시큐어 액세스 서비스 엣지(SASE) 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Secure Access Service Edge (SASE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683522

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

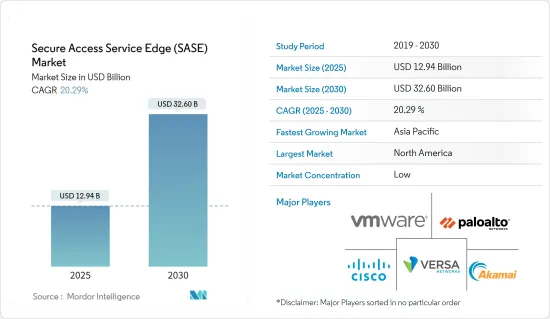

시큐어 액세스 서비스 엣지 시장 규모는 2025년에 129억 4,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 20.29%로 성장할 전망이며, 2030년에는 326억 달러에 달할 것으로 예측됩니다.

SASE는 네트워크 액세스 보안의 패러다임 시프트를 의미합니다. 이는 Firewall-as-a-service(FWaaS) 및 SD-WAN과 같은 네트워크와 보안 기능을 통합하고 네트워크-as-a-service(NaaS)를 단일 클라우드 네이티브 서비스에 통합한 것입니다. 이 통합을 통해 분산된 워크포스 및 클라우드 기반 애플리케이션은 확장 가능하고 유연하며 안전한 방식으로 보호되고 연결됩니다.

주요 하이라이트

SASE는 SDN 환경의 보안을 향상시키고 Software-Defined Networking(SDN) 시스템을 완성시킵니다. 동적 네트워크 구성은 SDN에 의해 가능하며 SASE는 변화하는 요구 사항을 수용하기 위해 변화하는 네트워크의 안전성을 보장합니다. SASE는 사물인터넷(IoT)의 발전과 함께 IoT 디바이스와 이들이 생성하는 데이터를 보호합니다. IoT 컨텍스트에서는 안전한 통신과 데이터 보호가 필수적입니다.

또한 클라우드 기반 SASE는 채용이 급증할 수 있습니다. 예를 들어, 2024년 2월, 화웨이는 IP Club Carnival에서 새로운 HiSec SASE 솔루션을 발표했습니다. 새롭게 발표된 이 솔루션은 클라우드 네트워크 엣ㅈ 엔드포인트 통합 지능형 보호 기능을 제공하여 기업의 본사와 지사에 일관된 보안 보증을 제공합니다.

퍼블릭 클라우드의 사용이 증가함에 따라 모든 기업에서 클라우드에 대한 지출이 증가하고 있습니다. 클라우드에 대한 지출은 이미 IT 예산에서 중요한 위치를 차지하고 있으며, 약 77%의 기업이 연간 클라우드 지출액이 1,200만 달러를 초과하고, 80%의 기업이 120만 달러를 초과한다고 응답하고 있습니다. 중소기업은 워크로드의 수가 적고 규모가 작기 때문에 클라우드의 전반적인 비용이 저렴합니다.

시장 관계자는 고객에게 SASE 서비스를 제공하면서 적절한 규제 준수를 유지하고 비용을 집행하는 데 관심이 있습니다. 공급업체는 자사의 기술을 보호하고 원활하게 운영하며 모든 적용 가능한 법률 및 규정을 준수하기가 어려울 수 있습니다. 공급업체가 규칙이나 기준을 준수하지 않으면 서비스에 부정적인 영향을 미치고 고객의 비즈니스 운영을 위험에 빠뜨릴 수 있습니다. 공급업체는 일반적으로 인정되는 기준과 서비스 제공 모범 사례를 준수하여 우선 순위를 정하는 프로그램과 서비스를 제공합니다. 공급업체는 진화하는 기술과 정부의 규제에 대응하기 위한 지원이 필요합니다.

전 세계적으로 더 많은 기업에서 투자 전략을 확대하면 비즈니스 성장을 지원하는 시큐어 액세스 서비스 엣지 채택을 가속화할 것으로 보입니다. COVID-19 이후의 시대에는 단일 공급업체에서 SASE를 제공하는 공급업체의 수가 크게 증가할 것으로 보입니다. COVID-19 이후 시대의 SD-WAN의 신규 구매는 싱글 벤더 SASE 제공 제품의 일부가 될 것으로 보입니다.

시큐어 액세스 서비스 엣지(SASE) 시장 동향

대기업이 큰 시장 점유율을 차지합니다.

엣지 컴퓨팅 채택 확대, 클라우드 인프라로의 전환, 원격 워크의 급증으로 기존 네트워크 아키텍처와 보안 모델이 크게 변화하고 있습니다. 대규모 IT 예산과 숙련된 직원을 이용할 수 있는 대기업은 이 시장의 현실에 빠르게 적응하고 있습니다.

분산형 워크포스 모델을 채택한 대기업은 VPN 집성 용량이 엄격하게 제한된 기존 WAN 아키텍처에서는 대부분의 WFA(Work-From-Anywhere) 워크플로를 지원할 수 없다는 것을 알고 있습니다. 기존 보안 모델과 고정 디지털 변환에 대한 투자는 지난 몇 년동안 대기업에서 SASE 채택을 늦추고 있습니다.

세계 시장에서는 새로운 IT 인프라가 확대되고 있습니다. 보안과 네트워크를 단일 클라우드 플랫폼에 통합하는 대기업이 급증하고 있습니다. 그 결과 멀웨어 아즈 어 서비스는 병원, 석유, 가스전, 전력망, 운송 서비스, 기업 네트워크 등 노출된 IoT와 OT에 대한 대규모 운영으로 전환하고 있습니다. 위협 행위자는 운영 환경과 임베디드 IoT 및 OT 장치의 구성을 밝히고 이를 악용하기 위해 상당한 조사 노력이 필요합니다.

마이크로소프트의 디지털 디펜스 보고서 2023에 따르면 세계적으로 공격이 증가하고 있으며, 그 중에서도 ID 공격이 가장 많아 전체의 42%가 ID 공격뿐이라고 합니다. 또한 사이버 공격은 해마다 증가하고 있으며, 랜섬웨어 관련 피해액은 세계적으로 증가하고 있습니다. Microsoft가 2024년에 발표한 보고서에 따르면 암호 공격 시도는 한 달에 약 30억 건에서 300억 건 이상으로 급증하고 있습니다.

연결된 디지털 세계에서는 장치가 대규모 시스템과 온라인으로 통신하고 대량의 데이터를 수집하며 대기업에 비즈니스 기회를 제공하는 가시성을 창출합니다. 이 상황은 또한 사이버 위협에 대한 문을 열고 사이버 범죄 사업을 수십억 달러 규모로 만듭니다. 컴퓨터, 라우터, 프린터, 웹캠, 원격 관리 장치 등의 IoT 장치는 보안 위험에 노출되어 있습니다. 이러한 장치는 많은 조직의 업무에 중요하기 때문에 즉시 책임이나 보안 위험이 될 수 있습니다. 모든 업계에서 IoT 솔루션이 빠르게 채택됨에 따라 공격의 벡터가 증가하고 조직이 위험에 노출될 기회가 늘어나고 있습니다. 원격 관리 장치에 대한 공격, 웹을 통한 공격, 데이터베이스에 대한 공격은 대기업에서 가장 많이 발생합니다.

앞서 언급한 인시던트는 다른 보안 네트워킹 전략과는 밀접하게 구분할 수 있는 능력을 가지고 있기 때문에 대기업에서 네트워크 아즈 어 서비스(NaaS)의 채택을 뒷받침할 가능성이 높습니다. SASE는 데이터센터의 보안에 의존하는 것이 아니라 사용자의 장치로부터의 전체 트래픽이 최종 목적지로 전송되기 전에 근처에 있는 지점에서 검사되기 때문에 직접적인 접근 방식을 채택하고 있습니다. 따라서 클라우드에서 분산된 워크포스 및 데이터를 보호하기 위한 이상적인 옵션입니다. 현대 클라우드 중심의 대기업에서 사용자, 디바이스 및 애플리케이션은 어디서나 작업할 수 있는 안전한 액세스가 필요합니다. 레거시 시스템은 이러한 유연성을 제공하는 데 필요한 대역폭을 견딜 수 없습니다. 그러나 SASE는 사용자나 장치의 위치에 관계없이 기업 수준의 보안을 유지하면서 액세스할 수 있으므로 이 부문 수요를 강화하고 있습니다.

북미가 큰 점유율을 차지합니다.

미국은 선진 경제권이며 선진 기술의 도입과 수용, 네트워크 자동화 개발, 클라우드 기반 서비스의 급증이 시큐어 액세스 서비스 엣지 시장에 크게 기여하고 있습니다. 최종 사용자 업계의 디지털화 진전 및 Cisco Systems Inc., Vmware Inc., Palo Alto Networks, Versa Networks Inc., Akamai Technologies 등 유명 벤더의 존재가 시장의 성장에 기여하고 있습니다.

기업의 디지털 변환이 빠르게 가속화됨에 따라 보안은 클라우드 컴퓨팅으로 전환하고 있습니다. 다수의 최종 사용자 산업에서 클라우드 서비스가 크게 채택되고 있기 때문에 네트워크 인프라의 안전성을 확보하고 복잡성을 줄이고 속도와 민첩성을 향상시켜야 합니다. 이것은 향후 몇 년동안 시장 벤더에게 큰 성장 기회를 가져올 것으로 예상됩니다.

미국에는 세 가지 주요 클라우드 서비스 제공업체가 있습니다. Amazon Web Services(Amazon Web Services), Microsoft Azure(Azure), Google Cloud(Google Cloud)입니다. 또한 5G, 자율주행, IoT, 블록체인, 인공지능, 게임 등 주요 기술 혁신의 거점으로도 생각되고 있습니다. SASE의 기능을 통합하면 제로 트러스트 보안 기능을 기업 아키텍처에 수렴할 수 있으며 이는 신뢰할 수 있는 네트워크 보안 시스템을 구현하는 데 가장 중요합니다. 따라서 SASE 솔루션은 최종 사용자의 네트워크 및 보안 아키텍처를 변화시켜 사이버 위험, 비용 및 복잡성을 줄이는 것으로 분석됩니다.

Orange Business, Palo Alto Networks, Orange Cyberdefense는 2023년 8월에 제휴하여 클라우드 네이티브 관리형 시큐어 액세스 서비스 엣지(SASE) 솔루션을 세계 기업에 제공했습니다. 기업이 하이브리드 업무에 대응하고 고객에게 최신 제품과 서비스를 제공하기 위해 클라우드 도입을 가속화하고 있기 때문에 디지털 공격 대상 영역이 확대되고 있습니다. 이 파트너십은 업계에서 가장 완벽한 AI를 활용한 SASE 솔루션, 권고 및 컨설턴트 서비스, 세계적인 관리 네트워크, 보안 및 디지털 서비스를 제공합니다. 이 서비스를 활용하는 조직은 SASE에 의한 혁신의 투자 수익률(ROI)을 극대화할 수 있습니다.

캐나다는 클라우드 전개의 최전선에 있습니다. 많은 조직이 퍼블릭, 프라이빗, 엣지 클라우드를 조합하여 도입하고 있습니다. 하이브리드 워크와 클라우드 변혁의 대두로 네트워크 경계를 넘어 확장하는 보안 서비스에 대한 수요가 높아지고 있으며 캐나다 시장의 성장에 긍정적인 영향을 미치고 있습니다. 게다가 이 나라에서는 데이터 보호 및 규제에 관한 법규가 엄격하여 최종 사용자 업계에서 SASE 솔루션 수요를 더욱 밀어 올리고 있습니다.

자동화의 진전과 연결 장비의 도입으로 시장 수요가 크게 증가할 것으로 예상됩니다. Network-as-a-Service(NaaS) 모델은 일상적인 장비 유지보수 부하를 줄이고 고객 서비스와 같은 작업에 집중함으로써 중소기업에 이익을 제공합니다. 캐나다에서는 소규모 기업이 많기 때문에 NaaS는 향후 몇 년동안 큰 동향이 될 것으로 예상됩니다.

시큐어 액세스 서비스 엣지(SASE) 시장 개요

시큐어 액세스 서비스 엣지 시장공급업체는 다양한 서비스를 제공하고 적당히 통합되어 있습니다. 그러나 VMware, Palo Alto Networks, Versa Networks Inc. 및 Cisco Systems Inc.와 같은 주요 공급업체는 다양한 지역의 다양한 최종 사용자에게 매우 선호되는 네트워크 서비스 제공 업체입니다.

2024년 1월-킨드릴은 고객이 보안 관리를 개선하고 사이버 인시던트를 사전에 대처하고 대응할 수 있도록 Cisco와 제휴하여 두 가지 새로운 보안 에지 서비스를 시작할 것이라고 발표했습니다. Kyndryl 및 Cisco의 가용 SD-WAN 서비스와 함께 새로 시작된 보안 에지 서비스는 기업이 시큐어 액세스 서비스 엣지(SASE) 아키텍처로 마이그레이션할 수 있는 견고한 기반을 구축할 수 있도록 합니다.

2024년 1월-AI/ML을 활용한 통합 시큐어 액세스 서비스 엣지(SASE) 솔루션의 선두 공급자인 버서 네트웍스는 통합 SASE 게이트웨이의 새로운 시리즈를 발표했습니다. 이 게이트웨이는 100Gbps 이상의 놀라운 처리량을 제공하며 향상된 컴퓨팅 기능에 대한 수요 증가에 대응하도록 설계되었습니다. 이러한 수요는 네트워킹과 보안 기능의 통합이 진행되는 업계에 의해 견인되고 있습니다. Versa의 새로운 게이트웨이는 고성능 하드웨어와 Versa 운영 체제(VOS)를 통합하고 단일 경로 아키텍처를 특징으로 하는 회사의 통합 SASE 소프트웨어 스택입니다. 이 성능 향상으로 기업은 처음으로 보안 기능과 여러 네트워킹을 단일 게이트웨이에 통합할 수 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도-Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

경쟁 기업간 경쟁 관계

대체품의 위협

시장에 영향을 미치는 거시경제 요인 평가

제5장 시장 역학

시장 성장 촉진요인

SD-WAN, FWaaS, SWG, CASB, ZTNA 기능을 결합한 단일 네트워크 아키텍처에 대한 요구 증가

보안 절차 및 도구 부족

데이터 보호 및 규제법에 대한 컴플라이언스 의무화

시장 성장 억제요인

클라우드 리소스, 클라우드 보안 아키텍처, SD-WAN 전략에 대한 지식 부족

높은 초기 도입 비용 및 SASE 아키텍처와 그 컴포넌트 표준화의 부족

제6장 시장 세분화

제공 유형별

서비스로서의 네트워크

서비스로서의 보안

조직 규모별

대기업

중소기업

최종 사용자 산업별

BFSI

IT 및 통신

소매

헬스케어

정부기관

제조업

기타 최종 사용자 산업별

지역별

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

벨기에

네덜란드

룩셈부르크

덴마크

핀란드

노르웨이

스웨덴

아이슬란드

아시아

인도

중국

일본

대만

한국

말레이시아

홍콩

호주 및 뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

Cisco Systems Inc.

VMWare Inc.

Palo Alto Networks.

Versa Networks Inc.

Akamai Technologies Inc.

Cato Networks

Fortinet Inc.

Check Point Software Technologies Ltd

Cloudflare Inc.

Forcepoint

제8장 투자 분석

제9장 시장 전망

AJY

영문 목차

영문목차

The Secure Access Service Edge Market size is estimated at USD 12.94 billion in 2025, and is expected to reach USD 32.60 billion by 2030, at a CAGR of 20.29% during the forecast period (2025-2030).

SASE signifies a paradigm shift in network access security. It combines network and security features, like Firewall-as-a-service (FWaaS) and SD-WAN, further combining network-as-a-service (NaaS) into a single cloud-native service. With this convergence, distributed workforces and cloud-based applications will be protected and connected in a scalable, flexible, and secure manner.

Key Highlights

SASE improves security in SDN environments, thereby completing software-defined networking (SDN) systems. Dynamic network configuration is made possible by SDN, and SASE guarantees that these networks are secure as they change in order to meet the changing requirements. SASE protects IoT devices and the data they generate as the Internet of Things (IoT) develops. In the context of the IoT, secure communications and data protection are essential.

Furthermore, cloud-based SASE may witness a surge in adoption. For instance, in February 2024, Huawei announced the new HiSec SASE Solution launch at the IP Club Carnival. This newly launched solution comes with cloud-network-edge-endpoint integrated intelligent protection, providing consistent security assurance for the enterprise headquarters and branches.

The increasing usage of the public cloud is boosting cloud spending for businesses of all kinds. Cloud spending is already a significant aspect of IT budgets, wherein about 77% of companies stated that their annual cloud spending value surpasses USD 12 million, and 80% of them stated that the value exceeds USD 1.2 million. As SMBs have fewer and smaller workloads, their overall cloud costs are cheaper.

The market players are concerned about maintaining proper regulatory compliance while offering clients SASE services and executing expenses. Sometimes, vendors find it difficult to safeguard their technology, keep running smoothly, and comply with all applicable laws and regulations. Vendors' non-compliance with rules and standards can adversely affect their services and jeopardize clients' business operations. By adhering to the accepted standards and best service-delivery practices, they offer programs and services to prioritize them. Vendors need help keeping up with evolving technologies and government regulations.

The growth in investment strategies in a larger share of businesses globally will accelerate the adoption of secure access service edge in supporting business growth. In the post-COVID-19 era, there will be a significant increase in the number of vendors with single-vendor SASE offerings. New SD-WAN purchases in the post-COVID-19 era will be part of a single-vendor SASE offering.

Secure Access Service Edge (SASE) Market Trends

Large Enterprises will Hold Major Market Shares

Increased adoption of edge computing, the shift to cloud infrastructure, and a surge in remote work have challenged many traditional network architectures and security models. Large enterprises with access to larger IT budgets and skilled employees are rapidly adapting to this market reality.

Large enterprises with a distributed workforce model find the traditional WAN architectures with rigidly limited VPN aggregation capacity inadequate for most work-from-anywhere (WFA) workflows. Existing security models and fixed digital transformation investments have slowed down the adoption of SASE among large enterprises over the last few years.

The global market is witnessing an expansion in new IT infrastructure. Large enterprises that combine security and networks into a single cloud platform are proliferating. As a result, Malware-as-a-service has moved to large-scale operations against exposed IoT and OT in hospitals, oil and gas fields, electrical grids, transportation services, and corporate networks. Threat actors require significant research efforts to uncover and exploit the configuration of operating environments and embedded IoT and OT devices.

According to the Microsoft Digital Defense Report 2023, Microsoft said that globally, there has been a growing number of attacks, of which identity attacks are the most common, and 42% of the total attacks are only identity attacks. Also, every year, there has been an increasing number of cyberattacks, and the cost of ransomware-related damage increases globally. As per the report published by Microsoft in 2024, attempted password attacks have soared to over 30 billion from around 3 billion per month.

In a connected digital world, devices communicate online with larger systems, collecting voluminous data and creating visibility to bring business opportunities to large enterprises. This situation also opens the doors for cyber threats, making the cybercrime business worth multi-billion dollars. IoT devices such as computers, routers, printers, web cameras, and remote management devices are at a security risk. These devices are critical to many organizations' operations; hence, they can quickly become a liability and security risk. The rapid adoption of IoT solutions close to every industry has increased the number of attack vectors and organizations' risk exposure. Attacks against remote management devices, attacks via the web, and attacks on databases are most prevalent among large enterprises.

The aforementioned incidents are likely to boost the adoption of the network-as-a-service (NaaS) in large enterprises due to its ability to stand out from other secure networking strategies. Rather than relying on data center security, SASE has a direct approach as the overall traffic from the users' devices is inspected at a nearby point of presence before being sent to its final destination. This makes it an ideal option for protecting distributed workforces and data in the cloud. In modern cloud-centric large enterprises, users, devices, and applications require secure access while working from anywhere. Legacy systems cannot tolerate the bandwidth needed to provide this flexibility. However, SASE can do so while maintaining enterprise-level security for users and devices at any location, which bolsters this segment's demand.

North America will Hold a Significant Share

The United States is a developed economy with a significant inclination toward implementing and accepting advanced technology, development in network automation, and surge in cloud-based services, thereby contributing to the secure access service edge market. The growing digitization among end-user industries and the presence of prominent market vendors, like Cisco Systems Inc., Vmware Inc., Palo Alto Networks, Versa Networks Inc., and Akamai Technologies, are contributing to the market's growth.

Security is moving toward cloud computation due to the fast acceleration of the digital transformation of businesses. The significant adoption of cloud services in several end-user industries necessitates securing the network infrastructure and reducing complexity to improve speed and agility. This is anticipated to create substantial growth opportunities for market vendors in the coming years.

The United States is home to three major cloud service providers: Amazon Web Services, Microsoft's Azure, and Google Cloud. It is also considered to be the hub for major technological innovations such as 5G, autonomous driving, IoT, Blockchain, artificial intelligence, and gaming. Integrating SASE capabilities converges zero trust security capabilities into enterprise architectures, which is paramount in achieving a trusted network security posture. Thus, SASE solutions are analyzed to transform the end-users networks and security architectures to reduce cyber risks, costs, and complexities.

Orange Business, Palo Alto Networks, and Orange Cyberdefense partnered in August 2023 to deliver a cloud-native managed security access service edge (SASE) solution to enterprises globally. The digital attack surface has expanded as organizations expedite cloud adoption to accommodate hybrid work and deliver the latest products and services to their customers. The partnership provides the industry's most complete AI-powered SASE solutions, advisory and consultant services, and global managed network, security, and digital services. Organizations using this offering can maximize their SASE transformation's return on investments (ROI).

Canada is at the forefront of cloud adoption. Many organizations are deploying a mix of public, private, and edge clouds. With the rise of hybrid work and cloud transformation, the demand for security services to expand beyond the network perimeter is increasing, positively impacting the growth of the country's market. In addition, stringent data protection and regulatory legislation in the country further drive the demand for SASE solutions in end-user industries.

The market demand is anticipated to rise significantly due to increasing automation and deploying connected devices. The network-as-a-service (NaaS) model benefits small businesses by offloading day-to-day equipment maintenance and focusing on tasks such as customer service. With a large base of small businesses in Canada, NaaS is expected to become a significant trend in the coming years.

Secure Access Service Edge (SASE) Market Overview

The secure access service edge market vendors are moderately consolidated with an array of services. However, major vendors like VMware, Palo Alto Networks, Versa Networks Inc., and Cisco Systems Inc. are highly preferred network service providers for various end users in various regions.

January 2024 - Kyndryl announced that the company partnered with Cisco to launch two of its new security edge services in order to help customers improvise their security controls and address and respond to cyber incidents proactively. The newly launched security edge services along with Kyndryl and Cisco's available SD-WAN services, enable organizations to build a solid foundation to transition into a secure access service edge (SASE) architecture.

January 2024-Versa Networks, a leading provider of AI/ML-powered Unified Secure Access Service Edge (SASE) solutions, has announced the launch of a new series of Unified SASE gateways. These gateways offer an impressive throughput exceeding 100 Gbps, designed to address the rising demand for enhanced computing capabilities. This demand is driven by the industry's increasing integration of networking and security functions. Versa's new gateways integrate high-performance hardware with the Versa Operating System (VOS), the company's unified SASE software stack, which features a single-pass architecture. This improved performance allows organizations to consolidate security functions and multiple networking into a single gateway for the first time.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Intensity of Competitive Rivalry

4.2.5 Threat of Substitute Products and Services

4.3 Assessment of Macro Economic Factors Impact on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Need for a Single Network Architecture that Combines SD-WAN, FWaaS, SWG, CASB, and ZTNA Capabilities

5.1.2 Lack of Security Procedures and Tools

5.1.3 Mandatory Compliance with Data Protection and Regulatory Legislation

5.2 Market Restraints

5.2.1 Lack of Knowledge of Cloud Resources, Cloud Security Architecture, and SD-WAN Strategy

5.2.2 High Upfront Implementation Costs and Lack of Standardization Around SASE Architecture and Its Components