중동 및 아프리카의 건설용 화학제품 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Middle East and Africa Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1684080

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

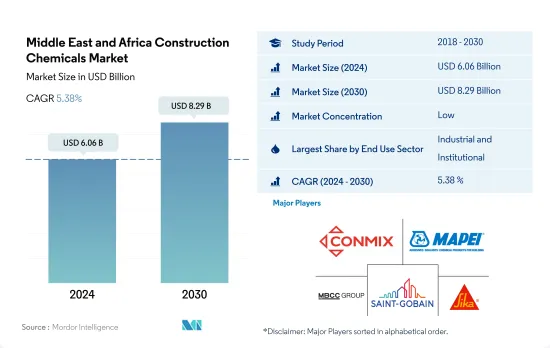

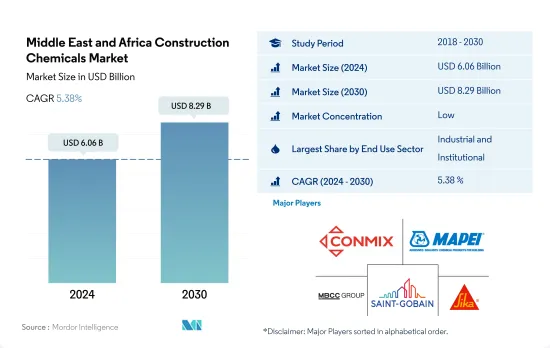

중동 및 아프리카의 건설용 화학제품 시장 규모는 2024년에 60억 6,000만 달러로 평가되었고, 2030년에는 82억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2030년) 중 CAGR 5.38%로 성장할 전망입니다.

상업 최종 사용자 부문이 성장률로 시장을 선도

2022년에는 사우디아라비아와 아랍에미리트(UAE) 인프라 부문이 건설용 화학제품 수요 급증을 가장 많이 참여했으며, 2019년부터 5%의 금액 증가를 차지했습니다. 주택 부문은 2023년 수요가 6% 증가한 것으로 평가되었으며 시장을 선도했습니다. 이처럼 주택 부문은 이 지역의 다른 모든 부문에 비해 가장 성장세를 기록했습니다.

사우디아라비아와 아랍에미리트(UAE)을 제외한 전체 지역에서는 산업 및 시설 부문이 건설용 화학제품의 주요 소비자입니다. 특히 바닥재용 수지, 콘크리트 혼화제, 표면처리용 화학약품이 이 분야를 지배하고 있으며, 2022년 동부문 수요의 16%를 차지했습니다.

주택 최종 사용자 부문은 이 지역에서 두 번째로 높은 건설용 화학제품의 소비자입니다. 게다가 사우디아라비아에서는 가장 많아 2022년 전체 최종 사용자 부문의 총 소비량의 42%를 차지했습니다. 2022년 콘크리트 혼화제, 표면처리 약품 및 접착제는 지역 전체와 사우디아라비아에서 이 최종 사용자 부문에 대한 수요의 대부분을 차지했습니다.

사우디아라비아와 아랍에미리트(UAE)은 이 지역 시장에 가장 큰 영향력을 갖고 있으며 건설용 화학제품 수요에서 가장 급성장하는 최종 사용자 부문은 상업용이기 때문에 지역 수준에서는 상업용 최종 사용자 부문 수요가 가장 급성장할 가능성이 높습니다. 이 수요는 추정 및 예측 기간 중 2023년부터 2030년까지 CAGR 5.83%를 기록할 것으로 예측되고 있습니다.

사우디아라비아의 주택 및 상업 부문이 이 지역 시장 성장에 가장 영향을 미칩니다.

이 지역의 건설용 화학제품 시장은 원유가격 상승과 견조한 경제 성장에 힘입어 2022년 현저한 고조를 보였습니다. 이 상승은 2021년에 비해 1억 5,000만 달러 시장 가치 상승으로 이어졌습니다. 2023년에는 시장이 2억 7,700만 달러를 더 확대해 주택과 상업 부문이 이 성장의 선두에 섰습니다.

사우디아라비아가 이 지역의 건설 부문에서 우위를 차지하고 있는 이유는 안정적인 정치적, 법적 틀이 비즈니스 환경을 요구하는 많은 건설 회사를 유치하고 있기 때문이라고 생각됩니다. 사우디아라비아의 풍부한 숙련 노동력은 주요 산유국으로서의 지위와 함께 이미 견조한 경제를 더욱 강화하고 건설 활동에 박차를 가하고 있습니다. 그 결과 사우디아라비아는 이 지역의 건설용 화학제품 수요를 견인하는 주요 국가로 부상했습니다.

아랍에미리트(UAE)는 건설 부문의 선두 주자로 사우디아라비아에 근소한 차이로 이어집니다. 아랍에미리트(UAE)의 매력은 외국 직접 투자(FDI)의 안정적인 유입에 의해 강화되고 있으며, 2021년에는 지역 내 대내 직접 투자로 선두 자리를 확보했습니다.

중동 및 아프리카에서 사우디아라비아는 건설용 화학제품 시장에 큰 영향력을 가지고 있습니다. 주요 최종 사용자인 주택 및 상업 분야로부터 수요 급증이 예상됨에 따라 사우디아라비아는 예측 기간 2023년부터 2030년까지 CAGR 6.18%로 성장이 전망되며, 이 지역에서 가장 빠른 시장 성장이 예상됩니다.

중동 및 아프리카의 건설용 화학제품 시장 동향

사우디아라비아에 의한 현대적인 오피스 빌딩 건설 프로젝트에 대한 고액 투자가 중동 상업 건축물의 신규 바닥 면적을 밀어 올릴 전망

2022년 중동 및 아프리카 상업 시설의 신규 바닥 면적은 3.56% 감소했지만, 이는 주로 철강 가격 상승 및 유통 후 운송 비용의 5배 증가로 인한 것입니다. 아랍에미리트(UAE)는 신규 바닥 면적의 42.20% 감소라는 상당한 하락으로 그 모순이 아랍에미리트(UAE)으로 향했습니다. 중동 및 아프리카 상업 시설의 신규 바닥 면적은 2023년 2022년 대비 2.83% 증가한 것으로 평가됐습니다.

COVID-19의 유행은 2020년 경기 감속으로 이어졌고, 그 결과 많은 건설 프로젝트가 중단되거나 연기되었습니다. 그 결과 2020년 신규 바닥 면적은 2019년에 비해 5.32% 감소했습니다. 2021년에 규제가 해제되고 건설 활동이 재개되면서 신규 바닥 면적은 2020년 대비 2.68% 증가했으며 사우디아라비아는 2.40%로 가장 높은 성장률을 보였습니다.

중동 및 아프리카 상업 시설의 신규 바닥 면적은 예측 기간 동안 CAGR 3.95%를 나타낼 것으로 예상되며, 그 중에서도 사우디아라비아는 가장 빠른 CAGR 4.34%를 나타낼 것으로 예상됩니다. 이것은 입주자가 오래된 오피스 빌딩에서 현대적이고 정비된 오피스 공간과 물류 공원으로 이동하는 동향을 받았습니다. 또한 두바이의 TECOM'S Innovation Hub Phase 2와 같이 35만 5,000평방피트에 달하는 여러 오피스 빌딩 프로젝트가 UAE의 A급 오피스 공간 수요 증가에 대응하기 위해 개발되었습니다. 또한 사우디아라비아는 Jabal Omar, Amaala, Al Widyaa 등의 프로젝트에 100억 달러 이상을 투자하여 지역 상업 건설을 강화할 예정입니다.

중동 및 아프리카에서는 고예산 주택 프로젝트에 대한 투자가 증가하여 주택 건설의 신규 바닥 면적을 밀어 올릴 것으로 전망됩니다.

2022년 중동 및 아프리카의 주택 건설 부문은 도시화의 진전 및 저렴한 주택에 대한 인구 수요의 급증으로 견인되어 신규 바닥 면적이 2.25% 증가했습니다. 이 성장은 더욱 가속화되고 2023년에는 사우디아라비아가 주도하여 3.89% 증가할 것으로 전망됩니다. 비전 2030의 일환으로 사우디아라비아의 지자체, 농촌 문제, 주택부는 2025년까지 4만 호의 저렴한 주택을 사우디아라비아 국민에게 제공하고, 2030년까지 주택 소유율을 70%로 끌어올리는 이니셔티브를 전개했습니다.

COVID-19의 유행은 이 지역 주택 건설에 현저한 영향을 미쳤습니다. 2020년에는 봉쇄 조치, 노동력 부족, 공급망 혼란, 개인 소비 감소로 인해 신규 바닥 면적은 2019년 대비 7.46% 감소했습니다. 그러나 폐쇄 조치가 완화되어 건설활동이 재개되었기 때문에 2021년에는 회복해 신규 바닥 면적은 전년대비 2.43% 증가했습니다.

중동 및 아프리카의 주택 건설 부문은 꾸준한 성장을 이루고 있으며 예측 기간 동안 CAGR은 3.05%를 나타낼 것으로 예상됩니다. 아랍에미리트(UAE)의 CAGR은 4.91%로 가장 빠를 것으로 예상됩니다. 예상 가격 56억 달러의 사우디아라비아 메가시티 NEOM과 8,000명 이상의 주민에게 주택을 제공하도록 설계된 UAE의 Al Quoz Creative Zone과 같은 주목할 만한 프로젝트가 이 지역의 주택 건설에 박차를 가할 것으로 예상됩니다. 2030년까지 신규 바닥 면적은 46억 4,000만 평방피트에 이를 것으로 예상되며, 2022년 36억 평방 피트에서 크게 증가할 전망입니다.

중동 및 아프리카의 건설용 화학제품 산업의 개요

중동 및 아프리카의 건설용 화학제품 시장은 세분화되어 상위 5개사에서 25.40%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Conmix, MAPEI SpA, MBCC Group, Saint-Gobain 및 Sika AG.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 용도 분야의 동향

상업

산업 및 시설

인프라

주택

주요 인프라 프로젝트(현재 및 발표됨)

규제 프레임워크

밸류체인 및 유통채널 분석

제5장 시장 세분화

최종 용도 분야별

상업

산업 및 시설

인프라

주택

제품별

접착제

서브 제품별

핫멜트

반응성

용제계

수계

앵커 및 그라우트

서브 제품별

시멘트계 고정재

수지 고정

기타 유형

콘크리트 혼화제

서브 제품별

촉진제

공기혼입 혼화제

고범위 감수제(초가소제)

지연제

수축 저감 혼화제

점도 조정제

감수제(가소제)

기타 유형

콘크리트 보호 페인트

서브 제품별

아크릴계

알키드

에폭시

폴리우레탄

기타 수지

바닥용 수지

서브 제품별

아크릴

에폭시

폴리아스파라긴

폴리우레탄

기타 수지 유형

보수 및 재생 화학제품

서브 제품별

섬유 포장 시스템

주입 그라우트재

마이크로 콘크리트 모르타르

개질 모르타르

철근 보호재

실링재

서브 제품별

아크릴

에폭시

폴리우레탄

실리콘

기타 수지

표면 처리 약품

서브 제품별

경화 컴파운드

이형제

기타 제품 유형

방수 솔루션

서브 제품별

화학제품

멤브레인

국가별

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Ahlia Chemicals Company

Arkema

CIKO Middle East

CMB

CMCI(Construction Material Chemical Industries)

Conmix

EAMIC

Fosroc, Inc.

Hemts Construction Chemicals

MAPEI SpA

MBCC Group

NCC X-CALIBUR

Saint-Gobain

Sika AG

SOCHEM

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계 밸류체인 분석

시장 역학(DROs)

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The Middle East and Africa Construction Chemicals Market size is estimated at 6.06 billion USD in 2024, and is expected to reach 8.29 billion USD by 2030, growing at a CAGR of 5.38% during the forecast period (2024-2030).

Commercial end-user sector to lead the market in terms of growth

In 2022, the infrastructure sectors of Saudi Arabia and the United Arab Emirates witnessed the highest surge in demand for construction chemicals, accounting for a 5% increase in value from 2019. The residential sector was projected to lead the market, with an estimated 6% increase in demand in 2023. Thus, the residential sector recorded the most growth compared to all other sectors in the region.

Across the region, except Saudi Arabia and the United Arab Emirates, the industrial and institutional sector is the primary consumer of construction chemicals. Notably, flooring resins, concrete admixtures, and surface treatment chemicals dominate this segment, collectively accounting for 16% of the sector's demand in 2022.

The residential end-user sector is the region's second-highest consumer of construction chemicals. Additionally, it is the highest in Saudi Arabia, with a share of 42% of the total consumption by all the end-user sectors in 2022. Concrete admixtures, surface treatment chemicals, and adhesives in 2022 made up most of the demand of this end-user sector in the region overall and in Saudi Arabia.

Since Saudi Arabia and the United Arab Emirates have the most influence over the market in the region, and as their fastest-growing end-user sector in terms of demand for construction chemicals is the commercial, the demand consequently will likely grow the fastest in the commercial end-user sector at a regional level. The demand is estimated to record a CAGR of 5.83% during the forecast period (2023-2030).

Saudi Arabia's residential and commercial sectors to have the most impact on the market's growth in the region

The construction chemicals market in the region witnessed a notable upswing in 2022, buoyed by rising oil prices and robust economic growth. This surge translated into a USD 150 million uptick in market value compared to 2021. The market further expanded by USD 277 million in 2023, with the residential and commercial sectors spearheading this growth.

Saudi Arabia's dominance in the regional construction sector can be attributed to its stable political and legal framework, which attracts numerous construction firms seeking a conducive business environment. The country's abundant skilled labor pool, coupled with its status as a major oil producer, bolsters its already robust economy, further fueling construction activities. Consequently, Saudi Arabia emerges as the primary driver of demand for construction chemicals in the region.

The United Arab Emirates (UAE) follows closely behind Saudi Arabia in terms of construction sector leadership. The UAE's attractiveness is bolstered by its consistent inflow of foreign direct investment (FDI), with 2021 seeing it secure the top spot in the region for inbound FDI.

Within the Middle East & Africa, Saudi Arabia wields significant influence over the construction chemicals market. Given the anticipated surge in demand from its key end-user sectors, residential and commercial, Saudi Arabia is poised to witness the region's fastest market growth, with a projected CAGR of 6.18% during the forecast period (2023-2030).

Middle East and Africa Construction Chemicals Market Trends

High investments in modern office building projects by Saudi Arabia are expected to propel the new floor area for commercial construction in the Middle East

In 2022, the Middle East & Africa witnessed a 3.56% decline in the new floor area for commercial construction, primarily due to surging steel prices and a fivefold increase in shipping costs post-pandemic. The United Arab Emirates bore the brunt, with a significant 42.20% drop in new floor area. The new floor area for commercial construction in the Middle East & Africa was expected to grow by 2.83% in 2023 compared to 2022.

The COVID-19 pandemic led to an economic slowdown in 2020, resulting in the cancellation or postponement of numerous construction projects. Consequently, the new floor area saw a 5.32% dip in 2020 compared to 2019. As the restrictions were lifted in 2021 and construction activities resumed, the new floor area grew by 2.68% compared to 2020, with Saudi Arabia having the highest growth of 2.40%.

The new floor area for commercial construction in the Middle East & Africa is expected to record a CAGR of 3.95% during the forecast period, with Saudi Arabia expected to record the fastest CAGR of 4.34%, following a trend of occupiers migrating from old office buildings to modern, well-maintained office spaces, and logistic parks. Furthermore, several office building projects like TECOM'S Innovation Hub Phase 2 in Dubai, spread across 355,000 square feet, are being developed to meet the growing demand for Grade A office spaces in the UAE. Additionally, Saudi Arabia will invest more than USD 10 billion in projects like Jabal Omar, Amaala, and Al Widyaa, among others, to bolster regional commercial construction.

Increasing investments in high-budget housing projects in the Middle East & Africa will likely drive the new floor area for residential construction

In 2022, the residential construction sector in the Middle East & Africa witnessed a 2.25% growth in new floor area, driven by increased urbanization and a surging population's demand for affordable housing. This growth was projected to accelerate, with an expected increase of 3.89% in 2023, led by Saudi Arabia. As part of its Vision 2030, the Ministry of Municipal and Rural Affairs and Housing in Saudi Arabia rolled out initiatives to deliver 40,000 affordable housing units to Saudi nationals by 2025 and raise the homeownership rate to 70% by 2030.

The COVID-19 pandemic had a notable impact on residential construction in the region. In 2020, as a result of lockdowns, labor shortages, disrupted supply chains, and reduced consumer spending, the new floor area saw a decline of 7.46% compared to 2019. However, as lockdown measures eased and construction activities resumed, the region rebounded in 2021, witnessing a 2.43% growth in new floor area compared to the previous year.

The residential construction sector in the Middle East & Africa is poised for steady growth, and it is expected to record a CAGR of 3.05% during the forecast period. The United Arab Emirates is expected to register the fastest CAGR of 4.91%. Noteworthy projects, such as Saudi Arabia's NEOM, a mega-city with an estimated value of USD 5.60 billion, and the Al Quoz Creative Zone in the UAE, designed to provide housing for more than 8,000 residents, are expected to fuel the region's residential construction. By 2030, the new floor area is anticipated to reach 4.64 billion square feet, a significant increase from 3.6 billion square feet in 2022.

Middle East and Africa Construction Chemicals Industry Overview

The Middle East and Africa Construction Chemicals Market is fragmented, with the top five companies occupying 25.40%. The major players in this market are Conmix, MAPEI S.p.A., MBCC Group, Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End Use Sector Trends

4.1.1 Commercial

4.1.2 Industrial and Institutional

4.1.3 Infrastructure

4.1.4 Residential

4.2 Major Infrastructure Projects (current And Announced)

4.3 Regulatory Framework

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

5.1 End Use Sector

5.1.1 Commercial

5.1.2 Industrial and Institutional

5.1.3 Infrastructure

5.1.4 Residential

5.2 Product

5.2.1 Adhesives

5.2.1.1 By Sub Product

5.2.1.1.1 Hot Melt

5.2.1.1.2 Reactive

5.2.1.1.3 Solvent-borne

5.2.1.1.4 Water-borne

5.2.2 Anchors and Grouts

5.2.2.1 By Sub Product

5.2.2.1.1 Cementitious Fixing

5.2.2.1.2 Resin Fixing

5.2.2.1.3 Other Types

5.2.3 Concrete Admixtures

5.2.3.1 By Sub Product

5.2.3.1.1 Accelerator

5.2.3.1.2 Air Entraining Admixture

5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

5.2.3.1.4 Retarder

5.2.3.1.5 Shrinkage Reducing Admixture

5.2.3.1.6 Viscosity Modifier

5.2.3.1.7 Water Reducer (Plasticizer)

5.2.3.1.8 Other Types

5.2.4 Concrete Protective Coatings

5.2.4.1 By Sub Product

5.2.4.1.1 Acrylic

5.2.4.1.2 Alkyd

5.2.4.1.3 Epoxy

5.2.4.1.4 Polyurethane

5.2.4.1.5 Other Resin Types

5.2.5 Flooring Resins

5.2.5.1 By Sub Product

5.2.5.1.1 Acrylic

5.2.5.1.2 Epoxy

5.2.5.1.3 Polyaspartic

5.2.5.1.4 Polyurethane

5.2.5.1.5 Other Resin Types

5.2.6 Repair and Rehabilitation Chemicals

5.2.6.1 By Sub Product

5.2.6.1.1 Fiber Wrapping Systems

5.2.6.1.2 Injection Grouting Materials

5.2.6.1.3 Micro-concrete Mortars

5.2.6.1.4 Modified Mortars

5.2.6.1.5 Rebar Protectors

5.2.7 Sealants

5.2.7.1 By Sub Product

5.2.7.1.1 Acrylic

5.2.7.1.2 Epoxy

5.2.7.1.3 Polyurethane

5.2.7.1.4 Silicone

5.2.7.1.5 Other Resin Types

5.2.8 Surface Treatment Chemicals

5.2.8.1 By Sub Product

5.2.8.1.1 Curing Compounds

5.2.8.1.2 Mold Release Agents

5.2.8.1.3 Other Product Types

5.2.9 Waterproofing Solutions

5.2.9.1 By Sub Product

5.2.9.1.1 Chemicals

5.2.9.1.2 Membranes

5.3 Country

5.3.1 Saudi Arabia

5.3.2 United Arab Emirates

5.3.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles

6.4.1 Ahlia Chemicals Company

6.4.2 Arkema

6.4.3 CIKO Middle East

6.4.4 CMB

6.4.5 CMCI (Construction Material Chemical Industries)

6.4.6 Conmix

6.4.7 EAMIC

6.4.8 Fosroc, Inc.

6.4.9 Hemts Construction Chemicals

6.4.10 MAPEI S.p.A.

6.4.11 MBCC Group

6.4.12 NCC X-CALIBUR

6.4.13 Saint-Gobain

6.4.14 Sika AG

6.4.15 SOCHEM

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)