Primer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1641865

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

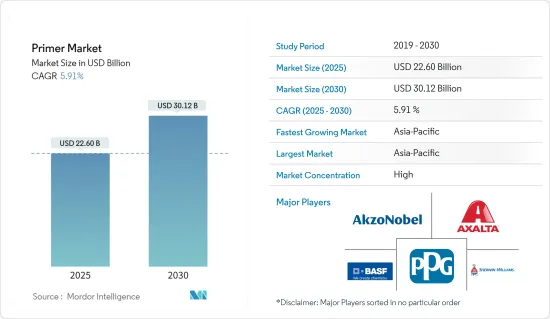

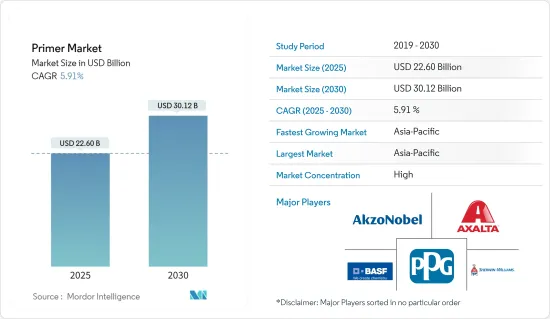

프라이머 시장 규모는 2025년에 226억 달러로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 5.91%로, 2030년에는 301억 2,000만 달러에 달할 것으로 예상됩니다.

COVID-19 팬데믹은 새로운 COVID-19 감염자의 확대를 억제하기 위해 건설 및 자동차 제조 활동이 일시적으로 중단되어 이러한 최종 사용자 산업에서 프라이머 소비가 감소하여 시장에 부정적인 영향을 미쳤습니다. 그러나 이 상황은 2021년에 회복하기 시작했습니다. 이러한 이유로 예측 기간 동안 이 제품 수요가 증가할 것으로 예상됩니다.

주요 하이라이트

단기적으로는 아시아태평양의 건설 활동 증가와 자동차 산업 성장이 시장 성장을 견인할 것으로 보입니다.

반면, 프라이머 사용에 관한 규제가 시장 성장을 방해할 가능성이 높습니다.

바이오 프라이머 사용의 혁신은 시장 성장 기회로 작용할 것으로 예상됩니다.

아시아태평양은 세계에서 가장 큰 시장으로 인도, 중국 및 기타 국가들에서의 수요와 소비가 가장 많아 세계 시장을 독점할 것으로 예상됩니다.

프라이머 시장 동향

건축 및 건설 부문이 시장을 독점

프라이머는 건축 및 건설 부문에서 널리 사용됩니다. 페인트를 칠하기 전에 벽이나 기타 기초에 예비 코팅으로 사용됩니다.

프라이머는 언더코트나 탑코트를 도포하기 전에 새로운 표면이나 낡은 표면에 도포되는 안료 도료입니다. 건설 산업의 성장은 페인트 및 코팅제 수요 증가에 큰 역할을 합니다. 건설 활동의 수가 많을수록 페인트 및 코팅제에 대한 수요도 늘어나고 결국 프라이머 시장을 밀어 올릴 것입니다.

건축 및 건설산업은 인구 증가, 신도시 개발, 도시지역 이민 증가, 기성도시 노후 인프라 갱신 등 요인에 따라 지난 수년간 성장을 이어가고 있으며, 2030년에는 4조 4,000억 달러의 매출에 이를 것으로 예상되고 있습니다.

북미 건설 산업에서는 미국이 큰 점유율을 차지하고 있습니다. 미국, 캐나다, 멕시코도 건설 부문 투자에 크게 기여하고 있습니다.

미국 인구조사국에 따르면 2023년 미국의 연간 건설액은 1조 9,787억 달러로 2022년 대비 약 7.03 증가했습니다.

아시아태평양 건설 부문은 세계 최대입니다. 인구 증가, 중간 소득층 증가, 도시화로 견실한 성장률을 보여줍니다.

중국과 인도의 주택 건설 시장 확대로 아시아태평양에서 가장 높은 성장이 예상됩니다. 이 나라들은 2030년까지 세계 중간층의 43.3% 이상을 차지할 것으로 예상됩니다.

따라서 위의 요인은 향후 몇 년 동안 시장에 큰 영향을 미칠 것으로 예상됩니다.

아시아태평양이 시장을 독점

예측 기간 동안 아시아태평양이 최대 성장을 이룰 것으로 예상됩니다. 이는 이 지역의 건설 산업과 자동차 생산이 증가하고 있기 때문입니다.

아시아태평양에는 인도, 중국, 인도네시아, 베트남과 같은 신흥 경제국이 많이 있습니다. 따라서 투자자들이 관심을 보이는 시장입니다.

2030년까지 세계 건설 시장은 8조 달러 규모에 이를 것으로 예상됩니다. 인도, 중국, 미국 등의 국가들이 이 성장의 대부분을 견인할 것으로 예상되고 있습니다.

중국은 건설 붐이 일고 있습니다. 이 나라는 세계 최대의 건축 시장을 보유하고 있으며, 세계 건설 투자 전체의 20%를 차지하고 있습니다. 2030년까지 중국에서만 약 13조 달러의 건축 투자가 예상됩니다.

중국국가통계국에 따르면 2023년 중국 건설산업의 총생산액은 1.99% 증가하여 71조 2,847억 2,000만 위안(10조 867억 8,000만 달러)을 차지합니다.

또한 인도에서는 주택 부문이 성장하고 있으며 정부의 지원과 이니셔티브가 수요를 더욱 밀어 올리고 있습니다. 2022년부터 2023년까지의 예산으로 주택도시개발부(MoHUA)는 주택건설과 정지중의 프로젝트를 완료하기 위한 자금 만들기에 약 98억 5,000만 달러를 할당했습니다.

건설 산업과 함께 자동차 산업도 이 지역의 주요 산업이며 프라이머의 큰 수요에 기여하고 있습니다.

아시아태평양은 세계에서 가장 가치있는 자동차 제조 업체의 본거지입니다. 중국, 인도, 일본, 한국 등의 국가들은 수익성을 높이기 위해 제조 거점 강화와 효율적인 공급망 개발에 주력하고 있습니다.

중국 기차공업협회(CAAM)에 따르면 중국은 세계에서 가장 중요한 자동차 생산 거점이며, 2023년의 자동차 총 생산 대수는 3,016만대로, 작년의 2,702만대에 비해 11.6% 증가를 기록합니다. 국제무역국(ITA)에 따르면 국내 자동차 생산량은 2025년까지 3,500만대에 달할 것으로 예상됩니다.

게다가 인도의 자동차산업은 세계 5위이며 2030년에는 3위가 될 것으로 예측됩니다. 국제자동차건설기구(OICA)에 따르면 2023년 인도 자동차 생산량은 약 7% 증가하여 585만대가 되었습니다.

위의 요인은 향후 몇 년 동안 시장에 큰 영향을 미칠 것으로 예상됩니다.

프라이머 산업 개요

프라이머 시장은 통합된 특성을 가지고 있습니다. 주요 기업에는 AkzoNobel NV, The Sherwin-Williams Company, Axalta Coating Systems LLC, PPG Industries Inc., BASF SE 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

아시아태평양의 건설 활동 증가

성장하는 자동차 산업

기타 촉진요인

성장 억제요인

프라이머의 사용에 관한 엄격한 환경 규제

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

구성 요소별

수지

아크릴

에폭시 수지

폴리아세트산비닐

알키드

기타 수지(말레산, 폴리에스테르, 폴리아미드 등)

첨가제별

분산제

살생물제

표면 개질제

기타 첨가제(방청제, 염해 방지제, 유화제, 안정제 등)

기타 성분(용제, 안료 등)

최종 사용자 산업별

자동차

건축 및 건설

가구

공업용

포장

기타 최종 사용자 산업(금속 가공, 플라스틱, 고무)

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

노르딕

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

나이지리아

카타르

이집트

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

인수합병, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

AkzoNobel NV

Asian Paints

Axalta Coating Systems LLC

BASF SE

Berger Paints India Limited

Hempel A/S

Jotun

Kansai Paint Co. Ltd

Masco Corporation

NIPSEA Group

PPG Industries Inc.

RPM International Inc.

The Sherwin-Williams Company

Tikkurila

제7장 시장 기회와 앞으로의 동향

친환경 기반 프라이머의 혁신

기타 기회

KTH

영문 목차

영문목차

The Primer Market size is estimated at USD 22.60 billion in 2025, and is expected to reach USD 30.12 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market as construction and automotive manufacturing activities were temporarily halted to reduce the spread of new COVID-19 cases, thereby decreasing the consumption of primer in these end-user industries. However, the condition started recovering in 2021. This is expected to increase the demand for the product during the forecast period.

Key Highlights

Over the short term, the growth of the market is likely driven by increasing construction activities in Asia-Pacific and the growing automotive industry.

On the flip side, regulations regarding the use of primers are likely to hinder market growth.

Innovations in the use of bio-based primers are expected to act as opportunities for market growth.

Asia-Pacific is the largest market in the world and is expected to dominate the global market, with the highest demand and consumption from India, China, and other countries.

Primer Market Trends

Building and Construction Segment to Dominate the Market

Primer is extensively used in the building and construction sectors. It is used as a preparatory coat on walls and other substrates before applying the paint.

Primers are pigmented coatings that are applied to new or old surfaces prior to the application of undercoats or topcoats. The growing construction industry plays a keen role in the increasing demand for paints and coatings. The greater the increase in the number of construction activities, the greater the demand for paints and coatings, which will eventually boost the market for primers.

The building and construction industry has been growing for the past few years, owing to factors such as increasing population, development of new cities, growing migration in urban areas, renewal of old infrastructure in established cities, and others, and it is expected to reach a revenue of USD 4.4 trillion by 2030.

The United States includes a significant share of the construction industry in North America. The United States, Canada, and Mexico also contribute significantly to the construction sector investments.

According to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which was an increase of about 7.03 compared to 2022.

The construction sector in Asia-Pacific is the largest in the world. It is growing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization.

The highest growth for housing is expected to be registered in Asia-Pacific, owing to the expanding housing construction markets in China and India. These countries are expected to represent over 43.3% of the global middle class by 2030.

Therefore, the factors mentioned above are expected to have a significant impact on the market in the coming years.

Asia-Pacific to Dominate the Market

During the forecast period, Asia-Pacific is expected to witness the maximum growth. This is because the construction industry and automotive production in the region are growing.

Asia-Pacific has a lot of countries with emerging economies, like India, China, Indonesia, and Vietnam. This has made it a market that investors are interested in.

By 2030, the global construction market is expected to be worth USD 8 trillion. Countries like India, China, and the United States are expected to drive most of this growth.

China is amid a construction boom. The country has the world's largest building market, accounting for 20% of all construction investment globally. The country alone is expected to spend nearly USD 13 trillion on buildings by 2030.

According to the National Bureau of Statistics of China, the gross output value of the construction industry in China in 2023 increased by 1.99%, accounting for CNY 71,284.72 billion (USD 10,086.78 billion).

In addition, the residential sector in India is growing, and government support and initiatives are further boosting demand. In the budget of 2022-2023, the Ministry of Housing and Urban Development (MoHUA) allocated about USD 9.85 billion to construct houses and create funds to complete the halted projects.

Along with the construction industry, the automotive industry is another major industry in the region contributing to significant demand for primers.

Asia-Pacific is home to some of the world's most valuable vehicle manufacturers. Countries like China, India, Japan, and South Korea have been working hard to strengthen their manufacturing bases and develop efficient supply chains for greater profitability.

According to the China Association of Automobile Manufacturers (CAAM), China has the most significant automotive production base in the world, with a total vehicle production of 30.16 million units in 2023, registering an increase of 11.6% compared to 27.02 million units produced last year. As per the International Trade Administration (ITA), domestic automotive production is expected to reach 35 million units by 2025.

Further, the Indian automotive industry is the fifth largest in the world and is projected to become the third largest by 2030. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), Indian automotive production in 2023 increased by about 7% and was valued at 5.85 million units.

The above factors are likely to have a significant effect on the market in the coming years.

Primer Industry Overview

The primer market is consolidated in nature. The major players (not in any particular order) include AkzoNobel NV, The Sherwin-Williams Company, Axalta Coating Systems LLC, PPG Industries Inc., and BASF SE.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Construction Activities in the Asia-Pacific Region

4.1.2 Growing Automotive Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stringent Environmental Regulations Regarding the Use of Primers

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Ingredient

5.1.1 Resin

5.1.1.1 Acrylic

5.1.1.2 Epoxy

5.1.1.3 Poly Vinyl Acetate

5.1.1.4 Alkyd

5.1.1.5 Other Resins (Maleic, Polyester, Polyamide, etc.)

5.1.2 By Additives

5.1.2.1 Dispersant

5.1.2.2 Biocides

5.1.2.3 Surface Modifier

5.1.2.4 Other Additives (Rust Inhibitors, Salt Inhibitors, Emulsifiers, Stabilizers, etc)

5.1.3 Other Ingredients (Solvent, Pigments, etc.)

5.2 By End-user Industry

5.2.1 Automotive

5.2.2 Building and Construction

5.2.3 Furniture

5.2.4 Industrial

5.2.5 Packaging

5.2.6 Other End-user Industries (Metalworking, Plastic, and Rubber)

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 NORDIC

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Nigeria

5.3.5.4 Qatar

5.3.5.5 Egypt

5.3.5.6 United Arab Emirates

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements