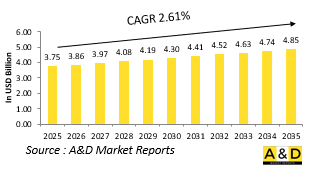

세계의 전차 탄약(120mm 및 125mm) 시장 규모는 2025년에 37억 5,000만 달러로 추정되고, 2035년까지 48억 5,000만 달러로 성장할 것으로 예측되며, 예측 기간인 2025-2035년 연간 평균 성장률(CAGR) 2.61%로 성장할 전망입니다.

120mm 구경 및 125mm 구경의 전차 탄약은 세계 주력 전차의 주무장으로 사용되고 있습니다. 이 탄약들은 특히 중장갑의 위협을 격파하고 사격 우세를 강화하며 공세 및 방어 작전 모두에서 기계화 부대를 지원하도록 설계되었습니다. 구경 120mm는 NATO 가입군에서 널리 사용되지만 구경 125mm는 러시아 또는 소련식 장갑교의를 따르는 국가들에서 일반적입니다. 두 구경 모두 고에너지를 공급할 수 있도록 조정되어 있으며 파괴력, 사거리, 범용성의 균형이 잡혀 있습니다. 탄약의 종류에는 철갑탄 핀 안정화 폐기 서봇(APFSDS), 고화력 대전차탄(HEAT), 전장의 다양한 목표에 대응할 수 있는 다목적탄 등이 있습니다. 이러한 탄약에 대한 세계의 수요는 전차의 현대화 계획, 장갑 전투의 증가 및 하이브리드 전쟁에서 육상 전투 차량의 지속적인 관련성에 의해 계속 안정되고 있습니다. 이러한 탄약은 전통적인 전장 지배뿐만 아니라 분쟁 지역에서의 억제력 유지에도 필수적입니다. 지정학적 역학이 변화하고 육상전이 전략적 우위를 되찾는 가운데 120mm와 125mm 전차 탄약은 전술적 균형을 유지하고 장갑 유닛과 요새 진지가 관여하는 잠재적인 고강도 분쟁에 대비하기 위해 여전히 필수적입니다.

최근 기술진보로 120mm 및 125mm 전차탄약의 성능과 전술적 가치가 대폭 향상되었습니다. 가장 주목할 만한 개발 중 하나는 운동에너지 관통탄의 개량으로 열화 우라늄 합금이나 고도의 텅스텐 복합재 등의 신소재가 보다 높은 철갑 효율을 실현하고 있습니다. 정밀 공학 또한 총구 속도의 향상과 탄도 성능의 안정화에 공헌하고 있으며, 그 결과, 보다 장거리에서의 명중 정밀도와 관통력이 향상되고 있습니다. 이 분야에서는 스마트 탄약이 등장하기 시작했으며 보병에 대한 에어버스트나 구조물 내부에서의 지연 기폭 등 특정 임무 프로파일에 맞춰 폭발 효과를 조정할 수 있는 프로그램 가능한 신관을 갖추고 있습니다. 게다가 화기 관제의 통합으로 탄약은 고도의 조준 시스템과 매끄럽게 인터페이스할 수 있게 되어 초탄의 살상력이 향상되고 있습니다. 불감 탄약의 개발로 사격 중 우발적인 폭발 가능성이 감소하고 전장에서의 생존성이 향상되었습니다. 상대 장갑 플랫폼에 배치된 능동 보호 시스템에 대항하기 위해 열 차폐 및 전자 차폐 기술도 연구되고 있습니다. 그 결과 신세대 전차탄은 살상 능력이 높을 뿐만 아니라 더 적응성이 높고 더 안전하게 사용할 수 있게 되어 있습니다. 이러한 기술 혁신은 일반형과 비대칭형 모두의 위협에 대한 전차의 타당성을 확대함으로써 장갑전의 미래를 만들어 가고 있습니다.

세계 방위 분야에서 120mm 및 125mm 전차 탄약의 지속적인 중요성과 개발이 형성되고 있는 배경에는 몇 가지 요인이 있습니다. 가장 큰 것이 장갑함대의 근대화이며, 많은 나라가 보다 효과적인 화력으로 주력 전차를 강화하려고 하고 있습니다. 새로운 설계의 전차가 취역하거나 오래된 플랫폼이 업그레이드됨에 따라 강화된 포 시스템이나 사격 통제 능력에 맞는 탄약의 수요도 병행해서 높아지고 있습니다. 또, 위협 환경의 진화에 수반해, 특히 반응 장갑이나 고도의 방어 수단을 갖춘 요새화 차량에 대한 대장갑 효과의 향상이 요구되고 있습니다. 시가지전이나 하이브리드전의 시나리오에서는 탁 트인 전장에서 좁은 시가지까지 복잡한 지형에서 효과적으로 활동할 수 있는 멀티롤 탄약에 대한 관심이 높아집니다. 훈련과 즉응 태세는 더욱 수요에 공헌하고, 군대는 전투 상황을 시뮬레이션하는 비용 대비 효과가 높으며, 게다가 현실적인 연습탄을 요구하고 있습니다. 국내 생산 능력의 유지나 해외 공급업체에 대한 의존도 저감의 필요성이라고 하는 산업 기반을 향한 염려도, 탄약 제조나 기술 혁신에의 투자를 뒷받침하고 있습니다. 또한 다양한 지역에서 지정학적 긴장이 높아짐에 따라 전략적 비축과 신속한 보충 능력이 필수적입니다. 이러한 요인들을 종합하면 120mm와 125mm 탄약은 작전, 전략, 로지스틱스를 고려한 것으로 지상부대의 대비로서 중요한 요소가 되고 있습니다.

120mm와 125mm 전차탄약의 생산, 배치, 진화를 형성하는데 있어 지역의 방위 역학이 큰 역할을 하고 있습니다. 유럽에서는, 통상형 억제력의 부활과 영토 방위에 대한 주목의 고조가, 특히 Leopard 전차나 Abrams 전차와 같은 플랫폼간에 표준화를 진행시키고 있는 NATO 가맹국 사이에서, 120mm 탄약에 대한 새로운 투자를 재촉하고 있습니다. 동유럽 국가에서는 소련 시대의 구식 전차를 아직도 운용하고 있는 나라도 있습니다만, 새로운 제조 기술을 도입하면서 125mm 탄약의 비축을 유지해, 현대화를 계속하고 있습니다. 아시아에서는, 육상에서의 긴장의 고조와 국경 경비의 우선 사항이, 양구경의 왕성한 수요를 뒷받침하고 있어, 지역의 주요국이 전략적 독립성을 확보하기 위해서 국내 생산에 투자하고 있습니다. 높은 작전 템포와 다양한 장갑 차량을 특징으로 하는 중동에서는 120mm와 125mm의 양구경의 지속적인 조달이 이루어지고 있으며, 대부분의 경우 시가지와 탁 트인 지형이 혼재하는 전투 환경용으로 조정되고 있습니다. 북미는 품질과 혁신성을 중시하고 차세대 전차 플랫폼의 능력에 걸맞은 선진적인 120mm 탄약에 중점을 두고 있습니다. 한편, 아프리카나 라틴 아메리카와 같은 지역에서는 잉여 물자와 현지 파트너 간에 조달의 균형을 맞추면서 혼성 함대를 운용하는 경우가 많습니다. 어느 지역에서나 전략적 요구와 전장에서의 경험이 이러한 전차 탄약의 조달, 개량, 배치 방법을 형성하고 있습니다.

Elbit Systems Ltd.는 오늘 NATO 회원국에 전차탄약을 공급하는 약 1억 1,500만 달러의 계약을 획득했다고 발표했습니다. 계약 기간은 3년이고 연장 옵션도 있습니다. Elbit Systems Land의 전차 탄약 시리즈는 NATO와 MIL-STD의 두 규격을 모두 충족하여 장갑부대의 화력과 작전 능력을 대폭 강화합니다. 105mm 탄약 시리즈는 M68, L7, F1 및 유사한 시스템을 포함한 모든 NATO 표준 105mm 포에서의 사용이 인정되고 있습니다. 120mm 시리즈는 Merkava 3 및 4, Leopard 2A4/A5/A6, M1A1/A2 Abrams, K1A1/A2, K2, ARIETE, M60A3 전차 등의 플랫폼에서 사용되는 NATO 120mm 활강포용으로 인증되었으며 L44/L55 활강포 시스템과 호환됩니다. 게다가 125mm 탄약은 T-72 및 T-90 주력 전차에서 사용이 인정되고 있으며, 100mm 시리즈는 T-54, T-54B, T-55 플랫폼용으로 설계되었습니다. 엘빗 시스템즈 랜드사는 제공하는 탄약의 높은 안전성, 신뢰성, 품질 기준을 강조하고 있습니다.

본 보고서에서는 세계의 전차 탄약(120mm 및 125mm) 시장에 대해 조사했으며, 10년간의 부문별 시장 예측, 기술 동향, 기회 분석, 기업 프로파일, 국가별 데이터 등을 정리했습니다.

지침별

유형별

지역별

이 장에서는 10년간의 전차 탄약 시장 분석을 통해 전차 탄약 시장의 성장, 변화하는 추세, 기술 채용 개요 및 시장 매력에 대한 자세한 개요를 제공합니다.

이 부문에서는 이 시장에 영향을 미칠 것으로 예상되는 상위 10개 기술과 이러한 기술이 시장 전체에 미칠 수 있는 영향에 대해 설명합니다.

이 시장의 10년간 전차 탄약 시장 예측은 위의 전체 부문에서 자세히 설명합니다.

이 부문에서는 지역별 전차 탄약 시장 동향, 촉진요인, 억제요인, 과제, 그리고 정치, 경제, 사회, 기술 등의 측면을 포괄하고 있습니다. 또, 지역별의 시장 예측 및 시나리오 분석도 상세하게 다루고 있습니다. 지역 분석의 마지막 부분에서는 주요 기업의 프로파일링, 공급업체의 정세, 기업 벤치마크 등에 대해 분석하고 있습니다. 현재 시장 규모는 일반 시나리오에 따라 추정되고 있습니다.

북미

촉진요인, 억제요인 및 과제

PEST

주요 기업

공급자 계층의 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

이 장에서는 이 시장에서 주요 방위 프로그램을 다루며 이 시장에서 신청된 최신 뉴스와 특허에 대해서도 설명하고, 국가 수준의 10년간 시장 예측과 시나리오 분석에 대해서도 설명합니다.

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global Tank Ammunition (120mm & 125mm) market is estimated at USD 3.75 billion in 2025, projected to grow to USD 4.85 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 2.61% over the forecast period 2025-2035.

Tank ammunition in the 120mm and 125mm calibers serves as the primary armament for main battle tanks around the world. These rounds are specifically designed to defeat heavily armored threats, reinforce fire superiority, and support mechanized forces in both offensive and defensive operations. The 120mm caliber is widely used by NATO-aligned forces, while the 125mm variant is more common among countries that follow Russian or Soviet-style armor doctrines. Both calibers are tailored for high-energy delivery, offering a balance between destructive power, range, and versatility. Ammunition types include armor-piercing fin-stabilized discarding sabot (APFSDS), high-explosive anti-tank (HEAT), and multi-purpose rounds capable of engaging various battlefield targets. The global demand for such ammunition remains steady, driven by tank modernization programs, increased armored engagements, and the continued relevance of land combat vehicles in hybrid warfare. These rounds are integral not only for traditional battlefield dominance but also for maintaining deterrent capabilities in contested regions. As geopolitical dynamics shift and land warfare regains strategic prominence, 120mm and 125mm tank ammunition remain essential for maintaining tactical parity and preparing for potential high-intensity conflicts involving armored units and fortified positions.

Recent technological advancements have significantly enhanced the performance and tactical value of 120mm and 125mm tank ammunition. One of the most notable developments is the improvement in kinetic energy penetrators, where new materials such as depleted uranium alloys and advanced tungsten composites offer greater armor-piercing efficiency. Precision engineering has also contributed to increased muzzle velocity and more consistent ballistic performance, which in turn improves accuracy and penetration at longer ranges. Smart munitions are beginning to emerge in this domain, featuring programmable fuses that allow crews to tailor explosive effects for specific mission profiles, such as airburst over infantry or delayed detonation inside structures. Additionally, fire control integration now enables ammunition to interface seamlessly with advanced targeting systems, improving first-shot lethality. The development of insensitive munitions has increased battlefield survivability by reducing the likelihood of accidental detonation under fire. Thermal and electronic shielding technologies are also being explored to counter active protection systems deployed on opposing armor platforms. The result is a new generation of tank rounds that are not only more lethal but also more adaptable and safer to use. These innovations are shaping the future of armored warfare by extending tank relevance against both conventional and asymmetric threats.

Several underlying factors are shaping the sustained importance and development of 120mm and 125mm tank ammunition across global defense sectors. Foremost among these is the modernization of armored fleets, as many nations seek to enhance their main battle tanks with more effective firepower. As newer tank designs enter service or older platforms undergo upgrades, there is a parallel demand for ammunition that matches enhanced gun systems and fire control capabilities. Evolving threat environments also necessitate greater anti-armor effectiveness, particularly against fortified vehicles equipped with reactive armor and advanced defensive measures. Urban and hybrid warfare scenarios drive interest in multi-role ammunition capable of operating effectively in complex terrains, from open battlefields to confined cityscapes. Training and readiness further contribute to demand, with militaries seeking cost-effective yet realistic practice rounds that simulate combat conditions. Industrial base concerns-such as the need to maintain domestic production capabilities or reduce reliance on foreign suppliers-also push investment in ammunition manufacturing and innovation. Moreover, as geopolitical tensions escalate in various regions, strategic stockpiling and rapid replenishment capabilities become essential. Collectively, these drivers reflect a blend of operational, strategic, and logistical considerations that make 120mm and 125mm ammunition a critical component of ground force preparedness.

Regional defense dynamics play a major role in shaping the production, deployment, and evolution of 120mm and 125mm tank ammunition. In Europe, the resurgence of conventional deterrence and increased focus on territorial defense have prompted renewed investment in 120mm ammunition, particularly among NATO members standardizing across platforms like the Leopard and Abrams tanks. Countries in Eastern Europe, some of which still operate legacy Soviet-era tanks, continue to maintain and modernize 125mm stockpiles while integrating newer manufacturing techniques. In Asia, rising land-based tensions and border security priorities drive robust demand for both calibers, with major regional powers investing in domestic production to ensure strategic independence. The Middle East, characterized by high operational tempo and diverse armored fleets, has seen ongoing procurement of both 120mm and 125mm rounds, often tailored for combat environments involving a mix of urban and open terrain. North America emphasizes quality and innovation, focusing on advanced 120mm munitions to match the capabilities of next-generation tank platforms. Meanwhile, regions like Africa and Latin America often operate mixed fleets, balancing procurement between surplus supplies and local partnerships. Across all regions, strategic needs and battlefield experiences shape how these tank munitions are sourced, improved, and deployed.

Elbit Systems Ltd. announced today that it has secured a contract valued at approximately $115 million to supply tank ammunition to a NATO member state. The contract will be executed over a three-year period, with options for extension. Elbit Systems Land's range of tank ammunition meets both NATO and MIL-STD standards and significantly enhances the firepower and operational capabilities of armored units. The 105mm ammunition series is certified for use with all NATO-standard 105mm guns, including the M68, L7, F1, and similar systems. The 120mm series is approved for NATO 120mm smoothbore guns used on platforms such as the Merkava 3 and 4, Leopard 2A4/A5/A6, M1A1/A2 Abrams, K1A1/A2, K2, ARIETE, and M60A3 tanks, and is compatible with L44/L55 smoothbore gun systems. Additionally, the 125mm ammunition is certified for use with T-72 and T-90 main battle tanks, while the 100mm series is designed for T-54, T-54B, and T-55 platforms. Elbit Systems Land emphasizes the high safety, reliability, and quality standards of its ammunition offerings.

By Guidance

By Type

By Region

The 10-year tank ammunition market analysis would give a detailed overview of tank ammunition market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year access control market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional access control market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.