ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

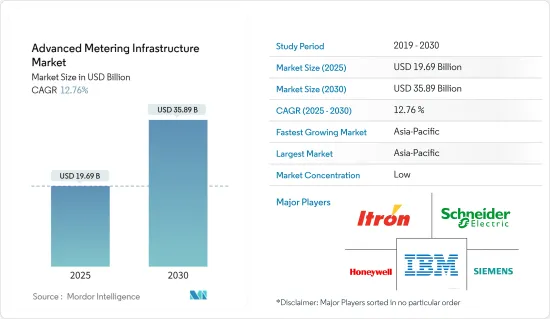

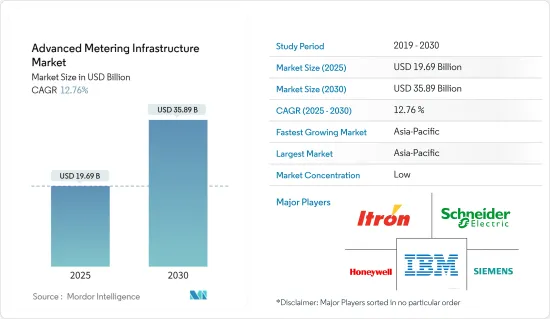

지능형 검침 인프라 시장 규모는 2025년에 196억 9,000만 달러로 추정됩니다. 2030년에는 358억 9,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 12.76%입니다.

스마트 미터는 유틸리티 업계에 변화를 가져오는 기술입니다. 이러한 기술적으로 진보된 미터는 에너지 사용에 대한 더 깊은 인사이트를 제공합니다. 스마트 미터는 세계 지능형 검침 인프라 개발의 일환으로 채택되었습니다.

주요 하이라이트

통합되고 IT화된 전력망과 그 패턴을 분석하는 다른 지원 소프트웨어를 개발하는 것은 사용자에게 큰 이점을 제공합니다. 스마트 그리드라고 불리는 이러한 그리드는 분산 생산의 확대를 지원하고 비용을 낮추고 에너지 효율을 촉진하며 생산, 변속기, 배전 시스템 전체의 신뢰성과 안전성을 향상시킵니다. AMI는 스마트 그리드 개념에 필수적인 요소입니다. 정부기관과 전력회사는 보다 큰 '스마트 그리드' 개념의 일환으로 AMI 시스템에 주목하고 있습니다.

유럽위원회의 조사에 따르면 EU에서는 2024년까지 전력용으로 약 2억 2,500만개, 가스용으로 약 5,100만개의 스마트 미터가 설치될 예정입니다. 2024년까지 유럽 소비자의 44%가 스마트 가스 미터를, 77%가 스마트 전기 미터를 가질 것으로 예상됩니다.

한편, COVID-19의 유행은 시장 성장에 긍정적인 영향을 미쳤습니다. 왜냐하면 에너지 및 유틸리티 부서는 업무 수행 방법과 직원 및 고객과의 관계를 재검토해야 하는 필수적인 서비스를 제공하기 때문입니다. COVID-19의 대유행은 다른 거의 모든 측면에 영향을 미쳤지만, 안전한 송전망을 유지할 필요성은 유틸리티자에게 여전히 우선권의 최전선에 있습니다. AMI는 유행 기간 동안 전력 회사가 수익 흐름을 유지하고 다양한 원격 근무을 관리하는 데 도움이되었습니다.

전력 인프라를 확대, 근대화, 분산화하여 신뢰성을 높이는 동시에 향후 25년간 스마트 그리드에 7조 6,000억 달러를 확보하는 세계경제포럼과 같은 단체로부터의 계획적인 투자에 의해 세계 많은 시장의 구조가 바뀔 것으로 예상됩니다.

세계 에너지 부문이 2050년까지 탄소 배출량 넷 제로를 달성하기 위해서는 2030년까지 매년 평균 약 6,000억 달러의 전력망에 대한 투자가 필요하다고 추정되고 있습니다. 그러므로 혁신에는 관민의 다양한 조직이 협력하여 공통 에너지 목표를 추진할 필요가 있습니다. 이 비전은 현재 유럽에서 실현되고 있습니다. 선도적인 전기 사업자 8개사가 E4S(Edge for Smart Secondary Substation Alliance)를 결성하고, 인텔 및 기타 기업이 스마트 그리드 실현을 위해 협력하고 있습니다.

