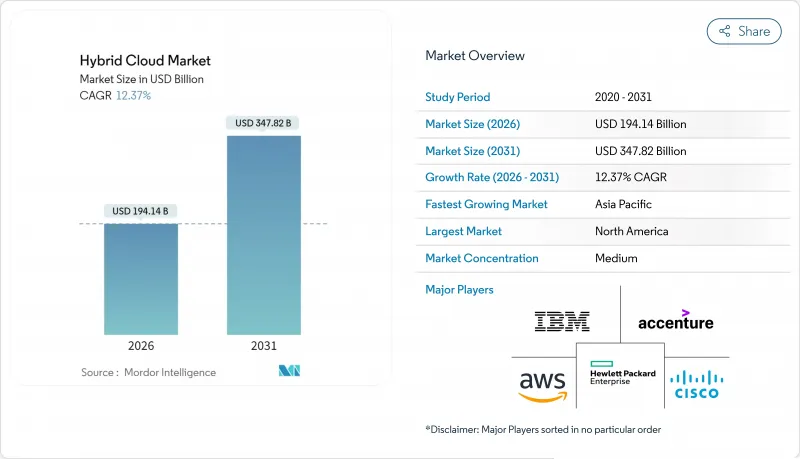

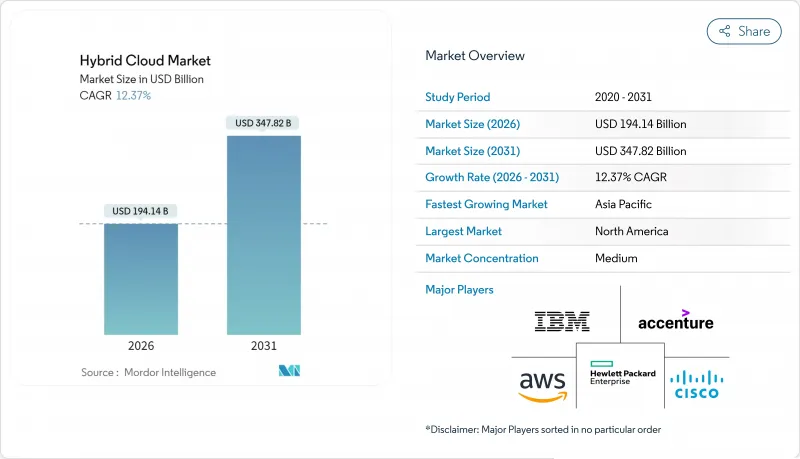

하이브리드 클라우드 시장은 2025년 1,727억 7,000만 달러로 평가되었고, 2026년 1,941억 4,000만 달러에서 2031년까지 3,478억 2,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 12.37%를 나타낼 전망입니다.

기업들은 운영 통제와 클라우드 네이티브 속도의 균형을 이루는 분산형 아키텍처로 전환하고 있으며, 특히 생성형 AI 워크로드가 엣지와 중앙 집중형 컴퓨팅 리소스 간의 긴밀한 연계를 요구함에 따라 이러한 추세가 가속화되고 있습니다. 강화되는 주권 규정, 멀티클라우드 선호도, 성숙해지는 컨테이너 오케스트레이션 프레임워크는 하이브리드 배포 모델에 대한 수요를 촉진합니다. 엣지 컴퓨팅 투자는 AI 추론의 지연 시간을 단축하는 동시에 규정 준수를 위해 온프레미스 데이터를 유지합니다. 대형 데이터센터 운영사들은 인프라 프로젝트를 기업의 탈탄소화 목표와 연계하며, 조달 기준으로 지속가능성을 추가하고 있습니다. 하이퍼스케일러와 전문 엣지 제공업체들의 전략적 인수는 하이브리드 클라우드 시장 전반에 걸쳐 경쟁 차별화를 심화시키고 있습니다.

하이브리드 환경은 이제 신중한 멀티클라우드 전략의 기반이 되고 있으며, 87%의 기업이 두 개 이상의 공급업체에 걸쳐 워크로드를 운영하고 있습니다. 플랫폼 팀은 중복 지출을 억제하고 거버넌스 일관성을 개선하기 위해 툴링을 표준화합니다. 하이브리드 클라우드 시장의 낭비를 줄이기 위해 설계 단계부터 재무 운영 관행이 내재화됩니다. 공급업체들은 사용량을 비용 센터에 매핑하는 통합 청구 대시보드를 제공하며 대응합니다. 멀티클라우드 성숙도가 높아짐에 따라 원활한 워크로드 이동성은 하이브리드 클라우드 시장의 핵심 구매 기준이 됩니다.

엄격한 개인정보 보호 규정이 워크로드 배치 결정을 재편하고 있으며, 특히 유럽에서는 84%의 조직이 12개월 이내에 주권 클라우드 솔루션을 사용하거나 도입할 계획입니다. 호주와 아시아 일부 지역도 유사한 규정을 채택하여 공급업체들이 지역별 제어 평면을 출시하도록 압박하고 있습니다. 특화된 주권 서비스는 데이터 거주지 보장, 키 관리, 현지 운영자 인력을 약속합니다. 하이퍼스케일러들은 이제 기밀 컴퓨팅과 전용 EU 지원 모델을 통합하여 하이브리드 클라우드 시장 점유율을 유지하고 있습니다. 따라서 규정 준수 복잡성은 민감한 데이터를 관할권 내에 유지하면서도 규제 부담이 적은 워크로드에는 세계의 규모를 활용하는 아키텍처 설계 수요를 촉진합니다.

현대화 프로젝트는 종종 문서화되지 않은 종속성을 드러내며 일정과 예산을 부풀립니다. 대형 은행들은 하이브리드 환경을 위한 핵심 결제 시스템 리팩토링 시 상당한 초과 비용을 보고합니다. 현재 기업의 73%는 리프트 앤 시프트 대신 리팩토링을 선택하여 일정은 연장되지만 더 나은 복원력을 제공합니다. 지속적 통합 파이프라인과 API 게이트웨이가 일부 장벽을 완화하지만, 기술적 부채는 하이브리드 클라우드 시장에 단기적 부담으로 남아 있습니다.

서비스 매출은 2025년 솔루션이 하이브리드 클라우드 시장 점유율 64.80%를 유지했음에도 불구하고 2031년까지 연평균 14.68% 성장할 것으로 전망됩니다. 이러한 높은 성장세는 기업들이 멀티클라우드 오케스트레이션, 주권 매핑, AI 스택 튜닝에 대한 전문가 지도를 요청함에 기인합니다. 랙스페이스(Rackspace)와 AWS는 툴링과 전문 서비스를 결합하여 전환 기간을 단축하는 ‘Rapid Migration Offer’ 프로그램을 출시했습니다.

관리형 핀옵스(FinOps), 컨테이너 보안, 플랫폼 운영에 대한 수요가 증가하면서 공급업체들은 서비스 라인을 확장하고 있습니다. 누타닉스(Nutanix)는 기술 인력 부족을 상쇄하기 위해 소프트웨어와 컨설팅을 결합한 엔터프라이즈 AI 플랫폼을 선보였습니다. 이러한 추세는 조직들이 복잡성을 아웃소싱함에 따라 서비스 부문이 하이브리드 클라우드 시장 규모에서 더 큰 비중을 차지할 것임을 시사합니다.

IaaS는 2026-2031년에 걸쳐 CAGR 13.62%로 확대될 것으로 전망됩니다. 한편 SaaS는 확고한 기업용 제품군 덕분에 54.10% 점유율을 유지할 전망입니다. 생성형 AI 훈련에는 GPU가 풍부한 클러스터가 필요하며, 고객들은 맞춤형 튜닝을 위해 종종 IaaS 위에 이를 구축합니다. Oracle은 컴퓨팅 자원을 열악한 지역에 배치하는 로빙 엣지(Roving Edge) 디바이스를 통해 분산형 클라우드 라인을 확장하며 IaaS의 다용도성을 강조했습니다.

Platform-as-a-Service(PaaS)는 추상화를 제공하면서도 맞춤형 런타임을 허용하는 전략적 가교 역할을 합니다. 스노우플레이크는 애널리틱스 개발자의 모델 사용을 간소화하기 위해 자사 플랫폼을 Azure OpenAI 서비스와 연동했습니다. AI와 개발 워크플로의 융합은 하이브리드 클라우드 시장에서 세 가지 모델 모두를 상호 연결된 상태로 유지할 것입니다.

하이브리드 클라우드 시장은 컴포넌트(솔루션, 서비스), 서비스 모델(IaaS, PaaS, SaaS), 조직 규모(대기업, 중소기업), 최종 사용자 업계(정부, 공공 부문, 의료 및 생명 과학, BFSI 등) 및 지역별로 분할됩니다. 시장 예측은 금액(달러) 기준으로 제공됩니다.

북미는 2025년 매출 점유율 25.30%를 기록했으며, 멀티클라우드 도입을 간소화하는 고밀도 하이퍼스케일러 인프라의 혜택을 누리고 있습니다. TP ICAP는 2026년까지 시스템의 80%를 AWS로 이전하는 동시에 자본 시장 혁신을 위한 AI 연구소를 설립할 계획입니다. 연방 개인정보 보호 규정은 관리 가능한 수준을 유지하여 기업들이 하이브리드 클라우드 시장 전반에 걸쳐 워크로드 배치를 자유롭게 최적화할 수 있도록 합니다.

아시아태평양 지역은 용량 증설과 디지털 서비스 수요 증가에 힘입어 2031년까지 12.89%의 가장 가파른 연평균 복합 성장률(CAGR)을 보일 전망입니다. 마이크로소프트는 증가하는 추론 요구사항을 해결하기 위해 일본 내 신규 AI 및 클라우드 존 구축에 29억 달러를 투자하기로 약속했습니다. 중국 공급업체들은 국내 성장세가 둔화됨에 따라 해외 확장을 추진 중입니다. 지역별 데이터센터 용량은 현재 가동 중인 12,206MW와 건설 중인 14,338MW로 총 26,544MW에 달하며, 이는 향후 하이브리드 클라우드 시장 성장을 뒷받침할 전망입니다.

유럽은 84%의 기업이 주권 클라우드 프레임워크를 도입하거나 계획 중이어서 꾸준한 성장세를 보이고 있습니다. 마이크로소프트는 논리적 격리, 현지 키 관리, EU 현지 지원팀을 아우르는 계층적 주권 솔루션을 출시했습니다. 러시아와 사우디아라비아의 강화된 데이터 현지화 법규는 복잡성을 가중시키지만 지역 전문가들에게 기회도 창출합니다. MEA 및 남미 신흥 시장들은 해저 케이블 노선과 재생에너지 프로젝트로 장벽이 낮아지면서 투자를 가속화해 하이브리드 클라우드 시장을 확장하고 있습니다.

The hybrid cloud market was valued at USD 172.77 billion in 2025 and estimated to grow from USD 194.14 billion in 2026 to reach USD 347.82 billion by 2031, at a CAGR of 12.37% during the forecast period (2026-2031).

Enterprises are steering toward distributed architectures that balance operational control with cloud-native speed, especially as generative-AI workloads require tight linkage between edge and centralized compute resources. Growing sovereignty rules, multicloud preferences, and maturing container orchestration frameworks spur demand for hybrid deployment models. Edge computing investments shorten latency for AI inference while retaining on-premises data for compliance. Large data-center operators are aligning infrastructure projects with corporate decarbonization targets, adding sustainability as a procurement criterion. Strategic acquisitions by hyperscalers and specialized edge providers intensify competitive differentiation across the hybrid cloud market.

Hybrid environments now underpin deliberate multicloud strategies, with 87% of enterprises operating workloads across more than one provider.Platform teams standardize tooling to curb redundant spend and improve governance consistency. Financial-operations practices are embedded at design stages to cut waste in the hybrid cloud market. Vendors respond by offering unified billing dashboards that map usage to cost centers. As multicloud maturity rises, seamless workload portability becomes a core purchase criterion for the hybrid cloud market.

Strict privacy regimes reshuffle workload placement decisions, particularly in Europe where 84% of organizations either use or plan sovereign cloud solutions within 12 months.Australia and parts of Asia adopt similar rules, pressing providers to launch region-specific control planes. Specialized sovereign offerings promise residency, key management, and local operator staffing. Hyperscalers now integrate confidential computing and dedicated EU support models to retain share in the hybrid cloud market. Compliance complexity therefore fuels demand for architecture designs that keep sensitive data in jurisdiction while leveraging global scale for less regulated workloads.

Modernization projects often reveal undocumented dependencies that inflate timelines and budgets. Large banks report significant overruns when refactoring core payment systems for hybrid environments. Seventy-three percent of enterprises now refactor rather than lift-and-shift, extending schedules yet delivering better resilience. Continuous integration pipelines and API gateways partly mitigate the hurdle, but technical debt remains a near-term drag on the hybrid cloud market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services revenue is forecast to rise at 14.68% CAGR through 2031, even though solutions retained 64.80% hybrid cloud market share in 2025. The higher growth stems from enterprises requesting expert guidance for multicloud orchestration, sovereignty mapping, and AI stack tuning. Rackspace and AWS launched Rapid Migration Offer programs that bundle tooling with professional services to shorten cut-over durations.

Demand for managed FinOps, container security, and platform operations pushes providers to expand service lines. Nutanix introduced an Enterprise AI platform that blends software with consulting to offset skills shortages. These trends suggest the services segment will account for a larger slice of hybrid cloud market size as organizations outsource complexity.

IaaS is projected to grow at 13.62% CAGR during 2026-2031, while SaaS keeps 54.10% share thanks to entrenched enterprise suites. Generative-AI training needs GPU-rich clusters that customers often build on IaaS for custom tuning. Oracle extended its distributed cloud line with Roving Edge devices that place compute in austere locations, underscoring the versatility of IaaS.

Platform-as-a-Service occupies a strategic bridge, offering abstraction yet permitting custom runtimes. Snowflake linked its platform with Azure OpenAI Service to simplify model usage for analytics developers. The convergence of AI and development workflows will keep all three models interlinked within the hybrid cloud market.

Hybrid Cloud Market is Segmented by Component (Solutions, Services), Service Model (IaaS, Paas, Saas), Organization Size (Large Enterprises, Smes), End-User Industry (Government and Public Sector, Healthcare and Life Sciences, BFSI, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America captured 25.30% revenue share in 2025 and benefits from dense hyperscaler footprints that simplify multicloud adoption. TP ICAP plans to shift 80% of systems to AWS by 2026 while creating AI labs for capital-markets innovation. Federal privacy rules remain manageable, allowing firms to optimize workload placement freely across the hybrid cloud market.

Asia-Pacific exhibits the steepest 12.89% CAGR through 2031, driven by capacity additions and rising digital-service demand. Microsoft pledged USD 2.9 billion for new AI and cloud zones in Japan to address growing inference requirements. China's providers pursue overseas expansion as domestic growth moderates. Regional data-center capacity now totals 12,206 MW in operation with 14,338 MW under build, underpinning future hybrid cloud market growth.

Europe advances at a steady clip as 84% of firms either deploy or plan sovereign cloud framework adoption. Microsoft rolled out a layered sovereignty solution spanning logical isolation, local key control, and EU-native support teams. Stricter data-localization laws in Russia and Saudi Arabia add complexity but also create opportunities for regional specialists. Emerging markets across MEA and South America accelerate investment as submarine cable routes and renewable energy projects reduce barriers, expanding the hybrid cloud market.