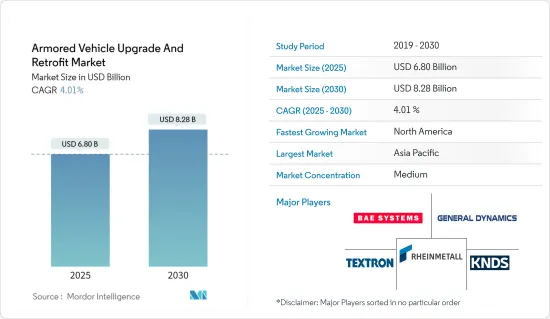

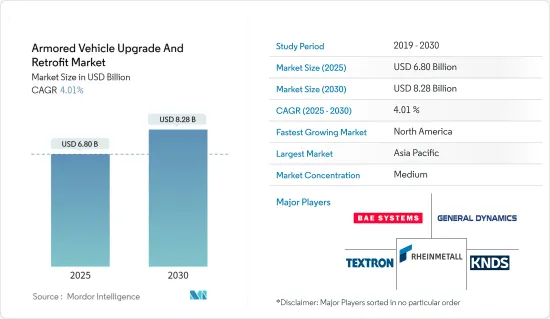

세계의 장갑차 업그레이드 및 레트로핏 시장 규모는 2025년 68억 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 4.01%를 나타낼 전망이며, 2030년에는 82억 8,000만 달러에 달할 것으로 예측됩니다.

육상 전투에서 매우 중요한 장갑차는 군사 작전에서 공격과 방어를 지원하는 이중 역할을 담당하고 있습니다. 이 차량은 군인과 화물을 운송하고 다양한 투사물을 비추는 무기와 장갑을 자랑하며 활발한 전투에 종사합니다. 국가의 군사력의 요인이며, 세계의 방위군에서 널리 활용되고 있습니다.

장갑차 업그레이드 및 레트로핏 시장은 세계 방위 예산의 확대가 주요 요인이 되어 진화하는 전장의 시나리오에 맞추어 자주 업그레이드가 이루어지고 있습니다. 또한 비용 효율적인 장갑 솔루션에 대한 의욕도 높아지고 있습니다. 스톡홀름 국제평화연구소(SIPRI)의 조사에 따르면 2023년 세계 국방비는 지난 2조 4,430억 달러에 달할 전망입니다.

세계 테러와 분쟁의 격화로 육상 차량의 최첨단 기술에 대한 수요가 급증하고 있습니다. 많은 국가들이 장갑차대의 노후화에 직면하고 있으며, 효율성, 살상력, 접속성을 높이기 위한 업그레이드 프로그램에 점점 눈길을 끌고 있습니다.

그러나, 특히 높은 연구개발비용과 장갑 시스템의 유효성과 수명을 저하시킬 가능성이 있는 고폭발성 대전차(HEAT) 탄두 등의 무기의 급속한 진보 등 과제는 산적하고 있습니다. 이러한 장애물이 시장 확대의 위협이 되는 한편, 노후화된 장갑차를 근대화하기 위한 세계의 대처가 진행되고 있기 때문에 향후 수년간은 시장을 추진할 자세입니다.

보병 전투 차량(IFV)은 기계화 보병 전투 차량(MICV)으로도 알려져 있으며 전투로 보병을 수송하고 직접 사격 지원을 제공하도록 설계된 장갑 차량입니다. IFV는 다양한 탄약으로부터 자신을 보호하기 위해 복합 장갑과 간격 적층 장갑과 같은 모듈 식 추가 장갑을 갖추고 있습니다. 시장의 성장은 주로 세계 방위 투자 증가와 방위력 강화에 대한 관심 증가로 이어집니다.

방위 예산이 확대됨에 따라 각국은 노후화된 IFV의 화기관제, 화력, 전반적인 기능을 업그레이드하고 있습니다. 또한 많은 국가가 신형 차량을 조달하고 있으며 차량 업그레이드 및 개조 수요가 급증하고 있습니다. 예를 들어, 2024년 3월 인도 국방부는 보병 전투 차량 BMP2에서 BMP2M으로 693 무장 업그레이드를 위해 Armoured Vehicles Nigam Limited(AVNL)와 최종 계약을 체결했습니다. 이 대규모 업그레이드는 Buy(인도의 독자적인 설계·개발·제조)로 분류되며, 야간 활성화, 포수 주 조준기, 지휘관 파노라마 조준기, 자동 목표 추적 장치가 있는 사격 통제 시스템(FCS)을 포함합니다.

