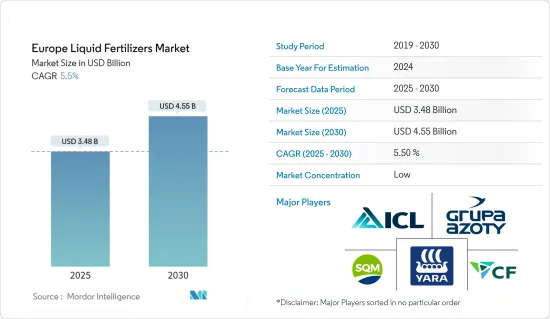

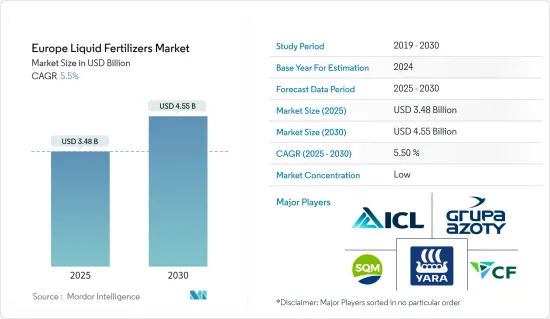

유럽의 액체 비료 시장 규모는 2025년에 34억 8,000만 달러, 2030년에는 45억 5,000만 달러에 달할 것으로 예측되고 있습니다. 예측 기간 중(2025년-2030년) CAGR은 5.5%를 나타낼 전망입니다.

유럽의 액체 비료 시장은 효율적이고 지속 가능한 농업에 대한 수요가 증가함에 따라 꾸준한 성장을 이루고 있습니다. 농가들에게 선호되는 선택이 되고 있습니다. 유엔 경제 사회국에 따르면 독일 인구는 2022년 8,410만 명에서 2023년에는 8,460만 명으로 증가하여 생산성을 높이고 소비자 수요를 충족시키기 위해 액체 비료의 큰 요구가 생겨나고 있습니다.기타 특전으로서, 정밀 농업의 기술적 진보에 의해 액체 비료의 정확한 시용이 촉진되어 낭비의 삭감과 환경에 대한 영향의 경감을 도모하고 있습니다.

우크라, 독일, 프랑스, 영국과 같은 국가는 첨단 농업 분야와 현대 농업 기술의 도입률이 높기 때문에 유럽의 액체 비료 시장을 독점하고 있습니다. 모늄 비료 소비량은 2022년에 190만 톤에 달했고, 전년 대비 5.5% 증가했습니다.

게다가 2022년 11월에 실시된 조사에서는 감자 재배에 액체 질소 비료인 질산우레아 암모늄(UAN)을 시용하면 러시아에서는 시장 유통 가능한 감자 수량이 6.4% 증가하고 총 수율이 최대 12.2% 증가한 것으로 나타났습니다. 2023년 유로스타트는 소규모 농부들이 유럽 지역 전체 농장의 거의 70%를 차지한다고 보고하며, 이들이 유럽 농업 환경에서 중요한 역할을 하고 있음을 강조했습니다.

지속가능성은 유럽농업부문의 중심적 초점이 되어 액체비료시장의 성장에 영향을 주고 있습니다. 이 전환은 규제 요건을 충족할 뿐만 아니라 환경 친화적인 농법을 요구하는 소비자 수요에도 부응하는 것입니다.

유럽에서는 기술 혁신과 정밀 농업 기술 등의 요인의 영향을 받아 액체 비료 시장이 크게 진화하고 있습니다. 지역에서 정밀 농업의 도입을 뒷받침하는 주요 요인이 되고 있습니다.액체 비료는 현대의 농가에게 다양한 이점을 가져오고, 양분의 이용 가능성에 대한 작물의 반응을 개선해, 생산성을 향상시킵니다.

질산 우레아 암모늄(UAN) 비료는 식물 영양의 액체 파워 하우스로 우레아와 질산 암모늄을 수용액에 혼합하여 효율적인 식물 영양 관리에 정확하게 사용됩니다. Institute)는 UAN의 질소 효력이 보통 28%에서 32%이기 때문에 이 지역의 정밀 농업에 사용되는 중요한 액체 비료입니다. 시장 경쟁력을 유지하기 위해 전략적 파트너십을 포함한 다양한 전략을 실시했습니다. AG와 전략적 합작 회사를 설립했습니다. 트리니다드에 액체 질소(UAN)의 제조 능력을 가진 HEML AG는 이 협력 관계를 통해 영국에 대한 비료 공급의 안전성을 높이는 것을 목표로 하고 있습니다.

게다가 유럽에서는 도시화로 인해 경작지가 점차 줄어들고 있어 비료 의존도가 높아지고 있습니다. 산업화로 악화된 경작지 면적의 감소로 식량안보를 유지하는 데 상당한 어려움을 겪고 있습니다. 화학 비료의 사용량이 역사상 최고를 기록했으며, 전국에서 1,400만 톤 가까이 적용되었습니다.

농산물 수입 증가는 이 지역 수요 증가와 생산량 부족을 나타냅니다. Map에 따르면 독일에서는 2023년 밀 수입량은 513만 톤에 이르렀으며, 2022년에는 410만 톤이었습니다.

러시아는 강력한 농업 기반과 비료의 대규모 생산으로 유럽 액체 비료 시장에서 중요한 역할을 하고 있습니다. 예를 들어, 러시아의 주요 비료 제조업체인 PhosAgro의 데이터에 따르면이 나라는 6,000 만 톤의 비료를 생산하고 있으며, PhosAgro는 2023년에 1,100 만 톤의 비료를 생산했습니다.

또한 러시아의 Life Force LLC는 식물 활성 성분의 혁신적인 배합을 특징으로하는 액체 비료 Life Force Acti Grow Fe/B/Zn/Mn을 제공합니다. 러시아의 농지는 도시화와 환경 문제에 대한 노력에 따라 감소의 일환을 따르고 있으며, 액체 비료의 역할은 점점 중요해지고 있습니다. 벼의 수확 면적은 16만 9,600헥타르로, 전년에 비해 8.94% 감소했습니다.정확한 영양 시용이 가능한 액체 비료를 사용하는 것으로, 러시아는 한정된 토지에서 작물의 수율을 늘리는 것을 목표로 하고 있습니다.

러시아의 농업 수출 능력, 특히 비료의 수출 능력은 국내와 유럽의 요구에 부응할 수 있게 하고 있습니다. 러시아에서 우레아와 질산암모늄의 액체 혼합물의 수출량은 202만 5,979톤이며, 이는 세계에서 30.9%의 금액 점유율이었습니다.

그러나 기타 국가와의 분쟁이 계속되고 있어 국내외공급 체인이 혼란해 비료 입수에 불확실성이 생기고 있습니다.

유럽의 액체 비료 시장은 분열되어 있어 안정적인 고객 기반을 유지하고 큰 시장 점유율을 얻기 위해 대기업 간의 경쟁이 치열 해지고 있습니다. 시장에서 가장 주목받고 있는 기업으로는 Yara International ASA, ICL Group Ltd., Groupa Azoty SA, CF Industries Holdings, Inc., Sociedad Quimica y Minera de Chile SA(SQM) 등이 있습니다. 각 회사는 유럽 액체 비료 시장에서 포트폴리오의 충실과 전략적 지위 확립을 위해 시설 확장 및 신제품 개발에 주력하고 있습니다.

The Europe Liquid Fertilizers Market size is estimated at USD 3.48 billion in 2025, and is expected to reach USD 4.55 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

The European liquid fertilizer market has experienced steady growth, propelled by the increasing demand for efficient and sustainable agricultural practices. Liquid fertilizers, valued for their ease of application and rapid nutrient absorption, are becoming a preferred choice for farmers in the region. The need to enhance crop yields, improve soil fertility, and meet the rising food demand of the growing population has further accelerated the adoption of these fertilizers. According to the United Nations, Department of Economic and Social Affairs, Germany's population increased to 84.6 million in 2023 from 84.1 million in 2022, creating a significant need for liquid fertilizers to boost productivity and satisfy consumer demand. Additionally, the market benefits from technological advancements in precision agriculture, which promote the precise application of liquid fertilizers, reducing wastage and environmental impact.

Countries such as Ukraine, Germany, France, and the United Kingdom dominate the European liquid fertilizer market due to their advanced agricultural sectors and higher adoption rates of modern farming techniques. For instance, according to FAOSTAT data, France's urea ammonium nitrate fertilizer consumption reached 1.9 million metric tons in 2022, an increase of 5.5% from the previous year. Key crops contributing to the market demand include cereals, oilseeds, fruits, and vegetables, all of which benefit from the nutrient efficiency offered by liquid fertilizers.

Furthermore, a research study conducted in November 2022 demonstrated that the application of Urea Ammonium Nitrate (UAN), a liquid nitrogenous fertilizer in potato cultivation resulted in a 6.4% increase in marketable potato yield and up to a 12.2% increase in total yield in Russia. In 2023, Eurostat reported that small-scale farmers constituted nearly 70% of all farms in the European region, underscoring their pivotal role in Europe's agricultural landscape. Typically spanning under 10 hectares, these farms are essential for fostering rural entrepreneurship and upholding traditional farming practices. Hence, liquid fertilizer is the most effective option for better yield for these farmers.

Sustainability has become a central focus in the European agricultural sector, influencing the growth of the liquid fertilizer market. Stricter environmental regulations and the European Union's Green Deal initiatives encourage the use of environmentally friendly fertilizers with reduced carbon footprints. Many liquid fertilizers are now developed to align with these goals, incorporating bio-based or organic ingredients to support sustainable farming. This shift not only meets regulatory requirements but also addresses consumer demand for eco-friendly farming practices. Therefore, due to the continued demand for high-efficiency fertilizers to boost production while minimizing harmful impacts on the environment, coupled with the active participation and involvement of players, the segment is anticipated to grow gradually during the forecast period.

In Europe, the liquid fertilizers market is evolving significantly, influenced by factors such as technological innovations, and precision agriculture techniques. Rising food security concerns due to changing climatic conditions, increasing population, and decreasing arable land availability are the primary factors bolstering the adoption of precision farming practices in the region. This, in turn, drives the market for liquid fertilizers as they provide an array of benefits to modern farmers that lead to improved crop response to the availability of nutrients and better productivity.

Urea ammonium nitrate (UAN) fertilizer, a liquid powerhouse of plant nutrition, blends urea and ammonium nitrate in an aqueous solution used precisely for efficient plant nutrient management. The International Plant Nutrition Institute highlights its nitrogen potency, typically ranging from 28% to 32%, hence it is an important liquid fertilizer used in precision farming in the region. Moreover, the European urea ammonium nitrate fertilizer market has witnessed the implementation of various strategies by industry participants, including strategic partnerships, to maintain market competitiveness. In 2022, Brineflow, a liquid fertilizer manufacturer headquartered in Great Yarmouth, established a strategic joint venture with HELM AG, a prominent German fertilizer producer. HEML AG, which possesses substantial liquid nitrogen (UAN) manufacturing capabilities in Trinidad, aims to enhance the security of fertilizer supply for the United Kingdom through this collaborative arrangement. This partnership exemplifies the industry's efforts to strengthen supply chains and maintain a competitive edge in the European market.

Furthermore, Europe has experienced a gradual reduction in arable land due to urbanization. This trend compels farmers to maintain or increase crop yields from a diminishing area, thereby increasing their reliance on fertilizers to optimize productivity. According to FAOSTATS data, the harvested area of cereal grains in Europe has reached 116.7 million hectares, a reduction of 3.42% from the previous year. Turkey has faced significant challenges in maintaining food security due to a decrease in arable land, exacerbated by urbanization, and industrialization. To mitigate these issues, in 2023, Turkey recorded the highest usage of chemical fertilizers in its history, with nearly 14 million metric tons applied across the country, according to the Ministry of Agriculture and Forestry, Turkey. This increase is part of a broader effort to counteract the decline in available agricultural land and ensure sufficient food production.

The growing import of agricultural produce further shows the growing demand and insufficient production in the region. For instance, according to the ITC Trade Map, in Germany, the import of wheat in 2023 reached 5.13 million metric tons which was 4.10 million metric tons in 2022. The reduction in arable land, increasing import, and growing adoption of precision agriculture, coupled with the need for increased agricultural productivity, is anticipated to drive the liquid fertilizer market in the forecast period.

Russia plays a critical role in the European liquid fertilizer market, driven by its strong agricultural base and extensive production of fertilizers. The country is a major producer of nitrogen-based liquid fertilizers, including urea ammonium nitrate (UAN) solutions, which are essential for European agricultural productivity. For instance, according to the data of PhosAgro, a leading fertilizer producer in Russia, the country has produced 60 million metric tons of fertilizers, with PhosAgro contributing 11 million metric tons in 2023.

Additionally, another Russian company Life Force LLC offers Life Force Acti Grow Fe/B/Zn/Mn, a liquid fertilizer featuring an innovative formula of active phytocomponents. As agricultural land in Russia continues to decrease due to urbanization and environmental initiatives, liquid fertilizers' role becomes even more significant. For instance, in 2022 the harvested area for rice was 169.6 thousand hectares in Russia with a reduction of 8.94% compared to the previous year. Using liquid fertilizer, that enables precise nutrient application, the country is aiming to boost crop yields on limited land.

Russia's agricultural export capacity, particularly in fertilizers, allows it to cater to both domestic and European needs. As European farmers seek to improve their crop yields with shrinking land, Russia's export-oriented strategy positions the country as a critical player in the regional and global fertilizer market. For instance, the export quantity of the liquid mixture of urea and ammonium nitrate in 2023 from Russia was 2,025,979 metric tons which was 30.9% value share worldwide according to the ITC trade map. According to Rosstat, the largest buyers of Russian fertilizers in the EU were Poland, France, and Germany. Poland increased its imports 2.7-fold year-on-year, and France increased its imports by 18% in 2023.

However, the ongoing conflict with other nations has disrupted both domestic and international supply chains, creating uncertainty in the availability of fertilizers. Despite these challenges, Russia continues to remain at the forefront of the European liquid fertilizer market, focusing on innovation and sustainability to maintain its critical role in feeding Europe's growing agricultural demands.

The European liquid fertilizer market is fragmented, intensifying competition among major players to maintain a stable customer base and capture significant market shares. Some of the most notable companies in the market are Yara International ASA, ICL Group Ltd., Grupa Azoty S.A., CF Industries Holdings, Inc., and Sociedad Quimica y Minera de Chile SA (SQM) among others. The companies have focused on facility expansions and developing new products to enhance their portfolio and strategize their hold in the European liquid fertilizer market.