전기자동차용 MLCC 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Electric Vehicles MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1684039

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

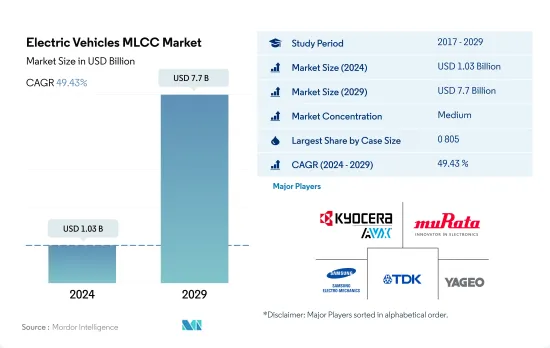

전기자동차용 MLCC 시장 규모는 2024년에 10억 3,000만 달러로 평가되었고, 2029년에는 77억 달러에 이를 것으로 예측되며, 예측 기간인 2024-2029년 CAGR 49.43%로 성장할 전망입니다.

MLCC를 통한 자동차 시스템 혁신을 통해 효율화를 추진하는 것은 다양한 사례 크기에 대한 수요를 더욱 강화하고 있습니다.

자동차 부문의 역동적인 진화 속에서 MLCC는 단순한 전자 부품으로서의 전통적인 역할을 초월했습니다. 이 컴팩트한 파워 하우스는 이제 배전, 노이즈 억제, 신호 컨디셔닝, 전압 레귤레이션 등 다양한 기능을 조화시키면서 현대 자동차 시스템의 요점으로 기능하고 있습니다.

이러한 상황에서 0 603 부문은 컴팩트하면서도 필수적인 존재로 부상하고 있습니다. 이 커패시터는 컴팩트하고 에너지 효율적인 설계가 특징입니다. 자동차 기술이 계속 발전하고 있는 가운데 합리화된 솔루션에 대한 수요는 0 603 부문의 중요성을 새로운 높이로 끌어올리고 있습니다.

0.805 커패시터는 특히 전기자동차(EV)가 주역이 되는 가운데 주목할 만한 지위를 차지하고 있습니다. EV의 급속한 보급은 효율적인 배전과 제어의 필요성을 두드러지게 하고, 0 805 부문의 매우 중요한 역할을 강조합니다. EV에 의해 재정의된 시대에 이러한 커패시터는 성능과 효율을 향상시키는 촉매로 등장합니다.

1 206 부문은 크기와 다양성 사이에 미묘한 균형을 맞추며 다양한 자동차 용도에 선호되는 옵션입니다. 자동차 산업이 급속한 기술적 진보를 이루면서 최첨단 진보와 원활하게 통합되는 1 210 부문의 필수성이 점점 밝혀지고 있습니다.

기타 범주에는 특수 자동차 요구 사항을 충족하도록 정밀하게 조정된 다양한 커패시턴스 값이 포함됩니다. 신기술부터 독특한 용도에 이 역동적인 부문은 자동차 영역의 독특하고 진화하는 요구에 부응하는 MLCC의 탁월한 적응성을 보여줍니다.

전기자동차 시장에서 적층 세라믹 커패시터(MLCC)의 성장을 가속하는 주요 촉매

시장 역학을 보면 금액 기준으로 아시아태평양이 44.97%의 압도적인 시장 점유율을 차지하고, 북미와 유럽은 각각 23.57%와 22.80%의 점유율을 유지하고 있습니다.

아시아태평양은 전기자동차(EV) 혁명의 최전선에 있으며 정부 지원, 기술 진보, 소비자 수요 증가로 상당한 성장을 보이고 있습니다. 중국과 같은 주요 기업이 지배하는 이 지역은 EV의 생산과 기술 혁신으로 선도하고 있으며, 세계 EV 시장에서 역동적인 세력으로서의 지위를 확고히 하고 있습니다.

지속가능성에 대한 헌신으로 유명한 유럽은 배출감소와 환경문제에 대한 해결책으로서 EV의 도입을 선구적으로 추진하고 있습니다. 엄격한 배기가스 규제 및 인센티브 프로그램이 유럽 각국에서 EV의 급속한 보급을 뒷받침하고 있습니다. 선도적인 자동차 제조업체는 보다 환경 친화적인 미래를 보장하기 위해 EV 생산, 충전 인프라 및 배터리 기술에 많은 투자를 하고 있습니다.

북미에서는 기존 기업 및 신흥 기업의 다양한 상황이 EV 시장을 형성하고 있습니다. 정부의 인센티브, 환경 의식 증가, 기술의 진보가 전동 이동성으로의 전환을 뒷받침하고 있습니다. 테슬라의 영향력은 여전히 크고, 이 지역 내에서의 혁신과 경쟁을 촉진하고 전기자동차 시장 성장을 가속하고 있습니다.

세계 기타 지역(RoW)은 독자적인 특징을 가지고 전동화를 받아들이고 있습니다. 전동 이륜차는 기세를 늘리고 도시의 혼잡에 대처하고 경제적 이익을 가져오고 있습니다. 세계 자동차 산업이 전기화를 향한 길을 걷고 있는 가운데 이러한 지역은 일체가 되어 전기차 MLCC 시장의 미래 형성에 공헌하고 있습니다.

세계의 전기자동차용 MLCC 시장 동향

공공 충전 인프라 배치를 지원하는 정부 정책은 배터리 전기자동차 판매 촉진

배터리 전기자동차(BEV)는 가솔린 엔진이 없는 전기자동차입니다. 차량 전체의 전원은 배터리 팩이며 그리드를 통해 충전되어 차량에 전원을 공급합니다. BEV는 제로 방출 차량이며 기존 가솔린 자동차와 같은 유해한 꼬리 파이프 배출이나 대기 오염의 위험이 없습니다. 배터리 전기자동차에서 사용되는 MLCC는 고품질이며 250V-4kV의 고전압에서 작동해야 합니다. 세라믹 MLCC는 고온을 견딜 수 있기 때문에 분포 커패시턴스로 선호되는 선택입니다.

배터리 전기차 출하량은 2022년에는 1,318만 대로, 2029년에는 2,714만 대로 증가할 것으로 예측됩니다. 2020년 첫 COVID-19의 파도는 BEV 판매량의 역사적인 감소를 일으키고 동시에 정책 입안자의 지지를 더욱 모았습니다. 2022년에는 BEV 판매가 증가했습니다.

보다 강력한 규제 및 소비자의 관심 고조에 따라 최근 EV로 시장 이동이 가속화되고 있습니다. 여러 기업이 수요가 높은 지역을 중심으로 BEV 생산 능력을 높이기 위해 BEV 전용 생산 시설의 신설을 검토하고 있습니다. 일부 정부는 각 지역에서 EV 생산 및 판매를 늘리기 위한 이니셔티브를 취하고 있습니다. 유럽은 목표인 플릿 평균 CO2 배출량 95g/km에 연동한 EV 생산 인센티브를 OEM에 제공합니다. 배터리 가격의 지속적인 하락과 BEV의 평균 배터리 크기 증가가 성장에 기여해 2016년부터 2019년까지 시장 보급이 꾸준히 확대되었습니다. BEV는 모든 지역의 대부분의 차량 부문에서 제공됩니다.

수소 스테이션의 인프라 정비가 판매 증가 계속

연료 전지 전기자동차(FCEV)는 연료로 저장한 수소에너지를 연료 전지를 통해 전기로 변환하여 전기차와 유사한 추진 메커니즘을 가지고 있습니다. 기존의 내연기관을 동력원으로 하는 자동차에 비해 FCEV는 유해한 배기 가스를 배출하지 않습니다.

연료 전지 전기자동차의 출하량은 2022년에는 4만 대였으며, 2029년에는 6만 6,000대에 이를 것으로 예상됩니다. 풍력이나 태양광과 같은 신재생 에너지가 수소 제조 공정에 기여함에 따라 에너지 효율이 높은 FCEV 수요가 크게 증가할 것으로 보입니다.

저배출 가스차에 대한 수요가 높아짐에 따라 이산화탄소 배출 기준이 엄격해지고, 신속한 연료 보급 등의 이점으로부터 FCEV의 채용이 보다 중시되고 있습니다. FCEV 개발을 촉진하기 위해 여러 정부 기관과 상업 단체가 협력하여 연료전지 기술의 진보와 수소 보급 인프라 개발에 투자하고 있습니다. IEA에 따르면 2021년 말에는 세계에서 약 730개 소의 수소 스테이션(HRS)이 약 51,600대의 FCEV에 연료를 공급하고 있으며, 이는 FCEV의 세계 스톡이 2020년부터 거의 50% 증가하고 HRS의 수가 35% 증가한 것을 보여줍니다. 이러한 요인은 향후 FCEV의 고성장에 기여할 것으로 예상됩니다.

전기자동차용 MLCC 산업 개요

전기자동차용 MLCC 시장은 적당히 통합되어 상위 5개사에서 41.80%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, Samsung Electro-Mechanics, TDK Corporation 및 Yageo Corporation(알파벳순 정렬).

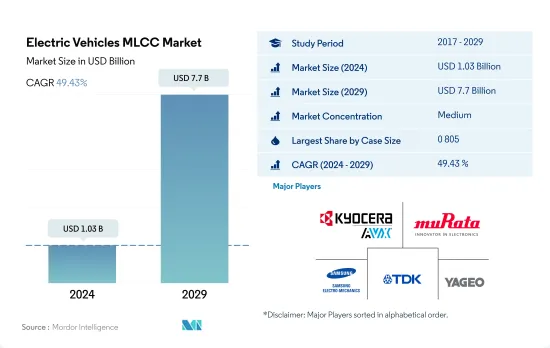

The Electric Vehicles MLCC Market size is estimated at 1.03 billion USD in 2024, and is expected to reach 7.7 billion USD by 2029, growing at a CAGR of 49.43% during the forecast period (2024-2029).

Driving efficiency through revolutionizing automotive systems with MLCCs is further propelling the demand for different case sizes

In the dynamic evolution of the automotive sector, MLCCs have transcended their conventional role as mere electronic components. These compact powerhouses now serve as the linchpin of contemporary vehicular systems, orchestrating a harmonious interplay of functions spanning power distribution, noise suppression, signal conditioning, and voltage regulation.

In this landscape, the 0 603 segment emerges as a compact yet indispensable contributor. These capacitors are characterized by compact and energy-efficient designs. As automotive technologies continue to advance, the demand for streamlined solutions has propelled the significance of the 0 603 segment to new heights.

The 0 805 capacitors hold a noteworthy position, particularly as electric vehicles (EVs) take center stage. The surging adoption of EVs accentuates the imperative of efficient power distribution and control, thereby underscoring the pivotal role of the 0 805 segment. In an era redefined by EVs, these capacitors emerge as catalysts for enhanced performance and efficiency.

The 1 206 segment strikes a delicate balance between size and versatility, rendering it a preferred choice for diverse automotive applications. As the automotive industry embraces rapid technological strides, the indispensability of the 1 210 segment becomes increasingly evident, seamlessly integrating with cutting-edge advancements.

The others category encompasses a diverse array of capacitance values meticulously tailored to address specialized automotive requisites. From emerging technologies to unique applications, this dynamic segment exemplifies the unparalleled adaptability of MLCCs in catering to the unique and evolving needs of the automotive realm.

Key catalysts that are fueling multilayer ceramic capacitor (MLCC) growth in the electric vehicle market

The market dynamics demonstrate, in terms of value, Asia Pacific supremacy with a dominant 44.97% market share, while North America and Europe maintain 23.57% and 22.80% shares, respectively.

The Asia-Pacific region is at the forefront of the electric vehicle (EV) revolution, showcasing remarkable growth driven by government support, technological advancements, and rising consumer demand. Dominated by key players like China, the region leads in EV production and innovation, solidifying its position as a dynamic force in the global EV market.

Europe, renowned for its commitment to sustainability, is pioneering the adoption of EVs as a solution to emissions reduction and environmental challenges. Stringent emission regulations and incentivized programs propel rapid EV adoption across European countries. Major automakers are investing significantly in EV production, charging infrastructure, and battery technology to ensure a greener future.

In North America, a diverse landscape of established and emerging players is shaping the EV market. Government incentives, growing environmental consciousness, and technological advancements are driving the transition toward electric mobility. Tesla's influence remains prominent, fostering innovation and competition within the region, thereby fueling the growth of the electric vehicle market.

The Rest of the World (RoW) is embracing electrification with unique characteristics. Electric two-wheelers are gaining momentum, addressing urban congestion and offering economic benefits. As the global automotive industry navigates the path to electrification, these regions collectively contribute to shaping the future of the electric vehicle MLCC market.

Global Electric Vehicles MLCC Market Trends

Supportive government policies for the deployment of public charging infrastructure will promote battery electric vehicle sales

Battery electric vehicles, or BEVs, are electric automobiles without a petrol engine. The entire vehicle is powered by the battery pack, which is recharged through the grid and powers the vehicle. BEVs are zero-emission vehicles because they produce no harmful tailpipe emissions or air pollution hazards like traditional gasoline-powered vehicles. The MLCCs consumed in battery electric vehicles must be of high-quality construction and operate at high voltages ranging from 250V to 4kV. Ceramic MLCCs are the preferred choice for distributed capacitance because of their ability to withstand high temperatures.

Battery electric vehicle shipments were 13.18 million units in 2022 and are projected to rise to 27.14 million units in 2029. The first COVID-19 wave in 2020 triggered a historic decline in BEV sales while garnering more policymakers' support. In 2022, BEV sales increased.

Stronger regulations and growing consumer interest have recently accelerated the market shift toward EVs. Several companies are considering adding a new dedicated BEV production facility to boost BEV production capability centered on high-demand regions. Several governments are taking initiatives to increase EV production and sales in the regions. Europe is providing OEMs with EV-production incentives tied to its targeted fleet average of 95 grams of CO2 per km. The continuous decline in battery prices and increase in the average battery size in BEVs contributed to the growth and helped market penetration grow steadily from 2016 through 2019. BEVs are being offered in most vehicle segments in all regions.

Infrastructure improvement for hydrogen stations continues to increase sales

Fuel cell electric vehicles (FCEVs) use hydrogen energy stored as fuel, which is then converted into electricity by the fuel cell and has a propulsion mechanism similar to that of an electric vehicle. Compared to vehicles powered by conventional internal combustion engines, FCEVs don't emit any harmful exhaust emissions.

Fuel cell electric vehicle shipments accounted for 40 thousand units in 2022 and are expected to reach 66 thousand units by 2029. As renewable energies like wind and solar contribute to the hydrogen manufacturing process, there will be a huge increase in the demand for energy-efficient FCEVs.

As the demand for low-emission vehicles is rising, there are stricter carbon emission standards, and more emphasis is being placed on the adoption of FCEVs due to benefits like quick refueling. To encourage the development of FCEVs, several government and commercial organizations are collaborating and investing in advancing fuel cell technology and the development of hydrogen refueling infrastructure. According to the IEA, at the end of 2021, there were about 730 hydrogen refueling stations (HRSs) globally providing fuel for about 51,600 FCEVs, representing an increase of almost 50% in the global stock of FCEVs and a 35% increase in the number of HRSs from 2020. These factors are expected to contribute to the high growth of FCEVs in the future.

Electric Vehicles MLCC Industry Overview

The Electric Vehicles MLCC Market is moderately consolidated, with the top five companies occupying 41.80%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, TDK Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Ev Sales

4.1.1 Global BEV (Battery Electric Vehicle) Production

4.1.2 Global FCEV (Fuel Cell Electric Vehicle) Production

4.1.3 Global HEV (Hybrid Electric Vehicle) Production

4.1.4 Global ICEV (Internal Combustion Engine Vehicle) Production

4.1.5 Global PHEV (Plug-in Hybrid Electric Vehicle) Production

4.1.6 Others

4.2 Regulatory Framework

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)