차세대 첨단 배터리 - 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

Next Generation Advanced Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1685877

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

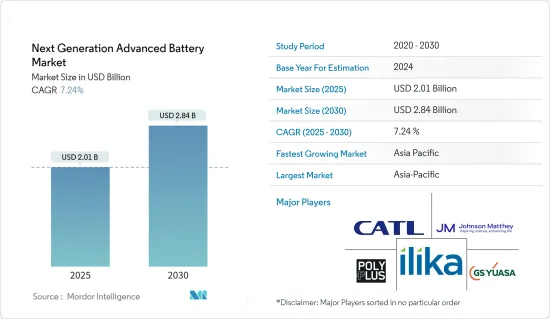

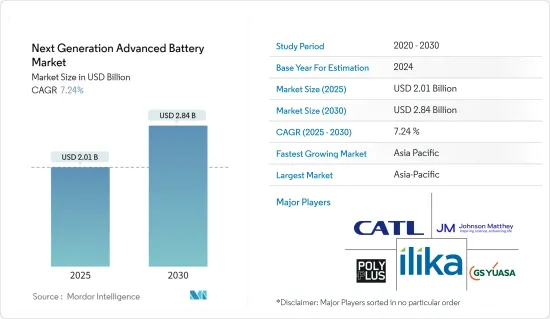

차세대 첨단 배터리 시장 규모는 2025년에 20억 1,000만 달러, 2030년에는 28억 4,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 7.24%를 나타낼 전망입니다.

시장은 2020년 COVID-19에 의해 부정적인 영향을 받았습니다.

주요 하이라이트

장기적으로는 수요의 확대와 전기자동차의 보급 확대가 시장의 성장을 견인할 것으로 전망됩니다.

한편, 제조 비용과 연구 개발 비용이 높은 것이, 예측 기간중의 차세대 첨단 배터리의 성장을 방해할 것으로 예상됩니다.

하지만 차세대 첨단 배터리의 제조 설비의 개척은 예측 기간 중에 차세대 첨단 배터리 시장에 유리한 성장 기회를 가져올 것으로 예상됩니다.

아시아태평양은 시장을 독점하고 있으며 예측기간 중에 가장 높은 CAGR로 성장할 것으로 예상됩니다.

차세대 첨단 배터리 시장 동향

시장을 독점할 것으로 예상되는 운송 부문

수송 시스템의 전동화가 인기를 끌고 있으며, 다양한 정부의 의무화에 의해 전기자동차의 도입이 가속되고 있기 때문에 수송 분야에 있어서의 차세대 첨단 배터리의 성장에 직접적인 도움이 되고 있습니다.

2021년, 자동차 대기업 제너럴 모터스가 2035년까지 가솔린차와 디젤차의 판매를 정지한다고 발표해, 아우디 AG는 2033년까지 그러한 자동차의 생산을 정지할 예정입니다.

혼다는 2022년 4월 전동화와 소프트웨어 기술에 398억 4,000만 달러를 투자해 향후 10년간 세계에 사업을 가속시킬 것이라고 발표했습니다. 라인을 건설하여 약 3억 4,265만 달러를 투자합니다.

국제에너지기구(IEA)에 따르면 세계의 전기자동차 스톡은 2015년 125만대에서 2020년에는 약 1,020만대로 증가했습니다.

게다가 알루미늄 공기 배터리는 기존의 리튬이온 전지에 비해 알루미늄이 연료의 역할을 하고, 전해액을 통해 공기가 금속과 반응하여 전력을 낳는다는 장점이 있습니다.

2021년 12월 독일의 자동차 제조업체인 메르세데스 벤츠는 폭넓은 전기자동차에 1억 달러를 투자한다고 발표했습니다.

2022년 4월, 닛산 자동차는 2028년까지 라미네이트형 고체 배터리를 시장에 투입할 계획으로, 프로토타입 생산 설비를 시작했습니다.

전체적으로, 자동차 제조업체는 고체 배터리와 금속 공기 배터리의 개발에 상당액의 투자를 실시하고 있어, 자동차는 차세대 첨단 배터리 시장의 주요 분야의 하나가 되고 있습니다.

아시아태평양이 시장을 독점

2021년 현재 중국, 인도, 일본이 아시아태평양의 차세대 첨단 배터리 기술의 잠재적 시장입니다.

2022년 3월 현재 중국의 배터리 에너지 저장 용량은 3GW에 달했으며 2019년 1.7GW에 비해 76.5% 증가한 것으로 나타났습니다. 배터리 축전 용량을 100GW까지 늘릴 것으로 예상되고 있습니다.

China Energy Storage Alliance(CNESA)에 따르면 에너지 저장의 주요 용도인 그리드 언시러리 서비스와 관련된 정책의 세련성과 칭하이, 광둥, 장쑤, 내몽골, 신장 등의 지역에서의 정책 개발에 의해 중국에서는 에너지 저장 건설 및 발전의 물결을 일으켰습니다. 이러한 정부의 정책에 의해 예측 기간중, 선진적인 배터리 기술에 대한 수요가 높아질 가능성이 높습니다.

현재 중국에서는 차세대 선진 전지 기술에 관한 다양한 개발 프로젝트와 투자가 진행되고 있습니다.

중국에서의 시나리오 외에도 2022년 1월에는 일본의 물질 및 재료연구기구(NIMS)와 소프트뱅크 주식회사가 현재의 리튬 이온 전지보다 상당히 높은 500Wh/kg 이상의 에너지 밀도를 가지는 리튬 공기 전지를 개발했습니다. 팀은 이 전지가 실온에서 충방전할 수 있는 것을 확인했습니다.연구 팀이 개발한 전지는 최고의 에너지 밀도와 사이클 수명 성능을 나타내고 있습니다.

리튬 공기 전지는 경량으로 대용량, 이론 에너지 밀도는 현재 시판되고 있는 리튬 이온 전지의 수배라는 궁극의 2차 전지가 될 가능성을 갖고 있습니다.

게다가 '메이크 인 인디아'는 인도에 있어서 우선 순위가 높은 운동이며, 이미 전기자동차를 생산하는 인센티브를 제공합니다. 차세대 선진 배터리가 성능 파라미터가 약간 높은 동급 리튬 이온 배터리에 대해 가격 우위를 가지고 있었다고 해도, 인도에서는 다른 지역보다 우수한 시장 기회를 찾을 수 있다고 생각됩니다.

2022년 3월 인도는 첨단 화학 전지(ACC) 축전지 제조를 위한 PLI 방식을 통한 우대 조치를 활용하는 4개 회사의 입찰을 승인했습니다. Limited의 4사는 인도의 배터리 셀 국산화를 촉진하는 1,810억 루피의 프로그램에 따라 인센티브를 받았습니다.

따라서, 상기 요인은 예측기간 중에 아시아태평양의 차세대 첨단 배터리시장을 견인할 것으로 예상됩니다.

차세대 첨단 배터리 산업 개요

차세대 첨단 배터리 시장은 어느 정도 통합되어 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2027년까지 시장 규모 및 수요 예측

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

억제요인

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 세분화

기술분야

고체 전해질 전지

마그네슘 이온 전지

차세대 플로우 배터리

금속공기 배터리

리튬 유황 전지

기타 기술

최종 사용자

가전

수송 기기

산업용

에너지 저장

기타 최종 사용자

지역

북미

아시아태평양

유럽

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Pathion Holding Inc.

GS Yuasa Corporation

Johnson Matthey PLC

PolyPlus Battery Co. Inc.

Ilika PLC

Sion Power Corporation

LG Chem Ltd

Saft Groupe SA

Contemporary Amperex Technology Co. Ltd

제7장 시장 기회와 앞으로의 동향

SHW

영문 목차

영문목차

The Next Generation Advanced Battery Market size is estimated at USD 2.01 billion in 2025, and is expected to reach USD 2.84 billion by 2030, at a CAGR of 7.24% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Key Highlights

Over the long term, the growing demand and increasing adoption of electric vehicles are expected to drive the growth of the market studied.

On the other hand, high manufacturing and R&D costs are expected to hamper the growth of Next-Generation advanced batteries during the forecast period.

Nevertheless, the development of manufacturing facilities for next-generation advanced batteries is likely to create lucrative growth opportunities for the Next-Generation advanced battery market in the forecast period.

Asia-Pacific region dominates the market and is also likely to witness the highest CAGR during the forecast period. This growth is attributed to the increasing investments, coupled with adoption of consumer electronics and electric vechiles in the countries of this region including India, China and Japan.

Next Generation Advanced Battery Market Trends

Transportation Segment Expected to Dominate the Market

The electrification of the transportation system is gaining popularity, and various government mandates have accelerated the adoption of electric vehicles, which directly aids the growth of next-generation advanced batteries in the transportation sector.

In 2021, automobile giants announced that General Motors will stop selling petrol and diesel models by 2035, and Audi AG plans to stop producing such vehicles by 2033. The carmakers are rushing to electrify their electric cars, which has led the company to invest in advanced batteries for more efficient and profitable electric vehicles.

In April 2022, Honda Motors announced that it would invest USD 39.84 billion in electrification and software technologies to accelerate its business globally for the next ten years. It will also build a demonstration production line for all-solid-state batteries in North America, allocating approximately USD 342.65 million. The investment company plans to launch two mid-to-large-scale electric vehicles (EV) models by 2024 with a partnership with General Motors.

According to the International Energy Agency (IEA), the global electric vehicle stock increased from 1.25 million in 2015 to about 10.2 million in 2020. In 2020, battery-electric vehicles accounted for most of the electric vehicles at about 6.85 million, and plug-in hybrid electric vehicles were about 3.35 million.

Furthermore, aluminium-air batteries have an advantage over the conventional lithium-ion battery as the aluminium acts as a fuel where air reacts with the metal via an electrolyte to produce power. It has a travel range similar to gasoline-powered cars and a higher energy density than the lithium-ion battery. However, it lacks government policy support and attention from automakers to make it a popular battery energy storage system for electric vehicles.

In December 2021, Mercedes Benz, a German car manufacturer, announced to invest of USD 100 million in a wide range of electric cars. The company also intends to integrate solid-state battery technology into a limited number of vehicles within the next five years. Mercedes Benz plans to invest tens of millions into Factorial Energy, a battery company to develop solid-state batteries.

In April 2022, Nissan Motor Company planned to bring laminated solid-state batteries to the market by 2028, with the beginning of a prototype production facility. It is a part of Nissan's Ambition 2030 strategy, plus an investment of USD 17 billion for the four new electric vehicle concepts.

Overall, automobile manufacturers are investing heavily in developing solid-state batteries and metal-air batteries, making automobiles one of the major sectors of the next-generation advanced battery market.

Asia-Pacific to Dominate the Market

As of 2021, China, India, and Japan were the potential markets for the next generation advanced battery technology in the Asia-Pacific region.

As of March 2022, China's battery energy storage capacity reached 3 GW, representing an increase of 76.5% compared to 1.7 GW in 2019. Furthermore, the Chinese Government is expected to increase its battery storage capacity to 100 GW by 2030. Such scenarios are creating vast opportunities for various next-generation advanced battery developers in the region.

According to the China Energy Storage Alliance (CNESA), the refinement of policy related to grid ancillary services - energy storage's primary application - as well as policy developments in regions including Qinghai, Guangdong, Jiangsu, inner Mongolia, and Xinjiang, have created a wave of energy storage construction and development in China. Such government policies will likely boost the demand for advanced battery technologies during the forecast period.

At present, various development projects and investments in the next generation advanced battery technologies are happening in China. In July 2021, CATL unveiled the first next-generation sodium-ion battery and its AB battery pack solutions. Also, CATL's quest to shift the electric vehicle market toward a sodium-ion cell received a boost from the central government after the Ministry of Industry and Information Technology announced the creation of standards for such battery types.

In addition to the scenario in China, in January 2022, Japan's National Institute for Material Science (NIMS) and the Softbank Corp. developed a lithium-air battery with an energy density of over 500Wh/kg-significantly higher than currently lithium-ion batteries. The research team confirmed that this battery could be charged and discharged at room temperature. The battery developed by the team shows the highest energy densities and best cycle life performances. These results signify a major step toward the practical use of lithium-air batteries.

The lithium-air batteries are expected to have the potential to be the ultimate rechargeable batteries: they are lightweight and high capacity, with theoretical energy densities several times that of currently available lithium-ion batteries. Because of these potential advantages, they may use various technologies, such as drones, electric vehicles, and household electricity storage systems.

Further, "Make in India" is a high-priority movement for India and has already provided incentives to produce electric cars. Batteries for cars and grid storage are high on the agenda for manufacturing in India. The EV market for two-wheelers, three-wheelers, cars, and minibusses is more price-sensitive than performance sensitive. If the next generation advanced batteries have a price advantage over a comparable lithium-ion battery whose performance parameters are marginally higher, it would still find a better market opportunity in India than elsewhere. The advanced batteries made with economies of scale have huge market potential in India.

In March 2022, India approved bids for four companies to avail incentives under the PLI Scheme for the Advanced Chemistry Cell (ACC) Battery Storage Manufacturing. Reliance New Energy Solar Limited, Ola Electric Mobility Private Limited, Hyundai Global Motors Company Limited, and Rajesh Exports Limited received incentives under India's INR 181 billion program to boost local battery cell production. Under the scheme, selected ACC battery storage manufacturers were expected to set up a production facility within two years. Such government-supportive incentives are expected to create an environment for the future development of the next generation advanced battery market.

Therefore, the above-mentioned factors are expected to drive the next-generation advanced battery market in the Asia-Pacific region during the forecast period.

Next Generation Advanced Battery Industry Overview

The next-generation advanced battery market is moderately consolidated in nature. Some of the major players in the market (in no particular order) include Sion Power Corporation, Contemporary Amperex Technology Co. Ltd, PolyPlus Battery Co. Inc., GS Yuasa Corporation, and Saft Groupe SA.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2027

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.2 Restraints

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Technology

5.1.1 Solid Electrolyte Battery

5.1.2 Magnesium Ion Battery

5.1.3 Next-generation Flow Battery

5.1.4 Metal-Air Battery

5.1.5 Lithium-Sulfur Battery

5.1.6 Other Technologies

5.2 End User

5.2.1 Consumer Electronics

5.2.2 Transportation

5.2.3 Industrial

5.2.4 Energy Storage

5.2.5 Other End Users

5.3 Geography

5.3.1 North America

5.3.2 Asia-Pacific

5.3.3 Europe

5.3.4 South America

5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements