ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

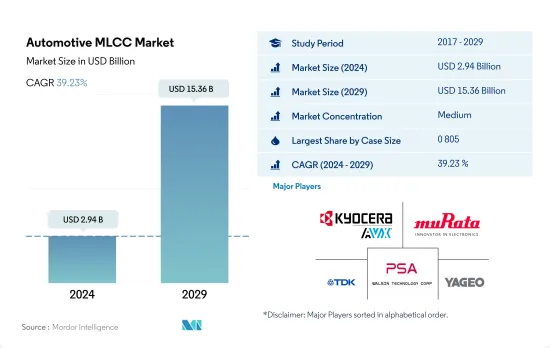

자동차용 MLCC 시장 규모는 2024년에 29억 4,000만 달러로 평가되었고, 2029년에는 153억 6,000만 달러에 이를 전망이며, 예측 기간인 2024-2029년 CAGR은 39.23%를 나타낼 것으로 예측됩니다.

자동차 진화에서 MLCC의 다면적 역할 해명이 MLCC 수요를 견인

진화를 계속하는 자동차 산업의 상황에서 MLCC의 역할은 단순한 전자 부품의 영역을 넘어서고 있습니다. 이러한 소형 파워 하우스는 배전 및 노이즈 억제에서 신호 컨디셔닝 및 전압 레귤레이션에 이르기까지 다양한 기능의 교향곡을 연주하는 현대 자동차 시스템의 핵심입니다.

0 603 MLCC는 컴팩트하면서도 필수적인 존재입니다. 이러한 커패시터는 작고 에너지 효율적인 설계로 이동하는 데 매우 중요한 역할을 합니다. 자동차 기술의 발전에 따라 합리화된 솔루션에 대한 수요가 0 603 부문의 존재감을 높이고 있습니다.

0 805 커패시터는 특히 전기자동차(EV)가 주류가 됨에 따라 시장에서 중요한 위치를 차지합니다. EV의 급속한 보급은 효과적인 배전과 제어의 필요성을 강조하고 0 805 부문의 중요성을 강조합니다. EV가 자동차 전망을 재정의하는 동안 이러한 커패시터는 성능과 효율성의 실현자 역할을 합니다.

1 206 커패시터는 크기와 다양성의 균형을 맞추며 다양한 자동차 용도에 적합한 옵션입니다. 자동차 산업이 기술의 진보를 수락함에 따라 1 210 부문의 중요성이 드러납니다.

기타 부문은 특수 자동차 요구 사항에 해당하는 다양한 커패시턴스 값을 포함합니다. 신기술부터 독특한 용도에 이르기까지 이러한 다양한 부문은 자동차의 명확한 요구를 충족시키는 MLCC의 적응성을 보여줍니다.

아시아태평양, 유럽, 북미에서 MLCC의 영향력 밝힙니다.

아시아태평양, 유럽, 북미는 자동차 산업에 있어서 변화의 원동력이 되고 있습니다. 기술 발전, 지속가능성, 스마트 모빌리티 솔루션의 추구는 자동차 진화를 지원하는 라미네이트 세라믹 커패시터(MLCC)의 중요한 역할을 돋보이게 합니다. 각 지역이 혁신과 효율성의 미래를 향해 추진하는 가운데 고품질 MLCC에 대한 수요는 계속 확대되고 있으며, 자동차의 밸류체인에서 MLCC의 중요성이 확고해지고 있습니다.

아시아태평양은 급속한 기술 발전과 소비자 수요 증가를 특징으로 하는 자동차 기술 혁신의 진원지입니다. 중국, 일본, 한국 등 주요 자동차 거점이 있는 이 지역은 전기자동차(EV) 도입, 커넥티드카, 자율주행에서 최첨단을 달리고 있습니다.

유럽 자동차 산업은 기술 혁신, 지속가능성, 엄격한 환경 규제의 대명사입니다. 이 지역은 이산화탄소 배출량을 줄이고 보다 깨끗한 이동성 솔루션으로 전환하기 위해 노력하고 있으며 자동차 전망을 재구성하고 있습니다. 전기자동차와 하이브리드 자동차의 보급에 따라 전원 관리, 노이즈 억제, 전압 조정용 MLCC 수요가 높아지고 있습니다.

북미의 자동차 부문은 스마트 이동성 솔루션과 첨단 기술의 추구를 특징으로 합니다. 북미의 소비자가 보다 충실한 운전 체험 및 최첨단 기능을 요구하는 가운데, EV, 인포테인먼트 시스템, ADAS 등의 용도에 있어서 MLCC 수요는 증가 경향에 있습니다. 이 지역의 역동적 인 자동차 상황은 MLCC 시장 확대의 주요 촉진요인이 되었습니다.

세계의 자동차용 MLCC 시장 동향

수소 스테이션의 인프라 정비가 판매 확대를 계속

연료 전지 전기자동차(FCEV)는 연료로 저장한 수소에너지를 연료 전지를 통해 전기로 변환하여 전기차와 유사한 추진 메커니즘을 가지고 있습니다. 기존의 내연기관을 동력원으로 하는 자동차에 비해 FCEV는 유해한 배기 가스를 배출하지 않습니다.

연료 전지 전기자동차의 출하대수는 2022년에는 4만 3,000대였으며, 2029년에는 7만 1,000대에 이를 것으로 예상됩니다. 풍력과 햇빛과 같은 신재생 에너지가 수소 제조 공정에 점점 기여하게 되면 에너지 효율적인 FCEV 수요가 크게 증가합니다.

저배출 가스차에 대한 수요가 높아짐에 따라, 보다 엄격한 이산화탄소 배출 규제가 실시되어, 신속한 연료 보급과 같은 이점으로부터 FCEV의 채용이 보다 중시되고 있습니다. FCEV 개발을 촉진하기 위해 여러 정부 기관과 상업 단체가 협력하여 연료전지 기술의 진보와 수소 보급 인프라 개발에 투자하고 있습니다. IEA에 따르면 2021년 말에는 세계에서 약 730개 소의 수소 스테이션(HRS)이 있으며, 약 51,600대의 FCEV에 연료를 공급하고 있습니다. 이는 2020년부터 FCEV의 세계 스톡이 거의 50% 증가하고 HRS 수가 35% 증가함을 의미합니다. 이러한 요인은 FCEV의 향후 고성장에 기여합니다.

엄격한 정부 규제가 전기자동차의 보급 촉진

MLCC는 고온 내성과 쉬운 표면 실장 폼 팩터를 제공하여 EV 전자 및 서브 시스템에 가장 적합한 부품으로 등장했습니다. 전기자동차에는 약 8,000-1만 개의 MLCC가 사용되고 있습니다. 전기자동차 MLCC는 배터리 관리 시스템(BMS), 자동차 충전기(OBC), DC/DC 컨버터에서 일반적으로 사용됩니다. 이러한 EV 서브시스템에 요구되는 일반 사양을 충족하고 EV 내의 가혹한 환경에서도 확실하게 기능할 수 있는 능력 외에도 부품 제조업체는 IATF16949 인증을 받아 AEC-Q200을 준수해야 합니다.

전기차 출하량은 2022년 1640만 대를 차지하였고, 2029년 2552만 대까지 증가할 것으로 예상됩니다. 온실가스 배출을 줄이고 기후 변화와 싸우기 위해 여러 국가가 엄격한 환경규제를 실시했습니다. 그 결과, 자동차 제조업체는 더 많은 전기자동차를 생산하고 화석 연료에 대한 의존도를 줄이기 위해 점점 더 강하게 요구되고 있습니다. 소비자의 환경 의식도 높아져, 종래의 가솔린차를 대신하는 지속 가능한 자동차를 요구하게 되어 있습니다.

COVID-19 팬데믹과 러시아 우크라이나 전쟁은 세계 공급망을 혼란시켰고 자동차 산업은 큰 영향을 받았습니다. 그러나 장기적으로 보면 EV 시장은 세계 일부 지역에서 매출을 늘리고 있습니다. 이는 공개적으로 이용 가능한 충전 인프라의 배치를 지원하는 정부와 기업의 노력이 EV 매출을 더욱 늘릴 수 있는 견고한 기반이 되기 때문입니다. 세계에서 공개적으로 이용 가능한 충전기는 180만 기에 가까워졌고, 2021년에는 약 50만 기가 설치되었으며, 그 중 3분의 1이 급속 충전기이며, 2017년에 설치된 공영 충전기의 총수를 웃돌았습니다.

자동차용 MLCC 산업 개요

자동차용 MLCC 시장은 적당히 통합되어 상위 5개사에서 60.58%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, TDK Corporation, Walsin Technology Corporation 및 Yageo Corporation(알파벳순 정렬).

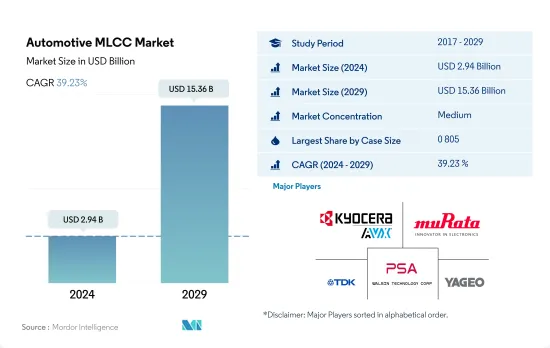

The Automotive MLCC Market size is estimated at 2.94 billion USD in 2024, and is expected to reach 15.36 billion USD by 2029, growing at a CAGR of 39.23% during the forecast period (2024-2029).

Unveiling the multifaceted role of MLCCs in the automotive evolution is driving MLCC demand

In the ever-evolving landscape of the automotive industry, the role of MLCCs has moved beyond mere electronic components. These miniature powerhouses are the cornerstone of modern vehicular systems, orchestrating a symphony of functions ranging from power distribution and noise suppression to signal conditioning and voltage regulation.

The 0 603 MLCCs are compact yet indispensable contributors. These capacitors play a pivotal role in shifting toward compact and energy-efficient designs. With advancements in automotive technologies, the demand for streamlined solutions has elevated the prominence of the 0 603 segment.

The 0 805 capacitors occupy a significant position in the market, particularly as electric vehicles (EVs) become mainstream. The surge in EV adoption emphasizes the need for effective power distribution and control, underscoring the relevance of the 0 805 segment. As EVs redefine the automotive landscape, these capacitors act as enablers of performance and efficiency.

The 1 206 capacitors represent a balance between size and versatility, making them a preferred choice for diverse automotive applications. As the automotive industry embraces technological advancements, the importance of the 1 210 segment becomes evident.

The 'others' segment encompasses an array of capacitance values that cater to specialized automotive requirements. From emerging technologies to unique applications, this diverse segment exemplifies the adaptable nature of MLCCs in meeting distinct automotive needs.

Unveiling the impact of MLCCs in Asia-Pacific, Europe, and North America

Asia-Pacific, Europe, and North America are driving transformative changes in the automotive industry. Their pursuit of technological advancements, sustainability, and smart mobility solutions underscores the crucial role of multi-layer ceramic capacitors (MLCCs) in supporting the evolution of vehicles. As each region propels toward a future of innovation and efficiency, the demand for high-quality MLCCs continues to grow, cementing their significance in the automotive value chain.

Asia-Pacific stands as an epicenter of automotive innovation characterized by rapid technological advancements and growing consumer demand. With major automotive hubs like China, Japan, and South Korea, this region is at the forefront of electric vehicle (EV) adoption, connected cars, and autonomous driving.

Europe's automotive industry is synonymous with innovation, sustainability, and stringent environmental regulations. The region's commitment to reducing carbon emissions and transitioning toward cleaner mobility solutions is reshaping the automotive landscape. As electric and hybrid vehicles gain traction, the demand for MLCCs for power management, noise suppression, and voltage regulation is escalating.

North America's automotive sector is characterized by its pursuit of smart mobility solutions and advanced technologies. As North American consumers seek enhanced driving experiences and cutting-edge features, the demand for MLCCs in applications like EVs, infotainment systems, and ADAS is on the rise. The region's dynamic automotive landscape positions it as a key driver of the MLCC market's expansion.

Global Automotive MLCC Market Trends

Infrastructure improvement for hydrogen stations continues to increase sales

Fuel cell electric vehicles (FCEVs) use hydrogen energy stored as fuel, which is then converted into electricity by the fuel cell and has a propulsion mechanism similar to that of an electric vehicle. Compared to vehicles powered by conventional internal combustion engines, FCEVs do not emit any harmful exhaust emissions.

Fuel cell electric vehicle shipments accounted for 0.043 million units in 2022, and these are expected to reach 0.071 million units in 2029. As renewable energies like wind and solar contribute increasingly to the hydrogen manufacturing process, there will be a huge increase in the demand for energy-efficient FCEVs.

As the demand for low-emission vehicles rises, stricter carbon emission standards are being implemented, and more emphasis is being placed on the adoption of FCEVs due to benefits like quick refueling. To encourage the development of FCEVs, several government and commercial organizations are collaborating and investing in advancing fuel cell technology and the development of hydrogen refueling infrastructure. According to the IEA, at the end of 2021, there were about 730 hydrogen refueling stations (HRSs) globally providing fuel for about 51,600 FCEVs. This represents an increase of almost 50% in the global stock of FCEVs and a 35% increase in the number of HRSs from 2020. These factors contribute to the high growth of FCEVs in the future.

Stringent government regulations are increasing the penetration of electric vehicles

MLCCs have emerged as a perfect component for EV electronics and subsystems, offering high-temperature resistance and an easy surface-mount form factor. Approximately 8,000-10,000 MLCCs are used in an electric vehicle. MLCCs in electric vehicles are commonly used in battery management systems (BMS), onboard chargers (OBC), and DC/DC converters. In addition to meeting the general specifications required for these EV subsystems and having the ability to function reliably in harsh environments inside an EV, component manufacturers should also be IATF 16949-certified and compliant with AEC-Q200.

Electric vehicle shipments accounted for 16.4 million units in 2022, and it is expected to rise to 25.52 million units in 2029. Several countries have implemented strict environmental regulations to reduce greenhouse gas emissions and combat climate change. As a result, automakers are under increasing pressure to produce more electric vehicles and reduce their reliance on fossil fuels. Consumers are becoming more environmentally conscious and are looking for more sustainable alternatives to traditional gasoline-powered vehicles.

The COVID-19 pandemic and Russia's war in Ukraine disrupted global supply chains, and the automotive industry has been heavily impacted. However, in the longer term, the EV market is witnessing sales growth in some regions of the world as government and corporate efforts to support the deployment of publicly available charging infrastructure are providing a solid basis for further increase in EV sales. Publicly accessible chargers worldwide approached 1.8 million, with nearly 500,000 chargers installed in 2021, of which a third were fast chargers, which accounted for more than the total number of public chargers installed in 2017.

Automotive MLCC Industry Overview

The Automotive MLCC Market is moderately consolidated, with the top five companies occupying 60.58%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, TDK Corporation, Walsin Technology Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Automotive Sales

4.1.1 Global BEV (Battery Electric Vehicle) Production

4.1.2 Global Electric Vehicles Sales

4.1.3 Global FCEV (Fuel Cell Electric Vehicle) Production

4.1.4 Global HEV (Hybrid Electric Vehicle) Production

4.1.5 Global Heavy Commercial Vehicles Sales

4.1.6 Global ICEV (Internal Combustion Engine Vehicle) Production

4.1.7 Global Light Commercial Vehicles Sales

4.1.8 Global Non-Electric Vehicle Sales

4.1.9 Global PHEV (Plug-in Hybrid Electric Vehicle) Production

4.1.10 Global Passenger Vehicles Sales

4.1.11 Global Two-Wheeler Sales

4.2 Regulatory Framework

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)