북미의 데이터센터 냉각 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

North America Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1685818

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

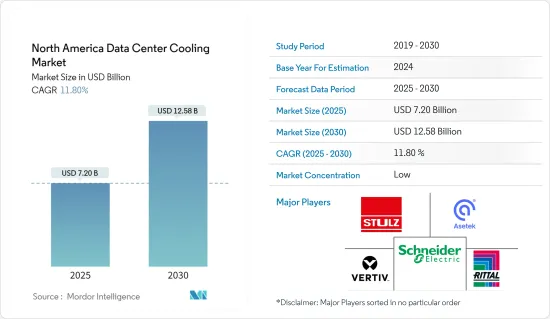

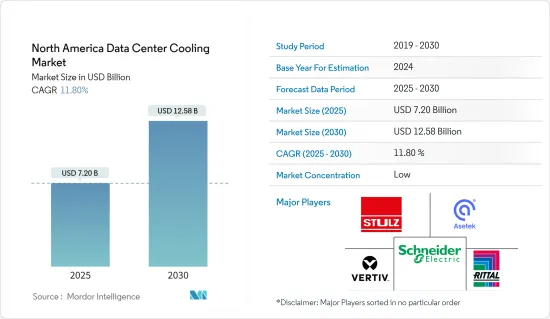

북미의 데이터센터 냉각 시장 규모는 2025년에 72억 달러에 달할 것으로 추정됩니다. 2030년에는 125억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 11.8%를 나타낼 것으로 전망됩니다.

다양한 컨테이너형, 모듈형, 성능 최적화형 데이터센터(POD) 시설의 급속한 개발로 데이터센터에서 이용가능한 다양한 냉각 시스템에 대한 수요가 전반적으로 높아지고 시장 성장을 폭넓게 견인할 것으로 예측됩니다.

미국은 공동 위치와 100MW 이상의 하이퍼스케일 시설 개발로 북미의 데이터센터 냉각 시장 전체를 지배하고 있습니다. 비용 효율적이고 효율적인 데이터센터에 대한 요구 급증, 데이터센터가 있는 기업의 건전한 성장, 친환경 데이터센터 솔루션을 위한 다양한 녹색 이니셔티브, 전력 밀도가 시장 성장을 가속할 것으로 예상됩니다.

또한 휴대용 냉각 및 액체 기반 냉각 기술의 출현, 모듈식 데이터센터 냉각 접근법에 대한 요구 증가는 북미의 데이터센터 냉각 시장에 유리한 기회를 제공할 것으로 기대됩니다. 북미의 데이터센터 냉각 시장을 독점하고 있는 것은 주로 에너지 효율이 높고 비용 효율적이며 환경 친화적인 냉각 솔루션의 채용이 증가하고 있기 때문에 정부 기관이 제공하는 다양한 엄격한 환경 안전 규칙을 따릅니다.

게다가 이 시장에서는 제품의 발매나 기술 혁신이 활발히 이루어져 시장을 크게 견인하고 있습니다. 예를 들어, 2023년 6월에는 버지니아의 Modine Rockbridge 시설에서 5MW의 최신 테스트 랩이 가동되어 Airedale by Modine이 데이터센터 고객에게 제공할 수 있는 서비스를 더욱 확장했고 검증된 지속 가능한 냉각 솔루션에 대한 데이터센터 업계 수요 증가에 대응했습니다. 이 새로운 실험실에서는 최대 2.1MW의 공냉식 냉동기와 최대 5MW의 수냉식 냉동기에 대응하여 모든 공조 기기의 시험이 가능합니다.

그러나 특수 인프라의 필요성, 높은 투자 비용, 정전시 다양한 냉각 문제 등이 예측 기간 동안 북미의 데이터센터 냉각 시장 성장을 제한할 것으로 예상됩니다.

COVID-19의 큰 유행으로 인해 데이터센터는 알려지지 않은 영역에 놓여졌습니다. 공급망의 혼란이 다발하여 세계의 정전에 의해 시스템의 원활한 운용에 큰 영향이 나왔습니다. 데이터센터 장비의 배송에 영향을 미치는 운송 중단 및 공장 폐쇄로 인해 운영자는 문제를 해결하기 위한 해결 방법을 찾았습니다. 그러나 COVID-19 이후의 예측 기간 동안 시장은 다양한 유리한 성장 기회를 목격할 것으로 예상됩니다.

북미의 데이터센터 냉각 시장 동향

건설 부문의 성장이 가구 제품 수요를 밀어

정보기술(IT)산업은 주로 개인사업주, 조직, 파트너십 등 다양한 사업체에 의한 정보기술(IT) 서비스 및 관련 상품의 판매 전반으로 구성되며, 주로 컴퓨터, 컴퓨터 주변기기, 통신기기를 사용하여 데이터를 검색, 저장, 전송, 조작을 합니다. IT 시장에는 컴퓨터 네트워크, 시스템 디자인 서비스, 방송, 전화 및 텔레비전과 같은 정보 전달 기술, 그 과정에서 사용되는 기타 장비도 포함됩니다. 이러한 거대한 요구사항은 장비가 정상적으로 작동하기 위한 적절한 냉각 시스템을 필요로 하기 때문에 전체 데이터센터 냉각 시장 수요를 견인하고 있습니다.

IT 업계에서는 온프레미스 개인 데이터 스토리지뿐만 아니라 조직 규모에 맞는 하이퍼스케일 데이터센터도 다양한 업무에 필요합니다. 특히 SaaS 제공업체의 성장으로 인해 클라우드 스토리지 채택이 이 지역에서 해마다 급격히 증가하고 있으며, 클라우드 스토리지 제공업체는 용량을 확장할 수 있으므로 데이터센터 냉각 시스템 수요가 극대화될 것으로 예상됩니다.

냉각 시스템은 IT 및 데이터센터 분야에서 필수적이며, 주된 이유는 전통적인 공기 냉각 솔루션보다 훨씬 효율적인 다양한 향상된 고품질 냉각 솔루션에 대한 요구가 있기 때문입니다. 또한 IT 인프라에서의 혁신을 높이고 다양한 스마트폰 제조업체의 열 관리를위한 냉각 시스템 수요 증가도 시장 성장을 크게 뒷받침하고 있습니다.

미국은 시장의 성장률을 높이는 다양한 원동력의 확립이라는 점에서 매우 중요한 역할을 하고 있습니다. 이는 주로 이 지역의 주요 시장 기업에 의한 데이터센터의 투자와 설립이 증가하고 있기 때문입니다. 예를 들어, 아마존 웹 서비스는 2023년 1월 버지니아 주 전역에 여러 데이터센터 캠퍼스를 설립했기 때문에 2040년까지 약 350억 달러를 투자할 의향입니다.

아시아태평양이 큰 시장 점유율을 차지할 전망

북미에서는 코로케이션 프로바이더나 하이퍼스케일 데이터센터 사업자에 의한 고액 투자뿐만 아니라, 많은 서비스 제공업체나 소프트웨어 프로바이더가 존재하는 미국이 시장을 독점할 전망입니다. 최근 몇 년 동안 데이터센터의 수가 크게 증가했습니다. 데이터센터의 성능을 향상시키기 위해 주어진 공간에서 상당한 수의 프로세서를 이용하게 되어 밀도가 높아지고 있습니다. 고밀도화에 따라 전력과 냉각에 대한 요구도 커지고 있습니다.

미국은 또한 은행, IT, 금융 서비스, 보험(BFSI), 소매, 헬스케어 산업 등 세계 데이터센터 요건에 크게 기여하고 있습니다. 이 지역의 데이터센터 서비스 제공 업체는 데이터센터 수와 확장을 고려하면 유리한 시장이므로 운영 비용을 관리하고 있습니다.

데이터센터의 전력 밀도는 랙당 평균 1.5kW 증가하여 공기 유통이 제한되고 발열이 증가하고 있습니다. 일반적으로 IT 기기는 1kW당 100-160cfm의 공기를 필요로 하지만 고밀도 환경에서는 100 이하로 감소하여 발열량이 증가하여 시장 성장을 크게 촉진합니다.

모바일 광대역 확대, 5G 출현, 빅데이터 분석 성장, 클라우드 컴퓨팅이 미국에서 새로운 데이터센터 인프라에 대한 수요를 추진하는 주요 요인입니다. 네트워크 제공업체는 보다 나은 기술 혁신을 위해 5G의 신속한 도입을 위해 노력하고 있습니다. 이러한 개발은 미국 기업들 사이에서 효율적인 데이터센터 냉각 솔루션과 서비스 수요를 더욱 촉진하고 있습니다.

Cloudscene에 따르면 2023년 9월 기준 미국의 데이터센터 총 수는 5,375이었고 독일은 522로 2위였습니다. 총 데이터센터는 영국이 517곳에서 3위, 중국은 448곳이었습니다. 이와 같이 미국에는 많은 데이터센터가 존재하기 때문에 예측기간을 통해 시장 성장이 가속될 것으로 예상됩니다.

북미의 데이터센터 냉각 산업 개요

북미의 데이터센터 냉각 시장은 경쟁이 치열하고 세분화되고 있습니다. Schneider Electric SE, Black Box Corporation, Asetek, Nortek Air Solutions LLC, Emerson Electric Co., 히타치 제작소, Rittal GmbH & Co.KG, Fujitsu Ltd, Stulz GmbH, Vertiv 등입니다. 기술 혁신에 대한 주목이 증가함에 따라 액체 기반 냉각 기술과 휴대용 냉각 기술과 같은 신기술에 대한 수요가 증가하고 있으며, 이 지역에서의 추가 개발을 위한 투자를 추진하고 있습니다.

2024년 5월, 슈투르츠는 최신 혁신인 CyberCool Coolant Management and Distribution Unit(CDU)을 발표했습니다. 제품 라인은 2개의 다른 크기로 유효한 4개의 모형으로 이루어져 있습니다. 이 장치는 345kW에서 1,380kW까지 광범위한 열교환 능력을 자랑합니다. 슈투르츠는 설비 급수 시스템의 정격 급수 온도를 32℃로 설정하고 기술 냉각 시스템의 액체 공급 온도는 36℃로 설정합니다.

2024년 3월, 리탈 프라이빗 리미티드는 인도의 방갈로르 제조 공장에 냉각 유닛 및 액체 냉각 패키지(LCP) 솔루션에 특화된 새로운 통합 센터를 개설했습니다. 이 전략적 움직임은 회사의 생산 능력을 강화할 뿐만 아니라 산업용 냉각 솔루션에 대한 수요 증가에 대응합니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요(대상 범위 : 데이터센터 냉각과 관련된 현재 지역 동향의 상세한 분석 포함)

냉각에 관한 주요 비용 고려 사항

DC 냉각을 중심으로 DC 운영과 관련된 주요 비용 오버헤드 분석

데이터센터 냉각의 주요 기술 혁신과 발전

데이터센터에서 채용되고 있는 주된 에너지 효율 사례

제5장 시장 역학

시장 성장 촉진요인(에너지 소비에 대한 강조 증가, 친환경 솔루션으로의 이동과 같은 주요 요인은 향후 5-7년간의 상대적 영향력을 기준으로 매핑됩니다.)

시장 역학(규제의 동적 특성, 진화하는 고객 요구와 같은 주요 요소는 향후 5-7년간의 상대적 영향력을 기반으로 매핑됩니다.)

시장 기회

격리가 있는 바닥과 격리가 없는 바닥의 비교

산업 생태계 분석

제6장 지역별 데이터센터의 실적 현황 분석

데이터센터 IT 부하 용량과 면적 실적의 지역별 분석(2017-2030년)

북미에서 확립된 DC 시장과 신흥 DC 핫스팟의 지역 분석

DC 냉각에 관한 규제 틀의 지역 분석

제7장 데이터센터 냉각 시장 세분화

냉각 기술별(주요 동향, 시장 규모 예측 및 전망, 2022-2029년)

공기 기반 냉각

CRAH

냉각기 및 이코노마이저

냉각탑(직접, 간접, 2단계 냉각 포함)

기타

액체 기반 냉각

액침 냉각

직접 칩 냉각

후면 도어 열교환기

업계별

IT 및 통신

소매 및 소비재

헬스케어

미디어 및 엔터테인먼트

연방 및 정부기관

기타 최종 사용자

국가별

미국

캐나다

제8장 경쟁 구도

기업 프로파일

Vertiv Group Corp.

Stulz GmbH

Schneider Electric SE

Rittal GmbH & Co. KG

Asetek A/S

Alfa Laval AB

Iceotope Technologies Limited

Green Revolution Cooling Inc.

Chilldyne Inc.

Airedale International Air Conditioning Ltd.

제9장 투자 분석

제10장 시장 기회와 앞으로의 동향

KTH

영문 목차

영문목차

The North America Data Center Cooling Market size is estimated at USD 7.20 billion in 2025, and is expected to reach USD 12.58 billion by 2030, at a CAGR of 11.8% during the forecast period (2025-2030).

The rapid development of various containerized, modular, and performance-optimized data center (POD) facilities is anticipated to boost the overall demand for various cooling systems that can be utilized in the data centers, driving the market's growth extensively.

The United States dominated the total North American data center cooling market mainly due to the growth in the development of colocation and hyperscale facilities with over 100 MW power capacity. A surge in the need for cost-effective and efficient data centers, healthy growth of enterprises with data centers, various green initiatives for eco-friendly data center solutions, and power density are expected to drive the market's growth.

In addition, the emergence of portable cooling and liquid-based cooling technologies and growth in the need for a modular data center cooling approach are expected to offer lucrative opportunities for the North American data center cooling market. The solution segment had ruled the North American data center cooling market primarily due to the rising adoption of energy-efficient, cost-effective, and environment-friendly cooling solutions in line with various stringent environmental safety rules offered by governmental bodies.

Moreover, the market witnessed significant product launches and innovations, driving the market significantly. For instance, in June 2023, a 5MW, state-of-the-art testing laboratory was commissioned at the Modine Rockbridge facility in Virginia, further expanding the services that Airedale by Modine can provide data center customers and meet growing demand from the data center industry for validated, sustainable cooling solutions. The new lab can test a complete range of air conditioning equipment, accommodating air-cooled chillers up to 2.1MW and water-cooled chillers up to 5MW.

However, the need for specialized infrastructure, higher investment costs, and various cooling challenges during a power outage are expected to restrict the growth of the North American data center cooling market throughout the forecast period.

The COVID-19 pandemic placed data centers in unchartered territory. There were many supply chain disruptions, and due to lockdowns globally, the smooth operations of the systems were hugely impacted. Owing to shipping disruptions and factory closures that affected the delivery of data center equipment, operators found workarounds to meet the challenges. However, during the post-COVID-19 period, the market is expected to witness various lucrative growth opportunities throughout the forecast period.

North America Data Center Cooling Market Trends

Growth in the Construction Sector Boosting the Demand for Furniture Products

The information technology (IT) industry primarily consists of the overall sales of information technology (IT) services and related goods by various entities such as sole traders, organizations, and partnerships that mainly apply computers, computer peripherals, and telecommunications equipment to retrieve, store, transmit and maneuver data. The IT market also involves computer networking, systems design services, broadcasting, information distribution technologies like telephones and television, and several other equipment used during the process. These huge requirements require a proper cooling system for the devices to perform normally, thereby driving the overall demand for the data center cooling market.

The IT industry needs on-premise private data storage as well as hyperscale data centers for its various operations according to the organization's size. The rise in the adoption of cloud storage has drastically increased over the years within the region, especially due to growth in SaaS providers, allowing cloud storage providers to extend their capacities, which is anticipated to maximize the demand for data center cooling systems.

The cooling system is essential in the IT and data center sector, primarily due to the need for various enhanced high-quality cooling solutions that are quite efficient than the traditional air-cooling solution. Also, the rise in technological innovation in the IT infrastructure, coupled with the increase in the demand for cooling systems among the various smartphone manufacturers for thermal management, is also driving the market growth extensively.

The United States plays a very significant role in terms of establishing various driving the market's growth rate, which is mainly due to the rising investments and establishments of the data center by the key major market players within the region. For instance, in January 2023, Amazon Web Services intends to invest a sum of around USD 35 billion by 2040 to establish various multiple data center campuses across Virginia.

Asia-Pacific is Expected to Hold Significant Market Share

The United States is poised to dominate the market in North America, owing to the presence of many services and software providers as well as high investments by colocation providers and hyper-scale data center operators. In the last few years, there has been a significant rise in the number of data centers. A considerable number of processors are being utilized in a given space to increase data centers' performance, which results in increased density. The requirement for power and cooling has grown along with increased density.

The United States also contributes substantially to the global data center requirements from the banking, IT, financial services, and insurance (BFSI), retail, and healthcare industries. Data center service providers in the region are prompted to manage their operating costs, as the region is a lucrative market, considering the number of data centers and their expansions.

Data centers' power density experiences growth by an average of 1.5 kW per rack, which results in limited air distribution and enhanced heat generation. In general, IT equipment typically needs between 100 and 160 cfm of air per kW, but in a dense environment, it diminishes to less than 100, which results in higher heat generation, driving the market's growth significantly.

The expansion of mobile broadband, the emergence of 5G, growth in Big Data analytics, and cloud computing are the primary factors driving the demand for new data center infrastructures in the United States. Network providers are working to ensure the rapid implementation of 5G for better innovation. Such developments are further driving the demand for efficient data center cooling solutions and services among United States's enterprises.

As per Cloudscene, as of September 2023, the total count of data centers in the United States was 5,375, whereas Germany ranked second with an overall count of 522 data centers. The United Kingdom ranked 3rd among countries in terms of the total number of data centers, with 517, while China recorded 448. This possession of a significant number of data centers in the United States is expected to amplify the market's growth throughout the forecast period.

North America Data Center Cooling Industry Overview

The North American data center cooling market is highly competitive and fragmented. Market penetration is growing with a strong presence of major players, such as Schneider Electric SE, Black Box Corporation, Asetek, Nortek Air Solutions LLC, Emerson Electric Co., Hitachi Ltd, Rittal GmbH & Co. KG, Fujitsu Ltd, Stulz GmbH, and Vertiv, in established markets. With the increasing focus on innovation, the demand for new technologies, such as liquid-based cooling and portable cooling technologies, is also growing, which, in turn, is driving investments for further developments in the region.

In May 2024, Stulz unveiled its latest innovation, the CyberCool Coolant Management and Distribution Unit (CDU), specifically engineered to optimize heat exchange efficiency in liquid cooling solutions. The product line comprises four models, available in two distinct sizes. These units boast an impressive heat exchange capacity, ranging from 345 kW to 1,380 kW. Stulz has set the rated water supply temperature for the facility water system at 32°C (89.6°F), with the liquid supply temperature for the technology cooling system pegged at 36°C (96.8°F).

In March 2024, Rittal Private Limited marked the opening of its new Integration Center, specifically tailored for Cooling Units and Liquid Cooling Package (LCP) solutions, at its Bangalore, India manufacturing plant. This strategic move not only bolsters the company's production capabilities but also positions it to cater to the escalating demand for Industrial Cooling Solutions.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview (Coverage: A detailed analysis of the current regional trends related to Data Center Cooling are included in this section)

4.2 Key cost considerations for Cooling

4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

4.2.2 Key innovations and developments in Data Center Cooling

4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

5.3 Market Opportunities

5.4 Comparison of raised floor with containment & raised floor without commitment

5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT REGIONAL DATA CENTER FOOTPRINT

6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

6.2 Regional Analysis of the Established DC Markets and Emerging DC Hotspots in North America region (we will include coverage by highlighting major established and emerging DC markets)

6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 DATA CENTER COOLING MARKET SEGMENTATION

7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)