Europe Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683767

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

유럽의 건축용 코팅 시장 규모는 2024년에 181억 5,000만 달러에 달했고, 2028년에는 207억 6,000만 달러에 이르고, 예측 기간(2024년-2028년)의 CAGR은 3.42%를 나타낼 것으로 예측됩니다.

주요 하이라이트

최종 사용자별 최대 부문 - 주거용 : 유럽에서 주거용 코팅의 점유율은 상업용 건축물에 비해 상대적으로 느린 주거용 건축물의 성장으로 인해 감소하고 있습니다.

기술별 가장 빠른 성장세 - 용매 기반 : 수성 코팅은 소비자 인식과 EU REACH와 같은 규제, 다양한 국가 차원의 규제로 인해 가장 크고 빠른 성장세를 보이고 있는 기술 유형입니다.

수지별 최대 부문 - 아크릴 : 아크릴은 유럽에서 가장 지배적인 수지 유형입니다. 아크릴 라텍스 에멀젼이 용매 기반 코팅을 대체할 것으로 예상됨에 따라 아크릴의 지배력은 계속 유지될 것으로 예상됩니다.

유럽의 건축용 코팅 시장 동향

주거용이 하위 최종사용자별로 가장 큰 부문

최종 사용자 부문 중 주거 부문은 2020년 건설 부문을 지배하며 71.61%의 점유율로 유럽 시장에서 건축용 코팅제에 대한 가장 높은 수요를 창출했습니다.

주거용 코팅의 점유율은 지난 5년간 상업용에 비해 상대적으로 느린 주거용 건설의 성장으로 인해 감소하고 있습니다. 그러나 2020년에는 많은 국가에서 주거용 DIY 부문의 높은 성장과 상업용 페인트 소비의 위축으로 인해 유럽 건축용 도료 시장에서 주거용 도료의 점유율이 급격히 증가했습니다.

상업용 부문의 성장은 주거용 부문보다 약간 더 높을 것으로 예상되어 예측 기간 동안 상업용 점유율이 약간 회복 될 수 있습니다.

국가별로 독일은 최대 부문

유럽에서는 독일이 17% 이상의 점유율로 건축용 코팅제 소비량이 가장 많으며 러시아, 프랑스, 이탈리아, 영국이 그 뒤를 잇고 있습니다. 스페인, 폴란드, 북유럽 지역은 2020년 한 해 동안 각각 약 5%의 점유율을 차지한 것으로 추정됩니다. 폴란드와 러시아 등 동구권 국가의 점유율은 1인당 평균 면적과 페인트의 증가로 인해 증가할 것으로 예상됩니다.

폴란드는 예측 기간 동안 약 4%의 성장률을 기록하며 유럽에서 가장 빠르게 성장하는 건축 시장이 될 것으로 예상되며, 러시아, 스페인, 프랑스가 약 3%의 성장률로 그 뒤를 이을 것으로 전망됩니다. 독일과 이탈리아 같은 성숙 시장은 2% 미만의 낮은 성장률을 보일 것으로 예상됩니다.

폴란드, 이탈리아, 독일과 같은 많은 국가에서는 주거용 DIY 부문의 소비가 크게 증가하여 2020년에 주거용 소비가 크게 증가했습니다.

유럽의 건축용 코팅 산업 개요

유럽의 건축용 코팅 시장은 적당히 통합되어 상위 5개사에서 41.46%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. AkzoNobel NV, DAW SE, Flugger group A/S, Nippon Paint Holdings and PPG Industries, Inc.(sorted alphabetically).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제3장 주요 산업 동향

바닥면적 동향

규제 프레임워크

밸류체인과 유통채널 분석

제4장 시장 세분화

하위 최종 사용자

상업

주거

기술분야

용매 기반

수성

수지

아크릴

알키드

에폭시

폴리에스테르

폴리우레탄

기타 수지

국가명

프랑스

독일

이탈리아

북유럽 국가

폴란드

러시아

스페인

영국

기타 유럽

제5장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

AkzoNobel NV

Brillux GmbH & Co. KG

CIN, SA

DAW SE

Flugger group A/S

Hempel A/S

KOBER SRL

Nippon Paint Holdings Co., Ltd.

POLICOLOR SA

PPG Industries, Inc.

Sniezka SA

제6장 CEO에 대한 주요 전략적 질문

제7장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류 체인 분석

시장 역학(DROs)

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

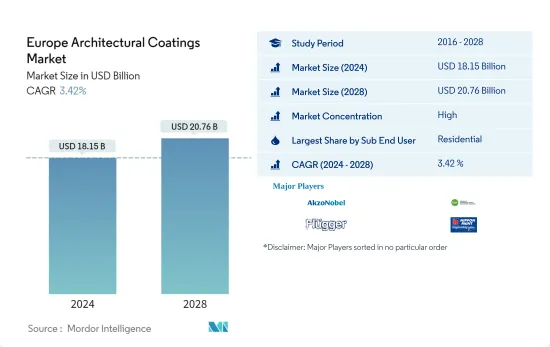

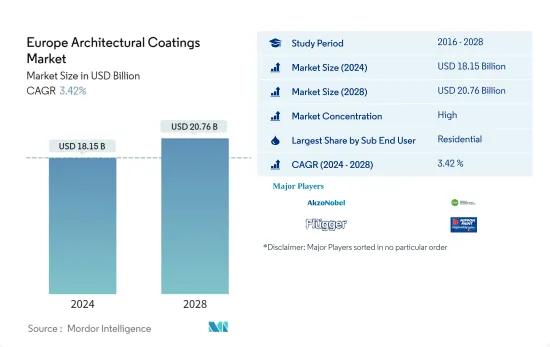

The Europe Architectural Coatings Market size is estimated at USD 18.15 billion in 2024, and is expected to reach USD 20.76 billion by 2028, growing at a CAGR of 3.42% during the forecast period (2024-2028).

Key Highlights

Largest Segment by End-user - Residential : The share of residential coatings has been declining in Europe due to the relatively slow growth of residential constructions compared to commercial constructions.

Fastest Segment by Technology - Solventborne : Waterborne coatings are the largest and fastest technology type due to consumer awareness and regulations, such as EU REACH, combined with various country-level regulations.

Largest Segment by Resin - Acrylic : Acrylics are the most dominant resin type in Europe. They are expected to continue their dominance as acrylic latex emulsions are expected to replace solvent-borne coatings.

Europe Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

Among the end-user segments, the residential segment dominated the construction sector in 2020, generating the highest demand for architectural coatings in the European market, with a share of 71.61%.

The share of residential coatings has been declining over the past five years due to the relatively slow growth of residential construction compared to commercial. However, in 2020, the high growth of the residential DIY segment in many countries and the contraction of commercial paint consumption contributed to the sudden increase in the share of residential coatings in the European architectural coatings market.

The growth of the commercial segment is expected to be slightly higher than its residential counterpart, which may result in a slight recovery of the commercial share during the forecast period.

Germany is the largest segment by Country.

In Europe, Germany has the largest architectural coatings consumption, with more than 17% share, followed by Russia, France, Italy, and the United Kingdom. Spain, Poland, and Nordic regions were estimated to have had a share of around 5% each during 2020. The share of eastern block countries such as Poland and Russia is expected to increase due to the increasing median floor area and paint per capita.

Poland is estimated to be the fastest-growing architectural market in Europe, with around 4% growth during the forecast period, followed by Russia, Spain, and France, with around 3% growth rates. Mature markets such as Germany and Italy are expected to have lower growth rates of less than and around 2% in volume.

Many countries such as Poland, Italy, and Germany saw huge increases in residential consumption in 2020 due to huge growth in consumption in the residential DIY segment.

Europe Architectural Coatings Industry Overview

The Europe Architectural Coatings Market is moderately consolidated, with the top five companies occupying 41.46%. The major players in this market are AkzoNobel N.V., DAW SE, Flugger group A/S, Nippon Paint Holdings Co., Ltd. and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

2.1 Study Assumptions & Market Definition

2.2 Scope of the Study

2.3 Research Methodology

3 KEY INDUSTRY TRENDS

3.1 Floor Area Trends

3.2 Regulatory Framework

3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

4.1 Sub End User

4.1.1 Commercial

4.1.2 Residential

4.2 Technology

4.2.1 Solventborne

4.2.2 Waterborne

4.3 Resin

4.3.1 Acrylic

4.3.2 Alkyd

4.3.3 Epoxy

4.3.4 Polyester

4.3.5 Polyurethane

4.3.6 Other Resin Types

4.4 Country

4.4.1 France

4.4.2 Germany

4.4.3 Italy

4.4.4 Nordic Countries

4.4.5 Poland

4.4.6 Russia

4.4.7 Spain

4.4.8 United Kingdom

4.4.9 Rest Of Europe

5 COMPETITIVE LANDSCAPE

5.1 Key Strategic Moves

5.2 Market Share Analysis

5.3 Company Landscape

5.4 Company Profiles

5.4.1 AkzoNobel N.V.

5.4.2 Brillux GmbH & Co. KG

5.4.3 CIN, S.A.

5.4.4 DAW SE

5.4.5 Flugger group A/S

5.4.6 Hempel A/S

5.4.7 KOBER SRL

5.4.8 Nippon Paint Holdings Co., Ltd.

5.4.9 POLICOLOR SA

5.4.10 PPG Industries, Inc.

5.4.11 Sniezka SA

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS