ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

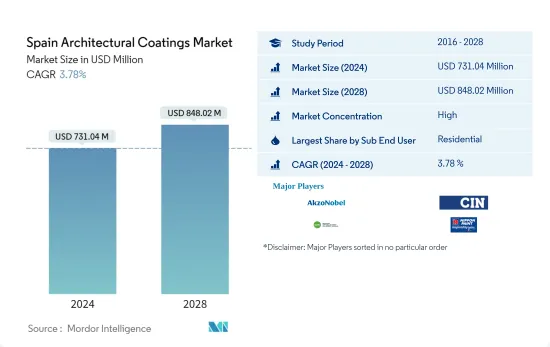

스페인 건축용 코팅 시장 규모는 2024년에 7억 3,104만 달러에 달했고, 2028년에는 8억 4,802만 달러에 이를 것으로 예측되며, 예측 기간(2024-2028년)의 CAGR은 3.78%를 나타낼 것으로 예상됩니다.

주요 하이라이트

최종 사용자별 최대 부문 - 주택 : 주택 건설 부문의 꾸준한 성장은 상업 부문의 성장 감소와 관련하여 주거 부문의 소비를 촉진합니다.

기술별 최대 부문 - 수성 : 건축용 코팅 제조업체에 의한 VOC 규제의 채택 확대와 에코 라벨의 판매가 수성 도료 시장 점유율 확대에 기여하고 있습니다.

수지별 최대 부문 - 아크릴 : 아크릴은 기술적 이점, 건축 분야의 VOC 배출량이 적고 건물의 외벽 코팅에 대한 선호도로 인해 수지의 주요 유형이 되었습니다.

스페인 건축용 코팅 시장 동향

서브 최종사용자별로는 주택이 최대 부문.

스페인의 건축용 코팅 소비량은 2013년 이후 장기 회복과 2017년 재활 공사 증가로 2017년 전년 대비 7.3% 증가한 호황을 맞았습니다. 그러나 건축용 코팅의 대부분을 차지하는 대체 분야는 2018년과 2019년 수리 허가의 감소로 감소했습니다.

2020년에는 COVID-19의 보급에 의해 주택 및 상업 모두 신축이 감소해, 건축용 코팅 소비량의 느린 성장이 관찰되었습니다. 그러나 신축의 감소는 2020년 주택 부문에서 DIY 분야의 성장에 의해 상쇄되었습니다.

2021년에는 주택 및 상업 부문 모두 회복해, 도료 소비량이 회복되었습니다. 건축용 코팅의 밝은 미래에 대한 코팅 기업의 자신감이 높아지면서 향후 수 년간 수요를 촉진할 수 있습니다.

스페인 건축용 코팅 산업의 개요

스페인의 건축용 코팅 시장은 상당히 통합되어 있으며 상위 5개 기업에서 73.89%를 차지합니다. 이 시장 주요 기업은 다음과 같습니다. AkzoNobel NV, CIN, SA, DAW SE, Nippon Paint Holdings and PPG Industries, Inc.(sorted alphabetically).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제3장 주요 산업 동향

바닥면적 동향

규제 프레임워크

밸류체인과 유통채널 분석

제4장 시장 세분화

서브 최종 사용자

상업

주택

기술

용제계

수성

수지

아크릴

알키드

에폭시

폴리에스테르

폴리우레탄

기타 수지 유형

제5장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 프로파일

AkzoNobel NV

CIN, SA

DAW SE

IVM Chemicals srl

Jotun

JUNO

Nippon Paint Holdings Co., Ltd.

Pinturas Decolor

PPG Industries, Inc.

The Barpimo Group

제6장 CEO에 대한 주요 전략적 질문

제7장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

SHW

영문 목차

영문목차

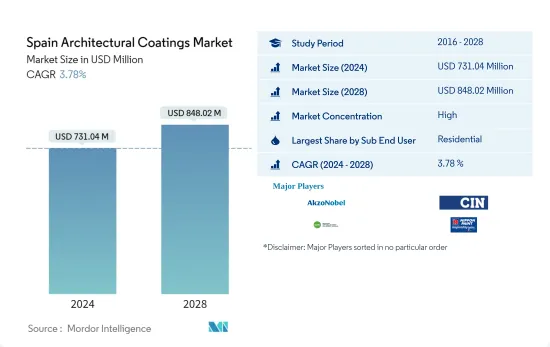

The Spain Architectural Coatings Market size is estimated at USD 731.04 million in 2024, and is expected to reach USD 848.02 million by 2028, growing at a CAGR of 3.78% during the forecast period (2024-2028).

Key Highlights

Largest Segment by End-user - Residential : The steady growth in the residential construction sector, accompanied by lower growth in the commercial sector, fuels the consumption in the residential segment.

Largest Segment by Technology - Waterborne : The growing adoption of VOC regulations by architectural coating manufacturers and marketing with eco-labels help waterborne coatings gain a significant market share.

Largest Segment by Resin - Acrylic : Acrylic is a leading type of resin due to its technological advantages, low VOC emissions in the architectural segment, and preference to coat the exterior wall of buildings.

Spain Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

The architectural coating consumption in Spain peaked in 2017 with an increment of 7.3% Y-o-Y due to the long-time recovery since 2013 and increased rehabilitation work in 2017. However, the repaint segment, which accounts for the major part of architectural coatings, declined due to lower restoration permits in 2018 and 2019.

The slow growth in the architectural coating consumption was observed in 2020 due to lower new constructions in both residential and commercial sectors due to the spread of COVID-19. However, the decline in new construction was countered by the growth in the do-it-yourself (DIY) segment in the residential sector in 2020.

The coating consumption recovered in 2021 due to a rebound in both residential and commercial sectors. The growing confidence of coating companies in the positive future of architectural coatings may fuel the demand over the coming years.

Spain Architectural Coatings Industry Overview

The Spain Architectural Coatings Market is fairly consolidated, with the top five companies occupying 73.89%. The major players in this market are AkzoNobel N.V., CIN, S.A., DAW SE, Nippon Paint Holdings Co., Ltd. and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

2.1 Study Assumptions & Market Definition

2.2 Scope of the Study

2.3 Research Methodology

3 KEY INDUSTRY TRENDS

3.1 Floor Area Trends

3.2 Regulatory Framework

3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

4.1 Sub End User

4.1.1 Commercial

4.1.2 Residential

4.2 Technology

4.2.1 Solventborne

4.2.2 Waterborne

4.3 Resin

4.3.1 Acrylic

4.3.2 Alkyd

4.3.3 Epoxy

4.3.4 Polyester

4.3.5 Polyurethane

4.3.6 Other Resin Types

5 COMPETITIVE LANDSCAPE

5.1 Key Strategic Moves

5.2 Market Share Analysis

5.3 Company Landscape

5.4 Company Profiles

5.4.1 AkzoNobel N.V.

5.4.2 CIN, S.A.

5.4.3 DAW SE

5.4.4 IVM Chemicals srl

5.4.5 Jotun

5.4.6 JUNO

5.4.7 Nippon Paint Holdings Co., Ltd.

5.4.8 Pinturas Decolor

5.4.9 PPG Industries, Inc.

5.4.10 The Barpimo Group

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS