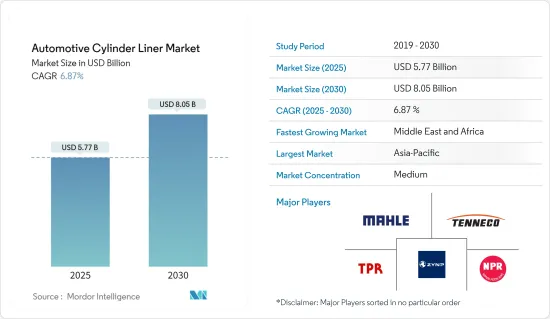

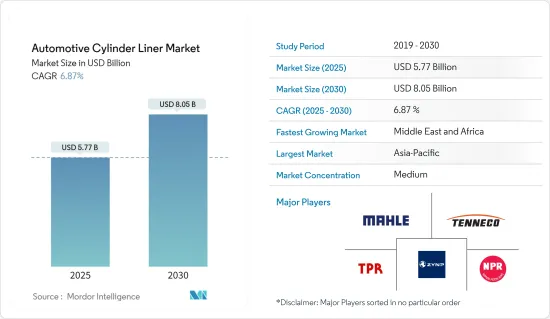

자동차 실린더 라이너 시장 규모는 2025년에 57억 7,000만 달러, 2030년에는 80억 5,000만 달러에 이를 것으로 예측되고 있습니다.예측 기간 중(2025-2030년) CAGR은 6.87%로 성장할 것으로 예상됩니다.

상용차 판매량 증가와 자동차 보유 대수 증가는 세계 자동차 산업 성장의 주요 결정 요인으로, 자동차 실린더 라이너 수요에 긍정적인 영향을 미치고 있습니다. 상용차의 성장은 주로 전자상거래의 확대 및 운송을 위한 상용차 사용 증가의 영향을 받습니다. 또한 자동차 산업의 발전과 발전을 지원하는 산업화와 인프라 개발 증가가 상용차 시장의 성장을 가속하고 있습니다.

국제자동차공업협회에 따르면 2022년 상용차의 세계 신차 판매량은 2,410만대에 달했습니다.

또한 주요 지역에서 수소 전기 상용차 수요가 증가함에 따라 실린더 라이너 제조업체에 첨단 기술 개발을 촉진하고 있습니다. 여러 주요 기업들이 수소 전기 트럭을 위한 실린더 라이너 기술을 도입하고 있으며 시장 성장을 가속하고 있습니다. 차량 스크랩 프로그램, 차량 길이 및 적재량 제한 등에 관한 엄격한 규제 기준도 시장 성장을 가속할 것으로 예상됩니다.

아시아태평양은 인도와 중국에서 자동차 산업의 잠재력이 증가함에 따라 자동차 실린더 라이너의 소비를 지배할 것으로 예상됩니다. 미국과 같은 세계의 많은 국가에서 원료 및 엔진 부품을 중국, 일본 및 기타 경제 지역에서 조달하고 완전한 엔진 챔버 아래에 조립합니다. 자동차 판매와 생산이 증가함에 따라 이 지역의 실린더 라이너 수요는 높은 수준을 유지할 것으로 예상됩니다.

승용차는 신흥국에서 가장 흔한 교통 수단입니다. 신흥국에서는 1인당 소득 증가에 따라 승용차의 보유 대수가 증가하고 있어 이러한 요인이 자동차 실린더 라이너 시장에 플러스의 영향을 미칠 것으로 보입니다. 인도와 같은 신흥국은 승용차용 에탄올과 같은 더 나은 연료를 찾고 있으며 시장 성장에 긍정적인 영향을 줄 수 있습니다.

예를 들어, 2023년 8월, Toyota Innova는 에탄올만으로 주행할 수 있는 세계 최초의 유연한 연료차가 되었습니다. 도요타 자동차는 100% 에탄올을 연료로 하는 자동차를 도입하는 세계 최초의 자동차 제조업체가 될 것으로 예측되고 있습니다. 2023년 8월 인도 연방 장관은 도요타에서 가장 인기 있는 승용차 '이노바'를 기반으로 한 차량을 출시했습니다. 이노바는 플렉서블 연료전기증명서를 갖춘 밸랏 페이즈 VI 차량을 탑재한 세계 최초의 모델이 되었습니다. 이 발표는 일본의 주요 자동차 제조업체가 수소 연료전지를 사용하는 미라이를 발표한 지 1년 후에 이루어졌습니다.

배기가스 규제 강화, 전기자동차 보급, 내연기관(ICE) 차량이 환경에 미치는 유해한 영향으로 인한 화석연료의 매장량 부족이 시장 성장에 과제를 줄 수 있습니다. 그러나 신흥국은 전기자동차를 위한 인프라 정비가 필요하며, 충전설비가 예측기간 동안 내연기관 시장 확대를 촉진할 것으로 예상됩니다. 국제자동차공업회(OICA)에 따르면 2022년 세계 승용차 신차 판매 대수는 5,740만대에 달하고, 2021년 대비 전년대비 1.9%의 성장세를 기록했습니다. 2022년 승용차 신차 판매 대수는 남아프리카가 전년대비 19.5% 증가, 태국이 10.0% 증가를 기록했습니다.

도시화율의 상승과 자가용 교통수단을 이용하는 소비자의 기호의 변화는 세계 자동차 산업을 견인할 것으로 예상되며, 나아가 선진 자동차 실린더 라이너 시장 수요를 견인할 것으로 기대됩니다. 세계 은행에 따르면 인도의 도시화율은 2018년의 34%에 비해 2022년에는 36%에 달했습니다. 신흥국 시장의 도시로 이주하는 소비자가 늘어나면서 개인적인 이동이 선호되고, 이는 전 세계 자동차 실린더 라이너 시장의 성장으로 이어질 수 있습니다.

아시아태평양의 자동차 실린더 라이너 시장은 중국과 인도의 자동차 부문이 확대됨에 따라 실린더 라이너 제품의 판매가 증가하고 있습니다. 양국은 자동차 판매에 박차를 가해 큰 엔진 수요를 낳고 있습니다.

인도는 이 지역의 주요 자동차 수출국 중 하나이며 현재의 이동성 확대 프로젝트를 보고 곧 강력한 수출 성장이 예상됩니다. 게다가 인도 정부에 의한 자동차 산업을 지원하는 호의적인 대처와, 이 나라 시장에 있어서의 대기업 자동차 제조업체의 존재가, 이 나라를 주요한 자동차 수출국의 하나로 발전시키는 일조가 되고 있습니다. 이 나라의 자동차 산업은 2000년 4월부터 2022년 9월까지 총 337억7,000만 달러의 직접 투자를 받았습니다. 정부는 2024년까지 자동차 산업 규모를 2배의 180억 달러로 확대할 것으로 전망하고 있습니다. 또한 중국은 자동차 산업의 처리 능력과 엔진 생산에서 아시아태평양에서 압도적인 지위를 차지하고 있습니다.

2022년 중국에서의 자동차 판매 대수는 2,680만대가 되어, 2021년의 2,627만대에서 전년대비 2.2%의 성장을 기록했습니다. 이 지역에서는 주요 엔진 제조업체나 상대방 상표 제품 제조업체(OEM)에 의한 투자, 확대, 개발이 확대되고 있습니다. 이것은 예측 기간 동안 실린더 라이너 수요를 완화시킬 것으로 예상됩니다.

예를 들어 2022년 3월 Harbin Dongan Auto Engine은 머시닝 센터, 마킹 머신, 조임 머신, 접착 머신 및 기타 장비를 포함할 것으로 예상되는 고효율 확장 범위 엔진용 생산 라인을 구축하기 위한 2022년 투자 계획을 발표했습니다. 이 프로젝트는Harbin Dongan Auto Engine의 자회사인 Harbin Dongan Automotive Engine Manufacturing Co.Ltd가 공동으로 정비할 계획으로 총 투자액은 7,233만 위안(1,085만 달러)입니다.

이 때문에 이 지역의 승용차·상용차 산업의 확대에 수반해, 자동차 실린더 라이너 시장 수요는 향후 수년에 급속히 급증할 것으로 예상됩니다. 그러나 정부가 전기자동차의 보급에 중점을 둔 것은 아시아태평양에서 장기적인 제품 성장의 큰 저해 요인이 될 수 있습니다. 그러나 단기적으로는 차량의 전기화를 향한 경쟁 시프트가 이러한 정부들에게 큰 과제가 되고 있습니다. 따라서 자동차 실린더 라이너 수요는 예측 기간 동안에도 견고하게 추이할 것으로 예상됩니다.

자동차 실린더 라이너 시장은 적당한 단편화를 보여주며, 조직화된 업체와 조직화되지 않은 업체가 혼합되어 업계 상황을 형성하고 있습니다. 실린더 라이너 시장의 주요 경쟁업체로는 Mahle GmBH, Tenneco Inc., TPR, 일본 피스톤 링, ZYNP 등이 있습니다. 주요 제조업체는 수익성과 제품 효율성을 높이기 위해 자동차 실린더 라이너의 연구 개발에 많은 투자를 하고 있습니다.

원재료 조달과 관련된 위험을 줄이기 위해 각 회사는 적극적인 접근 방식을 채택하고 주요 원료 공급업체와의 관계를 확대하고 있습니다. 이 전략은 실린더 라이너의 생산에 필요한 원재료의 안정적이고 지속적인 공급을 보장하는 데 성공했습니다.

2022년 10월 : 라인 메탈 AG의 주물 사업 부문(라인 메탈과 화우 기차 계통의 합작 회사)은 영국의 유명 스포츠카 제조업체에 V8 엔진 블록을 공급하는 중요한 수주를 획득했습니다. V8 엔진은 4자리에 다가오는 훌륭한 마력을 자랑합니다.

2022년 4월 : 북미 도요타는 미국 4개 공장에 3억 8,300만 달러를 투자할 의향을 밝혔습니다. 이 투자는 하이브리드와 기존의 파워트레인에 맞는 새로운 4 기통 엔진의 생산 준비를 목표로합니다. 엔진 생산 범위에는 엔진 헤드, 라이너 및 기타 다양한 부품을 포함한 엔드 투 엔드 조립이 포함됩니다.

The Automotive Cylinder Liner Market size is estimated at USD 5.77 billion in 2025, and is expected to reach USD 8.05 billion by 2030, at a CAGR of 6.87% during the forecast period (2025-2030).

The rising sales of commercial vehicles and increasing vehicle parc globally serve as major determinants for the growth of the automotive industry across the world, which, in turn, is positively impacting the demand for automotive cylinder liners. Commercial vehicle growth is primarily influenced by the expansion of e-commerce and the increasing use of commercial vehicles for transportation. Aside from that, rising industrialization and infrastructure development, which support advancement and development in the automotive industry, are driving market growth for commercial vehicles.

According to the International Organization of Motor Vehicle Manufacturers, the global sales of new commercial vehicles touched 24.1 million units in 2022.

Furthermore, rising demand for hydrogen electric commercial vehicles across major regions is pushing cylinder liner manufacturers to develop advanced technology. Several key players are introducing cylinder liner technology for hydrogen-electric trucks, boosting market growth. Vehicle scrappage programs and stringent regulatory norms for vehicle length and loading limits, among other parameters, are also expected to drive the growth of the market.

Asia-Pacific is expected to dominate the consumption of automotive cylinder liners, owing to the increased potential of the automotive industry in India and China. Many countries across the world, such as the United States, source their raw materials and engine components from China, Japan, and other economies to assemble them under complete engine chambers. With rising automotive sales and production, the region's demand for cylinder liners is expected to remain high.

Passenger cars are the most common form of transport in emerging countries. The number of passenger cars is increasing in developing countries with the rise in per capita income, and such factors are likely to impact the automotive cylinder liner market positively. Emerging countries, such as India, are looking for better fuels, like ethanol, for their passenger cars, which may positively impact the market growth.

For instance, in August 2023, Toyota Innova became the world's first flexible fuel vehicle that can run entirely on ethanol. Toyota Motor is projected to become the first automaker in the world to introduce cars powered by 100% ethanol. In August 2023, the Union Minister of India launched a vehicle based on Toyota's most popular passenger car, Innova. Innova became the first model in the world to feature a Bharat Phase VI vehicle with a flexible fuel electric certificate. The launch came a year after the Japanese auto giant introduced Mirai, which uses hydrogen fuel cells.

Increasing emission regulations, penetration of electric vehicles, and lack of fossil fuel reserves due to the toxic impact of internal combustion engine (ICE) vehicles on the environment could challenge the growth of the market. However, in emerging countries, there needs to be more infrastructure for electric vehicles, and charging facilities are expected to facilitate the expansion of the internal combustion engine market during the forecast period. According to the International Organization of Motor Vehicle Manufacturers (OICA), global new passenger car sales touched 57.4 million in 2022, recording a Y-o-Y growth of 1.9% compared to 2021. Countries such as South Africa and Thailand recorded 19.5% and 10.0% Y-o-Y growth, respectively, in new passenger car sales in 2022 compared to the previous year.

The rising urbanization rate and the shifting preference of consumers toward availing private transportation mediums are anticipated to drive the automotive industry across the world, which, in turn, is expected to drive the demand for the advanced automotive cylinder liner market. According to the World Bank, the urbanization rate in India stood at 36% in 2022, compared to 34% in 2018. As more consumers migrate to urban areas in developing nations, there will be a preference for personal mobility, which, in turn, may lead to the growth of the automotive cylinder liner market across the world.

The Asia-Pacific automotive cylinder liner market is witnessing elevated sales of cylinder liner products owing to the expanding auto sector of China and India. Both countries are fuelling vehicle sales, generating significant engine demand.

India is one of the major automobile exporters in the region, and strong export growth is expected shortly, seeing its present mobility expansion projects. Furthermore, favorable initiatives by the Indian government to support the automotive industry and the presence of major automakers in its market are assisting in developing the country into one of the major automobile exporters. The automotive industry in the country received a cumulative FDI inflow of approximately USD 33.77 billion between April 2000 and September 2022. The government expects to double the size of the automotive industry to USD 18 billion by 2024. Furthermore, China holds the dominant hand in Asia-Pacific in terms of auto industry throughput and engine production.

In 2022, the total number of vehicles sold in China stood at 26.8 million units, compared to 26.27 million units in 2021, registering a year-on-year growth of 2.2%. The region is witnessing extended investment, expansion, and development, proliferated by key engine manufacturers and original equipment manufacturers (OEMs). This is expected to mitigate the demand for cylinder liners over the forecast period.

For instance, in March 2022, Harbin Dongan Auto Engine Co. Ltd unveiled its investment plan for 2022 for building a production line for high-efficiency extended-range engines, which was expected to involve machining center, marking machines, tightening machines, gluing machines, and other equipment. The project was planned to be jointly maintained by Harbin Dongan Automotive Engine Manufacturing Co. Ltd, the subsidiary of Harbin Dongan Auto Engine, with a total investment of CNY 72.33 million (USD 10.85 million).

Therefore, with the region's expanding passenger car and commercial vehicle industry, the demand for the automotive cylinder liner market will showcase a rapid surge in the coming years. However, shifting the government's focus to promote the adoption of electric vehicles could act as a major deterrent to the growth of these products in the long run in Asia-Pacific. However, a competitive shift toward electrification of vehicle fleets in the short run is a major challenge for these governments. Therefore, the demand for automotive cylinder liners is expected to remain strong during the forecast period.

The automotive cylinder liner market exhibits moderate fragmentation, with a mix of organized and unorganized players shaping the industry landscape. Among the key contenders in the cylinder liner market, notable players include Mahle GmBH, Tenneco Inc., TPR Co. Ltd, Nippon Piston Ring Co. Ltd, and ZYNP. Significant manufacturers are channeling substantial investments into the research and development of automotive cylinder liners to enhance profitability and product efficiency.

To mitigate the risks associated with raw material procurement, companies have adopted a proactive approach, maintaining extended relationships with their primary raw material suppliers. This strategy has proven successful in ensuring a consistent and uninterrupted supply of materials necessary for cylinder liner production.

October 2022: Rheinmetall AG's Castings business unit, a joint venture between Rheinmetall and HUAYU Automotive Systems Co. Ltd, secured a significant order to supply a V8 engine block to a renowned English sports car manufacturer. Notably, the V8 engines boast an impressive horsepower output, approaching four figures.

April 2022: Toyota Motor North America disclosed its intention to invest USD 383 million in four US-based plants. This investment is aimed at preparing to produce a new four-cylinder engine variant tailored for hybrid and conventional powertrains. The scope of engine production encompasses end-to-end assembly, encompassing engine heads, liners, and various other components.