ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

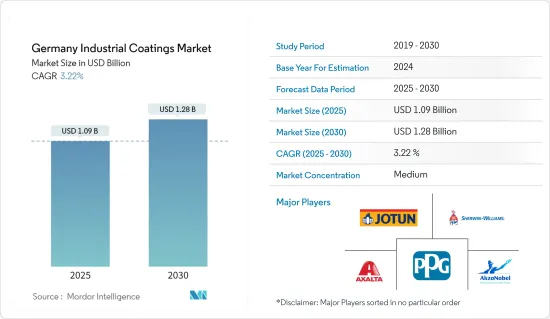

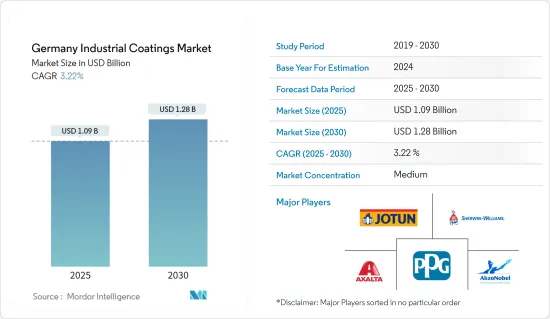

독일의 산업용 코팅 시장 규모는 2025년에 10억 9,000만 달러, 2030년에는 12억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2025년-2030년) CAGR은 3.22%를 나타낼 전망입니다.

COVID-19의 발생으로 산업용 코팅 부문은 부정적인 영향을 받았습니다. 자동차 산업은 2019년부터 2020년까지 판매 부진, 구조적인 감속, 경기 침체를 나타냈습니다.

주요 하이라이트

단기적으로는 산업 인프라 건설 증가와 석유 및 가스 및 석유 화학 산업에서의 수요 증가가 시장 성장을 끌어올릴 것으로 예상됩니다.

그러나, 휘발성 유기 화합물(VOC) 배출에 관한 엄격한 규제가 시장 성장의 방해가 될 것으로 예상됩니다.

그럼에도 불구하고 환경 친화적인 코팅 제품에 대한 수요 증가는 조사 대상 시장에 유리한 성장 기회를 가져올 가능성이 높습니다.

독일의 산업용 코팅 시장 동향

번영하는 석유 및 가스 섹터가 보호 코팅 수요를 높인다.

석유 및 가스산업은 보호도료의 주요한 최종사용자 중 하나입니다.

석유 및 가스산업에서는 정유소로의 석유 및 가스 운송 중 부식을 방지하기 위해 업스트림와 하류 모두에 보호도료를 사용하고 있습니다.

석유 및 가스의 해양 생산은 가장 엄격한 조건의 하나입니다.그 때문에 사용되는 코팅 시스템은 이러한 조건에 대응할 수 있는 것이 아니면 안됩니다.

그러나 러시아와 우크라이나 전쟁에 따라 독일은 우크라이나를 지원하기 위해 다른 제재 조치 외에도 러시아의 가스 파이프라인 '노르드 스트림 2'의 인증 프로세스를 중지하는 조치를 취했습니다.

BP 통계에 따르면, 2021년 독일의 석유 총 소비량은 하루 204만 5,000배럴로, 2020년의 204만 9,000배럴에 비해 0.2% 감소했습니다.

같은 출처에 따르면, 2021년의 천연가스 총소비량은 905억 입방미터로, 2020년의 871억 입방미터로부터 4.2%의 성장을 기록했습니다.

이상과 같은 움직임으로부터, 예측 기간중, 석유 및 가스 산업용 보호 코팅 수요는 증가할 것으로 예상됩니다.

에폭시 수지의 사용량 증가

에폭시 수지는 석유 유래의 강화 폴리머 복합재료입니다.에폭시드 단위를 포함한 반응 프로세스의 결과입니다.이 수지는 바닥이나 금속 용도의 코팅의 내구성을 높이기 위해서, 코팅 용도의 바인더로서 사용됩니다.

