ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

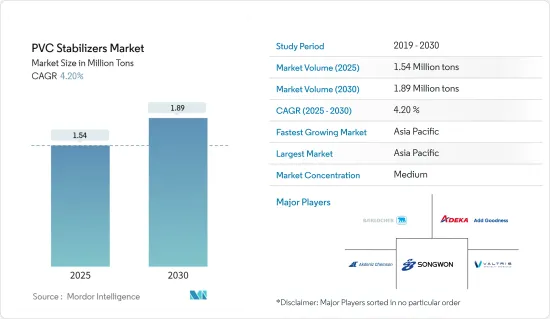

PVC 안정제 시장 규모는 2025년에 154만 톤으로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 4.2%로 성장할 전망이며, 2030년에는 189만 톤에 달할 것으로 예측되고 있습니다.

COVID-19의 유행은 PVC 안정제 시장에 부정적인 영향을 미쳤습니다. 세계의 가동 중단과 엄격한 정부 규제로 인해 대부분의 생산 기지가 가동을 중단하고 치명적인 후퇴를 강요했습니다. 그럼에도 불구하고 시장은 2021년에 회복되어 향후 몇 년동안 크게 상승할 것으로 예상됩니다.

주요 하이라이트

단기적으로는 PVC 파이프, 튜브 및 피팅용 안정제 수요 증가와 자동차 산업에서의 사용 증가가 PVC 안정제 수요를 촉진하는 주요 요인입니다.

그러나 납 기반 안정제의 사용과 관련된 건강 피해와 엄격한 정부 규제가 시장 성장을 방해할 것으로 예상됩니다.

그럼에도 불구하고 환경 친화적인 선택으로 유기 주석계 안정제의 사용이 증가하고 있기 때문에 시장 조사에 새로운 기회가 생길 것으로 예상됩니다.

아시아태평양은 세계의 PVC 안정제 시장을 독점하고 있습니다. 이 지역 국가의 건축 및 건설을 포함한 다양한 최종 사용자 산업에서의 PVC 안정제 수요 증가는 아시아태평양 시장을 견인하고 있습니다. 중국과 인도는 이 지역 시장에 크게 기여하고 있습니다.

PVC 안정제 시장 동향

시장을 독점하는 건축 및 건설 부문

PVC는 건축 및 건설 산업에서 주요 플라스틱으로 돋보입니다. 견고하면서도 경량이기 때문에 내후성, 화학 부식, 마모에 대한 내구성이 보장됩니다. PVC로 만든 일반적인 제품에는 파이프, 케이블, 창틀, 바닥재, 지붕재 등이 있습니다.

PVC 파이프는 상하수도 시스템에서 매우 중요한 역할을 합니다. 그것은 부드럽고 마찰없는 흐름을 보장하고 빌드 업, 스케일링 및 부식에 저항합니다. 특히 PVC 파이프는 식수의 운송에 안전하다고 생각되며, 지하에 설치하면 100년이 넘는 수명을 자랑합니다. 또한 비용 효율이 높고 8-10회 재활용할 수 있습니다.

옥스포드 이코노믹스는 세계 건설 생산량이 강력한 성장 궤도를 그릴 것으로 예측하고 있으며 현재 4조 2,000억 달러 이상에서 2037년에는 13조 9,000억 달러 이상으로 증가할 것으로 예측했습니다.

중국은 세계 PVC 파이프의 50-60%를 생산하며 세계를 석권하고 있습니다. 특히 염화 비닐 폴리머로 만들어진 경질 튜브, 파이프, 호스의 최대 수출국이 되고 있습니다.

2023년 중국의 건설 산업은 실액으로 6.5%의 성장을 이루었습니다. 국가통계국(NBS) 발표에 따르면 이 산업의 경제공헌은 지난 9개월간 전년 동기 대비 7.2% 증가로 급증했습니다.

인베스트 인디아에 따르면 도시화 동향에 따르면 2030년까지 인구의 40% 이상이 도시에 거주하게 되며, 2,500만 호의 중급 주택과 저렴한 주택이 더욱 필요하다고 합니다. 또한 주택도시에 따르면 AMRUT 계획에 따라 약 134,000호의 수도와 102,000호의 하수도가 정비될 예정입니다.

미국에서는 파리 협정에 맞추어 2030년까지 배출량을 2005년 대비 50-52% 삭감하겠다는 미국 정부의 목표가 있기 때문에 향후 수년간 PVC 생산에 영향이 미칠 가능성이 높습니다. 그 결과 미국 PVC 산업은 온실가스(GHG) 배출을 억제하기 위한 실질적인 대책을 준비하고 있으며, 2050년까지 탄소 중립을 목표로 하고 있습니다.

또한 2023년 12월에는 미국 환경보호청(EPA)이 PVC 규제 계획을 발표하고 폐기 의무화의 형태를 바꿀 계획입니다.

European Council of Vinyl Manufacturers에 따르면, 창문, 파이프, 바닥재, 지붕 막과 같은 건축용 제품은 유럽 PVC의 70%를 사용합니다. 유럽의 건축 및 건설 업계에서 PVC는 주요 플라스틱입니다.

독일의 견조한 경제는 상업 공간 수요를 급증시키고 있습니다. 특히 고품질의 ESG에 준거한 오피스 빌딩에 대한 관심이 높아지고 있으며, 프라임 임대료가 상승하고 있다는 점에서도 분명합니다. 2023년 3분기에는 24만 6,000평방미터의 사무실 공간이 가동되었고, 2024년에는 총 180만 평방미터가 된 것으로 평가되고 있습니다.

이러한 움직임을 감안할 때, 세계 건설 업계의 융성은 앞으로 수년간 PVC 안정제의 완고한 전망을 시사하고 있습니다.

아시아태평양이 시장을 독점

아시아태평양은 중국, 인도 등 국가의 건설과 자동차 등 산업 수요 급증으로 PVC 안정제 시장을 선도하고 있습니다.

PVC 파이프와 바닥재는 내구성, 미적 유연성, 쉬운 설치, 간단한 청소, 재활용 등의 장점을 제공합니다. 건축 및 건설 업계에서는 PVC 지붕재는 유지보수 수고가 적고 30년 이상 긴 수명이 지지되고 있습니다.

중국 홍콩 주택 당국은 저가 주택 건설을 추진하기 위해 몇 가지 조치를 취하고 있습니다. 당국은 2030년까지 10년간 30만 1,000호의 공공 주택을 공급하는 것을 목표로 하고 있습니다.

게다가 일본의 건설 업계도 최근 몇 년동안 PVC 안정제의 주요 소비자가 되었습니다. 일본에서는 미쓰비시지소가 2027년 완성을 목표로 매월 4만 3,000달러의 임대료가 전망되는 고급 아파트 50호를 보유한 일본 제일의 고층 빌딩을 도쿄역 근처에 건설하는 등 주목해야 할 건설 프로젝트가 진행되고 있습니다.

PVC는 자동차 산업에서 전통적인 자동차 및 전기자동차의 보닛 내부 및 인테리어 등에 일반적으로 사용됩니다.

중국은 세계 최대의 자동차 제조업체 중 하나입니다. OICA에 따르면 2023년 중국 승용차 생산량은 2,600만 대로 2022년 대비 10% 이상 증가했습니다.

또한 OICA에 따르면 2023년 인도 자동차 생산 대수는 585만 대로 2022년 대비 7% 이상 증가를 기록했습니다. 이 나라의 승용차 생산 대수는 478만대로 2022년 대비 7.9% 증가하여 시장 성장을 지원했습니다.

신화사 통신 데이터에 따르면 중국의 전자기기 제조업은 생산량 증가와 국내 및 세계 수요 회복에 힘입어 2024년 연초 4개월에 호조로운 실적을 보였습니다. 산업정보화부의 보고에 따르면 중국의 일렉트로닉스 산업의 주요 기업은 2024년 1월부터 4월까지의 총 이익이 전년 동기 대비 75.8% 급증하여 1,442억 위안(-203억 달러)에 이르렀습니다.

인도 포장 산업 협회(PIAI)는 인도 포장 산업이 예측 기간 동안 22%의 견조한 성장을 이룰 것으로 예측됩니다. 게다가 인도의 포장 시장은 2025년까지 2,048억 1,000만 달러에 달할 기세이며, 그때까지의 CAGR은 26.7%라는 경이적인 성장을 자랑할 전망입니다. 이 급증은 향후 수년간 인도 전역에서 PVC 안정제 수요가 높아지는 것을 뒷받침하고 있습니다.

이러한 역학과 정부의 뒷받침을 감안할 때, 아시아태평양은 예측 기간 동안 PVC 안정제 시장에서 수요 증가를 기록할 준비가 되어 있습니다.

PVC 안정제 산업 개요

PVC 안정제 시장은 그 특성상 부분적으로 단편화됩니다. 주요 기업(순부동)에는 Baerlocher GmbH, ADEKA Corporation, Akdeniz Chemson, SONGWON, Valtris Specialty Chemicals 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

PVC 파이프, 튜브, 피팅용 안정제 수요 증가

자동차 산업에서의 사용 증가

기타 촉진요인

성장 억제요인

납계 안정제의 사용에 관한 건강 피해 및 엄격한 정부 규제

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형별

칼슘 베이스

납 베이스

주석 베이스

바륨계

기타 유형

최종 사용자 산업별

건축 및 건설

자동차

전기 및 전자

포장

양말

기타 최종 사용자 산업

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

이집트

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%)** 및 랭킹 분석

주요 기업의 전략

기업 프로파일

Adeka Corporation

Akdeniz Chemson

Baerlocher GmbH

Clariant

Galata Chemicals

Goldstab Organics Pvt. Ltd

KD Chem Co. Ltd

Kunshan Maijisen Composite Materials Co. Ltd

Pau Tai Industrial Corp.

PMC Group Inc.

Ra Chemicals Pvt. Ltd

Reagens SpA

Shandong Jinchangshu New Material Technology Co. Ltd

SONGWON

Timah

Valtris Specialty Chemicals

Vikas Ecotech Ltd

제7장 시장 기회 및 향후 동향

환경 친화적인 선택으로 유기 주석 안정제의 사용 증가

기타 기회

AJY

영문 목차

영문목차

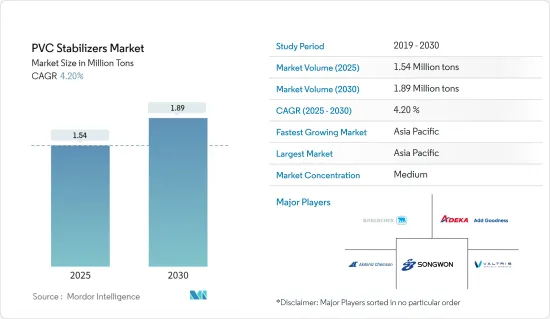

The PVC Stabilizers Market size is estimated at 1.54 million tons in 2025, and is expected to reach 1.89 million tons by 2030, at a CAGR of 4.2% during the forecast period (2025-2030).

The COVID-19 pandemic adversely affected the PVC stabilizers market. Global lockdowns and severe government rules resulted in a catastrophic setback, as most production hubs were shut down. Nonetheless, the market recovered in 2021 and is expected to rise significantly in the coming years.

Key Highlights

Over the short term, growing demand for stabilizers for PVC pipes, tubings, and fittings and increasing use in the automotive industry are the major factors driving demand for PVC stabilizers.

However, health hazards and stringent government regulations regarding the use of lead-based stabilizers are expected to hinder the market's growth.

Nevertheless, the rising usage of organo-tin stabilizers as an environmentally friendly option is expected to create new opportunities for the market studied.

Asia-Pacific dominates the global PVC stabilizers market. Rising demand for PVC stabilizers in different end-user industries, including building and construction in the countries of this region, is driving the Asia-Pacific market. China and India are the major contributors to this regional market.

PVC Stabilizers Market Trends

The Building and Construction Segment to Dominate the Market

Polyvinyl chloride (PVC) stands out as the predominant plastic in the building and construction industry. Its robust yet lightweight nature ensures durability against weathering, chemical corrosion, and abrasion. Common products crafted from PVC include pipes, cables, window profiles, flooring, and roofing.

PVC pipes play a pivotal role in water, waste, and sewage systems. They resist build-up, scaling, and corrosion, ensuring a smooth, friction-free flow. Notably, PVC pipes are deemed safe for transporting drinking water, boasting a service life exceeding 100 years for underground installations. Additionally, they are cost-effective and can be recycled 8-10 times.

Oxford Economics forecasts a robust growth trajectory for global construction output, projecting an increase from over USD 4.2 trillion currently to a staggering USD 13.9 trillion by 2037, predominantly fueled by the construction powerhouses of China, the United States, and India.

China dominates the global landscape, producing 50-60% of the world's PVC pipes. Notably, it stands as the foremost exporter of rigid tubes, pipes, and hoses crafted from vinyl chloride polymers.

In 2023, China's construction industry witnessed a 6.5% growth in actual value. The industry's economic contribution surged by 7.2% Y-o-Y during the initial nine months, as highlighted by the National Bureau of Statistics (NBS).

As per Invest India, urbanization trends suggest that by 2030, over 40% of the population will reside in urban locales, driving the need for an additional 25 million mid-end and affordable housing units. Furthermore, according to the Ministry of Housing & Urban Affairs, around 134 lakh water tap connections and 102 lakh sewer/septage connections have been provided under the AMRUT scheme.

PVC production in the United States is likely to be affected in the coming years due to the US government's target of reducing emissions by 50-52% from 2005 benchmarks by 2030, aligning with the Paris Agreement. Consequently, the US PVC industry is gearing up for substantial measures to curtail greenhouse gas (GHG) emissions, eyeing carbon neutrality by 2050.

Furthermore, in December 2023, the US Environmental Protection Agency (EPA) unveiled plans to regulate PVC, a move poised to reshape disposal mandates.

According to the European Council of Vinyl Manufacturers, windows, pipes, flooring, roofing membranes, and other building products use 70% of all European PVC. It is the leading plastic in the European building and construction industry.

Germany's robust economy is driving a surge in demand for commercial spaces. Notably, there has been a growing interest in high-quality, ESG-compliant office buildings, evident from rising prime rents. In Q3 2023, 246,000 sq. m of office space came online, with forecasts suggesting a total of 1.8 million sq. m in 2024.

Given these dynamics, the global construction industry's prominence suggests a bullish outlook for PVC stabilizers over the coming years.

Asia-Pacific to Dominate the Market

Asia-Pacific leads the PVC stabilizers market, driven by surging demand from industries like construction and automotive in countries like China and India.

PVC pipes and flooring offer benefits like durability, aesthetic flexibility, easy installation, simple cleaning, and recyclability. In the building and construction industry, PVC roofing is favored for its low maintenance and longevity, lasting over 30 years.

The housing authorities of Hong Kong, China, have launched several measures to push the construction of low-cost housing. The officials aim to provide 301,000 public housing units in 10 years till 2030.

In addition, Japan's construction industry has been another major consumer of PVC stabilizers in recent times. Japan is witnessing notable construction projects, including Mitsubishi State's endeavor of erecting the nation's tallest building near Tokyo station, featuring 50 luxury apartments projected to earn USD 43,000 monthly in rent, with a completion target of 2027.

PVC is commonly used in under-the-hood applications, interiors, and other areas in conventional vehicles and electric vehicles in the automotive industry.

China is one of the largest automotive manufacturers worldwide. According to OICA, in 2023, the production of passenger vehicles in China stood at 26 million units, an increase of more than 10% compared to 2022.

Moreover, according to the OICA, in 2023, the total production of vehicles in India stood at 5.85 million units, registering an increase of more than 7% compared to 2022. The production of passenger vehicles in the country stood at 4.78 million units, registering an increase of 7.9% compared to the year 2022, thereby supporting the growth of the market.

As per data from Xinhua News Agency, China's electronics manufacturing industry showcased robust performance in the initial four months of 2024, buoyed by rising production and a rebound in both domestic and global demand. Major companies in China's electronics industry, as reported by the Ministry of Industry and Information Technology, saw their combined profits surge by 75.8% Y-o-Y, reaching CNY 144.2 billion (~USD 20.3 billion) from January to April 2024.

The Packaging Industry Association of India (PIAI) projects the Indian packaging industry to grow at a robust 22% during the forecast period. Furthermore, the Indian packaging market is on track to hit USD 204.81 billion by 2025, boasting an impressive CAGR of 26.7% until then. This surge underscores a rising demand for PVC stabilizers across India over the coming years.

Given these dynamics and government backing, Asia-Pacific is poised to register heightened demand in the PVC stabilizers market during the forecast period.

PVC Stabilizers Industry Overview

The PVC stabilizers market is partially fragmented by nature. The major players (not in any particular order) include Baerlocher GmbH, Adeka Corporation, Akdeniz Chemson, SONGWON, and Valtris Specialty Chemicals.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand for Stabilizers for PVC Pipes, Tubings and Fittings

4.1.2 Increasing Use In the Automotive Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Health Hazards and Stringent Government Regulations Regarding the Use of Lead-based Stabilizers

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 By Type

5.1.1 Calcium-based

5.1.2 Lead-based

5.1.3 Tin-based

5.1.4 Barium-based

5.1.5 Other Types

5.2 By End-user Industry

5.2.1 Building and Construction

5.2.2 Automotive

5.2.3 Electrical and Electronics

5.2.4 Packaging

5.2.5 Footwear

5.2.6 Other End-user Industries

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 NORDIC Countries

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 Qatar

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Egypt

5.3.5.6 South Africa

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements