지열 에너지 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Geothermal Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1687155

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

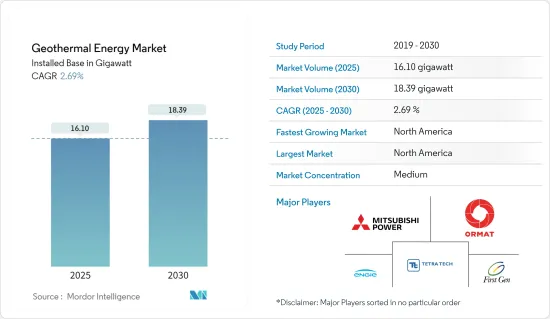

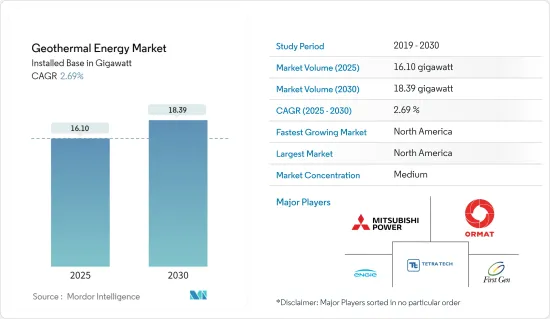

지열 에너지 시장 규모는 설치 기준으로 2025년 16.10기가와트로 추정되고, 2030년에는 18.39기가와트로 성장할 전망이며, 예측 기간인 2025-2030년 CAGR 2.69%로 성장할 전망입니다.

주요 하이라이트

중기적으로는 깨끗하고 친환경 자원에 의한 전력 안보에 대한 관심 증가 및 지중 열원 히트 펌프와 지역 난방을 포함한 냉난방 시스템 수요 증가 등의 요인이 지열 에너지 시장의 성장을 견인하고 있습니다.

한편, 태양광이나 풍력과 같은 대체 클린 에너지원은 유리한 시장이기 때문에 예측 기간 중 시장 성장의 방해가 될 가능성이 높습니다.

지속가능한 에너지 생산을 촉진하기 위한 재정적 급부나 세금 환급 등 정부 주도의 대처는 예측 기간 중 지열 에너지 시장에 많은 성장 기회를 만들어낼 것으로 추정됩니다.

북미는 예측기간 중 최대 시장이 될 것으로 예상되며, 수요의 대부분은 미국, 캐나다, 멕시코 등의 나라들로부터 가져옵니다.

지열 에너지 시장 동향

바이너리 사이클 지열 발전소가 크게 성장할 전망

바이너리 사이클 지열 발전소는 섭씨 182도(화씨 360도) 이하의 저온 유체를 내장하고 있어, 2차 유체로 이루어지는 열교환기를 통과시키고 있습니다. 2차 또는 바이너리 유체는 지열액을 기화시키고 터빈을 돌려 발전합니다.

바이너리 사이클 지열 발전소에서는 지열 유체가 직접 터빈과 접촉하지 않기 때문에 다른 두 가지 지열 기술과는 다른 기능을 가지고 있습니다.

바이너리 사이클 발전소의 장점은 고온 지열 자원보다 중온 지열 유체가 더 이용 가능하기 때문에 미국 에너지부의 발표에 따르면 바이너리 사이클 발전소는 이 특성을 살린 발전으로 보급될 수 있다는 것입니다.

바이너리 사이클 발전소의 구성 요소는 열교환기, 팽창기, 응축기, 발전기, 생산 웰, 재압입 웰, 터빈을 포함합니다. 이 발전소의 평균 정격 용량은 약 6MW입니다. 반대로 이중 압력 사이클, 이중 유체 사이클, 카리나 바이너리 사이클과 같은 바이너리 설계 사이클에는 큰 정격 용량이 공존합니다.

바이너리 사이클 발전소의 장점은 고온 지열 자원보다 중온 지열 유체가 더 가용성이 높기 때문에 미국 에너지부에 따르면 이 특성을 발전에 활용하기 위해 바이너리 사이클 발전소가 보급될 수 있다는 것입니다.

최근 몇 년 동안 많은 새로운 설치가 발표되었으며 예측 기간 동안 지열 에너지 시장의 성장을 지원할 수 있습니다. 2023년 9월, 튀르키예의 MTN 에너지 회사는 바바데레 지열 발전소의 2호기의 환경 영향 평가(EIA) 방법을 실시하기 위한 프로세스를 다시 시작했습니다. 이 검토는 지역 전력 수요를 충족시키기 위해 11.8MW 바이너리 사이클 발전소를 확대하기 위해 실시됩니다.

2023년 현재 이탈리아 정부는 토스카나 주에서 제안된 10MW 바이너리 사이클 지열 발전소 개발을 수락하고 있습니다. 이탈리아 최초의 바이너리 발전소는 2027년에 가동할 예정입니다. 32,000가구의 전력 수요를 충족하고 최대 4만 톤의 이산화탄소 배출을 줄일 수 있습니다. 따라서 이러한 프로젝트의 시작은 예측 기간에 바이너리 사이클 발전소를 활용하는 데 도움이 될 가능성이 높습니다.

게다가 2023년에는 지열에너지의 총 설비 용량은 세계 전체에서 약 14,846MW가 되어, 2022년의 1만 4,653MW로부터 증가했습니다. 설비 용량은 전 세계적으로 큰 폭으로 증가하고 있습니다.

따라서, 상기 요인이나 최근의 동향으로부터, 바이너리 사이클 발전소 부문은 예측 기간 중에 크게 성장할 것으로 예상됩니다.

북미가 시장을 독점할 전망

북미는 지열 에너지의 세계 주요 시장 중 하나이며, 미국은 설치 용량에 관해서 지역과 세계 시장을 리드하고 있습니다. 2023년에는 미국에서 약 16.5테라와트시의 지열 발전이 이루어졌습니다. 이것은 2022년부터 약 0.5테라와트시의 증가입니다.

국내의 지열발전소의 대부분은 지열에너지 자원이 지표에 가까운 서부의 주와 하와이 섬에 있습니다. 캘리포니아주는 지열에 의한 발전량이 가장 많고, 북캘리포니아의 가이저스 건식 증기 리저버는 세계 최대의 건식 증기 필드로 알려져 있습니다.

게다가 캘리포니아에는 국내에서 가장 많은 지열발전소가 있습니다. 2023년 현재 캘리포니아 주에는 전력회사가 운영하는 지열발전소가 31곳 있습니다. 이어 네바다 주에는 26개의 지열발전소가 있습니다. 이 해, 미국 전체의 지열 발전량은 164억 6,000만 킬로와트시의 정점에 이르렀습니다.

2024년 국제재생가능에너지기구(International Renewable Energy Agency 2024)에 따르면 2023년 미국의 지열발전 설비 용량의 합계는 약 2674만kW였습니다. 게다가 2023년 5월, Contact Energy는 Microsoft와 10년간의 전력 구매 계약을 맺었다고 발표했습니다. 이 계약에 근거해, Contact Energy는, 이 회사가 뉴질랜드에 보유하는 51.4 MW의 테 후카 유닛 3 지열 발전소에서 발전된 신재생 에너지 전량을 공급합니다. Contact Energy는 2022년 8월에 테 후카 유닛 3 지열 발전소를 발표하고 1억 8,900만 달러에 건설될 예정입니다. 2023년 말까지 운전을 시작할 예정입니다.

2024년 2월, 미국 에너지성의 지열기술국은 지열시스템의 갱정 시추 툴과 산업 시스템에 대한 저온지열 이용을 지원하는 프로젝트에 대해 최대 3,100만 달러의 자금제공 기회를 발표하였습니다. 또한 최대 2,310만 달러의 자금 제공으로 갱내 시멘트 및 케이스 평가 툴에 대응하는 프로젝트가 강화됩니다.

게다가 이 지역에서는 새로운 프로젝트도 계획되고 있어, 이 지역 시장 성장을 지지하는 것으로 기대되고 있습니다. 예를 들면, 2023년 3월, 멕시코 정부는, 연방 전력 위원회(CFE)아래에서 '지열정 굴착 서비스의 획득'이라고 하는 입찰을 통한 탐사 프로젝트를 발표했습니다.

따라서 상기 요인으로부터 예측 기간 중 북미가 지열 에너지 시장을 독점할 것으로 예상됩니다.

지열 에너지 산업 개요

지열 에너지 시장은 세분화되어 있습니다. 이 시장의 주요 기업에는 Mitsubishi Power Ltd, Ormat Technologies Inc., Engie SA, Tetra Tech Inc., First Gen Corporation 등이 있습니다.(순부동)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

지열 에너지의 설치 용량 및 예측(-2029년)

최근 동향 및 개발

정부 규제 및 시책

시장 역학

성장 촉진요인

깨끗하고 친환경 자원에 의한 전력 안보에 대한 우려 증가

지중 열원 히트 펌프를 포함한 냉난방 시스템에 대한 수요 증가

성장 억제요인

태양광이나 풍력 등의 대체 클린 에너지원에 대한 유리한 시장 기회

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

투자분석

제5장 시장 세분화

플랜트 유형별

건식 증기 플랜트

플래시 증기 플랜트

바이너리 사이클 발전 플랜트

시장 분석 : 지역별 시장 규모 및 수요 예측(-2029년)

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

스페인

노르딕

튀르키예

러시아

기타 유럽

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

나이지리아

카타르

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

주요 기업의 전략

기업 프로파일

Geothermal Power Plant Equipment Manufacturers

Toshiba Corporation

Ansaldo Energia SpA

Fuji Electric Co. Ltd.

Baker Hughes Company

Doosan Skoda Power

Geothermal Power Plant EPC Companies and Operators

Mitsubishi Power Ltd

Ormat Technologies Inc.

Kenya Electricity Generating Company(KenGen)

Sosian Energy Limited

Tetra Tech Inc.

Engie SA

First Gen Corporation

PT Pertamina Geothermal Energy

Enel SpA

Aboitiz Power Corporation

시장 랭킹 및 공유(%) 분석

제7장 시장 기회 및 향후 동향

금융급여 및 세환급 등 정부가 주도하는 이니셔티브 고조

AJY

영문 목차

영문목차

The Geothermal Energy Market size in terms of installed base is expected to grow from 16.10 gigawatt in 2025 to 18.39 gigawatt by 2030, at a CAGR of 2.69% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as increasing electricity security concerns due to clean and eco-friendly resources and increasing demand for heating and cooling systems, including ground source heat pumps and district heating, are driving the growth of the geothermal energy market.

On the other hand, the lucrative market for alternative clean energy sources like solar and wind is likely to hinder the market growth during the forecast period.

Nevertheless, government-undertaken initiatives such as financial benefits and tax refunds to promote sustainable energy production are estimated to generate numerous growth opportunities for the geothermal energy market during the forecast period.

North America is expected to be the largest market during the forecast period, with most of the demand coming from countries like the United States, Canada and Mexico, etc.

Geothermal Energy Market Trends

The Binary Cycle Power Plants Segment is Expected to Witness Significant Growth

The binary cycle geothermal power plants incorporate low-temperature fluids below 182 degrees Celsius (or 360 degrees Fahrenheit) that are made to pass through a heat exchanger consisting of a secondary fluid. This secondary or binary fluid vaporizes the geothermal liquid and propels the turbine to produce electricity.

In a binary-cycle geothermal power plant, the geothermal fluid does not directly come into contact with turbines, which makes it function differently from the other two geothermal technologies.

The advantage of binary cycle power plants is that as the geothermal fluid of moderate temperature has greater availability than high-temperature geothermal resources, binary cycle power plants might become more prevalent to take advantage of this attribute in electricity generation, as per the US Department of Energy.

The components of a binary cycle power plant include a heat exchanger, expander, condenser, generator, production well, reinjection well, and turbine. The average rated capacity of these power plants is around 6 MW. Conversely, large rated capacities co-exist with binary design cycles such as dual pressure, dual-fluid, and Kalinabinary cycles.

The advantage of binary cycle power plants is that as the geothermal fluid of moderate temperature has greater availability than high-temperature geothermal resources, binary cycle power plants might become more prevalent to take advantage of this attribute in electricity generation, as per the US Department of Energy.

Many new installations have been announced in recent years, which may support the growth of the geothermal energy market during the forecast period. As of September 2023, MTN Energy in Turkey re-initiated the process to conduct an Environmental Impact Assessment (EIA) method for the 2nd unit of the Babadere geothermal power plant. The examination is done to expand 11.8 MW of binary cycle plant to fulfill the electricity requirement of the region.

As of 2023, the government of Italy consented to develop the proposed 10 MW binary cycle geothermal plant in Tuscany. Italy's first-ever binary cycle plant is expected to become active in 2027. It holds the potential to fulfill the power requirement of nearly 32,000 households and curtail carbon emissions of up to 40,000 tonnes. Hence, the onset of such projects could likely help in utilizing binary cycle plants in the forecast period

Moreover, in 2023, the total geothermal energy installed capacity globally was around 14,846 MW, increasing from 14,653 MW in 2022. The capacity is increasing significantly across the world.

Therefore, based on the abovementioned factors and recent developments, the binary cycle power plants segment is expected to grow significantly during the forecast period.

North America is Expected to Dominate the Market

North America is one of the leading markets for geothermal energy worldwide, with the United States leading the regional and global markets regarding installed capacity. In 2023, approximately 16.5 terawatt hours of geothermal electricity were generated in the United States. This was an increase of roughly 0.5 terawatt hours from the 2022.

Most of the geothermal power plants in the country are in the western states and the island state of Hawaii, where geothermal energy resources are close to the Earth's surface. California generates the most of the electricity from geothermal energy, whereas Northern California's Geysers dry steam reservoir is the world's largest known dry steam field.

Moreover, California is home to the greatest number of geothermal power plants in the country. As of 2023, there were 31 such plants operated by electric utilities in the state. Nevada followed, with 26 geothermal power plants. That year, geothermal electricity generation across the United States reached a peak of 16.46 billion kilowatt hours.

According to the International Renewable Energy Agency 2024, the total geothermal installed capacity in United States was around 2,674 MW in 2023. Moreover, in May 2023, Contact Energy announced that the company had signed a 10-year Power Purchase Agreement with Microsoft. Under the contract, Contact Energy will supply all the renewable energy attributes generated by the company's 51.4 MW Te Huka Unit 3 geothermal power station, New Zealand. Contact Energy announced the Te Huka Unit 3 geothermal power station in August 2022 and will be built at a cost of USD 189 million. The plant is expected to commence operations by the end of 2023.

In February 2024, the United States Department of Energy's Geothermal Technologies Office announced a funding opportunity of up to USD 31 million for projects that support geothermal systems wellbore tools as well as the use of low-temperature geothermal heat for industrial systems. Also, funding of up to USD 23.1 million will enhance projects to address downhole cement and casing evaluation tools.

Furthermore, new projects are also planned in the region, which is expected to support the region's market growth. For example, in March 2023, Also, the government in Mexico announced a exploratory project under Federal Electricity Commission (CFE) through a tender called 'Acquisition of Geothermal Well Drilling Services.

Therefore, based on the above factors, North America is expected to dominate the geothermal energy market during the forecast period.

Geothermal Energy Industry Overview

The geothermal energy market is semi-fragmented. Some of the major players in the market (in no particular order) include Mitsubishi Power Ltd, Ormat Technologies Inc., Engie SA, Tetra Tech Inc., and First Gen Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Geothermal Energy Installed Capacity and Forecast, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Electricity Security Concerns Due to Clean and Eco-Friendly Resources

4.5.1.2 Increasing Demand for Heating and Cooling Systems, Including Ground Source Heat Pumps

4.5.2 Restraints

4.5.2.1 Lucrative Market Opportunities for Alternative Clean Energy Sources Like Solar and Wind

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Plant Type

5.1.1 Dry Steam Plants

5.1.2 Flash Steam Plants

5.1.3 Binary Cycle Power Plants

5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 France

5.2.2.3 United Kingdom

5.2.2.4 Spain

5.2.2.5 NORDIC

5.2.2.6 Turkey

5.2.2.7 Russia

5.2.2.8 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 India

5.2.3.3 Japan

5.2.3.4 South Korea

5.2.3.5 Malaysia

5.2.3.6 Thailand

5.2.3.7 Indonesia

5.2.3.8 Vietnam

5.2.3.9 Rest of Asia-Pacific

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Colombia

5.2.4.4 Rest of South America

5.2.5 Middle-East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 United Arab Emirates

5.2.5.3 South Africa

5.2.5.4 Nigeria

5.2.5.5 Qatar

5.2.5.6 Egypt

5.2.5.7 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Geothermal Power Plant Equipment Manufacturers

6.3.1.1 Toshiba Corporation

6.3.1.2 Ansaldo Energia SpA

6.3.1.3 Fuji Electric Co. Ltd.

6.3.1.4 Baker Hughes Company

6.3.1.5 Doosan Skoda Power

6.3.2 Geothermal Power Plant EPC Companies and Operators

6.3.2.1 Mitsubishi Power Ltd

6.3.2.2 Ormat Technologies Inc.

6.3.2.3 Kenya Electricity Generating Company (KenGen)

6.3.2.4 Sosian Energy Limited

6.3.2.5 Tetra Tech Inc.

6.3.2.6 Engie SA

6.3.2.7 First Gen Corporation

6.3.2.8 PT Pertamina Geothermal Energy

6.3.2.9 Enel SpA

6.3.2.10 Aboitiz Power Corporation

6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Rising Government-Undertaken Initiatives such as Financial Benefits and Tax Refunds