에폭시 코팅은 내식성, 내마모성, 내후성이 뛰어나기 때문에 가혹한 사용 환경에 있는 철강 용도에 적합합니다. 또 고온에도 강하기 때문에 고온의 제품을 저장해, 극단적인 열에 노출되는 탱크에도 적합합니다.

공업용 에폭시 코팅은 일반적으로 3층으로 사용됩니다.우선, 아연 프라이머 등의 프라이머를 도포합니다.

에폭시 폴리아미드 코팅은 내습성이 뛰어나 에폭시 마스틱 코팅은 막 두께가 뛰어나, 페놀 에폭시 코팅은 내약품성이 뛰어납니다.

에폭시 수지는 산업용 코팅의 바인더로 자주 사용됩니다.이 코팅은 선박 및 화학 약품 저장 탱크에 사용되는 높은 접착성, 높은 내약품성(내 부식성), 내물리성을 제공합니다.

에폭시 코팅은 그 입수의 용이함으로부터, 수많은 공업 용도에 사용되고 있습니다.

에폭시 코팅의 장점은 몇 가지 있다:

에폭시 코팅은 오래 지속되고 비용 효율적이고 방수성이 있으며 충격에 강합니다.

연마된 콘크리트처럼 미끄러지기 어려워 작업의 안전성을 높이기 위해 사용됩니다.

에폭시 수지는 광택이 있기 때문에 시인성이 높고, 광원을 반사해 안전한 작업 환경을 실현합니다.

이상과 같은 요인이, 예측 기간 중에 조사된 시장에 있어서의 에폭시 수지 수요를 증대시킬 가능성이 있습니다.

독일의 산업용 코팅 산업 개요

독일의 산업용 코팅 시장은 본질적으로 부분적으로 통합되어 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

산업 인프라 건설 증가

석유 및 가스 및 석유화학산업에서의 수요 증가

억제요인

VOC 배출에 관한 엄격한 규제

기타 억제요인

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

수지 유형

에폭시

아크릴

알키드

폴리우레탄

기타 수지 유형

코팅 기술

수성 코팅

용제형 코팅

방사선 경화형 코팅

분체 도료

유형

일반 공업용

보호

석유 및 가스

광업

전력

인프라

기타 보호

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

AkzoNobel NV

Axalta Coating Systems

Beckers group

Hempel AS

Jotun

MIPA SE

PPG Industries Inc.

RPM International Inc.

The Sherwin-Williams Company

제7장 시장 기회와 앞으로의 동향

친환경 페인트에 대한 수요 증가

SHW

영문 목차

영문목차

The Germany Industrial Coatings Market size is estimated at USD 1.09 billion in 2025, and is expected to reach USD 1.28 billion by 2030, at a CAGR of 3.22% during the forecast period (2025-2030).

Due to the outbreak of COVID-19, the industrial coatings sector was negatively impacted. Sales were affected due to GDP movement. Most production units were shut down due to the lockdowns and shortage of human resources. This resulted in uncertainty among various producers. Furthermore, supply chain constraints significantly obstructed the expansion of the industry. The automotive industry showed sluggish sales, a structural slowdown, and a sputtering economy in 2019-2020. However, the easing of lockdowns, along with incentive packages to support economic revival, benefited the regional automotive industry. The market recovered in 2021 and is expected to grow at a significant rate in the coming years.

Key Highlights

Over the short term, the increasing construction of industrial infrastructure and the growing demand from oil and gas and petrochemical industries are expected to boost the market growth.

However, the stringent regulations for volatile organic compound (VOC) emissions are expected to hinder the market's growth.

Nevertheless, the rising demand for eco-friendly coating products is likely to create lucrative growth opportunities for the studied market.

German Industrial Coatings Market Trends

Flourishing Oil and Gas Sector to Rise the Demand for Protective Coatings

The oil and gas sector is one of the major end users of protective coatings. The industry requires heat-resistant coatings due to the high-temperature environment of its business operations. The coatings are also used to protect metal and steel structures from corrosion when exposed to moist and damp conditions. They are used in the oil and gas industry for tanks, pipes, valves, pumps, etc.

The oil and gas industry uses protective coatings for both upstream and downstream segments to prevent corrosion during oil and gas transportation toward refineries. The industry has been trying to find ways to cut capital charges. Along with the need to adhere to strict environmental regulations, this has led to the demand for a coating system with a long life, which may be effective in protecting assets.

Offshore oil and gas production has some of the most demanding conditions. Therefore, the coating systems used must be equipped for these conditions. Prolonged exposure to penetrating UV rays and constant contact with rough seawater increases the need for industrial coatings.

However, with the Russia-Ukraine war, Germany has taken steps to halt the process of certifying the Nord Stream Two gas pipeline from Russia, besides other sanctions, in support of Ukraine. The temporary halts on the imports of petroleum and allied products from Russia are likely to affect the market studied in the country.

According to BP Stats, the total oil consumption in Germany was 2,045 thousand barrels per day in 2021, registering a decline rate of 0.2% compared to 2,049 thousand barrels per day in 2020.

As per the same source, the total natural gas consumption in the country was 90.5 billion cubic meters in 2021, registering a growth rate of 4.2% from 87.1 billion cubic meters in 2020.

All the above-motioned factors are expected to augment the demand for protective coatings for the oil and gas industry during the forecast period.

Rising Usage of Epoxy Resins

Epoxy resins are reinforced polymer composites derived from petroleum sources. They are the result of a reactive process involving epoxide units. These resins are used as binders for coating applications to enhance the durability of coatings for floor and metal applications.

Epoxy coatings are suitable for steel applications in harsh operating environments because of their resistance to corrosion, abrasion, and weathering. These coatings are also resistant to extremely high temperatures, making them suitable for use on tanks that store hot products and are exposed to extreme heat.

Industrial epoxy coatings are commonly used in three layers. Firstly, a primer, such as zinc primer, is applied. The epoxy is then sprayed on. An epoxy binder or polyurethane topcoat is applied to complete the coating process.

Epoxy polyamide coatings are ideal for moisture resistance, epoxy mastic coatings are used for film thickness, and phenolic epoxy coatings are excellent for chemical resistance. Depending on the application, epoxies can be used as a priming, intermediate coat, or even a topcoat.

Epoxy resins are frequently used as binders in industrial coatings. Those coatings provide high adhesion and high chemical (corrosion) and physical resistance for use on ships and chemical storage tanks.

Due to their availability, epoxy coatings find numerous industrial applications. Epoxy powder coatings are used on washers, dryers, white goods, steel pipes, and fittings used in the oil and gas industry, water transmission pipelines, and concrete reinforcing rebar due to their flexible applicability.

Several advantages of epoxy coatings are:

Epoxy coatings are long-lasting, cost-effective, waterproof, and shock-resistant.

They are used to improve operational safety since they are not slippery like polished concrete.

Epoxy increases visibility with its high sheen, reflecting light sources and improving visibility making for a safer working environment.

All the above-mentioned factors may augment the demand for epoxy resins for the market studied during the forecast period.

German Industrial Coatings Industry Overview

The Germany industrial coatings market is partially consolidated in nature. Some of the major key playersin the market include PPG Industries Inc., The Sherwin-Williams Company, AkzoNobel NV, Axalta Coating Systems and Jotun.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Industrial Infrastructure Construction

4.1.2 Growing Demand from Oil and Gas and Petrochemical Industries

4.2 Restraints

4.2.1 Stringent Regulations for VOC Emissions

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

5.1 Resin Type

5.1.1 Epoxy

5.1.2 Acrylic

5.1.3 Alkyd

5.1.4 Polyurethane

5.1.5 Other Resin Types

5.2 Technology

5.2.1 Water-borne Coatings

5.2.2 Solvent-borne Coatings

5.2.3 Radiation-cured Coatings

5.2.4 Powder Coatings

5.3 Type

5.3.1 General Industrial

5.3.2 Protective

5.3.2.1 Oil and Gas

5.3.2.2 Mining

5.3.2.3 Power

5.3.2.4 Infrastructure

5.3.2.5 Other Protectives

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements