ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

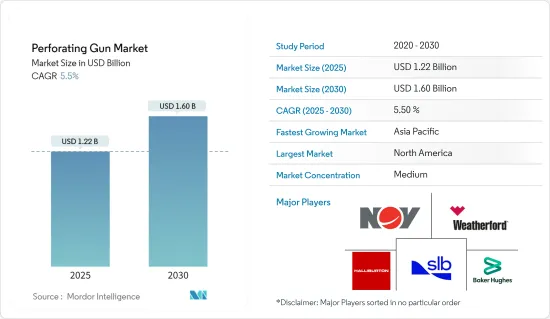

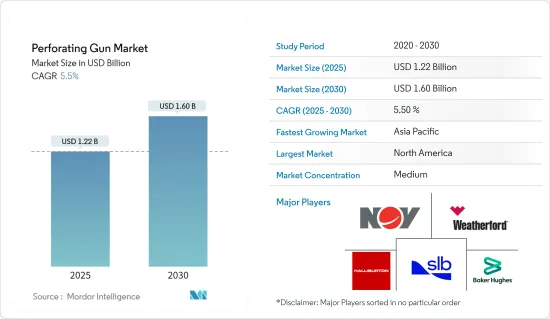

천공 건 시장 규모는 2025년에 12억 2,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.5%로, 2030년에는 16억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 세계의 석유 및 가스 드릴링 활동의 활성화, 셰일 가스 탐사 증가, 천공 암 시스템의 기술 개발 등의 요인이 예측 기간 중의 천공 건 시장을 견인할 것으로 예상됩니다.

한편, 재생가능에너지는 향후 수십년 동안 그 점유율을 확대하여 세계 전력의 50%에 기여할 가능성이 높습니다. 앞으로 몇 년동안 재생 가능 에너지가 천공 건 시장을 억제할 것으로 예상됩니다.

새로운 비전통적인 갱정의 발견은 천공 건 시장에 기회를 제공할 것으로 예상됩니다.

북미는 천공 건의 최대 시장 중 하나이며, 주로 타이트 오일과 셰일의 매장량에 있어서의 탐사와 생산 활동 증가에 의해 미국이 주도하고 있습니다.

천공 건 시장 동향

수평 갱정과 편위 갱정 부문이 시장을 독점

수평 및 편위 갱정 개발은 그 이점과 경제성의 향상으로 이어진 기술의 진보에 의해 인기를 모으고 있습니다.

갱정에 대한 접근성을 향상시키고 저류층에 대한 효율적인 자극을 보장하는 천공 암의 효과는이 부문에서 인기를 끌고 있습니다. 비전통적인 자원의 지속적인 성장과 수평 드릴링 기술에 대한 선호도가 증가함에 따라, 수평 및 편위 갱정 부문은 천공 건 시장의 지속적인 확장으로의 궤도를 조타하는 주요 추진력이 될 것으로 예상됩니다.

멀티 라테랄 갱이의 보급이 진행됨에 따라, 해안 지역에서의 수평 드릴링 수요가 높아져, 결과적으로 시장을 이끌고 있습니다. 지속적인 기술의 진보와 수평 드릴링의 효율성 향상은 다단 수압 파쇄 기술의 진보와 더불어 비전통적인 셰일과 치밀 탄화수소의 매장량을 대폭 개발할 수 있게 하고 있습니다. 이 동향은 에너지 탐사 및 생산의 진화에 수반하는 시장 역학의 주목할만한 변화를 반영하고 있습니다.

또한 2023년 8월, Arabian Drilling Company는 Saudi Aramco로부터 사우디아라비아의 비재래형 가스 프로그램 대신 10개의 육상 리그를 추가하는 5년 계약을 여러 차례 획득했습니다. Saudi Aramco는 또한 북아라비아, 남부 가와르, 재프라 등의 지역에서 새로운 비재래형 매장량에 접근하기 위한 검사 프로젝트의 실시와 필요한 인프라의 설치를 검토하고 있습니다. 이 때문에 천공 건 시장의 향후 성장이 기대됩니다.

또한 아랍에미리트(UAE), 이집트, 카타르, 알제리, 리비아, 사우디아라비아와 같은 국가들이 셰일 매장량의 상업적 가능성을 탐구하기 시작했습니다. 2023년 8월, 이집트의 석유 및 광물자원성은 2024년과 2025년 사이에 35개의 신규 천연가스 드릴링 활동이 예정되어 있으며, 생산율 향상을 위해 15억 달러 이상이 투자될 것으로 추정 및 예측했습니다.

2022년 중동의 석유 생산량은 14억 4,160만 톤으로 2021년 13억 1,600만 톤에서 증가하여 9.5% 이상의 성장률을 기록했습니다.

따라서 수평 굴착에 의한 셰일 오일 및 가스의 탐사,생산 증가에 따라 천공 건 시장도 큰 수요가 예상됩니다. 따라서 위에서 언급한 요인들로 인해 수평 및 경사 시추 부문은 예측 기간 동안 지배적인 성장을 보일 것입니다.

시장을 독점하는 북미

석유 및 가스 수요가 높아지는 가운데, 북미에서의 굴착 활동이 활발해지고 있습니다. 수직 갱정에서 수평 갱정으로의 전환은 이 지역에서 지난 10년간의 가장 중요한 변화이며, 갱정의 비용을 조금씩 증가시키는 반면, 지층에 대한 접근을 확대할 수 있게 되었습니다. 굴착 활동의 급증은 북미 석유 및 가스 시장에 낙관적인 견해를 가져오고, 따라서 천공 암 시장에 있어서는 좋은 징후라고 생각됩니다.

그러나 이 시나리오는 2023년 최근 몇 개월 만에 회복을 보였습니다. 예를 들어, Baker Hughes Rig Count에 따르면 2023년 6월 9일 현재 미국에서는 695기의 로터리 리그가 가동하고 있으며, 그 중 20기가 오프쇼어 리그, 675기가 온쇼어 리그였습니다. 2022년 말 가동 리그 수가 15기였던 것에 비해 해외 리그 수는 증가하고 있습니다. 이러한 동향은 앞으로도 계속되어 이 나라의 해양 석유 및 가스 시추 시장의 성장을 지지할 것으로 예상됩니다. 마찬가지로 2022년 방향성 회전식 드릴링 리그의 수는 46기로 2021년 30기에서 증가했습니다.

2023년 3월 미국 정부는 알래스카의 윌로우 석유 프로젝트의 드릴링 활동을 승인했습니다. 윌로우 프로젝트에서는 피크시에 하루 약 18만 배럴의 원유 생산이 예상되며, 이는 알래스카의 기존 닛산량의 거의 40%에 해당합니다.

또한 멕시코만에서도 새로운 프로젝트가 시작되어 회복의 조짐이 보이기 시작하고 있습니다. 멕시코만에서의 쉘오프쇼어에 의한 Vito와 같은 심해,초심해 드릴링 활동에 대한 지속적인 석유 및 가스 투자는 이 나라의 천공 건 시장에 새로운 길을 열 것으로 기대되고 있습니다.

따라서 북미 생산은 현저하게 발전하고 있으며, 이 지역에서 성장하는 셰일 산업은 천공 건 시장에 종사하는 유전 서비스 제공업체에게 큰 기회를 창출할 것으로 예상됩니다.

천공 건 산업 개요

천공 건 시장은 반쯤 분열 상태입니다. 주요 기업(특정 순서 없음)에는 Baker Hughes Company, Schlumberger Limited, Weatherford International PLC, NOV Inc., Halliburton Company 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위: 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

석유 및 가스 드릴링 활동과 관련 투자 증가

천공 건 시스템의 기술 개발

억제요인

증가하는 에너지 수요를 충족시키기 위한 재생 가능 에너지 기술에 대한 주목 증가

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 세분화

캐리어 유형

중공 캐리어

확대형 충전 건

기타 캐리어 유형

폭약 유형

시클로트리메틸렌,트리니트라민(RDX)

시클로테트라메틸렌트리니트라민(HMX)

헥사니트로실벤(HNS)

갱정 유형

수평 갱정과 편위 갱정

수직 갱정

지역

북미

미국

캐나다

기타 북미

유럽

노르웨이

영국

러시아

기타 유럽

아시아태평양

중국

인도

인도

말레이시아

기타 아시아태평양

남미

칠레

브라질

아르헨티나

남아프리카

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

이집트

나이지리아

중동 및 아프리카의 나머지 지역

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Baker Hughes Company

Schlumberger Limited

Weatherford International PLC

NOV Inc.

Halliburton Company

Hunting PLC

DMC Global Inc.

DynaEnergetics GmbH & Co KG

China Shaanxi FYPE Rigid Machinery Co. Ltd

Core Laboratories NV

시장 랭킹/공유(%) 분석

제7장 시장 기회와 앞으로의 동향

비재래형 저류층의 개발

SHW

영문 목차

영문목차

The Perforating Gun Market size is estimated at USD 1.22 billion in 2025, and is expected to reach USD 1.60 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Key Highlights

Over the medium term factors such as the rise in oil and gas drilling activities across the world, increased shale gas exploration, and technological developments in perforating gun systems are expected to drive the perforating gun market during the forecast period.

On the other hand, renewable energy is likely to increase its share and contribute to 50% of global power in the next few decades. It is expected to restrain the perforating gun market in the coming years.

Nevertheless, the discovery of new unconventional wells is expected to provide opportunities for the perforation gun market.

North America is one of the largest markets for perforating guns, led by the United States mainly due to increased exploration and production activities in its tight oil and shale reserves.

Perforating Gun Market Trends

Horizontal and Deviated Well Segment to Dominate the Market

The horizontal and deviated well development is gaining popularity, owing to the benefits associated with the same and technological advancements that have led to increased economic viability.

The effectiveness of perforating guns in enhancing wellbore access and ensuring efficient reservoir stimulation has fueled their popularity in this segment. With the continuous growth of unconventional resources and the increasing preference for horizontal drilling techniques, the horizontal and deviated well segment is anticipated to be a key driver, steering the trajectory of the perforating gun market toward sustained expansion.

The rising prevalence of multilateral wells is fostering an increased demand for horizontal drilling in offshore areas, consequently propelling the market forward. Continuous technological advancements and enhanced efficiency in horizontal drilling, coupled with advancements in multi-stage hydraulic fracturing technologies, are unlocking extensive reserves of unconventional shale and tight hydrocarbons. This trend reflects a notable shift in the market dynamics, driven by the evolving landscape of energy exploration and production.

Moreover, in August 2023, the Arabian Drilling Company received multiple contracts of five- years from Saudi Aramco for ten additional land rigs instead of the unconventional gas program in Saudi Arabia. Saudi Aramco is also investigating conducting trial projects and setting up the required infrastructure to access new unconventional reserves in regions such as North Arabia, South Ghawar, and Jafurah. This is expected to help the perforating gun market to grow in the future.

Also, countries such as the United Arab Emirates, Egypt, Qatar, Algeria, Libya, and Saudi Arabia have started exploring the commercial viability of their shale reserves. In August 2023, the Ministry of Petroleum and Mineral Resources of Egypt noted forthcoming drilling activities for 35 new natural gas wells during 2024 & 2025 with estimated investments of over USD 1.5 billion to increase production rates, thus benefitting the perforating gun market in the forecast period.

As per the Statistical Review of World Energy, in 2022, the oil production in the Middle-Eastern region stood at 1,441.6 million tonnes, an increase from 1,316 million tonnes in 2021, registering a growth rate of more than 9.5%.

Hence, with the rising exploration and production of shale oil and gas through horizontal drilling, the perforating gun market is also expected to witness a significant

demand. Therefore, the horizontal and deviated healthy segment will witness dominant growth during the forecast period due to the above points.

North America to Dominate the Market

Drilling activities in North America have increased amid the rising oil and gas demand. The shift from vertical to horizontal wells is the most significant change over the last decade in the region, allowing for greater formation access while only incrementally increasing the cost of the well. The surge in drilling activities has created optimism in the North American oil and gas market and hence may be considered a good sign for perforating gun markets.

However, this scenario saw a recovery in the recent months of 2023. For example, according to the Baker Hughes Rig Count, on 9th June 2023, the United States had 695 active rotary rigs, of which 20 were offshore rigs and 675 onshore rigs. This recorded a rise in the offshore rig counts compared to the 15 active rigs at the end of 2022. These trends will likely continue and support the growth of the country's offshore oil and gas drilling market. Likewise, the directional rotary drilling rig count in 2022 was 46, which increased from 30 counts in 2021.

In March 2023, the United States government approved drilling activities on the Willow oil project in Alaska. The Willow project is expected to garner peak production of about 180,000 barrels of oil per day, nearly forty percent of existing daily production in Alaska.

Also, the Gulf of Mexico has started to witness signs of recovery as new projects are coming up. Ongoing oil and gas investments in deepwater and ultra-deepwater drilling activities, such as one by Shell Offshore for Vito in the Gulf of Mexico, are expected to create new avenues for the perforating gun market in the country.

Therefore, North American production has developed significantly, and the growing shale industry in the region is expected to create significant opportunities for the oilfield service providers engaged in the perforating gun market.

Perforating Gun Industry Overview

The perforating gun market is semi-fragmented. Some of the major companies (in no particular order) are Baker Hughes Company, Schlumberger Limited, Weatherford International PLC, NOV Inc., and Halliburton Company.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Rise In Oil And Gas Drilling Activities And Associated Investments

4.5.1.2 Technological Developments In Perforating Gun Systems

4.5.2 Restraints

4.5.2.1 Increased Focus On Renewable Energy Technologies To Fulfill Rising Energy Demand

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Carrier Type

5.1.1 Hollow Carrier

5.1.2 Expandable Shaped Charged Gun

5.1.3 Other Carrier Types

5.2 Explosive Type

5.2.1 Cyclotrimethylene Trinitramine (RDX)

5.2.2 Cyclotetramethylene Trinitramine (HMX)

5.2.3 Hexanitrosilbene (HNS)

5.3 Well Type

5.3.1 Horizontal and Deviated Well

5.3.2 Vertical Well

5.4 Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Rest of North America

5.4.2 Europe

5.4.2.1 Norway

5.4.2.2 United Kingdom

5.4.2.3 Russia

5.4.2.4 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 China

5.4.3.2 India

5.4.3.3 Indoensia

5.4.3.4 Malaysia

5.4.3.5 Rest of Asia-Pacific

5.4.4 South America

5.4.4.1 Chile

5.4.4.2 Brazil

5.4.4.3 Argentina

5.4.4.4 Rest of South Africa

5.4.5 Middle East & Africa

5.4.5.1 United Arab Emirates

5.4.5.2 Saudi Arabia

5.4.5.3 South Afica

5.4.5.4 Egypt

5.4.5.5 Nigeria

5.4.5.6 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements