Sensors In Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1641974

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

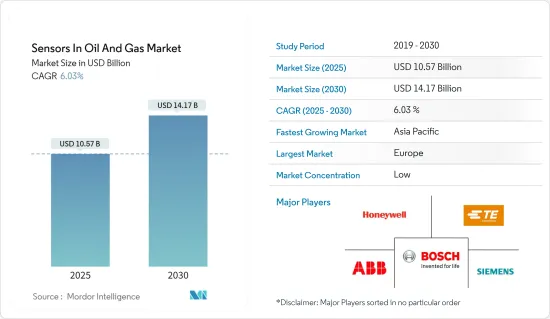

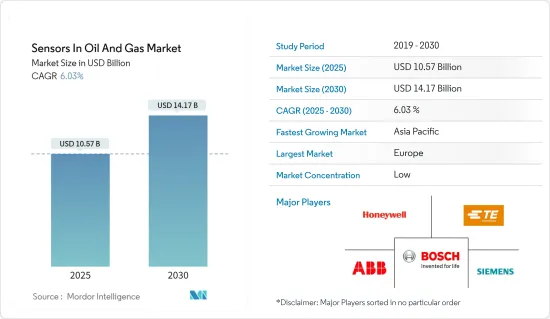

석유 및 가스 센서 시장 규모는 2025년에 105억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 6.03%로, 2030년에는 141억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

세계 경제는 석유 및 가스 산업에 의존하고 있습니다. 석유 및 가스 산업은 세계의 기본 에너지의 대부분을 생산하는 것 외에 살충제, 비료, 의약품, 용제, 폴리머 등 다양한 화학제품의 원료의 중요한 공급원이 되고 있습니다. 석유 및 가스산업의 효율적이고 안정적인 조업에는 제어와 모니터링이 필수적입니다. 생산성 향상, 비용 절감, 수익성 증진 석유 및 가스 산업의 제어 및 모니터링은 센서에 크게 의존합니다.

시장 확대에 영향을 미치는 주요 요인은 기술적 진보에 대한 주력 증가와 정부의 지원 시책입니다. 산업화의 진전과 각종 안전,노동위생규제의 엄격화는 시장 규모를 저하시키고 있습니다. 대기 오염에 대한 의식이 높아지고 소형화된 무선 센서공급 확대로 시장이 성장하고 있습니다. 시장의 급증에 기여하는 또 다른 요소는 마이크로 일렉트로 머신 부문의 확장과 성장입니다.

석유 및 가스 산업에서 IIoT(Industrial Internet of Things) 센서의 채용이 증가하고 있는 것은 주로 비용 절감의 필요성 때문입니다. 센서 제조업체가 최종 사용자에게 제공하는 기술의 발전과 간단한 조립 옵션 덕분에 이러한 센서를 설치하는 데 드는 시간과 비용이 적습니다.

현재의 석유가격환경은 석유 및 가스산업 전체에 큰 변화와 어려운 결정을 촉구하고 있습니다. 단기 및 중기 시장의 수급 역학에 대응하기 위해서는 CAPEX와 OPEX를 개선하는 새로운 운영 모델과 전략이 필요합니다. 안전과 환경 성능을 강화하는 지속 가능한 솔루션에 대한 장기적인 요구는 최우선 과제입니다. 드릴 패드에서 정유소에 이르기까지 센서 용도는 업스트림, 중류, 하류 기술 혁신 및 솔루션 스펙트럼을 통해 운영자가 고유의 균형을 달성하는 데 도움이 됩니다.

센서 제조업체는 조립이 간편한 센서를 제공합니다. 기술이 발전함에 따라 센서의 주요 제조업체와 IoT 제품의 서비스 제공 업체 간의 경쟁이 치열 해지고 있으며 석유 및 가스 산업에서 센서 채택을 추진하고 있습니다.

게다가 석유 및 가스 산업은 숙련 노동자 부족에 시달리고 있습니다. 얕은 인재 풀이 존재하기 때문에 석유 및 가스 회사는 새로운 에너지 원을 다루는 데 필요한 기술 기술을 가진 직원을 고용하는 것이 복잡해졌습니다. 또한 COVID-19 기간 중 원유 가격 상승과 사우디아라비아와 러시아 등 국가 간의 가격 경쟁이 산유 기업의 생산 효율 향상과 이 부문 수요 증가를 촉진할 것으로 예상됩니다.

석유 및 가스용 센서 시장 동향

업스트림 산업이 성장 가능성을 제공

천연가스와 원유는 업스트림부문에서 발견,생산됩니다. 발전, 산업 공정 및 운송은 원유에 크게 의존합니다. 천연가스·원유는 암석층에 의해 지하 깊게 숨겨져 있습니다. 많은 저류층은 수중이나 기후가 엄격하고 도달하기 어려운 곳에 있습니다.

따라서 센서 및 기타 중요한 지진 이미지는 제조업체가 정확한 드릴링 위치 정보를 얻는 데 도움이 됩니다. 이를 통해 드릴링과 관련된 추가 비용을 줄일 수 있습니다. 게다가 석유 및 가스 조달 과정에서의 센서 수요는 합리적인 가격의 센서, 접속성의 확대, 계산 능력의 상승에 의해 견인되고 있습니다. 기기에 내장된 센서가 제공하는 실시간 데이터는 수리 스케줄링 및 일상 업무의 합리화에 있어 기업을 지원합니다.

석유 및 가스 부문의 시스템, 장비 및 센서는 효율성, 생산성, 건강 및 안전성을 높이기 위해 데이터를 통신하고 서로 학습해야 합니다. 따라서 무선 센서 및 개인 모니터링 장치를 사용하면 작업자가 건강에 해로운 유해 물질에 노출되는 시기를 쉽게 식별할 수 있습니다. 그 결과 효과적인 조치를 취할 수 있습니다. 따라서 상기 요인이 예측기간을 통해 석유 및 가스산업의 센서 시장에 호영향을 미칠 것으로 예상됩니다.

BP PLC와 같은 대기업의 업스트림 및 저탄소 에너지 사업 부문은 2022년 894억 4,000만 달러를 창출했습니다. 또한 Abu Dhabi National Oil Company(ADNOC)는 업스트림 메탄 강도 목표를 수정하고 2025년까지 0.15% 달성을 목표로 발표했습니다. 중동에서 가장 낮은 이 새로운 목표는 저탄소 에너지의 윤리적 생산에서 ADNOC의 선구자로서의 지위를 강화하는 것입니다. 메탄 배출 모니터링을 개선하기 위해 ADNOC는 위성 모니터링 및 드론 탑재 센서 등의 실험적 기술도 검토하고 있습니다.

유럽이 큰 시장 점유율을 차지

정부가 공해방지와 에너지 효율 요건에 중점을 두게 되었기 때문에 석유 및 가스용 센서는 독일, 프랑스, 영국을 포함한 유럽 국가에서 널리 사용되고 있습니다. 최종 사용자 인프라의 확장과 가스 센서의 용도 확장은 이 부문 시장 성장을 가속하는 두 가지 요인입니다.

유럽 연합(EU)의 엄격한 배기 가스 규제 요건과 에너지 효율 증진을 위한 정부 활동은 유럽의 대상 시장 확대에 기여하고 있습니다. 이 가스 센서는 동일한 원리로 작동하는 가스 경보기 및 연기 경보기에도 사용됩니다. 또한 소비자의 환경 안전에 대한 의식이 높아져 오염 수준과 휘발성 유기 화합물을 검출하는 공기 모니터링 시스템에 사용되는 상품의 채용 증가로 이어지고 있습니다. 현재 유럽 시장을 독점하고 있는 것은 적외선 센서 유형의 가스용 센서 기술입니다.

유럽의 첨단 석유 및 가스 산업은 센서와 같은 사물인터넷(IoT) 스마트 객체에서 눈을 돌리고, 이러한 객체에서 얻은 데이터를 사용하여 비즈니스 성장에 도움이 되는 보다 지능적인 비즈니스 모델을 구축하기 위한 대담한 전략을 개발하는 것에 다시 주목하고 있습니다.

석유 및 가스 정제 공장은 IoT 센서가 수집한 정보를 사용하여 배송된 석유 유형을 알 수 있습니다. 이를 통해 기업은 제조, 재고 및 운영에 관한 중요한 결정을 내릴 수 있습니다. IoT 센서와 강화된 연결성을 통한 실시간 재고 관리는 유럽의 석유 및 가스 산업을 통해 효율적인 공급망을 제공할 수 있습니다.

또한 노르웨이 경찰은 최근 노르드 스트림 가스 파이프라인의 손상에 대응하고 최근 안전 위반을 조사하기 위해 드론 감지 시스템을 해양 석유 및 가스 시설에 설치했습니다. 센서를 전략적으로 배치함으로써 등록되지 않은 무인 항공기를 감지하고 사용을 방지할 수 있었습니다.

석유 및 가스용 센서 산업 개요

석유 및 가스용 센서 시장은 세분화되어 경쟁이 심합니다. 업스트림, 중류, 하류 등 석유 및 가스 산업의 다양한 활동으로 센서 배치가 조직 수준에서 진행되고 있습니다. 이러한 이유로 진출기업 간의 경쟁 환경이 형성됩니다. Honeywell International Inc., Siemens, ABB 등이 그 예입니다.

2023년 3월, 전자정보기술부는 IoT 센서의 CoE에서 스마트 디지털 온도계, IoT 대응 환경 모니터링 시스템, 다채널 데이터 수집 시스템 등 3개의 IoT 센서 기반 제품 출시를 발표했습니다.

2022년 10월, Honeywell은 지속 가능한 에너지로의 전환을 지원하기 위해 아부다비 국제 석유 전시회 및 회의에서 최신 센서 기술을 전시했습니다. 전시된 기술에는 에너지 저장 시스템, 배출 가스 모니터링 시스템, 이 사업의 첨단 플라스틱 재활용 기술, 작업자 안전 솔루션 포트폴리오, 탄소 회수 및 수소 생성 기술이 포함됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

시장 성장 촉진요인

석유 및 가스 산업에 있어서의 안전 시스템 수요의 고조

무선 센서 부문의 간소화된 네트워크 아키텍처에 대한 요구 증가

시장 성장 억제요인

석유 및 가스 시추 활동에 부과되는 엄격한 규제

제6장 시장 세분화

센서 유형별

가스용 센서

온도 센서

초음파 센서

압력 센서

유량 센서

레벨 센서

기타 센서 유형

접속성별

유선

무선

활동별

업스트림

중류

하류

지역별

북미

미국

캐나다

유럽

영국

독일

기타 유럽

아시아태평양

중국

인도

인도네시아

기타 아시아태평양

라틴아메리카

멕시코

브라질

아르헨티나

기타 라틴아메리카

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

중동 및 아프리카의 나머지 지역

제7장 경쟁 구도

기업 프로파일

Honeywell International Inc.

TE Connectivity Ltd.

Robert Bosch GmbH

ABB Ltd.

Siemens AG

Rockwell Automation Inc.

Analog Devices Inc.

Emerson Electric Company

GE Sensing & Inspection Technologies GmbH

SKF AB

제8장 투자 분석

제9장 시장의 미래

SHW

영문 목차

영문목차

The Sensors In Oil And Gas Market size is estimated at USD 10.57 billion in 2025, and is expected to reach USD 14.17 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

Key Highlights

The global economy depends on the oil and gas industry. In addition to producing most of the world's basic energy, the oil and gas sector also serves as a substantial source of raw materials for various chemical goods, such as insecticides, fertilizers, medicines, solvents, and polymers. Control and monitoring are crucial for efficient and stable oil and gas industry operations. It improves productivity, cuts costs, and promotes profitability. The control and monitoring of the oil and gas industry depend heavily on sensors.

The primary factors influencing market expansion are a greater focus on technical advancement and supportive governmental policies. Growing industrialization and stricter enforcement of various safety and occupational health regulations reduce market value. The market will grow due to increased awareness of air pollution and the growing supply of miniaturized wireless sensors. Another element contributing to the surge of the market is the expansion and growth of the micro-electromechanical sector.

The rising adoption of IIoT (Industrial Internet of Things) sensors in the oil and gas industry is mainly driven by the need to reduce costs. The installation of these sensors takes less time and costs less, owing to technological advancements and easy assembling options that sensor manufacturers offer to end users.

The current oil price environment is driving significant changes and difficult decisions across the oil and gas industry. New operating models and strategies that improve CAPEX and OPEX are required to respond to short- and mid-term market supply and demand dynamics. The long-term requirement for sustainable solutions that reinforce safety and environmental performance is a topmost priority. From drill pad to refinery, the application of sensors helps operators achieve a unique balance through a spectrum of upstream, midstream, and downstream technological innovations and solutions.

Sensor manufacturers are increasingly offering sensors designed with easy assembling options. Owing to technical advancements, the competition among significant manufacturers of sensors and service providers of IoT products is intensifying, thereby boosting the adoption of these in the oil and gas industry.

Additionally, the oil and gas industry suffers from a skilled labor shortage. The presence of a shallow talent pool has made it complicated for oil and gas companies to hire new employees who possess the technical skills that are required to work on new energy sources. Moreover, stress with the oil prices during COVID-19 and the price war between countries such as Saudi Arabia and Russia was expected to drive oil-producing companies to enhance their production efficiency and increase the demand in the sector.

Oil & Gas Sensors Market Trends

Upstream Industries Offer Potential Growth

Natural gas and crude oil are discovered and produced in the upstream sector. Electricity generation, industrial processes, and transportation heavily rely on crude oil. Rock layers hide the deep subterranean locations of natural gas and crude oil. Many reservoirs are located underwater or in hard-to-reach places with harsh climates.

As a result, sensors and other important seismic images assist manufacturers in obtaining precise drilling location information. This aids them in cutting down on the additional expenses related to drilling. In addition, the demand for sensors during the oil and gas procurement process is driven by affordable sensors, expanding connectivity, and rising computational power. Real-time data provided by sensors built into equipment assist businesses in scheduling repairs and streamlining daily operations.

The oil and gas sector's systems, equipment, and sensors must communicate data and learn from one another to enhance efficiency, productivity, health, and safety. Therefore, it will be simple to identify when workers are exposed to unhealthy hazardous substances with the aid of wireless sensors and personal monitoring devices. Consequently, effective steps can be taken. Therefore, it is anticipated that the abovementioned factors will favorably affect the oil and gas industry's sensors market throughout the forecast period.

The upstream and low carbon energy business segment of major firms such as BP PLC generated USD 89.44 billion in 2022. Moreover, the Abu Dhabi National Oil Company (ADNOC) announced that it revised its upstream methane intensity objective and aims to achieve 0.15 percent by 2025. The new goal, the lowest in the Middle East, strengthens ADNOC's position as a pioneer in the ethical production of low-carbon energy. To improve the monitoring of methane emissions, ADNOC is also looking into experimental technologies, including satellite monitoring and drone-mounted sensors.

Europe Holds a Significant Market Share

Due to governments' increased focus on pollution control and energy efficiency requirements, oil and gas sensors have become more common in European countries, including Germany, France, and the United Kingdom. An expanding end-user base and expanded applications for gas sensors are two factors that would fuel market growth in this sector.

The strict emission control requirements and government activities in the European Union to promote energy efficiency are credited with expanding the target market in Europe. These gas sensors are also used in gas or smoke alarms, which operate on the same principles. Additionally, consumers' growing awareness of environmental safety is driven by the increased adoption of goods used in air monitoring systems to detect pollution levels and volatile organic compounds. The infrared sensors type of gas sensor technology currently rules the European market.

The more forward-thinking oil and gas industry in Europe is refocusing its attention away from the Internet of Things (IoT) smart objects like sensors and other devices and toward developing audacious strategies for using the data obtained from these objects to build more intelligent business models that help their business grow.

Oil and gas refineries can be informed about the sorts of oil that have been delivered using the information gathered by IoT sensors. This allows businesses to decide on crucial manufacturing, inventory, and operational decisions. Real-time inventory management with IoT sensors and enhanced connectivity can provide a more efficient supply chain for the European oil and gas industry.

Moreover, the Norwegian police put drone detection systems on offshore oil and gas facilities to investigate recent safety violations in reaction to recent damage to the Nord Stream gas pipelines. Strategic placement of the sensors allowed for the detection of unregistered drones and the prevention of their use.

Oil & Gas Sensors Industry Overview

The oil and gas sensors market is fragmented and competitive. The deployment of sensors at different oil and gas industry activities, such as upstream, midstream, and downstream, is growing at an organizational level. This creates a competitive environment among the players. Some players are Honeywell International Inc., Siemens AG, and ABB Ltd.

In March 2023, The Ministry of Electronics and Information Technology announced the launch of three IoT sensor-based products, which include a Smart Digital Thermometer, IoT Enabled Environmental Monitoring System, and a Multichannel Data Acquisition System in the CoE in IoT Sensors.

In October 2022, Honeywell displayed its latest sensor technologies at the Abu Dhabi International Petroleum Exhibition and Conference to help the transition to sustainable energy. The technologies displayed included energy storage systems, emission monitoring systems, the business's advanced plastics recycling technology, its portfolio of worker safety solutions, and carbon capture and hydrogen generation technologies.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand for Safety Systems in the Oil and Gas Industry

5.1.2 Increasing Need for a Simplified Network Architecture in the Wireless Sensor Segment

5.2 Market Restraints

5.2.1 Rigid Regulations Imposed on Oil and Gas Drilling Activities