금속 가공유 시장 전망 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

Metal Working Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1640577

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

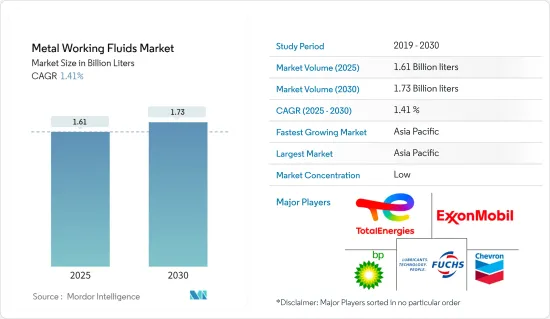

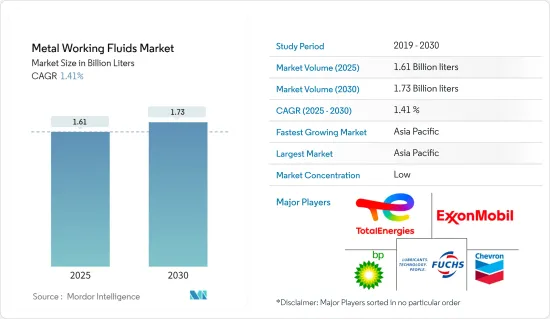

금속 가공유 시장 규모는 2025년에 16억 1,000만리터로 추정되며 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 1.41%로, 2030년에는 17억 3,000만리터에 달할 것으로 예측됩니다.

주요 하이라이트

자동차 부문과 중장비 산업 수요 증가는 금속 가공유 수요를 견인하는 주요 요인입니다.

그러나 건식 가공 기술의 채택과 엄격한 환경 규제가 시장을 저해할 것으로 예상됩니다.

그럼에도 불구하고 다상 금속 가공유의 출현과 기술 발전은 연구 대상 시장에 새로운 기회를 창출할 것으로 예상됩니다.

아시아태평양이 시장을 독점하고 있으며, 중국, 인도, 일본 등이 가장 큰 소비국입니다.

금속 가공유 시장 동향

자동차 부문 수요 증가

금속 가공유는 자동차 부문에서 매우 중요합니다. 금속 가공유는 공구와 공작물 사이의 마찰을 줄이고 표면 품질을 개선하며 금속 칩 제거를 용이하게 하고 공구 수명을 연장합니다. 이러한 유체는 가공 작업의 효율성을 높여 기계 생산성을 높이는 데 기여합니다.

세계자동차공업협회(OICA)에 따르면 2023년에는 전 세계적으로 약 9,355만 대의 차량이 생산되어 2022년의 8,483만 대에 비해 약 10.26%의 성장률을 기록할 것으로 예상되어 자동차 산업에서 금속 가공유에 대한 수요가 증가할 것으로 전망됩니다.

아시아, 오세아니아 지역은 다른 지역을 앞지르며 자동차 제조의 선두 주자로 부상했습니다. OICA 데이터에 따르면 이 지역의 자동차 생산량은 2023년 5,511만 대에 달해 2022년 5,022만 대보다 10.18% 증가할 것으로 예상됩니다. 특히 중국, 일본, 한국, 인도와 같은 주요 국가들이 이 생산량을 주도하고 있습니다.

세계자동차공업협회(OICA)에 따르면 2023년 중국은 3,016만 대의 자동차를 생산하며 세계 최대 자동차 생산 허브로서의 입지를 공고히 할 것으로 예상됩니다. 이는 2022년의 2,702만 대 생산량에서 12% 증가한 수치입니다.

한편, 미국은 세계에서 두 번째로 큰 자동차 제조업체로서의 입지를 공고히 했습니다. 자동차 부문은 미국 경제의 초석으로, 2023년 미국 GDP의 3%에서 3.5%를 차지할 것으로 예상되었습니다. 미국은 국내 수요를 충족할 뿐만 아니라 미주, 유럽, 아시아태평양 시장에 차량을 수출하는 주요 자동차 제조업체의 본거지입니다.

세계자동차제조업협회(OICA)는 2023년 미국이 전년 대비 6% 증가한 1061만 대의 자동차를 생산할 것으로 예상했습니다.

유럽은 2023년 자동차 생산량이 눈에 띄게 증가했습니다. 전체적으로 생산량은 전년 대비 13% 증가했습니다. 특히 승용차와 LCV 생산량은 12%와 19% 증가하여 2023년에 각각 1,540만 대와 160만 대를 기록할 것으로 예상됩니다.

자동차 산업이 확대되고 있기 때문에 금속 가공유 수요는 예측 기간 중에 증가할 것으로 보입니다.

아시아태평양 지역의 급성장

아시아 태평양 지역은 자동차 및 중장비 부문의 수요 증가에 힘입어 시장을 주도하고 있습니다. 중국, 인도, 일본과 같은 국가에서는 산업화와 경제 성장에 힘입어 중장비 산업이 급성장하고 있습니다.

금속가공유는 중장비 및 장비의 제조에 중요한 역할을 하고 있습니다.

중장비 산업은 공작 기계, 중전기 장비, 시멘트 기계, 자재 취급, 플라스틱 가공, 공정 플랜트 장비, 토공, 건설, 광업용 장비 등 다양한 하위 분야를 포괄합니다.

중국의 14차 5개년 계획은 농업 및 농촌의 변화를 강화하는 것을 목표로 하고 있으며, 이는 농업 및 건설 분야에서 중장비의 사용 증가와 직접적인 관련이 있습니다.

중국의 농기계 산업은 꾸준한 상승세를 이어가고 있으며, 약 10,000개의 농기계 회사와 20,000개 이상의 유통업체가 존재합니다. 2023년 농기계 수출은 14개 대외 무역 하위 부문 중 특히 대형 및 중형 트랙터 부문에서 전년 대비 33.5%의 견조한 증가세를 보였습니다.

또한 중국건설기계협회(CCMA)의 데이터에 따르면 2024년 6월 굴삭기 판매량은 전년 대비 5.31% 증가한 총 16,603대를 기록했습니다. 국내 판매량은 7,661대로 연간 25.6%의 높은 성장률을 기록했습니다.

인도의 농업 장비 부문은 글로벌 무대에서 엄청난 비중을 차지하고 있으며, 수많은 인도 제조업체들이 국내 및 해외 시장을 모두 공략하고 있습니다. 트랙터 제조업체 협회는 2023년 12월 트랙터 판매량이 2022년 55,390대에서 44,735대로 19.24% 감소했다고 보고했습니다. 그러나 해외 수출은 2022년 131,850대에서 감소했지만 2023년 96,223대로 견조한 수준을 유지했습니다.

인도의 건설기계산업은 2023-2024회계연도에 26%의 성장을 이루었으나 이는 주로 정부의 인프라 주도의 의제에 의한 것입니다. 인도 건설기계공업회(ICEMA)에 따르면 2023년 판매량은 13만 5,650대에 달하고, 전년 10만 7,779대에서 증가했습니다. 특히 산업 최대의 부문인 토목기계의 판매 대수는 2023-2024년도에 21% 증가한 9만 3,531대가 되어, 판매 대수 전체의 약 70%를 차지했습니다.

자동차 딜러 협회 연맹의 보고에 따르면 2023 회계연도에 인도의 승용차 판매량은 23% 증가했습니다. 주요 제조업체들은 특히 반도체와 전자제품의 간헐적인 공급망 문제를 해결했습니다. 가처분 소득의 증가, 새로운 스포츠 유틸리티 차량의 등장, 매력적인 대출 금리에 힘입어 인도의 승용차 판매량은 2023 회계연도에 처음으로 400만 대를 돌파했습니다.

