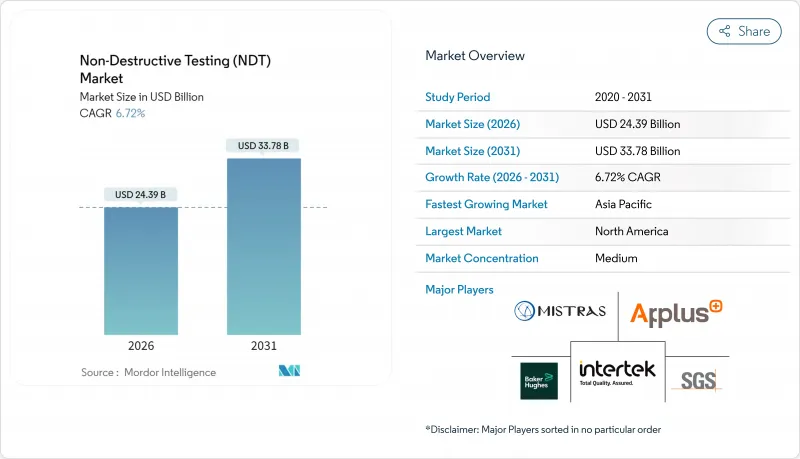

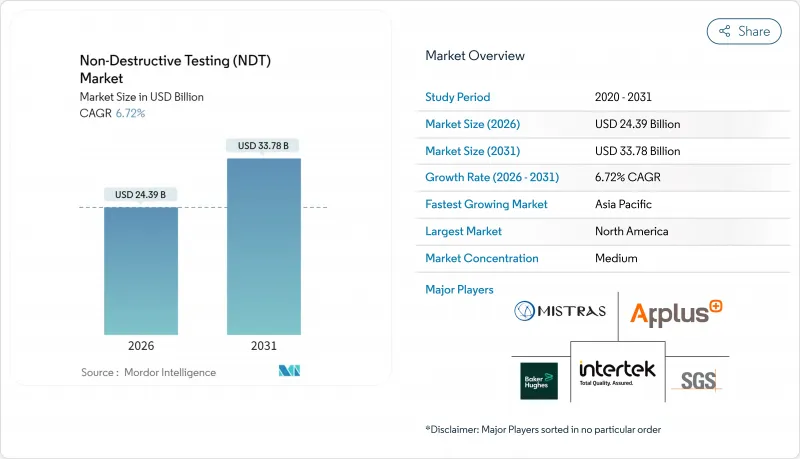

비파괴 검사(NDT) 시장은 2025년에 228억 6,000만 달러로 평가되었고, 2026년 243억 9,000만 달러에서 2031년까지 337억 8,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 6.72%를 나타낼 전망입니다.

전 세계적으로 강화된 안전 규정, 노후 자산의 가속화된 교체, AI 기반 진단 플랫폼의 급속한 도입으로 비파괴 평가가 사후적 결함 탐지에서 예측적 자산 관리로 전환되고 있습니다. 북미와 유럽의 규제 기관들은 이제 압력 용기, 파이프라인, 항공기 구조물, 원자로에 대한 더 빈번한 검사를 의무화하여 꾸준한 수요 기반을 마련하고 있습니다. 한편, 인공지능 기반 분석은 검사 주기를 단축하고 데이터 처리 시간을 대폭 줄이며 소프트웨어 공급업체에게 새로운 구독형 수익원을 창출합니다. 서비스 제공업체들은 휴대용 위상 배열 장비 및 디지털 방사선 촬영 장비와 클라우드 분석을 결합하여 생산성을 높이고 총 검사 비용을 절감하는 방식으로 대응하고 있습니다. 통합 업체들이 하드웨어, 소프트웨어, 인증된 인력을 묶어 최종 사용자의 규정 준수를 간소화하는 턴키 솔루션으로 제공하기 위해 노력함에 따라 인수합병을 통한 시장 통합이 가속화되고 있습니다.

미국기계공학회(ASME), 원자력규제위원회(NRC), 연방항공청(FAA) 등 규제 기관들은 2024년 규정을 개정하여 압력 용기, 원자로 구성품, 복합재 항공기 부품에 대한 비파괴 검사의 빈도와 포괄성을 강화했습니다. 이러한 강화된 규정은 구매 결정을 선택적 지출에서 의무적 규정 준수로 전환시켜 경기 침체기에도 기본 수요를 보장합니다. 고온 압력 용기에 대한 위상 배열 초음파의 의무적 사용과 디지털 기록 보관 규정이 결합되면서 자산 소유자들은 장비 군을 현대화하고 있습니다. 서비스 제공업체는 수익 예측 가능성을 높이는 다년간 검사 계약으로 혜택을 보며, 장비 공급업체는 규정 준수 업데이트와 연계된 교체 판매 가속화와 반복적 소프트웨어 구독을 통해 이득을 얻습니다. 추가 관할권이 미국 및 유럽 표준과 조화를 이루면서 이 촉진요인의 영향력은 확대되어 비파괴 검사 시장의 장기적 성장 추세를 강화하고 있습니다.

북미 교량의 40% 이상이 설계 수명을 초과했으며, 1960년대 설치된 파이프라인은 중대한 검사 주기에 진입하고 있습니다. 1970년대 가동된 원자력 발전소의 수명 연장 프로그램은 면허 갱신 전 광범위한 초음파 용기 스캔을 요구합니다. 이에 따른 검사 적체는 고처리량 검사 서비스, 지능형 피깅 도구, 자동화된 데이터 분석에 대한 기록적 수요를 촉진합니다. 인프라 결함은 사회적·경제적 비용이 막대하기 때문에 규제 당국은 자산 소유자가 연기할 수 없는 엄격한 검사 일정을 시행합니다. 이러한 장기적 추세는 비파괴 검사 서비스 수익의 장기적 가시성을 보장하며 현장 생산성을 향상시키는 휴대용 장비 투자를 촉진합니다. 아시아태평양 지역 유틸리티 기업들도 유사한 업그레이드 주기에 착수함에 따라 글로벌 수요 곡선은 계속 가팔라지고 있습니다.

완전 자동화 위상 배열 스캐너는 20만-50만 달러에 달하는 가격으로 중소 규모 서비스 업체의 예산을 압박합니다. 연간 교정, 소프트웨어 라이선싱, 교육 비용이 추가되어 총 소유 비용이 두 배로 증가하며 손익분기점 도달 시기를 연장시킵니다. 인건비가 낮은 신흥 시장에서는 운영사들이 주기 시간이 더 길더라도 수동 검사를 선호하는 경우가 많아, 고수익 자동화 솔루션의 시장 침투가 지연됩니다. 자본 규모가 부족한 중소 벤더들은 경쟁에서 밀려 시장 통합이 가속화되고 있습니다. 금융 도구 또는 장비 리스 모델이 성숙해질 때까지, 특히 고부가가치 에너지 및 항공우주 부문 외에서는 이러한 제약이 도입을 계속 저해할 것입니다.

서비스 부문이 2025년 매출의 78.90%를 차지했으나, 소프트웨어 부문은 연평균 11.71% 성장률로 확대될 전망이며, 이는 비파괴 검사 시장에 새로운 가치 창출 곡선을 제시합니다. AI 기반 이미지 인식 엔진은 테라바이트 규모의 스캔 데이터를 단 몇 분 만에 실행 가능한 유지보수 인사이트로 변환하여 서비스 경제성을 시간당 청구에서 성과 기반 가격 책정으로 재편하고 있습니다. 장비 공급업체들은 이제 하드웨어와 클라우드 분석을 번들로 제공하며, 초기 판매를 넘어 수익을 확장하는 연간 구독 서비스를 포함시키고 있습니다. 엣지 컴퓨팅 모듈의 급증은 검사 현장에서 실시간 분석을 가능하게 하여 데이터 주권 문제를 완화하고 대역폭 비용을 절감합니다.

소프트웨어의 부상은 현장 노동을 대체하지 않으면서 업무 배분을 재정의합니다. 기술자는 더 높은 품질의 데이터를 신속하게 수집하는 반면, 중앙 분석가는 AI가 생성한 경고 신호를 검증하고 규정 준수 준비가 완료된 보고서를 작성합니다. 이 모델은 현장 초과 근무를 줄이고 장비 가동률을 높이며 플랫폼 공급업체에게 새로운 반복 수익을 창출합니다. 규제 기관이 디지털 서명 보고서를 수용함에 따라 비파괴 검사 산업은 속도와 감사 가능성을 동시에 확보하며, 현대 검사 워크플로우에서 소프트웨어의 중추적 역할을 부각시킵니다.

초음파 방식은 용접부, 단조품, 복합재 검사의 다용도성 덕분에 2025년 비파괴 검사 시장 점유율의 27.95%를 차지했습니다. 고급 위상 배열 구성은 장비 분해 없이도 신속한 부식 매핑과 체적 결함 측정이 가능합니다. 그러나 항공우주 복합재 및 적층 제조 부품에 사용되는 전도성 재료의 미세 균열 탐지 능력 덕분에 와전류 검사는 2031년까지 연평균 9.07% 성장할 것으로 예상됩니다.

개선된 프로브 설계와 다중 주파수 어레이는 이제 더 깊은 침투력과 빠른 스캐닝을 제공하여 초음파가 전통적으로 강세를 보였던 얇은 벽 검사 분야에서 도전장을 내밀고 있습니다. 한편, 디지털 방사선 촬영은 파이프라인 용접 검증에서 여전히 중요한 역할을 수행하며, 자성 입자 검사는 강자성 부품의 표면 결함 탐지에 필수적입니다. 이러한 상호 보완적인 방법들은 자산 소유자가 결함 유형과 재료에 따라 속도, 감도, 규제 수용성을 조화시킨 균형 잡힌 도구 세트를 활용할 수 있도록 보장합니다.

북미는 성숙한 규제 감독, 노후화된 인프라, AI의 조기 도입에 힘입어 2025년 36.30%의 점유율을 유지했습니다. 이 지역의 압력 용기, 파이프라인, 항공기 구조물의 대규모 설치 기반은 꾸준한 검사 물량을 보장하는 한편, 석유 및 가스 운영사들은 자산 수명 연장을 위해 첨단 로봇 피깅(pigging)에 투자하고 있습니다. 원자력 발전소 수명 연장 프로그램을 지원하는 정부 보조금 역시 체적 초음파 스캐닝 수요를 유지합니다.

유럽은 약간 뒤처지지만, 엄격한 안전 지침과 그린딜 하의 재생에너지 프로젝트 추진이라는 유럽연합의 정책 혜택을 받습니다. 풍력 터빈 블레이드 검사, 복합재 로터 결함 모니터링, 수소 파이프라인 시범 사업이 지역 비파괴 검사 시장을 종합적으로 견인합니다. 프랑스와 영국의 원자로 지속적인 업그레이드는 장기 검사 계약 추가를 촉진하고 있으며, ESG(환경·사회·지배구조) 문제로 인해 유해 폐기물 양을 줄이기 위한 필름에서 디지털 방사선 촬영으로의 전환이 가속화되고 있습니다.

아시아태평양 지역은 중국과 인도의 대규모 인프라 프로젝트와 확장되는 항공우주 및 반도체 제조업에 힘입어 7.61%의 연평균 성장률(CAGR)로 가장 강력한 성장 모멘텀을 보이고 있습니다. 일본과 한국 정부는 현지 규정을 ASME 및 IEC 표준에 맞추어 검사 기준을 강화하고 있습니다. 신흥 동남아시아 경제국들은 규정 준수를 위해 국제 인증 기관에 의존하는 경우가 많아 글로벌 기업들에게 서비스 기회가 열리고 있습니다. 일대일로 파이프라인 네트워크는 지능형 피깅 수요를 촉진하며, 지역 내 신규 조선소들은 대형 선체 용접부에 대한 자분 및 위상 배열 검사를 필요로 합니다.

중동 및 아프리카는 해양 석유·가스 투자와 석유화학 플랜트 확장으로 이익을 얻고 있습니다. 홍해와 서아프리카 해상 프로젝트는 심해 인증 검사 기술을 요구합니다. 일부 국가의 정치적 불안은 프로젝트 지연을 초래해 지역 전망에 변동성을 주지만, 압축된 일정 하에 프로젝트가 진행될 경우 프리미엄 마진을 창출하기도 합니다. 라틴아메리카는 브라질의 프리솔트 개발과 멕시코 정유소 현대화를 중심으로 완만한 성장을 기록하며, 양쪽 모두 고사양 비파괴 검사를 필요로 합니다.

The non-destructive testing market was valued at USD 22.86 billion in 2025 and estimated to grow from USD 24.39 billion in 2026 to reach USD 33.78 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031).

Heightened global safety rules, the accelerating replacement of aging assets, and the rapid adoption of AI-enabled diagnostic platforms are shifting non-destructive evaluation from reactive fault finding toward predictive asset management. Regulatory agencies in North America and Europe now mandate more frequent inspections for pressure vessels, pipelines, aircraft structures, and nuclear reactors, anchoring a steady demand floor. Meanwhile, AI-driven analytics shorten inspection cycles, slash data-processing time, and create new subscription revenue streams for software vendors. Service providers are responding by pairing portable phased-array and digital radiography equipment with cloud analytics, raising productivity and lowering total inspection costs. Consolidation through mergers and acquisitions is intensifying, as integrated players seek to bundle hardware, software, and certified labor into turnkey offerings that simplify compliance for end users.

Regulatory bodies, such as the American Society of Mechanical Engineers, the Nuclear Regulatory Commission, and the Federal Aviation Administration, updated their codes in 2024, which now require more frequent and comprehensive non-destructive examinations of pressure vessels, reactor components, and composite aircraft parts. These tighter rules have shifted purchasing decisions from discretionary spending to mandatory compliance, guaranteeing baseline demand even in downturns. The mandatory use of phased-array ultrasonics for high-temperature pressure vessels, combined with digital record-keeping rules, is prompting asset owners to modernize their equipment fleets. Service providers benefit from multiyear inspection contracts that improve revenue predictability. Equipment vendors win through accelerated replacement sales and recurring software subscriptions tied to code compliance updates. As additional jurisdictions align with U.S. and European standards, the driver's influence broadens, reinforcing a long-term growth thrust for the non-destructive testing market.

More than 40% of North American bridges now exceed design life, while pipelines installed during the 1960s are approaching critical inspection intervals. Life-extension programs for nuclear plants commissioned in the 1970s require extensive ultrasonic vessel scans to be performed before license renewal. The resulting inspection backlog fuels record demand for high-throughput testing services, intelligent pigging tools, and automated data analytics. Because infrastructure failures carry high social and economic costs, regulators enforce strict inspection calendars that asset owners cannot defer. This secular trend secures long-term visibility for non-destructive testing service revenue and spurs investment in portable equipment that improves site productivity. As Asia-Pacific utilities embark on similar upgrade cycles, global demand curves continue to steepen.

Fully automated phased-array scanners can cost USD 200,000-500,000, a price point that strains the budgets of small and mid-sized service firms. Annual calibration, software licensing, and training double the lifetime ownership cost, extending breakeven periods. In emerging markets with lower labor costs, operators often favor manual inspection despite longer cycle times, which slows the penetration of high-margin automated solutions. Smaller vendors lacking capital scale struggle to compete, accelerating market consolidation. Until financing tools or equipment leasing models mature, this restraint will continue to dampen uptake, especially outside high-value energy and aerospace segments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services held 78.90% of 2025 revenue, yet the software slice is forecast to expand at 11.71% CAGR, setting a new value-creation arc for the non-destructive testing market. AI-driven image-recognition engines convert terabytes of scan data into actionable maintenance insights within minutes, reshaping service economics from hourly billing toward outcome-based pricing. Equipment vendors now bundle cloud analytics with hardware, embedding annual subscriptions that stretch revenue beyond the initial sale. The surge in edge-computing modules enables real-time analytics at inspection sites, easing data sovereignty concerns and reducing bandwidth costs.

Software's rise does not eclipse field labor but redefines task allocation. Technicians capture higher-quality data more quickly, while centralized analysts validate AI-generated flags and produce compliance-ready reports. The model trims field overtime, increases fleet utilization, and creates new recurring revenue for platform providers. As regulatory bodies accept digitally signed reports, the non-destructive testing industry gains both speed and auditability, underscoring the pivotal role of software in modern inspection workflows.

Ultrasonic methods accounted for 27.95% of the 2025 non-destructive testing market share, owing to their versatility in inspections of welds, forgings, and composites. Advanced phased-array configurations enable rapid corrosion mapping and volumetric flaw sizing without the need for dismantling equipment. Yet, eddy-current testing is expected to grow at a 9.07% CAGR through 2031, driven by its ability to detect micro-cracks in conductive materials used in aerospace composites and additive-manufactured parts.

Improved probe design and multi-frequency arrays now deliver deeper penetration and faster scanning, challenging ultrasonics' historical stronghold in thin-wall inspections. Meanwhile, digital radiography continues to play a critical role in pipeline weld validation, and magnetic particle testing remains indispensable for detecting surface flaws in ferromagnetic components. Together, these complementary methods ensure that asset owners deploy a balanced toolbox that blends speed, sensitivity, and regulatory acceptance, depending on the defect type and material.

The Global Non-Destructive Testing (NDT) Market Report is Segmented by Component (Equipment, Software, Services, and Consumables), Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, and More), Technique (Traditional/Conventional and AI-Enabled), End-User Industry (Oil and Gas, Power Generation, Aerospace, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained a 36.30% share in 2025, driven by mature regulatory oversight, aging infrastructure, and early adoption of AI. The region's large installed base of pressure vessels, pipelines, and aircraft structures ensures steady inspection volumes, while oil and gas operators fund advanced robotic pigging to extend the life of their assets. Government grants supporting nuclear plant life-extension programs also sustain demand for volumetric ultrasonic scanning.

Europe trails slightly, yet benefits from rigorous safety directives and the European Union's push for renewable energy projects under the Green Deal. Wind-turbine blade inspections, composite rotor defect monitoring, and hydrogen pipeline pilots collectively bolster the regional non-destructive testing market. Ongoing upgrades to nuclear reactors in France and the United Kingdom are driving the addition of long-term inspection contracts, while ESG concerns are accelerating the shift from film to digital radiography to reduce hazardous-waste volumes.

The Asia-Pacific region is delivering the strongest forward momentum, with a 7.61% CAGR, driven by massive infrastructure projects in China and India, as well as expanding aerospace and semiconductor manufacturing. Governments in Japan and South Korea align local codes with ASME and IEC standards, thereby raising the rigor of inspections. Emerging Southeast Asian economies often rely on international certifiers for compliance, presenting opportunities for service to global firms. Belt and Road pipeline networks drive demand for intelligent pigging, while new shipyards across the region require magnetic particle and phased-array inspections of large hull welds.

The Middle East and Africa gain from offshore oil and gas investments and petrochemical plant expansions. Subsea projects in the Red Sea and offshore West Africa call for deepwater-qualified inspection technologies. Political instability in certain countries can delay projects, injecting volatility into regional forecasts but also producing premium margins when projects advance under compressed timelines. Latin America records moderate growth, centered on Brazilian pre-salt developments and Mexican refinery upgrades, both of which require high-specification non-destructive examinations.