데이터센터용 CDU 시장 : 유형별, 냉각 유형별, 최종사용자별, 지역별, 예측(-2032년)

Data Center Coolant Distribution Units Market by Type (In-Row, In-Rack, FDU), Cooling Type (Direct to Chip Cooling, Immersion Cooling), End User (Colocation Providers, Enterprises, Hyperscale), and Region Global Forecast to 2032

상품코드:1830051

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 263 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

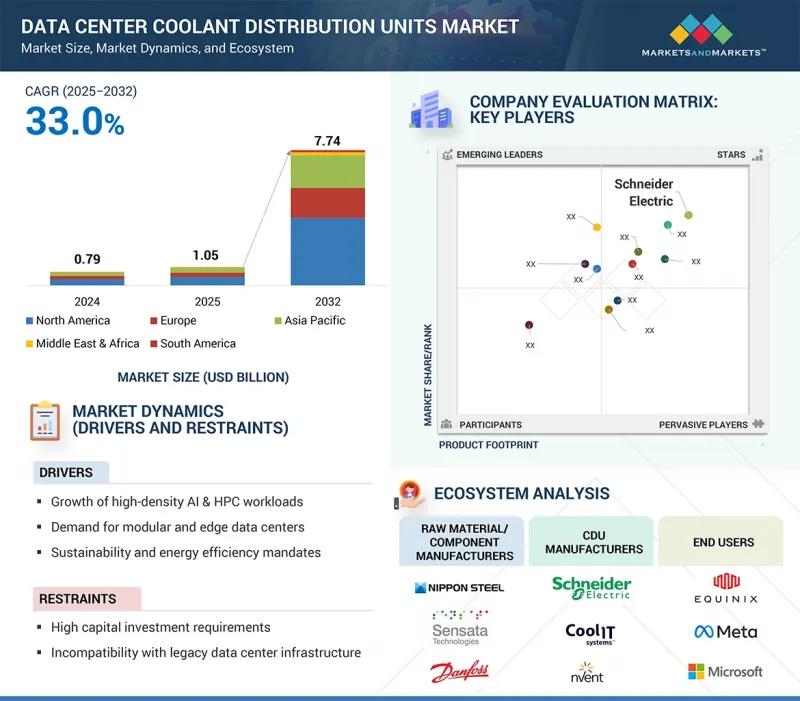

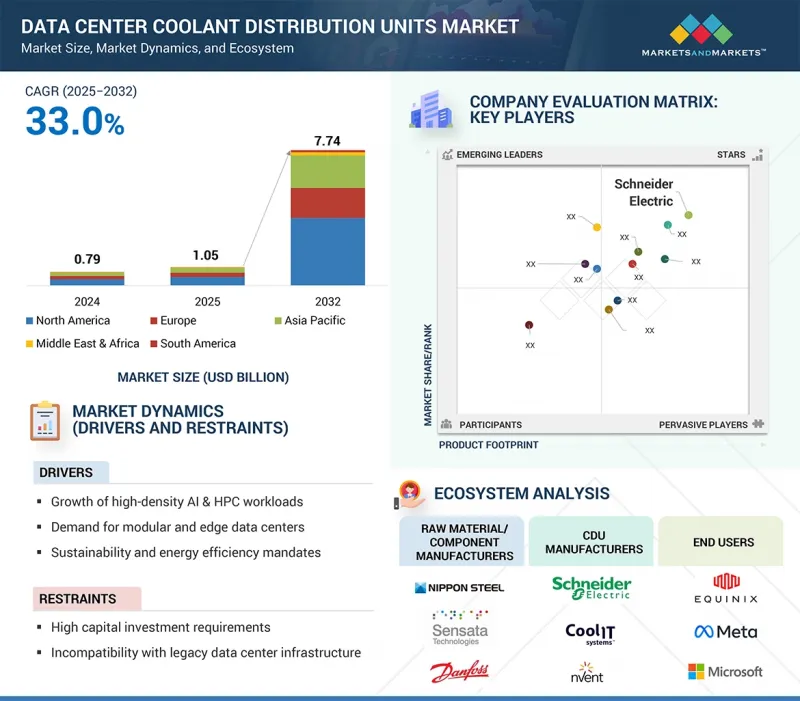

세계의 데이터센터용 CDU 시장 규모는 2025년 10억 5,000만 달러에서 2032년까지 77억 4,000만 달러에 이르고, 예측 기간에 CAGR 33.0%의 성장이 전망됩니다.

조사 범위

조사 대상 연도

2021-2032년

기준연도

2024년

예측 기간

2025-2032년

단위

100만 달러

부문

유형, 냉각 유형, 프로세스, 냉각 능력, 데이터센터 유형, 최종사용자, 지역

대상 지역

아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미

CDU는 수냉식 시스템의 중요한 구성요소로서 시설 수준의 냉각 인프라와 IT 기기를 연결하고 열원에서 효율적으로 열을 제거합니다. 또한, 정밀 냉각, 랙 밀도 향상, 에너지 사용 최적화를 실현할 수 있도록 지원합니다. 따라서 차세대 데이터센터에서 선호되는 솔루션이 되고 있으며, 이는 하이퍼스케일, 코로케이션, 엔터프라이즈, 엣지 시설에서 세계 CDU 시장의 급격한 성장을 견인하고 있습니다.

"FDU 부문이 예측 기간 동안 가장 높은 CAGR을 나타낼 것입니다. "

하이퍼스케일 및 엔터프라이즈 데이터센터에서의 고밀도 랙 배치가 증가함에 따라, 플로어 마운트 분배 장치(FDU) 부문은 예측 기간 동안 가장 빠른 CAGR로 성장할 것으로 예측됩니다. FDU는 높은 냉각 능력, 확장성, 대규모 IT 부하를 지원하는 능력을 갖추고 있어 AI, HPC, 클라우드 집약적인 워크로드를 실행하는 시설에 적합합니다. FDU는 시설 수준의 냉수 시스템과 밀접하게 연결되도록 설계되어 정확하고 신뢰할 수 있는 열 제거에 적합합니다. 북미, 유럽, 아시아태평양의 데이터센터에 대한 대규모 투자와 에너지 절약형 지속 가능한 냉각 솔루션으로의 전환이 FDU의 채택을 촉진하고 있습니다.

"Direct to Chip Cooling 부문이 예측 기간 동안 가장 높은 CAGR을 나타낼 것입니다. "

Direct to Chip Cooling 부문은 AI 워크로드, HPC, 고급 클라우드 컴퓨팅 설정에 사용되는 고성능 프로세서와 GPU에서 직접 열을 제거할 수 있는 능력으로 인해 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다. Direct to Chip Cooling 솔루션의 효율성은 열원에서의 열 관리에서 기존 공랭식 냉각을 능가하며, 고밀도 랙과 전반적인 시스템 성능을 지원합니다. 이 부문의 성장은 AI 기반 데이터센터, 대규모 HPC 구축, 기업의 디지털 전환 노력 증가로 인한 것으로 분석됩니다. 북미, 유럽, 아시아태평양 등의 지역에서는 하이퍼스케일 제공업체와 코로케이션 제공업체들이 수냉식 인프라에 많은 투자를 하고 있어, 도입이 더욱 가속화되고 있습니다. Direct to Chip Cooling 기술은 세계 지속가능성 및 에너지 효율 목표에 부합하는 기술입니다. DTC Cooling은 전력 소비를 줄일 뿐만 아니라 운영 안정성을 향상시켜 차세대 데이터센터에서 가장 수요가 많은 냉각 기술 중 하나로 자리매김하고 있습니다.

하이퍼스케일 데이터센터가 예측 기간 동안 가장 높은 CAGR을 나타낼 것입니다.

하이퍼스케일 데이터센터 부문은 AI, HPC, 빅데이터 용도의 급속한 확장, 세계 클라우드 제공업체들의 대규모 투자로 인해 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다. 하이퍼스케일 데이터센터는 높은 랙 밀도와 전력 수요로 운영되기 때문에 기존의 공랭식 냉각 방식으로는 충분하지 않은 것으로 밝혀졌습니다. 따라서 하이퍼스케일 사업자들은 효율적인 수냉식 냉각을 가능하게 하고, 에너지 사용을 최적화하며, 수천 대의 서버의 안정적인 열 관리를 보장하기 위해 CDU의 채택을 늘리고 있습니다. 북미, 유럽, 아시아태평양 등의 지역에서는 사업자들이 지속가능성 목표를 달성하면서 규모를 확대하고자 하기 때문에 채택이 증가하고 있습니다. CDU는 차세대 하이퍼스케일 데이터센터의 열효율 향상과 운영 비용 절감을 효과적으로 지원하는 차세대 하이퍼스케일 데이터센터에 매우 중요한 기술이 되고 있습니다.

"북미가 예측 기간 동안 가장 큰 시장 점유율을 차지할 것입니다. "

북미는 주로 하이퍼스케일 데이터센터, 코로케이션 데이터센터, 엔터프라이즈 데이터센터 생태계가 구축되어 있어 예측 기간 동안 데이터센터용 CDU 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 미국은 클라우드 도입 및 AI 기반 인프라의 주요 국가 중 하나이며, Google, Microsoft, Amazon, Meta 등 주요 수냉식 기업들을 보유하고 있습니다. 이들 기업은 더 높은 랙 밀도와 에너지 효율이 필요한 용도를 위한 수냉식 기술 개발 및 채택에 집중 투자하고 있습니다.

세계의 데이터센터용 CDU 시장에 대해 조사 분석했으며, 주요 성장 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

The global data center coolant distribution units market is projected to grow from USD 1.05 billion in 2025 to USD 7.74 billion by 2032, at a CAGR of 33.0% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD Million)

Segments

Type, Cooling Type, Process, Capacity, Data Center Type, End User, and Region

Regions covered

Asia Pacific, Europe, North America, the Middle East & Africa, and South America

Coolant distribution units act as an important component in liquid cooling systems, connecting the facility-level cooling infrastructure with the IT equipment to efficiently remove heat at the source. They support the delivery of precision cooling, higher rack densities, and optimized energy use. This makes them a preferred solution in next-generation data centers. Consequently, this fuels the rapid growth of the global coolant distribution units market in hyperscale, colocation, enterprise, and edge facilities.

"FDU segment to register highest CAGR during forecast period"

The Floor-Mounted Distribution Unit (FDU) segment is expected to grow at the fastest CAGR during the forecast period due to increasing deployments of high-density racks in hyperscale and enterprise data centers. FDUs offer high cooling capacity, scalability, and the ability to support large IT loads, making them ideal for facilities that perform AI, HPC, and cloud-intensive workloads. They are designed to connect closely with facility-level chilled water systems, which makes them well-suited for precise and reliable heat removal. Large investments in data centers across North America, Europe, and Asia-Pacific, combined with a shift toward energy-efficient and sustainable cooling solutions, have driven the adoption of FDUs.

"Direct to Chip Cooling segment to record highest CAGR during forecast period"

The Direct to Chip Cooling segment is projected to grow at the highest CAGR during the forecast period, driven by its ability to remove heat directly from high-performance processors and GPUs used in AI workloads, HPC, and advanced cloud computing setups. The efficiency of direct to chip cooling solutions surpasses traditional air cooling for thermal management at the source, supporting higher-density racks and overall system performance. The growth of this segment is largely due to the rise of AI-powered data centers, large-scale HPC deployments, and digital transformation initiatives by enterprises. Regions such as North America, Europe, and Asia-Pacific are further boosting adoption, with hyperscale and colocation providers investing heavily in liquid-cooling infrastructure. Direct to chip cooling technologies align with global sustainability and energy-efficiency goals. Besides reducing power consumption, DTC cooling improves operational reliability, making it one of the most in-demand cooling technologies in next-generation data centers.

Hyperscale data centers to record highest CAGR during forecast period"

The Hyperscale Data Center segment is expected to grow at the highest CAGR during the forecast period, driven by rapid expansion in AI, HPC, big data applications, and significant investments from global cloud providers. Traditional air-cooling methods are proving inadequate as hyperscale data centers operate with high rack densities and power demands. Therefore, hyperscale operators are adopting more coolant distribution units to enable efficient liquid cooling, optimize energy use, and ensure reliable heat management for thousands of servers. Regions such as North America, Europe, and Asia-Pacific are leading the way in adoption, as operators aim to scale up while meeting sustainability goals. Coolant distribution units are becoming a crucial technology for next-generation hyperscale data centers, effectively supporting improved thermal efficiency and lowering operating costs.

"North America to account for maximum market share during forecast period"

North America is expected to hold the largest share of the data center coolant distribution units market during the forecast period, primarily due to the well-established ecosystem of hyperscale, colocation, and enterprise data centers. The US is one of the top countries for cloud adoption and AI-driven infrastructure and hosts some of the major liquid-cooling companies, such as Google, Microsoft, Amazon, and Meta, which heavily invest in developing and adopting liquid-cooling technologies for applications requiring higher rack densities and energy efficiency. Additionally, the strong regulatory focus on sustainability and carbon reduction, along with the availability of advanced cooling technologies and robust infrastructure, further strengthen North America's position in this market. Favorable investment trends, rapid digitalization of sectors, and early adoption of next-generation liquid-cooling technology ensure that North America will continue to dominate the data center coolant distribution units market throughout the forecast period.

Profile break-up of primary participants for the report:

By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

By Designation: C-level- 30%, Director Level- 40%, and Others - 30%

By Region: North America - 25%, Europe - 30%, Asia Pacific - 35%, South America - 5%, and Middle East & Africa - 5%

Schneider Electric (France), Vertiv Group Corp. (US), Delta Electronics, Inc. (Taiwan), nVent (US), and DCX Liquid Cooling Systems (Poland) are some of the major players in the data center coolant distribution units market. These companies have adopted strategies such as product launches, acquisitions, collaborations, and expansion to grow their market share and revenue.

Research Coverage

The report defines, segments, and estimates the size of the data center coolant distribution units market based on type, cooling type, end user, and region. It strategically profiles key players and thoroughly analyzes their market share and core competencies. It also monitors and examines competitive developments, such as new product development, collaborations, partnerships, acquisitions, and expansions that they undertake in the market.

Reasons to Buy the Report

The report is intended to help both market leaders and new entrants by providing close estimates of revenue figures for the data center coolant distribution units and their segments. It aims to assist stakeholders in understanding the market's competitive landscape, gaining insights to strengthen their business positions, and developing effective go-to-market strategies. Additionally, it enables stakeholders to understand market trends and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of critical drivers (Growth of high-density AI & HPC workloads), restraints (High capital investments), opportunities (AI-based cooling control and predictive optimization), and challenges (precision control and flow management complexity) influencing the growth of the data center coolant distribution units.

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities in the data center coolant distribution units.

Market Development: Comprehensive information about lucrative markets - the report analyzes the data center coolant distribution units across varied regions.

Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the data center coolant distribution units.

Competitive Assessment: Comprehensive analysis of market shares, growth strategies, and product offerings of leading companies such as DCX Liquid Cooling Systems (Poland), nVent (US), NIDEC CORPORATION (Japan), Schneider Electric (France), Vertiv Group Corp (US), KAORI HEAT TREATMENT CO., LTD. (Taiwan), Shenzhen Envicool Technology Co., Ltd. (China), Boyd (US), Delta Electronics Inc. (Taiwan), Coolcentric (US), Hewlett Packard Enterprise Development LP (US), LiquidStack Holding B.V. (US), Shanghai Venttech Refrigeration Equipment Co., Ltd. (China), Chilldyne Inc. (US), COOLIT SYSTEMS (Canada), Trane (Ireland), Munters Group AB (Sweden), Lenovo (China), Super Micro Computer Inc. (US), STULZ GMBH (Germany), Rittal GmbH & Co. KG (Germany), LITE-ON Technology Corporation (Taiwan), FlaktGroup (Germany), and Nautilus Data Technologies (US) in the data center coolant distribution units.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Breakdown of interviews with experts

2.2 MATRIX CONSIDERED FOR DEMAND-SIDE ANALYSIS

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.4 CALCULATION FOR SUPPLY-SIDE ANALYSIS

2.5 GROWTH FORECAST

2.6 DATA TRIANGULATION

2.7 RESEARCH ASSUMPTIONS

2.8 RESEARCH LIMITATIONS

2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES IN DATA CENTER COOLANT DISTRIBUTION UNITS MARKET

4.2 DATA CENTER COOLANT DISTRIBUTION UNITS MARKET, BY COOLING TYPE

4.3 DATA CENTER COOLANT DISTRIBUTION UNITS MARKET, BY END USE

4.4 NORTH AMERICA: DATA CENTER COOLANT DISTRIBUTION UNITS MARKET, BY TECHNOLOGY AND COUNTRY

4.5 DATA CENTER COOLANT DISTRIBUTION UNITS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 MARKET DYNAMICS

5.1.1 DRIVERS

5.1.1.1 Growth of high-density AI & HPC workloads

5.1.1.2 Demand for modular and edge data centers

5.1.1.3 Sustainability and energy efficiency mandates

5.1.2 RESTRAINTS

5.1.2.1 High capital investment

5.1.2.2 Incompatibility with legacy data center infrastructure

5.1.3 OPPORTUNITIES

5.1.3.1 Integration with waste heat recovery systems

5.1.3.2 Innovation in nanofluids and next-generation coolants

5.1.3.3 AI-based cooling control and predictive optimization

5.1.4 CHALLENGES

5.1.4.1 Precision control and flow management complexity

5.1.4.2 Integration with diverse cooling architectures

6 INDUSTRY TRENDS

6.1 PORTER'S FIVE FORCES ANALYSIS

6.1.1 THREAT OF NEW ENTRANTS

6.1.2 THREAT OF SUBSTITUTES

6.1.3 BARGAINING POWER OF BUYERS

6.1.4 BARGAINING POWER OF SUPPLIERS

6.1.5 INTENSITY OF COMPETITIVE RIVALRY

6.2 KEY STAKEHOLDERS AND BUYING CRITERIA

6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.2.2 BUYING CRITERIA

6.3 VALUE CHAIN ANALYSIS

6.3.1 RAW MATERIAL SUPPLIERS

6.3.2 COMPONENT MANUFACTURERS

6.3.3 SYSTEM ASSEMBLERS/COOLANT DISTRIBUTION UNITS MANUFACTURERS

6.3.4 OEMS/SYSTEM INTEGRATORS

6.3.5 END USE

6.4 ECOSYSTEM ANALYSIS

6.5 TECHNOLOGY ANALYSIS

6.5.1 KEY TECHNOLOGY

6.5.1.1 Direct-to-Chip Liquid Cooling (D2C)

6.5.1.2 Two-Phase Liquid Cooling

6.5.2 ADJACENT TECHNOLOGY

6.5.2.1 Immersion Cooling Systems

6.5.2.2 Rear Door Heat Exchangers (RDHx)

6.5.3 COMPLEMENTARY TECHNOLOGY

6.5.3.1 Advanced Thermal Interface Materials

6.5.3.2 Thermal Interface Materials (TIMs)

6.6 CASE STUDY ANALYSIS

6.6.1 IMPACT OF COOLANT DISTRIBUTION DESIGN ON SERVER-LEVEL THERMAL MANAGEMENT IN DATA CENTERS

6.6.1.1 Objective

6.6.1.2 Solution Statement

6.6.2 COMMISSIONING OF LIQUID-TO-AIR COOLANT DISTRIBUTION UNITS FOR DIRECT-TO-CHIP DATA CENTER COOLING

6.6.2.1 Objective

6.6.2.2 Solution Statement

6.7 PATENT ANALYSIS

6.7.1 METHODOLOGY

6.8 PRICING ANALYSIS

6.8.1 AVERAGE SELLING PRICE TREND OF DATA CENTER IMMERSION COOLING FLUIDS, BY REGION, 2024

6.8.2 AVERAGE SELLING PRICE TREND OF DATA CENTER COOLANT DISTRIBUTION UNITS, BY KEY PLAYER, 2024

6.8.3 AVERAGE SELLING PRICE TREND OF DATA CENTER COOLANT DISTRIBUTION UNITS, BY TYPE, 2024

6.9 REGULATORY LANDSCAPE

6.9.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.10 KEY CONFERENCES & EVENTS IN 2025

6.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.12 GLOBAL MACROECONOMIC OUTLOOK

6.12.1 GDP

6.13 INVESTMENT AND FUNDING SCENARIO

6.14 IMPACT OF 2025 US TARIFF

6.14.1 INTRODUCTION

6.15 KEY TARIFF RATES

6.16 PRICE IMPACT ANALYSIS

6.17 IMPACT ON COUNTRY/REGION

6.17.1 US

6.17.2 EUROPE

6.17.3 ASIA PACIFIC

6.18 IMPACT ON END-USE INDUSTRIES

6.19 IMPACT OF AI/GEN AI

6.19.1 INTRODUCTION

6.19.2 SURGE IN THERMAL LOAD FROM AI INFRASTRUCTURE

6.19.3 AI-ENHANCED COOLANT DISTRIBUTION UNITS INTELLIGENCE AND CONTROL

6.19.4 PREDICTIVE MAINTENANCE AND FAULT DETECTION

6.19.5 GENERATIVE AI IN COOLANT DISTRIBUTION UNITS DESIGN AND SIMULATION

6.19.6 DCIM INTEGRATION AND SMART COOLING ORCHESTRATION

6.19.7 COOLANT DISTRIBUTION UNITS MARKET OPPORTUNITY ALIGNED WITH AI DEMAND

7 DATA CENTER COOLANT DISTRIBUTION UNITS MARKET, BY TYPE

7.1 INTRODUCTION

7.2 IN-ROW COOLANT DISTRIBUTION UNITS

7.2.1 SPACE-SAVING COOLING SOLUTION WITH TARGETED EFFICIENCY TO SUPPORT HIGH-DENSITY DATA CENTER GROWTH

7.3 IN-RACK COOLANT DISTRIBUTION UNITS

7.3.1 RACK-INTEGRATED COOLING FOR PRECISION FLOW CONTROL IN HIGH-DENSITY DATA CENTERS

7.4 FACILITY DISTRIBUTION UNITS

7.4.1 HIGH-CAPACITY COOLING INFRASTRUCTURE FOR FACILITY-WIDE LIQUID-COOLED DATA CENTERS

8 DATA CENTER COOLANT DISTRIBUTION UNITS MARKET, BY COOLING TYPE

8.1 INTRODUCTION

8.2 DIRECT TO CHIP COOLING

8.2.1 COMPACT COOLING ARCHITECTURE ACCELERATES INTEGRATION IN HIGH-DENSITY RACKS

8.3 IMMERSION COOLING

8.3.1 IMMERSION COOLING ARCHITECTURE ACCELERATING DEPLOYMENT IN HIGH-DENSITY COMPUTE ENVIRONMENTS

9 DATA CENTER COOLANT DISTRIBUTION MARKET, BY END USE

9.1 INTRODUCTION

9.2 COLOCATION PROVIDERS

9.2.1 ENABLING FLEXIBLE COOLING FOR MULTI-TENANT HIGH-DENSITY ENVIRONMENTS