2024년 3월, Nexter는 카타르의 2030년 이후 군사 현대화 계획에 따라 최신 VBCI 보병 전투 차량을 카타르에 선보였습니다. 이 프레젠테이션은 프랑스군을 위해 개선된 VBCI II 계약의 가능성을 제시했습니다. 또한 2022년 12월, 스웨덴은 슬로바키아 공화국 국방부와 BAE Systems의 CV9035 보병 전투차 152량을 13억 7,000만 달러로 계약했습니다. CV90MkIV로 판매되는 CV9035는 첨단 능력과 디지털 기술을 자랑합니다. 강화된 전장 속도, 뛰어난 핸들링, 미래를 바라보는 전자 아키텍처를 갖춘 이 차량은 현대 전장의 진화하는 요구에 부응하기에 충분한 장비를 갖추고 있습니다. 이러한 현재 진행중인 현대화 노력은 예상되는 IFV 업그레이드 프로그램과 함께 향후 몇 년동안 이 부문의 성장을 가속하는 태세를 갖추고 있습니다.

장갑차 업그레이드 및 레트로핏 시장에서는 북미가 향후 몇 년동안 우위를 차지하고 있습니다. 이 우위성은 이 지역의 왕성한 국방지출, 충실한 기존의 장갑차 보유 대수, 특히 미국과 캐나다의 군사근대화 투자 확대에 뿌리를 두고 있습니다. 스톡홀름 국제평화연구소(SIPRI)가 2022년에 발표한 보고서에서는 미국의 국방예산이 2023년에는 9,160억 달러에 달하는 등 미국의 헌신적인 자세가 강조되고 있습니다. 이 국방 예산의 급증은 수많은 업그레이드와 리노베이션의 구상에 박차를 가해 국가의 방위력을 강화했습니다. 예를 들어, 2024년 5월, 미국 육군은 차세대 Bradley 전투 차량을 강화하기 위해 Elbit Systems와 3,700만 달러의 계약을 체결했습니다. General Dynamics Ordnance and Tactical Systems는 Elbit의 Iron Fist 액티브 프로텍션 시스템(APS)을 Bradley M2A4E1에 통합을 촉진했습니다.

미국 육군은 주력전차, 장갑병원 수송차, 공병지원차, 지뢰방호차 등 다양한 장갑차량을 보유하고 있습니다. 이 다양성은 원동기, 기동포병, 경전술차부터 유틸리티 차량에 이르기까지 다양한 트럭에 걸쳐 있습니다. 차량은 70톤이 넘는 무게의 에이브람스 주력 탱크에서 특수 부대가 선호하고 사용하는 1톤 전후의 민첩한 경량 전술 전지형 대응 차량까지 폭넓은 스펙트럼을 보여줍니다. 또한 육군은 덤프 트럭이나 픽업 트럭 등, 시판되고 있는 다양한 차량을 작전상의 요구에 맞추어 창조적으로 재이용하고 있습니다. 합계하면 미국 육군의 차량수는 약 36만 69대. 대조적으로 캐나다 육군은 대형 병수차(HLVW) 차량에 크게 의존하고 있으며 전투 보급, 병원 운송, 화물 운송, 예비 부품 운송이 우수합니다. 이러한 역학은 군의 근대화 노력 증가와 국방 예산의 증강과 함께 시장의 성장을 뒷받침하고 있습니다.

장갑차 업그레이드 및 레트로핏 시장은 반고정적이며 일부 세계 및 현지 기업이 큰 점유율을 차지하고 있습니다. 시장의 주요 기업으로는 General Dynamics Corporation, Rheinmetall AG, KNDS NV, Textron Inc., BAE Systems PLC 등이 있습니다.

시장의 주요 기업은 R&D 투자를 강화하고 장갑차용 최첨단 솔루션의 도입에 주력하고 있습니다. BMC Otomotive는 2023년 4월 Altay MBT의 양산 전 모델 2량을 군에 인도했습니다. 이러한 프로토타입은 본격적인 생산으로 전환하기 전에 1년 반에서 2년의 대규모 현장 시험 단계에 들어가게 됩니다. 주목할만한 것은 BMC Otomotive가 10개의 Altay MBT 샘플을 제작했으며 각각 독특한 엔진 및 변속기 설정을 특징으로 합니다. 2024년부터 2025년 사이에 전차를 연속 생산할 예정이며, 이러한 전진은 향후 수년간 시장을 견인하는 원동력이 될 것으로 보입니다.

The Armored Vehicle Upgrade And Retrofit Market size is estimated at USD 6.80 billion in 2025, and is expected to reach USD 8.28 billion by 2030, at a CAGR of 4.01% during the forecast period (2025-2030).

Armored vehicles, pivotal in land combat, play dual roles in military operations, supporting offense and defense. These vehicles transport military personnel and cargo and engage in active combat, boasting weapons and armor to deflect various projectiles. They are the cornerstone of a nation's military might and are widely utilized across defense forces worldwide.

The armored vehicle upgrade and retrofit market is predominantly driven by the escalating defense budgets globally, leading to frequent upgrades to match evolving battlefield scenarios. Moreover, there is a rising appetite for cost-efficient armor solutions. In 2023, global defense spending, as highlighted by the Stockholm International Peace Research Institute (SIPRI), hit a record high of USD 2,443 billion.

Mounting global terrorism and conflicts are driving a surge in demand for cutting-edge technologies in land vehicles. With many nations facing aging armored fleets, they are increasingly turning to upgrade programs to boost efficiency, lethality, and connectivity.

However, challenges persist, especially with the high R&D costs and the swift advancements in weaponry, such as high explosive anti-tank (HEAT) warheads, which can potentially reduce the effectiveness and lifespan of armored systems. While these hurdles pose a threat to market expansion, the ongoing global efforts to modernize aging armored vehicles are poised to propel the market in the coming years.

An infantry fighting vehicle (IFV), also known as a mechanized infantry combat vehicle (MICV), is an armored vehicle designed to transport infantry into battle and provide direct-fire support. IFVs feature modular add-on armor, including composite or spaced laminated armor, to protect against various munitions. The market's growth is primarily driven by increasing global defense investments and a growing focus on enhancing defense capabilities.

As defense budgets expand, nations are upgrading their aging IFVs' fire control, firepower, and overall functionality. Many are also procuring new vehicles, leading to a surge in demand for vehicle upgrades and retrofits. For instance, in March 2024, the Indian Ministry of Defence finalized a deal with Armoured Vehicles Nigam Limited (AVNL) for 693 armament upgrades of infantry combat vehicles BMP2 to BMP2M. This extensive upgrade, categorized as Buy (Indian-Indigenously Designed, Developed, and Manufactured), includes Night Enablement, a Gunner Main Sight, a Commander Panoramic Sight, and a Fire Control System (FCS) with an Automatic Target Tracker.

In March 2024, Nexter showcased its latest VBCI infantry fighting vehicle to Qatar, aligning with the latter's military modernization plans post-2030. The presentation hinted at potential contracts for the VBCI II, a refined version tailored for the French armed forces. Additionally, in December 2022, Sweden secured a USD 1.37 billion deal with the Slovak Republic's Ministry of Defense for 152 CV9035 infantry fighting vehicles from BAE Systems. Marketed as the CV90MkIV, the CV9035 boasts advanced capabilities and digital technology. With enhanced battlefield speeds, superior handling, and a forward-looking electronic architecture, the vehicle is well-equipped to meet the evolving demands of modern battlefields. These ongoing modernization efforts, alongside anticipated IFV upgrade programs, are poised to drive the segment's growth in the coming years.

In the market for armored vehicle upgrades and retrofits, North America is poised for supremacy in the years ahead. This dominance is rooted in the region's robust defense spending, a substantial existing fleet of armored vehicles, and escalating investments in military modernization, particularly from the US and Canada. A 2022 report by the Stockholm International Peace Research Institute (SIPRI) highlighted the US's dedication, with its defense budget reaching a staggering USD 916 billion in 2023. This surge in defense funding spurred numerous upgrade and retrofit initiatives, enhancing the nation's defense capabilities. For example, in May 2024, the US Army sealed a USD 37 million deal with Elbit Systems to boost the next-gen Bradley fighting vehicle. General Dynamics Ordnance and Tactical Systems facilitated the integration of Elbit's Iron Fist Active Protection System (APS) into the Bradley M2A4E1.

The US Army boasts a diverse armored vehicle fleet, including main battle tanks, armored personnel carriers, engineering support vehicles, and mine-protected variants. This diversity extends to prime movers, mobile artillery, and a range of trucks, from light tactical to utility vehicles. The fleet showcases a broad spectrum, from the hefty 70-plus ton Abrams main battle tank to the agile Lightweight Tactical All-Terrain Vehicle favored by Special Forces, weighing around one ton. Additionally, the Army creatively repurposed various commercially available vehicles, like dump trucks and pickups, to meet its operational needs. In total, the US Army's vehicle count was around 360,069 units. In contrast, the Canadian Army heavily relies on its Heavy Logistics Vehicle Wheeled (HLVW) fleet, excelling in combat supply, troop, cargo, and spare part transportation. These dynamics, coupled with heightened military modernization efforts and bolstered defense budgets, are propelling the market's growth.

The armored vehicle upgrade and retrofit market is semi-consolidated, with several global and local players holding significant shares. Some of the key players in the market are General Dynamics Corporation, Rheinmetall AG, KNDS NV, Textron Inc., and BAE Systems PLC.

Key market players are intensifying their R&D investments, focusing on introducing state-of-the-art solutions for armored vehicles. BMC Otomotive, in April 2023, handed over two pre-production models of its Altay MBT to the military. These prototypes are set for an extensive 1.5-2 year field testing phase before moving into full-scale production. Noteworthy is BMC Otomotive's creation of 10 Altay MBT samples, each featuring unique engine and transmission setups. With a tentative timeline for serial tank production between 2024 and 2025, these strides are primed to drive the market in the coming years.