남미의 레디믹스 콘크리트 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

South America Ready Mix Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1684083

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

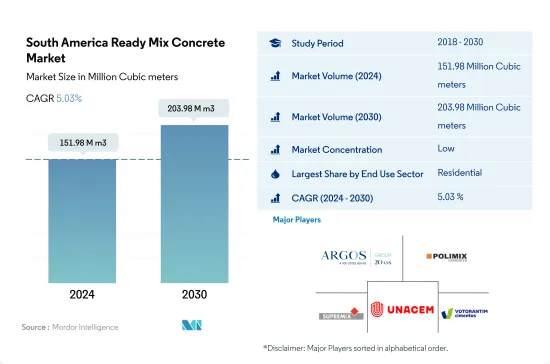

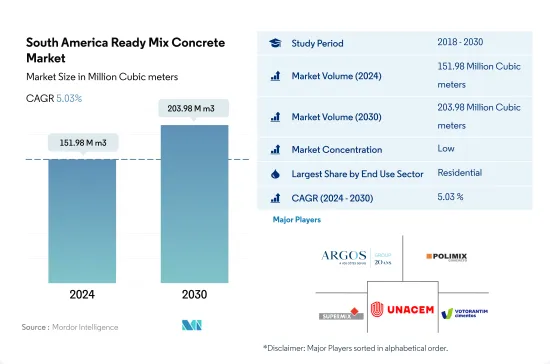

남미의 레디믹스 콘크리트 시장 규모는 2024년에 1억 5,198만 입방미터로 평가되었고, 2030년에는 2억 398만 입방미터에 이를 전망이며, 예측 기간(2024-2030년) 중 CAGR 5.03%로 성장할 것으로 예측됩니다.

상업 부문이 이 지역에서 가장 급성장하는 최종 용도 부문인 반면, 주택 부문은 남미의 예측 기간 동안 최고 자리를 유지할 전망입니다.

2022년 남미에서는 레디믹스 콘크리트 소비가 급증하여 전년 대비 1,410만 톤의 현저한 성장을 보였습니다. 이 회복은 이 지역이 COVID-19 팬데믹의 좌절에서 회복된 것이 주된 원인입니다. 분야를 넘어 건설 활동이 급증하면서 남미는 2023년 레디믹스 콘크리트 소비량이 1.71% 증가했습니다.

2022년에는 주택 부문이 남미의 레디믹스 콘크리트 시장 지배하여 36.3%의 큰 점유율을 차지했습니다. 이 분야에서 운송용 레디믹스 콘크리트가 선호되는 옵션으로 부상했으며, 이 분야 총 소비량의 75%를 크게 차지했습니다. 예측에 따르면 2023년 주택 부문의 레디믹스 콘크리트 수요는 1억 4,480만 입방미터 가까이 증가하였으며 2022년부터 1.71% 증가했습니다.

남미의 인프라 부문은 레디믹스 콘크리트 분야의 또 다른 중요한 기업입니다. 2022년에는 이 지역 수요의 30%라는 큰 점유율을 차지했습니다. 특히 운송용 레디믹스 콘크리트는 2023-2030년 가장 높은 CAGR 4.86%를 나타낼 것으로 예상되고 있습니다.

남미의 상업 분야는 예측 기간 동안 CAGR 5.78%로 예측되며 레디믹스 콘크리트 소비의 가장 현저한 급증을 보일 전망입니다. 이 상승은 주로 이 지역의 상업 바닥 면적의 확대로 인한 것입니다. 예를 들어 상업용 신규 바닥 면적은 예측 기간 2023-2030년 중 2억 1,100만 평방피트에서 2억 8,300만 평방피트로 확대될 것으로 예상됩니다.

브라질은 남미 최대의 급성장 레디믹스 콘크리트 시장

남미에서 레디믹스 콘크리트 시장은 주로 주택 부문과 인프라 부문이 견인하고 있습니다. 2022년 이 분야의 점유율은 각각 36%와 30%였습니다. 2023년, 이 지역 레디믹스 콘크리트 소비량은 2022년 대비 약 1.71% 증가하여 주로 주택 부문 수요 증가가 그 요인이 되고 있습니다.

남미 국토의 절반 이상을 차지하고, 이 지역 최대의 경제대국인 브라질은 레디믹스 콘크리트의 주요 소비국입니다. 2022년에는 브라질 주택 부문이 이 나라의 총 소비량의 63%를 차지하며 상당한 성장을 보였습니다. 상업 부문의 신규 바닥 면적이 가장 높은 성장률을 나타낼 것으로 예상되며, 소비량은 예측 기간 동안 CAGR 7.65%를 나타낼 것으로 예측되고 있습니다.

남미 제2경제대국인 아르헨티나도 이 지역의 레디믹스 콘크리트 소비량에서 돌출한 지위를 차지하고 있습니다. 2022년 아르헨티나 주택 부문 소비량은 220만 입방미터로 2021년부터 4.44% 감소했습니다. 아르헨티나 시장은 레디믹스 콘크리트의 전통적인 형태인 트랜짓 믹스 유형이 지배적입니다.

남미 국가들 중에서 브라질은 가장 낮은 레디믹스 콘크리트 소비량의 급증을 예상하고 있으며 예측 기간 동안 CAGR은 6.02%를 기록할 전망입니다. 이 성장은 벌크 체적 감소 및 트럭 적재 능력 향상과 같은 이점을 제공하는 수축 콘크리트의 채택이 증가하고 있기 때문입니다. 브라질의 수축 콘크리트 소비량은 예측 기간 동안 가장 빠른 CAGR 7.22%를 나타낼 것으로 예상됩니다.

남미의 레디믹스 콘크리트 시장 동향

이 지역의 외국 직접투자(FDI) 확대가 향후 시장 수요를 뒷받침

2022년 남미의 상업 부문에서는 아르헨티나의 9.16% 감소로 크게 견인되어 신규 바닥 면적이 16.2%로 대폭 감소했습니다. 그러나 이 분야는 2023년에는 회복을 향해 생산량이 4.75% 증가한 것으로 평가됩니다. 이 성장은 2022년에 이 지역의 다양한 산업이 외국 직접투자(FDI)를 유치함으로써 경제 성장 및 상업 건축의 급증에 기인하고 있습니다. 2022년 라틴아메리카 카리브해 경제위원회(ECLAC)는 이 지역의 FDI가 55.2% 증가했다고 보고했습니다.

이 부문의 건설량은 2020년에는 15.9%, 2021년에는 3.29%의 현저한 성장을 보였습니다. 이 성장은 남미 정부가 인프라와 건설 부문을 선호한 결과입니다. 남미 정부는 규제를 완화하고 민간 및 유틸리티에서 건설, 유지 보수 및 프로젝트 개발을 허용했습니다. 이 움직임은 중요한 이정표, 기한, 경기 회복 목표를 달성하는 것을 목표로 합니다.

남미의 상업 부문에서는 신규 바닥 면적 건설이 견조한 성장을 보이며 예측 기간 2023-2030년 CAGR은 수량 기준으로 4%를 나타낼 것으로 예측되고 있습니다. 이 지역에서는 상업 시설의 건설 상황에 현저한 변화가 있습니다. 2023년에 시작된 파울리니아 데이터센터와 포르투알레그리 데이터센터 i와 같은 주목할 만한 프로젝트는 이 지역에서 가장 큰 것입니다. 또한 투자자들은 브라질 오피스 빌딩, 쇼핑 센터, 로지스틱 파크에 주목하고 있으며 앞으로 수년간 시장 수요를 촉진할 것으로 예상됩니다.

남미에서는 저렴한 주택 제도 및 보조금이 주택 부문 건설 증가에 영향을 미칩니다.

2022년 남미 주택 부문은 전년 대비 3.35% 증가했습니다. 그러나 아르헨티나는 이 지표에서 9.16%의 현저한 침체를 보였습니다. 2023년에는 2022년보다 3.3% 증가한 것으로 평가되었습니다. 이 성장은 도시화의 진전, 1인당 소득 증가 및 전체적인 경기 확대 등의 요인에 의한 것으로, 이들 모두가 주택 수요를 부추기고 있습니다.

2020년 COVID-19 팬데믹을 배경으로 남미에서는 신규 바닥 면적 건설이 전년대비 11.83%로 대폭 증가했습니다. 이는 남미 정부의 의도적인 움직임으로 가계 소득의 급격한 감소를 바탕으로 경기후퇴를 완화하고 노동자를 지원하기 위해 건설 부문을 우선시했습니다. 그 결과 검역을 포함한 건설 활동의 한계가 완화되었습니다.

남미의 일부 국가에서는 증가하는 인구를 위해 주택을 더 합리적인 가격으로 만들기 위한 이니셔티브를 개발하고 있습니다. 예를 들어, 브라질은 2023년 2월 저소득자를 대상으로 전국 연방 주택 프로그램을 재개했습니다. 2023년 10월, 세계은행은 에콰도르에 대한 1억 달러의 대출 패키지를 승인했습니다. 볼리비아는 저가 주택공급을 확대하고 적정 가격을 유지하기 위한 노력을 계속하고 있으며, 주택 수요를 더욱 환기시키는 자세입니다. 그 결과, 남미의 주택 분야는 예측 기간 2023-2030년 중 4.09%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측되고 있습니다.

남미의 레디믹스 콘크리트 산업 개요

남미의 레디믹스 콘크리트 시장은 세분화되어 상위 5개사에서 21.90%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Argos Group, Polimix Concreto, Supermix, UNACEM and Votorantim Cimentos(알파벳순 정렬).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 용도 분야의 동향

상업

산업 및 시설

인프라

주택

주요 인프라 프로젝트(현재 및 발표됨)

규제 프레임워크

밸류체인 및 유통채널 분석

제5장 시장 세분화

최종 용도 분야별

상업

산업 및 시설

인프라

주택

제품별

센트럴 믹스

수축 믹스

트랜짓 믹스

국가별

아르헨티나

브라질

기타 남미

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Argos Group

CEMEX, SAB de CV

Holcim

LenoBetao

Melon SA

Polimix Concreto

Supermix

ULTRACEM SAS

UNACEM

Votorantim Cimentos

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계 밸류체인 분석

시장 역학(DROs)

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The South America Ready Mix Concrete Market size is estimated at 151.98 million Cubic meters in 2024, and is expected to reach 203.98 million Cubic meters by 2030, growing at a CAGR of 5.03% during the forecast period (2024-2030).

The commercial sector is the fastest-growing end-use sector in the region, while the residential sector is to remain at the pole position during the forecast period in South America

In 2022, South America witnessed a surge in ready-mix concrete consumption, with a notable uptick of 14.1 million tons compared to the previous year. This rebound was largely attributed to the region's recovery from the setbacks of the COVID-19 pandemic. Bolstered by a surge in construction activities across sectors, South America was poised to witness a 1.71% growth in ready-mix concrete consumption in 2023.

In 2022, the residential sector dominated South America's ready-mix concrete landscape, accounting for a significant 36.3% share. Within this sector, transit-mixed ready-mix concrete emerged as the preferred choice, capturing a substantial 75% of the sector's total consumption. Projections indicated that the residential sector's demand for ready-mix concrete will climb to nearly 144.8 million cubic meters in 2023, marking a 1.71% increase from 2022.

The infrastructure sector in South America is another key player in the ready-mix concrete arena. In 2022, it commanded a sizable 30% share of the region's demand. Notably, transit-mixed ready-mix concrete is anticipated to witness the highest compound annual growth rate (CAGR) of 4.86% in volume between 2023 and 2030.

South America's commercial sector is set to witness the most significant surge in ready-mix concrete consumption, with a projected CAGR of 5.78% during the forecast period. This uptick is primarily driven by the region's expanding commercial floor area. For instance, the commercial new floor area is expected to grow from 211 million square feet to 283 million square feet during the forecast period (2023-2030).

Brazil is the largest and fastest-growing market for ready-mix concrete in South America

In South America, the ready-mix concrete market is predominantly driven by the residential and infrastructure sectors. In 2022, these sectors held shares of 36% and 30%, respectively. In 2023, the region's ready-mix concrete consumption grew by approximately 1.71% compared to 2022, primarily fueled by increased demand from the residential sector.

Accounting for over half of South America's landmass and being the largest economy in the region, Brazil stands as the leading consumer of ready-mix concrete. In 2022, Brazil's residential sector accounted for a significant 63% of the country's total consumption. The commercial sector's new floor area is expected to witness the highest growth rate, and the consumption volume is projected to record a CAGR of 7.65% during the forecast period.

Argentina, the second-largest economy in South America, also holds a prominent position in terms of ready-mix concrete consumption in the region. In 2022, the residential sector in Argentina consumed 2.2 million cubic meters, marking a 4.44% decline from 2021. Argentina's market is dominated by the transit mixed type, which is the traditional form of ready-mix concrete.

Among the South American nations, Brazil is expected to witness the most significant surge in ready-mix concrete consumption, recording a CAGR of 6.02% during the forecast period. This growth is attributed to the rising adoption of shrink-mixed concrete, which offers advantages like reduced bulk volume and enhanced truck loading capacity. Brazil's consumption of shrink-mixed concrete is projected to record the fastest CAGR of 7.22% during the forecast period.

South America Ready Mix Concrete Market Trends

Growing foreign direct investments (FDIs) in the region to aid the market demand in the coming years

In 2022, the commercial sector in South America saw a significant decline of 16.2% in new floor area construction, largely driven by a 9.16% drop in Argentina. However, the sector was poised for a rebound in 2023, with a projected 4.75% increase in volume output. This growth can be attributed to economic growth and a surge in commercial construction, as various industries in the region attracted foreign direct investments (FDI) in 2022. In 2022, the Economic Commission for Latin America and the Caribbean (ECLAC) reported a robust 55.2% rise in FDI in the region.

The construction volume in the sector witnessed a notable growth of 15.9% in 2020 and a further 3.29% in 2021. This growth was a result of South American governments prioritizing the infrastructure and construction sectors. They eased restrictions, allowing construction, maintenance, and project development activities in private and public ventures. This move aimed to meet crucial milestones, deadlines, and economic recovery goals.

The commercial sector in South America is projected to witness robust growth in new floor area construction, registering a CAGR of 4% in volume during the forecast period (2023 to 2030). The region is witnessing a notable shift in its commercial construction landscape. Notable projects like the Paulinia Data Center and Porto Alegre Data Center I, initiated in 2023, are among the largest in the region. Additionally, investors are eyeing office buildings, shopping centers, and logistic parks in Brazil, which are expected to fuel market demand in the coming years.

Affordable housing schemes and subsidies in South America to influence higher construction in the residential sector

In 2022, the residential sector in South America witnessed a 3.35% surge in new floor area construction compared to the previous year. However, Argentina saw a notable decline of 9.16% in this metric. In 2023, the sector was projected to maintain its growth trajectory, with a construction volume expected to be 3.3% higher than in 2022. This growth can be attributed to factors like increasing urbanization, rising per capita income, and overall economic expansion, all of which are fueling the demand for housing.

Amidst the backdrop of the COVID-19 pandemic in 2020, South America saw a significant uptick of 11.83% in new floor area construction compared to the previous year. This was a deliberate move by the South American government, which prioritized the construction sector to mitigate the economic downturn and support workers, given the sharp decline in household incomes. Consequently, restrictions on construction activities, including quarantines, were eased.

Several South American nations are rolling out initiatives to make housing more affordable for their growing populations. For example, in February 2023, Brazil relaunched its nationwide federal housing program, targeting low-income individuals. In October 2023, the World Bank approved a USD 100 million financing package for Ecuador, specifically aimed at bolstering affordable and resilient housing. Bolivia's efforts to ramp up the supply of low-cost housing and maintain reasonable prices are poised to further stoke the demand for residential spaces. As a result, the residential sector in South America is projected to witness a CAGR volume of 4.09% during the forecast period (2023-2030).

South America Ready Mix Concrete Industry Overview

The South America Ready Mix Concrete Market is fragmented, with the top five companies occupying 21.90%. The major players in this market are Argos Group, Polimix Concreto, Supermix, UNACEM and Votorantim Cimentos (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End Use Sector Trends

4.1.1 Commercial

4.1.2 Industrial and Institutional

4.1.3 Infrastructure

4.1.4 Residential

4.2 Major Infrastructure Projects (current And Announced)

4.3 Regulatory Framework

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

5.1 End Use Sector

5.1.1 Commercial

5.1.2 Industrial and Institutional

5.1.3 Infrastructure

5.1.4 Residential

5.2 Product

5.2.1 Central Mixed

5.2.2 Shrink Mixed

5.2.3 Transit Mixed

5.3 Country

5.3.1 Argentina

5.3.2 Brazil

5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles

6.4.1 Argos Group

6.4.2 CEMEX, S.A.B. de C.V.

6.4.3 Holcim

6.4.4 LenoBetao

6.4.5 Melon S.A

6.4.6 Polimix Concreto

6.4.7 Supermix

6.4.8 ULTRACEM S.A.S

6.4.9 UNACEM

6.4.10 Votorantim Cimentos

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)