인덕터, 코어 및 비드 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Inductors, Cores and Beads - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683231

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

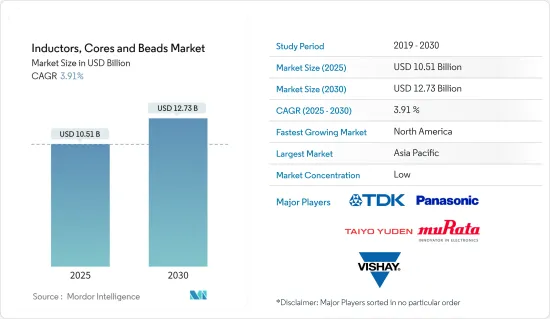

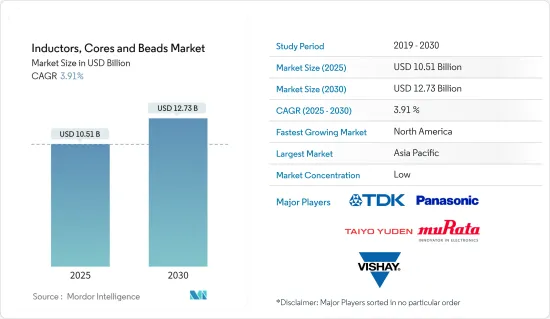

인덕터, 코어 및 비드 시장 규모는 2025년에 105억 1,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 3.91%로, 2030년에는 127억 3,000만 달러에 달할 것으로 예측됩니다.

스마트폰, 모듈, IoT 단말기용 소형 칩과 자동차용 고신뢰성 칩을 중심으로 SMD의 신제품 개발이 활발해지고 있습니다.

주요 하이라이트

전원 공급 장치의 밀도와 효율을 높이는 것은 대부분의 인덕터 설계자가 직면한 과제입니다. 점점 더 엄격해지는 용도 요구 사항을 충족하기 위해 크기를 줄이고 고성능 전력 솔루션이 지속적으로 요구되고 있습니다.

세계적으로 스마트폰, 태블릿, 휴대용 게임 콘솔, 노트북, 셋톱박스 등 가전제품에 대한 수요가 증가하면서 다양한 인덕터, 코어 및 비드에 대한 수요가 증가하고 있는 것이 주요 요인입니다.

또한 산업, 항공우주 및 방위, 의료 부문에서 높은 신뢰성이 요구되는 용도의 수요도 증가하고 있습니다.

인덕터, 코어 및 비드 시장 동향

상당한 시장 점유율을 보이는 소비자 가전 제품

스마트폰의 약 15%는 세라믹과 유리로 만들어지며, 열 관리를 위한 회로 기판은 인덕터, 퓨즈 또는 저항과 같은 수동 부품의 코어를 사용하는 전자에서 사용됩니다.

사물 인터넷과 5G 네트워크는 기기와 네트워크 간 정보 통신의 전반적인 속도와 효율성, IoT, 자율 주행 및 M2M 성능을 향상시킬 것으로 예상됩니다.

대부분의 소비자 가전 제품은 고전력 장치이며 전력은 수백에서 수 킬로와트까지 다양하며, 사용되는 자기 부품의 양은 충전 파일의 전력에 따라 달라집니다. 평균적으로 충전 파일에는 20개의 자기 부품이 필요하며, 이 중 인덕터는 더 많은 양이 사용됩니다.

문제는 여전히 넓은 칩 면적 활용도입니다. 예를 들어 인텔은 멀티코어 프로세서의 전력 관리를 위해 DC-DC 컨버터에 사용되는 온칩 인덕터가 전체 사용 가능한 칩 면적의 약 4분의 1을 차지하기 때문에 비용이 많이 든다고 밝혔습니다.

북미가 큰 시장 점유율을 차지

미국은 자동차 전자 장치에서 인덕터 사용이 증가하고 스마트 그리드 기술 채택이 증가하고 있습니다. 인덕터는 다양한 응용 분야로 인해 많은 전자 시스템의 주요 구성 요소 중 하나입니다. 광범위한 사용으로 인해 북미 전역의 여러 산업에서 더 많은 인덕터가 적용되고 있습니다.

미국 전력회사들은 2016년에 발전, 송전, 배전 인프라에 약 1,440억 달러를 투자했습니다. IEA에 따르면 2018년 미국의 스마트 그리드 인프라에 대한 투자액은 126억 달러에 달했습니다.

인덕터, 코어 및 비드는 저전력 소비와 다기능 적응성으로 인해 기존의 할로겐 및 HID 헤드라이트, ADAS, 자동차 점화 시스템 등을 대체하는 최신 적응형 LED 헤드라이트에서 응용 분야를 찾고 있습니다.

2018년 미국의 자동차 생산 대수는 113억 1,000만 대, 캐나다의 자동차 생산 대수는 202만 대에 달했습니다.

미국이 2,000억 달러의 중국 제품에 대한 수입 관세를 인상함으로써 전자 부품 산업은 더욱 영향을 받았습니다.

인덕터, 코어 및 비드 산업 개요

인덕터, 코어 및 비드 시장의 기회로 인해 치열한 경쟁이 벌어지고 있습니다. 시장 점유율을 높이기 위해 경쟁하는 제조업체가 상당수 존재합니다. 시장에서는 더 높은 인덕턴스를 달성하기 위해 크기를 줄이고 코어의 형태를 다양화하는 등 혁신이 증가하고 있습니다.

2019년 9월 : TDK는 열악한 자동차 환경의 까다로운 조건을 충족하는 금속 코어 전력 인덕터를 출시했습니다.

2019년 6월 : TDK는 기존 제품보다 4% 더 높은 전류와 12% 더 낮은 저항을 처리하는 모바일 기기 설계 전용 박막 전력 인덕터를 출시했습니다.

2019년 6월 : Kemet Corporation은 노트북 컴퓨터, 태블릿, 서버 및 HDTV를 비롯한 다양한 상업용 및 소비자용에 사용되는 DC-DC 컨버터의 최신 전력 용도에 적합한 새로운 SMD 금속 복합 전력 인덕터 제품군을 출시했습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

산업의 매력 - Porter's Five Forces 분석

신규 참가업체의 위협

구매자, 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

시장 성장 촉진요인과 시장 성장 억제요인의 도입

시장 성장 촉진요인

시장 성장 억제요인

제5장 시장 세분화

인덕터 유형별

전력 인덕터

다층 칩 인덕터

RF 인덕터

기타 인덕터 유형

재료별

에어 코어

페라이트 코어

세라믹 코어

기타 코어 유형

칩 비드별

다층 비드

페라이트 비드

EMI 비드

최종 사용자 산업별

자동차

컴퓨팅

통신 기기

소비자 가전

기타

지역

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

제6장 경쟁 구도

기업 프로파일

TDK Corporation

Vishay International Inc.

Panasonic Corporation

Murata Manufacturing Co. Ltd.

Taiyo Yuden Co. Ltd.

Kemet Corporation

AVX Corporation

Texas Instruments

TT Electronics Plc

Hefei MyCoil Technology Co., Ltd.

제7장 투자 기회

제8장 시장 기회와 앞으로의 동향

HBR

영문 목차

영문목차

The Inductors, Cores and Beads Market size is estimated at USD 10.51 billion in 2025, and is expected to reach USD 12.73 billion by 2030, at a CAGR of 3.91% during the forecast period (2025-2030).

New product development of SMDs are gaining momentum, centering on small chips for smartphones, modules, and IoT terminals, and high-reliability chips for automotive application.

Key Highlights

The increasing power supply density and efficiency is a challenge for most of the inductor designers. There is a continuous need for reduced size and high-performance power solutions to meet increasingly stringent application requirements.

Globally, the growing demand for consumer electronics, such as smartphones, tablets, portable gaming consoles, laptops, set-top boxes, among others, is the major factor driving the demand for various inductors, core and beads.

The market is also witnessing a boost in demand from applications, which require high reliability, in the industrial, aerospace and defense, and medical sectors.

Inductors Cores & Beads Market Trends

Consumer Electronic to Witness a Significant Market Share

Around 15 percent of a smartphone is made from ceramics and glass that is from electronic applications with circuit boards for thermal management employs cores of passive components like inductors, fuses or resistors.

The Internet of Things and 5G network is expected to boost the overall speed and efficiency of communicating information between devices and networks, IoT, autonomous driving and M2M performances.

Most of consumer electronic products are high-power devices, and the power ranges from hundred to several kilowatts.The amount of magnetic components employed depends on the power of the charging pile. On an average, 20 magnetic components are required in a charging pile, of which the inductor is used in a larger amount.

The challenge remains the large chip area utilisation. For instance, Intel stated that the on-chip inductors used in their DC-DC converters for power management in multi-core processors occupy approximately a quarter of the total available chip area, which made them costly.

North America to Hold a Significant Market Share

The United States witnesses a growing use of inductors in automotive electronics and increasing adoption of smart grid technologies. Due to their various applications, inductors are one of the primary components of many electronic systems. Because of the extensive usage, more inductors are being applied in several industries across North America.

U.S. utilities invested approximately USD 144 billion in electricity generation, transmission, and distribution infrastructure in 2016. According to IEA, U.S. investments in smart grids infrastructure stood at USD 12.6 billion in 2018.

The application of inductors, core and beads find their applications in modern adaptive LED headlights because of their low power consumption and multifunctional adaptability, these are replacing conventional halogen and HID headlights, ADAS, automotive ignition systems, among others.

The Unites States automotive production in 2018 stands at 11.31 billion cars and commercial vehicles and Canada's automotive production at 2.02 miliion cars and commericial vehicles, as per OICA.

The region expects a gradual ease in China-US trade spats after May of 2019, when the United States raised import tariffs on USD 200 billion of Chinese goods, which further affected the electronic component industry.

Inductors Cores & Beads Industry Overview

The inductor, cores and beadsmarket's opportunities have resulted in intense competition. There are a significant number of manufacturers vying for the increasing market share. The market witnesses increased innovation in the form of reduced size and varying the form of cores to achieve higher inductance.

September 2019 - TDK introduced metal-core power inductors tomeet the tough conditions forharsh automotive environments, these conductors have a wide operating temperature range from -55 °C up to +155 °C.

June 2019 -TDK launched a Thin-Film Power Inductor specifically for Mobile Device Design tohandle 4% higher currents and 12% lower resistance than conventional products.

June 2019 - Kemet Corporation launched new range of SMD metal composite power inductors to suit modern power applications inDC-DC converters that are utilized in a variety of commercial and consumer applications including notebook computers, tablets, servers and HDTVs.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Force Analysis