또한 지능형 검침 인프라(AMI) 통신 네트워크는 저대역폭, 저비용 및 지연의 영향을 받지 않는 측정의 필요성에 의해 추진되고 있습니다. 네트워크와 각 미터 내의 통신 모듈은 가능한 한 저렴한 비용이어야 합니다. AMI 초기에는 협대역 전력선 통신(PLC)과 RF 메쉬가 AMI 사용을 뒷받침하는 주요 통신 기술이었습니다. 통신 기술이 개발됨에 따라 광대역 PLC 및 저전력 광역 네트워크(LPWAN)와 같은 새로운 기술이 큰 동향이 되고 있습니다.

AMI에는 많은 장점이 있지만 표준화, 초기 비용 상승, 다른 그리드 시스템과의 통합으로 인해 도입이 어렵습니다. 이로 인해 스마트 미터 하드웨어 가격이 상승합니다. 또한 운영 요구와 소비자의 요구에 따라 다양한 스마트 미터가 추가 매개 변수로 설계되므로 비용이 증가합니다. 신기술에 투자하는 한편, 예산의 관리나 추가 자금의 확보는 어렵고, ROI는 정확해야 합니다.

지능형 검침 인프라(AMI) 시장 동향

스마트 미터링 장치가 큰 시장 점유율을 차지

스마트 미터 솔루션에는 미터 또는 미터에 설치된 통신 기능(단방향 또는 양방향)이 있는 미터 또는 모듈이 포함됩니다. 스마트 미터가 보급되고 있는 이유는 미터와 전력 회사가 사용하는 중앙 시스템 간의 양방향 통신이 가능하기 때문입니다. 이는 사람들이 더 많은 에너지를 사용하는 것이 주요 우려 사항이기 때문입니다.

스마트 미터는 가스, 전기, 수도 등 여러 배치에 채용되고 있습니다. 그 이유는 양방향 통신 기능에 의해 유틸리티자와 소비자의 쌍방에 의한 공공요금의 사용 상황의 실시간 감시가 가능하게 되고, 또한 공급자에 의한 원격조작으로공급 개시, 검침, 차단이 장려되기 때문입니다. 스마트 미터의 도입은 개별 가정이나 빌딩 전체의 전력 사용 상황을 가시화할 수 있는 홈 에너지 관리 시스템(HEMS)과 빌딩 에너지 관리 시스템(BEMS)의 도입도 가능하게 합니다.

전력 네트워크의 효율성을 높이기 위해 세계 각국의 정부는 스마트 그리드와 스마트 미터의 설치에 수십억 달러를 투자하고 있습니다. 또한 수많은 새로운 스마트 시티 개념이 세계적으로 지속적으로 도입되고 있습니다. 이러한 요인에 의해 스마트 미터 수요는 세계적으로 높아질 것으로 보입니다.

보다 깨끗하고 효과적인 에너지 시스템을 구축하기 위해 중국이나 인도 등 국가에서는 주택과 상업시설에 스마트 미터를 지속적으로 설치하고 있습니다. 각국 정부는 스마트 미터의 이용을 촉진하기 위해 많은 새로운 대처를 시작하고 있습니다. 예를 들어 인도 정부가 2021년에 도입한 RDSS(Revamped Distribution Sector Scheme)에서는 2025년 3월 말까지 2,500만대의 스마트 선불 미터를 배치할 필요가 있습니다. 아시아 국가들은 스마트 미터의 도입을 추진하기 위해 자국을 자리잡고 있습니다.

게다가 마콤 캐피탈에 따르면 2022년 1월에 전국에서 가장 스마트 미터가 설치된 것은 인도의 우타르 프라데시 주에서 115만대를 넘어섰습니다. 비하르와 라자스탄은 이에 이어집니다. 전국 배전공사가 설립한 합작회사인 Energy Efficiency Services Limited가 스마트 미터의 설치를 하청했습니다. 이처럼 아시아 전역에서 스마트 미터의 설치가 급피치로 진행되고 있는 것은 시장 성장을 뒷받침할 것으로 보입니다.

향후 소프트웨어와 클라우드 컴퓨팅 개발, 전력망 시스템의 디지털화에 대한 투자 증가, 에너지 낭비에 대한 대응 요구 증가, 사물인터넷을 이용하는 사람 증가 등이 시장 성장을 뒷받침할 것으로 예상됩니다.

현저한 성장이 예상되는 북미

북미는 스마트 미터의 급속한 보급으로 지능형 검침 인프라(AMI) 시장에서 큰 점유율을 차지할 것으로 예상됩니다. 미국은 이 지역의 주요 국가로 미국 부흥 재투자법(ARRA)과 스마트 그리드 투자 보조금(SGIG) 프로그램을 통해 스마트 미터 시장을 견인하고 있습니다.

미국에서는 주택 수가 가스 지원 유틸리티 시장 잠재력을 나타냅니다. 더 많은 신축 주택이 건설됨에 따라 AMI 프로그램의 일환으로 스마트 미터가 설치되는 주택의 비율이 증가하고 보급이 계속되고 있습니다. 미국 에너지 정보국(EIA)에 따르면 2021년 시점에서 미국에는 1억 1,100만대 이상의 고도 미터가 설치되어 있습니다. 이 나라는 지능형 검침 인프라의 범위를 꾸준히 확대하고 있습니다. 또한 가까운 미래에도 증가할 것으로 예상됩니다.

또한 캐나다는 피크 시간대 부하 감소를 주요 동기로 삼아 5년 전 정부 차원에서 스마트 전력 미터를 도입한 이후 대규모로 스마트 전력 미터를 도입했습니다. 따라서 수요 증가와 엄격한 규제가 최종 사용자 간 스마트 미터 채택을 자극하고 있습니다.

ACEEE(American Council for an Energy-Efficient Economy)에 따르면 미국의 퍼시픽 가스 앤 일렉트릭(Pacific Gas &Electric)사는 주택 리노베이션 프로그램의 AMI 타겟팅에 의해 타겟이 된 주택에서 3.5배의 에너지 절약을 달성했다고 보고했습니다. 또한 스마트 전기 미터와 데이터 분석과 같은 기술의 통합은 이 지역 시장 성장을 더욱 촉진할 것으로 예상됩니다.

또한 2021년 4월 미국 Aclara Technologies LLC는 Austin Utilities가 전기, 가스 및 수도 고객에게 서비스를 제공하기 위해 Aclara RF 네트워크를 기반으로 하는 엔드 투 엔드 지능형 검침 인프라 솔루션을 도입할 것이라고 발표했습니다. 이 포인트-투-멀티포인트 AMI 네트워크는 수동 검침 시스템을 대체하며 이 유틸리티단의 전기 1만 2,000개, 수도 9,500개, 가스 1만 1,000개의 미터를 지원합니다.

또한 2021년에는 카라베라스 카운티 수도국이 뮐러 시스템즈와 제휴하여 지능형 검침 인프라(AMI) 네트워크를 전개합니다. 이 네트워크는 1,000 평방 마일을 커버하며 1만 3,000 AMI 엔드포인트가 설치됩니다. 이 프로젝트는 이 지역의 대부분의 미터를 교환하고 모든 미터에 통신 기능을 추가합니다. 카라베라스 카운티 수도국은 카운티 내의 6개 서비스 구역으로 1만 3,000명 이상의 시영, 주택 및 상업 고객에게 수도 서비스를 제공합니다.

지능형 검침 인프라(AMI) 산업 개요

지능형 검침 인프라 시장은 매우 세분화되었습니다. 통합 및 IT화된 전력망과 패턴 분석을 위한 기타 지원 소프트웨어 개발, 스마트 미터 및 수도 미터 솔루션의 사용 증가, 지역 전반의 디지털화 노력은 지능형 검침 인프라 시장에 유리한 기회를 제공합니다. 전반적으로 기존 경쟁업체 간의 적대관계는 높습니다.

2022년 12월, Siemens는 North Delta Electricity Distribution Company를 위한 배전 관리 시스템과 지능형 검침 인프라를 구축하는 새로운 계약을 수주했습니다. 또한 제어 센터는 스마트 그리드 관리를 보장하기 위해 최첨단 IT 애플리케이션과 지능형 시스템을 도입하여 전력 공급 효율, 품질 및 안정성을 향상시키는 것을 목표로 하고 있습니다.

2022년 12월, ESB Networks는 아일랜드의 국가 스마트 미터링 프로그램 시행을 지원하기 위해 스마트 미터를 공급할 공급업체 중 하나로 첨단 계량 인프라(AMI), 스마트 그리드, 스마트 시티 및 사물 인터넷(IIoT)을 위한 솔루션을 제공하는 선도적인 글로벌 공급업체의 사업부인 Trilliant Networks Operations (UK) Ltd를 선정할 예정입니다. 이 프로그램을 통해 고객은 에너지 사용량 관리, 절약, 이산화탄소 배출량을 줄일 수 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력도 - Porter's Five Forces 분석

신규 진입업자의 위협

구매자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업 간 경쟁 관계의 강도

시장에 대한 COVID-19의 영향

제5장 시장 역학

시장 성장 촉진요인

에너지 효율 및 절약 대안으로의 전환

채용을 촉진하는 유리한 정부 이니셔티브

시장의 과제

높은 초기 비용

제6장 시장 세분화

유형별

스마트 미터 기기(전기, 수도, 가스)

솔루션

미터 통신 인프라(솔루션)

소프트웨어

미터 데이터 관리

미터 데이터 분석

기타 소프트웨어

서비스(프로페셔널- 프로그램 관리, 도입, 컨설팅, 매니지드)

최종 사용자별

주택

상업

산업

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

Itron Inc.

IBM Corporation

Landis Gyr

Sensus Solutions

Siemens AG

Tyto Corporation

Aclara Technologies LLC

Cisco Systems Inc.

Mueller Systems LLC

Trilliant Inc.

Schneider Electric SE

Honeywell International Inc.

제8장 투자 분석

제9장 시장 전망

KTH

영문 목차

영문목차

The Advanced Metering Infrastructure Market size is estimated at USD 19.69 billion in 2025, and is expected to reach USD 35.89 billion by 2030, at a CAGR of 12.76% during the forecast period (2025-2030).

Smart meters represent a transformative technology for the utility industry. These technologically advanced meters provide greater insight into the usage of energy. Smart meters have been employed as a part of advanced metering infrastructure development initiatives around the world.

Key Highlights

Developing an integrated and IT-enabled power grid and other support software to analyze the patterns provides significant benefits to the user. Such a grid, known as a "smart grid," supports the expansion of distributed production, lowers costs, promotes energy efficiency, and improves the reliability and security of the entire production, transmission, and distribution system. AMI is a vital part of any smart grid initiative. Government agencies and utilities are turning toward AMI systems as part of larger "smart grid" initiatives.

Smart meter pilot projects are also being launched in European nations like France and the U.K. In the EU, approximately 225 million smart meters for electricity and 51 million for gas will be installed by 2024, according to a study by the European Commission. By 2024, it is anticipated that 44% of European consumers will have smart gas meters, and 77% of them will have smart electric meters.

The COVID-19 outbreak, on the other hand, had a positive impact on market growth because the energy and utility sectors provide essential services that have forced the sector to rethink how their operations are carried out and how they engage with both their employees and their customers. While the COVID-19 pandemic affected nearly every other aspect, the need to maintain a secure grid remains at the forefront of priorities for utilities. AMI has helped utilities maintain their revenue flow and manage various remote operations during the pandemic.

Expanding, modernizing, and decentralizing the electricity infrastructure to make it more reliable, as well as planned investments from groups like the World Economic Forum, which has set aside USD 7.6 trillion for smart grids over the next 25 years, are expected to change the way many markets work around the world.

For the global energy sector to achieve net-zero carbon emissions by 2050, it is estimated that investment in electricity grids must average about USD 600 billion annually through 2030. Therefore, innovation will involve a variety of public and private organizations working together to advance common energy goals. This vision is currently being implemented in Europe. Eight major electric utility providers have formed the Edge for Smart Secondary Substation Alliance (E4S), a partnership with which Intel and other businesses are collaborating to create a smart grid.

Moreover, Advanced Metering Infrastructure (AMI) communications networks are driven by the need for low-bandwidth, low-cost, delay-insensitive metering. Both the network and the communications module in each meter must be as low-cost as possible. In the early days of AMI, narrow-band power-line communication (PLC) and RF-mesh were the main communication technologies that pushed the use of AMI. As communication technology has developed, newer technologies, like broadband PLC and low-power wide-area networks (LPWAN), have become bigger trends.

Although AMI has many advantages, implementing it is difficult due to standardization, high upfront costs, and integration with other grid systems. This raises the price of smart metering hardware. Additionally, based on operational needs and consumer demands, various smart meters are designed with additional parameters, which raises their cost. While investing in new technology, managing budgets or securing additional funding is difficult, and the ROI must be precise.

Smart Metering Devices Will have the Significant Market Share

Smart metering solutions include meters or modules with communication capabilities (either unidirectional or bidirectional) embedded within the meter or attached to the meter. Smart meters are becoming more popular because they allow two-way communication between the meter and the central system used by utilities. This is because the main concern is that people are using more energy.

Smart meters are increasingly being adopted for multiple deployments, such as gas, electricity, and water, due to their two-way communication feature, which enables real-time monitoring of utility usage by both the utility supplier and consumer and also encourages the start, reading, and cutting off of supply remotely by the supplier. Smart meter deployment also enables the implementation of a home energy management system (HEMS) or building energy management system (BEMS) that allows visualization of the electric power usage in individual homes or entire buildings.

To increase the effectiveness of power networks, governments worldwide are investing billions of dollars in installing smart grids and smart meters. Additionally, numerous fresh smart city initiatives are continuously being introduced globally. Such factors will raise the demand for smart meters globally.

In order to create a cleaner and more effective energy system, nations like China and India are constantly installing smart meters in residential and commercial structures. Governments are starting a number of new initiatives to promote the use of smart meters. For instance, the Revamped Distribution Sector Scheme (RDSS), which was introduced by the Indian government in 2021, calls for the deployment of 25 crore smart prepaid meters by the end of March 2025. Asian countries are positioning themselves to move forward with the adoption of smart meters.

Additionally, according to Mercom Capital, the state of Uttar Pradesh in India had the most smart meters installed nationwide in January 2022, with over 1.15 million of them. Bihar and Rajasthan came after this. Energy Efficiency Services Limited, a joint venture company established by various public power distribution companies in the nation, took on the installation of smart meters. Such a rapid pace for the installation of smart meters across the Asian region will boost market growth.

In the future, developments in software and cloud computing, rising investments in digitalizing grid systems, a growing need to deal with energy waste, and more people using the internet of things are all expected to help the market grow.

North America Region is Expected to Grow at Significant Pace

North America is expected to hold a prominent share in the Advanced Metering Infrastructure (AMI) market due to the rapid adoption of smart metering in the region. Favorable government initiatives and increasing government investments in smart meter deployment across regions drive market growth.The United States is the key country in the region, driving the smart meter market through the American Recovery and Reinvestment Act (ARRA) and the Smart Grid Investment Grant (SGIG) program.

In the United States, the number of houses represents the market potential for gas-enabled utilities. As more new houses are built, a growing proportion of homes will have smart meters installed as part of the AMI program, which continues its widespread adoption. According to the US Energy Information Administration (EIA), over 111 million advanced meters were installed in the US as of 2021. The nation has been steadily increasing the scope of its advanced metering infrastructure. It is also expected to increase in the near future.

Further, Canada has also witnessed the large-scale incorporation of smart electricity meters after the governmental mandate was introduced more than five years ago with the prime motive of reducing peak-time loads. Thus, increasing demand and stringent regulations are stimulating the adoption of smart meters among end users.

Along with leveraging smart electric meters for energy efficiency, targeted programs for end users are likely to benefit.As per the American Council for an Energy-Efficient Economy (ACEEE), Pacific Gas & Electric in the United States reported that AMI targeting for a home retrofit program delivered 3.5 times more energy savings in the targeted homes. Additionally, the integration of smart electric meters with technologies such as data analytics is expected to further foster the growth of the market in the region.

Moreover, in April 2021, Aclara Technologies LLC, US, announced that Austin Utilities would implement an end-to-end advanced metering infrastructure solution based on the Aclara RF network to serve its electric, gas, and water customers. The point-to-multipoint AMI network replaces a manual meter-reading system and supports 12,000 electric, 9,500 water, and 11,000 gas meters for the combination utility.

Also in 2021, Calaveras County Water District partnered with Mueller Systems for the deployment of an advanced metering infrastructure (AMI) network. It will cover 1,000 square miles with 13,000 AMI endpoints. The project replaces most of the district's meters and adds communication capabilities to all meters. Calaveras County Water District provides water service to over 13,000 municipal, residential, and commercial customers in six service areas throughout the county.

Advanced Metering Infrastructure (AMI) Industry Overview

The advanced metering infrastructure market is highly fragmented. The development of integrated and IT-enabled power grids and other support software to analyze the patterns, the increase in the use of smart meters and water metering solutions, and digitization initiatives across regions provide lucrative opportunities in the advanced metering infrastructure market. Overall, the competitive rivalry among existing competitors is high.

In December 2022, Siemens will be awarded a new contract to establish a distribution management system and advanced metering infrastructure for North Delta Electricity Distribution Company. Additionally, the control centers aim to enhance the efficiency, quality, and stability of the power supply by implementing the most advanced IT applications and intelligent systems to ensure smart grid management.

In December 2022, ESB Networks will choose Trilliant Networks Operations (UK) Ltd., a division of the leading global provider of solutions for advanced metering infrastructure (AMI), the smart grid, smart cities, and the Internet of Things (IIoT), as one of the suppliers to provide smart meters in support of the implementation of Ireland's National Smart Metering Programme. Customers will find it simpler to manage their energy use, save money, and reduce their carbon footprint thanks to the program.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porters Five Forces Analysis

4.2.1 Threat of New Entrants

4.2.2 Bargaining Power of Buyers

4.2.3 Bargaining Power of Suppliers

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Impact of COVID-19 on the market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Shift Toward Energy Efficient/Saving Alternatives