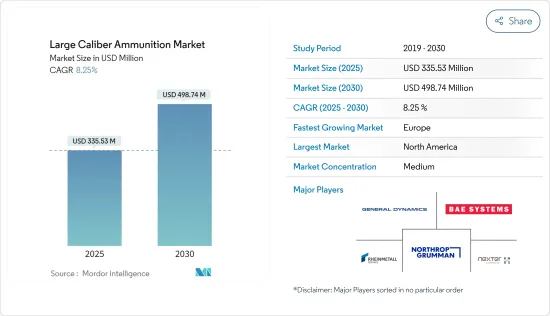

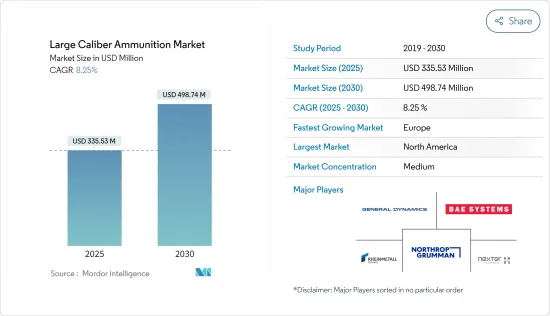

대구경탄약 시장 규모는 2025년에 3억 3,553만 달러, 2030년에는 4억 9,874만 달러에 달할 것으로 예측됩니다. 예측기간(2025년-2030년) CAGR은 8.25%를 나타낼 전망입니다.

COVID-19의 팬데믹이 시장에 미치는 영향은 극히 적었습니다. 이는 주로 세계 주요 국가의 국방비가 증가했기 때문입니다. 러시아와 우크라이나 사이에서 진행 중인 전쟁은 무기와 탄약 사용 증가로 이어지고, NATO 국가로부터의 방위 지출 증가는 유럽 전체 시장 성장을 가속하고 있습니다.

세계 각국의 정부는 육해공의 국경 경비, 민간인 보호, 군의 살상력을 강화하기 위해, 야포, 박격포, 함포 등의 무기에 대한 투자를 실시했습니다.

고속 발사, 레이저 유도 시스템, 적 아군 식별 및 정밀 조준 기술에 대한 요구 증가 등의 대폭적인 기술 진보가 GPS 대응 포탄 및 박격포탄 시장 성장을 뒷받침하고 있습니다. 정치적 갈등, 테러리즘, 국경을 넘어서는 갈등이 증가함에 따라 부대의 신속한 전개에 대한 필요성이 증가하고 동시에 전장에서의 화력 지원 수요가 증가하고 대구경 탄약 시장 성장을 가속하고 있습니다.

국제전략정세의 큰 변화에 따라 국제안보시스템의 구성은 패권주의, 단독주의, 파워폴리틱스의 고조에 의해 손상되어 현재 진행중인 여러 국제분쟁에 박차를 가하고 있습니다.

이 점에서 각국 정부의 가장 흔한 반응은 자국의 안보를 향상시키기 위해 군사비를 늘리는 것입니다. 지출은 2020년과 2021년에도 계속 성장했습니다. 지출은 2012년보다 19% 증가했습니다. 미국, 영국, 중국, 인도 등의 군사대국은 군사화력과 방위력의 증강에 주력해 왔습니다.

일부 군은 차량 탑재 무기, 함포 시스템, 박격포, 유탄포 구입 등 군사 화력 능력의 업그레이드에 많은 자원을 투입하고 있습니다. 이 때문에 관련 탄약 수요가 세계적으로 높아지고 있습니다. 국방군은 향후 수년간 8,000만 유로 상당의 대구경 및 소구경 탄약을 수령한다고 발표했습니다.

미국은 세계 최대의 국방지출국입니다.미국의 국방비는 2020년의 7,782억 3,000만 달러에서 2021년에는 8,010억 달러에 달했으며, 거의 2.9% 증가했습니다. 예산권은 2020년 7,050억 달러에서 170억 달러 증가한 약 7,220억 달러로, 2023년도 대통령 예산 요구는 7,730억 달러였습니다.

2022년 국방차관 보고서에서 미군은 2023년도 미사일과 군수품에 247억 달러의 예산을 요구했습니다. 그 주요 목적은 고급 전투에 필수적인 수요가 높은 무기와 군수품에 대해 이용 가능한 산업 능력을 충분히 활용하고 높은 생산률로 조달함으로써 부대의 전반적인 살상력을 높이는 것을 주요 목표로 하고 있습니다. 또한 2023년도에는 방위 예산의 9%를 미사일과 탄약 할당에 요청되었습니다. 탄약 포트폴리오에는 총알, 카트리지, 박격포, 폭약, 포탄 등 주로 지상부대가 필요로 하는 것이 포함되었습니다. 이러한 방위 플랫폼과 관련 탄약 조달 계획은 예측 기간 동안 북미에서 조사된 시장을 견인할 것으로 예상됩니다. 예를 들어 미국은 우크라이나에 제공하기 위해 한국의 무기 제조업체에서 10만발의 155mm 곡사포탄을 구입할 예정입니다.

대구경 탄약 시장은 다양한 군에 공급되는 탄약의 소수의 기존 기업과 현지 제조업체에서 적당히 통합되어 있습니다. 유명한 시장 기업으로는 General Dynamics, BAE Systems, Northrop Gramman, Line Metal AG, Nexter Group KNDS 등이 있습니다. 설계, 재료, 살상력 등의 혁신이 시장을 견인하고 있습니다. 비공개회사는 현지 민간·정부계 탄약회사의 강화에 주력하고 있습니다. 사우디아라비아, 아랍에미리트(UAE), 중국, 인도 등의 국가들은 각 군의 필요성을 충족시키기 위해 현지 제조 회사를 장려하고 현지 기업의 시장 점유율 확대에 기여하고 있습니다.

예를 들어, 2022년 5월, 미국 육군은 120mm 전차 훈련 탄약을 조달하기 위한 2개의 계약을 발표했습니다. M865A1 신제작운동에너지탄, M1002탄약에 대해 6,670만 달러 상당의 계약을 노스롭 그라만에 발주했습니다. M1002 신제조 다목적 전차 훈련탄에 대해 5,080만 달러의 계약을 제너럴 다이내믹스 코퍼레이션에 주문했습니다.

The Large Caliber Ammunition Market size is estimated at USD 335.53 million in 2025, and is expected to reach USD 498.74 million by 2030, at a CAGR of 8.25% during the forecast period (2025-2030).

The COVID-19 pandemic had a negligible impact on the market. This is mainly attributed to the increase in defense expenditure across major world powers. The military expenditure as of 2021 was valued at USD 2.1 trillion, with the United States spending the highest, followed by China and India. Furthermore, the ongoing war between Russia and Ukraine leads to the rising use of weapons and ammunition, and growing defense expenditure from NATO countries drives market growth across Europe. Thus, the growth in geopolitical conflicts among the countries of the region played a major role in driving defense spending toward large-caliber weapons and ammunition, driving the market.

Governments across the world are making investments in weapons, such as field artillery, mortars, naval guns, etc., to strengthen the land and maritime border security, civilian protection, and lethality of armed forces. These weapons are a cost-effective option over costly missiles and rockets used for ground attack operations. These factors are driving the demand for large-caliber ammunition globally.

Significant technological advancements, such as high-speed projectile firing, laser guidance systems, and the increasing need for friend or foe identification and precision targeting technology, drive the market growth for GPS-enabled artillery and mortar shells. Due to increased political disputes, terrorism, and cross-border conflicts, the need for rapid deployment of forces has increased, simultaneously increasing the demand for firepower support on the battlefield, driving the market growth for large-caliber ammunition.

Owing to profound changes in the international strategic landscape, the configuration of international security systems has been undermined by the growing hegemonism, unilateralism, and power politics, which have fuelled several ongoing global conflicts. Uncertainties in territorial rights, political tensions, and the quest for universal dominance among the military powerhouses are the major causes disturbing the geopolitical scenario.

In this regard, the most common reaction of the governments is to increase their military spending to improve security in their respective countries. Despite the economic impact of the COVID-19 pandemic, global defense expenditure continued to grow in 2020 and 2021. According to SIPRI, the global military expenditure in 2021 rose to USD 2113 billion, an increase of 7% from 2020. billion. Global spending in 2021 was 19% higher than in 2012. The five largest military spenders in 2021 were the United States, China, India, the United Kingdom, and Russia, which accounted for 62% of world military spending. Military powerhouses, such as the United States, United Kingdom, China, and India, have been focused on augmenting their military firepower and defensive capabilities. The colossal budgets also facilitate the R&D of new weapon and ammunition systems to engage hostile forces and neutralize threats.

Several armed forces have invested significant resources in upgrading their military firepower capabilities, including purchasing vehicle-mounted weapons, naval gun systems, mortars, and howitzers. This has been increasing the demand for related ammunition globally. For instance, in September 2021, the Estonian Defense Forces announced that it would receive large and small caliber ammunition worth EUR 80 million in the next few years. Under the procurement plan, the defense forces would receive large caliber ammunition worth EUR 30 million from eight suppliers over the next four to eight years.

The United States is the largest defense spender in the world. The US defense expenditure increased by almost 2.9% in 2021 to reach USD 801 billion from USD 778.23 billion in 2020. The United States remained the largest defense-spending country in 2021 and represented 38% of global spending. For FY 2022, the Department of Defense's budget authority is approximately USD 722 billion, an increase of USD 17 billion from USD 705 billion in 2020, while the FY 2023 President's budget request was USD 773 billion for the DoD. The budget primarily aims at modernizing capabilities in the air, maritime, and land warfighting domains and on innovations to strengthen the country's competitive advantage.

In the 2022 report of the Under Secretary of Defense, the United States military has requested a budget of USD 24.7 Billion in FY 2023 for missiles and munitions with a prime objective to increase the overall lethality of the force by procuring at high rates of production, fully utilizing the available industrial capacity for high demand weapons and munitions that are essential for the high-end combat. Furthermore, in FY 2023, 9% of the defense budget is requested to allocate toward missiles and munitions. The ammunition portfolio includes bullets, cartridges, mortars, explosives, and artillery projectiles needed mostly by ground forces. Such procurement plans for defense platforms and related ammunition are anticipated to drive the market studied in North America during the forecast period. For instance, the United States plans to buy 100,000 rounds of 155mm howitzer ammunition from South Korean arms manufacturers to provide to Ukraine.

The market for large-caliber ammunition is moderately consolidated with few established players and local manufacturers of the ammunition supplied to various armed forces. Some prominent market players are General Dynamics, BAE Systems, Northrop Grumman, Rheinmetall AG, and Nexter group KNDS. Innovations in design, materials, lethality, etc., drive the market. Several companies are focusing on strengthening their local private and government-owned ammunition companies. Countries like Saudi Arabia, the United Arab Emirates, China, and India, are encouraging local manufacturing companies to cater to the need of their respective armed forces, thereby helping the local companies to increase their share in the market studied.

For instance, in May 2022, the United States army announced two contracts to procure 120 mm tank training ammunition. The Army awarded a contract worth USD 66.7 million to Northrop Grumman for 120 mm M1002 multi-purpose tank training rounds, 120 mm M865A1 new production kinetic energy rounds, and M1002 ammunition. Also, the US Army awarded another contract worth USD 50.8 million to General Dynamics Corporation for 120mm M865A1 new production kinetic energy rounds and 120 mm M1002 new production multi-purpose tank training rounds.