인해 발생하든 아니든 시장의 성장을 저해할 수 있습니다

북미의 HVAC 장비 시장 동향

히트펌프가 크게 성장

히트 펌프가 차지하는 시장 점유율은 큰 것으로 예측됩니다. 기후 조건, 장비 편의성, 정부 세금 공제, 규제 등 다양한 요인으로 인해 히트 펌프 사용이 북미에서 꾸준히 증가하고 있습니다.

에너지 효율적인 제품을 채택하는 방향으로의 패러다임 시프트와 소비 지출 증가에 의해 미국의 주택용 히트 펌프 시장은 앞으로도 견고하게 확대할 것으로 보입니다. 사업환경은 탈탄소경제로의 진행에 의해 자극되고, 이는 법제화된 에너지 정책과 인센티브에 의해 지원될 것으로 보입니다. 노후화된 건물의 개수가 진행됨에 따라, 유연성과 쾌적성의 향상에 대한 수요가 높아질 것으로 예상됩니다. 이로 인해 업계는 더욱 역동적일 것으로 보입니다.

히트 펌프는 수열원, 공기 열원, 지중 열원 등의 유형으로 분류됩니다. 공기 열원 히트펌프(ASHP)는 전기를 흡수하고 주변 공기에서 열을 꺼내 섭씨 90도까지 온수를 생성합니다. 주변 공기에서 열을 꺼내기 때문에 공기가 차갑습니다. 따라서 온수와 냉기 모두에 대한 요구는 공기 열원 히트 펌프의 성장을 가속합니다.

게다가 북미의 많은 지역에서 한랭지용 히트펌프의 인기가 높아지고 있으며, 이것이 이 분야에서 큰 기술 혁신의 원동력이 되고 있습니다. 한랭지용 히트펌프는 섭씨 마이너스 25도까지의 조건 하에서 효율적으로 작동하도록 개발되고 있으며, 섭씨 마이너스 18도에서도 200% 이상의 효율을 유지하는 시스템도 있습니다.

2022년 6월, 미국(DOE)은 레녹스 인터내셔널이 미국 에너지부(DOE)의 주택용 한랭지 히트펌프 기술의 첫 파트너가 되었습니다고 발표했습니다.

미국이 큰 시장 점유율을 차지

미국은 필수 장비 시장 중 하나이며 안정적인 성장률을 보여줍니다. 건설 활동의 활성화, 고효율 시스템의 가용성, 극단적 인 기후 조건이 시설 전체에 시스템을 설치하는 데 유리합니다. 게다가 경력, 에머슨 일렉트릭사 등의 주요 제조업체의 존재가 향후 북미 시장의 성장을 보완하고 있습니다.

또한 사물인터넷(IoT)의 통합에 따라 여러 업체들이 스마트 난방 및 공조 및 환기 시스템 제공을 시작하여 미국 전체 시장 성장을 가속하고 있습니다.

지속가능한 미래를 확보하기 위해 미국 에너지부(DOE)는 국가 전체의 에너지 효율 기준 개선에 많은 투자를 하고 있습니다. DOE는 환경, 에너지, 원자력 문제에 대한 과학기술의 해결책을 찾는 것으로 미국의 안전과 번영을 확실히 하고 싶다고 생각합니다.

게다가 에너지정보국(EIA)의 주택에너지소비조사(RECS)에 따르면 주로 거주하는 미국의 주택 7,600만호(전체의 64%)가 센트럴 공조장비를 사용하고 있는 것으로 추정되고 있습니다. 약 1,300만 가구(11%)가 냉난방에 히트 펌프를 사용하고 있습니다. 2023년까지 미국에서 판매되는 모든 새로운 주거용 에어컨 및 공기 열원 히트 펌프 시스템은 최신 에너지 효율 기준을 충족해야 하며 HVAC 장비의 성장을 촉진할 것입니다.

또한 미국 인구조사국에 따르면 2022년 6월 미국의 신축주택건설건수는 약 136만건이었습니다. 2022년 6월 미국의 개인 소유 신축 주택 호수는 약 155만 호였습니다. 이것은 또한 예측 기간 동안 이 나라에서 히트 펌프의 큰 새로운 수요를 생성할 것으로 예상됩니다.

북미의 HVAC 장비 산업 개요

북미의 HVAC 장비 시장 경쟁 기업간 경쟁 관계는 높고, 다이킨, 경력, 레녹스 등의 유명 벤더가 각 분야에서 주요 시장 점유율을 차지하고 확립된 유통망을 이용하고 있습니다. HVAC 장비 산업은 가장 큰 시장이기 때문에 시장 점유율에 타협하지 않고 많은 수의 주요 공급업체가 존재할 수 있습니다. 그러나 각 벤더는 특히 냉난방 분야에서 더 큰 점유율을 얻기 위해 치열한 경쟁을 벌이고 있습니다.

2023년 2월 - Lenox는 Enlight와 Xion 제품 라인을 도입하여 패키지형 옥상 유닛의 종합적인 구색을 강화했습니다. 이 회사의 Enlight 제품군은 환경에 미치는 영향을 최소화하고 효율성을 극대화하기 위한 것입니다.

2022년 10월-Carrier Corporation은 북미에서 AquaEdge19DV 수냉 터보 냉동기의 용량 확대를 선언. AquaEdge19DV는 상업용 고층 빌딩, 복합 용도 빌딩, 대규모 제조 시설 및 의료기관과 같은 대용량 수요에 부응하기 위해 최대 1,150톤까지 공급할 수 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 및 지원

목차

제1장 서론

조사의 상정과 시장의 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 역학

시장 성장 촉진요인

주택 및 비주택 유저 증가

시장 성장 억제요인

HVAC 장비의 높은 에너지 소비량

제6장 시장 세분화

장비별

공조장비

난방장비

히트 펌프

제습기 및 가습기

최종 사용자별

주택

산업

상업

국가별

미국

캐나다

제7장 경쟁 구도

기업 프로파일

Johnson Controls International PLC

Daikin Industries Ltd

Lennox International Inc.

Electrolux AB

Emerson Electric Co.

Carrier Corporation

Rheem Manufacturing Company Inc.

Uponor Corp.

Ingersoll Rand Inc.(Trane Inc.)

Nortek Global HVAC, LLC

제8장 투자 분석

제9장 시장의 미래

SHW

영문 목차

영문목차

The North America HVAC Equipment Market size is estimated at USD 31.12 billion in 2025, and is expected to reach USD 43.86 billion by 2030, at a CAGR of 7.1% during the forecast period (2025-2030).

Increasing disposable income, rapidly expanding construction activity, and changing weather patterns are driving the growth of the market studied. North America is witnessing a significant increase in the implementation of smart home and smart city programs, driving the market's growth.

Key Highlights

Growing government support, in the form of higher budget allocations designed to increase sustainable community development, may contribute to the continually growing commercial and industrial construction sectors. Besides, increased construction activities, rapid urbanization, and infrastructural reforms result in an upsurge in HVAC unit replacements, thus driving the HVAC equipment market.

The growth of the North American HVAC equipment market is driven by an increase in demand for smart systems and the integration of the Internet of Things (IoT), industrial automation systems, smart manufacturing, and industry 4.0. A significant portion of the market's above-average growth is anticipated from the uptick in green building construction activities. The smart home market, which is expanding rapidly, is projected to boost the HVAC system market's growth.

Green building construction projects further support the empowerment of the HVAC equipment market in the region. For instance, in February 2022, Canada Green Building Council (CAGBC) announced that the country ranked second globally on the annual list of Top 10 Countries and Regions for LEED (Leadership in Energy and Environmental Design), a green building certification program used worldwide, in 2021. Installation of HVAC equipment with standards imposed by the governmental bodies for the rising awareness of occupants' health and energy consumption is becoming a vital criteria in green building designs.

However, as per IEA and the U.S. Department of Energy, around 25-35% of electricity consumption is due to HVAC systems. According to the same source, a large part (20% - 60%) of this energy consumption is contributed by parasitic energy use (energy used to power fans and pumps used for the transfer of heating and cooling). Thus, centralized HVAC systems have burdened energy bills despite being more efficient (in terms of energy units' consumption per unit area of space conditioned) than unitary systems.

There is a lack of employment in the whole manufacturing sector. Sadly, there is no exception in the heating and air conditioning industry Whether or not current workforce shortages are caused by these, they will likely be exacerbated might hamper the market gorwth

North America HVAC Equipment Market Trends

Heat Pumps to Witness Significant Growth

The market share that heat pumps are predicted to command is significant. Due to various factors, including climatic conditions, the convenience provided by the equipment, government tax credit benefits, regulations, etc., the use of heat pumps has steadily increased in the North American region.

Owing to a paradigm shift toward adopting energy-efficient products and rising consumer spending, the residential heat pump market in the United States would continue to expand steadily. The business environment will be stimulated by the ongoing progress toward a decarbonized economy, which will be supported by legislative energy policies and incentives. As the number of old buildings that are being fixed up goes up, there will be more demand for flexibility and better comfort. This will make the industry more dynamic.

The heat pumps are been categorized based on types, such as water source, air source, and ground source. The air-source heat pump (ASHP) takes in electricity, extracts heat from the surrounding air, and produces hot water up to 90 degrees Celsius. Due to the extraction of heat from the ambient air, it gets cooler. Thus, the requirement for both hot water and cold air is driving the growth of air-source heat pumps.

Moreover, Cold climate heat pumps are becoming increasingly popular in many regions across North America, and this has been driving significant innovation in the space. Cold climate heat pumps are developed to work efficiently in conditions down to -25 degrees Celsius, with some systems maintaining an efficiency of over 200% at -18 degrees Celsius.

In June 2022, the U.S (DOE) announced that Lennox International had became the first partner in the U.S. Department of Energy's (DOE's) Residential Cold Climate Heat Pump Technology has Challenge to develop an next-generation electric heat pump which woyuld that can more effectively heat homes in northern climates relative to current models.

United States Holds Major Market Share

The United States is one of the essential equipment markets, witnessing a steady growth rate. The growing construction activity, availability of high-efficiency systems, and extreme climatic conditions favour system installation across the facilities. Additionally, the presence of leading manufacturers, such as Carriers, Emerson Electric Co., and others, is complementing the growth of the North American market in the future.

Additionally, with the Internet of Things (IoT) integration, several manufacturers have initiated smart heating, air conditioning, and ventilation system offers that, in turn, are propelling market growth across the United States.

To ensure a sustainable future, the U.S. Department of Energy (DOE) is heavily investing in improving energy efficiency standards throughout the country. The DOE wants to make sure that America is safe and doing well by finding science and technology solutions to its environmental, energy, and nuclear problems.

Moreover, the Energy Information Administration's (EIA) Residential Energy Consumption Survey (RECS) estimates that 76 million primarily occupied US homes (64% of the total) use central air-conditioning equipment. About 13 million households (11%) use heat pumps for heating or cooling. By 2023, all new residential air-conditioning and air-source heat pump systems sold in the United States will require meeting the latest energy efficiency standards, fueling the growth of HVAC equipment.

Furthermore, according to the US Census Bureau, new home construction in the United States in June 2022 was around 1.36 million. There were approximately 1.55 million new privately owned housing units in the United States in June 2022. This is further expected to create significant new demand for heat pumps in the country over the forecast period.

North America HVAC Equipment Industry Overview

The competitive rivalry in the North American HVAC equipment market is high, as the market studied is home to prominent vendors like Daikin, Carrier, and Lennox that command a major market share in different segments and have access to well-established distribution networks. Owing to the HVAC equipment industry being one of the largest markets, the existence of such a high number of major vendors without compromising on their market shares is sustainable. However, each vendor, especially in the heating and cooling segments, is fiercely competing to gain a larger share of the market studied.

February 2023 - Lennox enhanced its comprehensive selection of With the introduction of the Enlight and Xion product lines, packaged rooftop units have been introduced. The company's Enlight product family aims to minimize environmental impact and maximize efficiency.

October 2022 - Carrier Corporation declared that it had increased In North America, the AquaEdge 19DV watercooled Centrifugal chiller offers a range of capacities. The AquaEdge19DV is capable of supplying the customer with up to 1150 tonnes in order to meet their demand for larger capacities, as regards Commercial Highrise and mixed Use Building Applications, Large Manufacturing Establishments or Health Institutions.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumption and Market Defnition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 An Assessment of Impact of Macro Economic Trends on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rise in Residential and Non-residential Users