인도 자동차 제조업체 협회(SIAM)에 따르면 2023년 승용차, 세단, 유틸리티 차량의 판매량은 410만 대를 넘어섰습니다. 이는 2022년의 379만 대 판매량보다 8.2% 증가한 수치입니다. 이러한 급증은 주로 유틸리티 차량이 주도했으며, 전체 판매량의 57.4%를 차지했습니다.

이러한 역학을 감안하면, 아시아태평양은 향후 수년간 금속 가공유 시장을 주도해 나갈 것으로 예상됩니다.

금속 가공유제산업 개요

금속 가공유 시장은 부분적으로 통합되어 있습니다. 주요 진출기업(특정한 순서 없음)에는 ExxonMobil, FUCHS, TotalEnergies, BP PLC, Chevron Corporation이 포함됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 성장 촉진요인

자동차 산업에서의 수요 증가

중기 산업에서의 수요 증가

기타 촉진요인

시장 성장 억제요인

건식 가공 기술의 채용

엄격한 환경 규제

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 기준 시장 규모)

제품 유형별

제거액

성형액

보호액

처리액

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

이집트

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율, 랭킹 분석

주요 기업의 전략

기업 프로파일

BP PLC

Carl Bechem Lubricants India Private Limited

Chevron Corporation

Exxon Mobil Corporation

FUCHS

Hindustan Petroleum Corporation Limited

Indian Oil Corporation Ltd

Kemipex

SKF

Motul

PETRONAS Lubricants International

TotalEnergies

Saudi Arabian Oil Co.

제7장 시장 기회와 앞으로의 동향

다상 금속 가공유의 출현

기술의 진보

기타 기회

HBR

영문 목차

영문목차

The Metal Working Fluids Market size is estimated at 1.61 billion liters in 2025, and is expected to reach 1.73 billion liters by 2030, at a CAGR of 1.41% during the forecast period (2025-2030).

Key Highlights

The growing demand from the automotive sector and the heavy machinery industry are the major factors driving the demand for metalworking fluids.

However, the adoption of dry machining technologies and stringent environmental regulations are expected to hinder the market.

Nevertheless, the emergence of multi-phase metal working fluids and advancements in technology are expected to create new opportunities for the market studied.

Asia-Pacific dominates the market, with countries like China, India, and Japan being the biggest consumers.

Metal Working Fluids Market Trends

Growing Demand from the Automotive Sector

Metalworking fluids are crucial in the automotive sector. They reduce friction between tools and workpieces, enhance surface quality, facilitate metal chip removal, and extend tool life. By boosting the efficiency of machining operations, these fluids contribute to heightened machine output.

According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), in 2023, around 93.55 million units of vehicles were produced worldwide, witnessing a growth rate of around 10.26% compared to 84.83 million units of vehicles in 2022, thereby indicating an increased demand for metalworking fluids from the automotive industry.

The Asia-Oceania region emerged as the frontrunner in vehicle manufacturing, outpacing other regions. OICA data highlights that automotive production in this region reached 55.11 million units in 2023, up by 10.18% from 50.02 million units in 2022. Notably, this production is spearheaded by key players like China, Japan, South Korea, and India.

According to the OICA (Organisation Internationale des Constructeurs d'Automobiles), in 2023, China solidified its position as the world's largest automotive production hub, churning out 30.16 million vehicles. This marks a notable 12% uptick from the 27.02 million units produced in 2022.

Meanwhile, the United States solidified its position as the world's second-largest automotive manufacturer. The automotive sector stands as a cornerstone of the US economy, contributing between 3% and 3.5% to the nation's GDP in 2023. The United States is home to major automakers who not only meet domestic demands but also export vehicles to markets spanning the Americas, Europe, and the Asia-Pacific.

The Organisation Internationale des Constructeurs d'Automobiles (OICA) reported that the United States produced 10.61 million units of vehicles in 2023, marking a 6% increase from the previous year.

Europe witnessed a notable growth in motor vehicle production in 2023. Overall, production surged by 13% compared to the previous year. Specifically, passenger car and LCV production saw increases of 12% and 19%, culminating in 15.4 million units and 1.6 million units, respectively, in 2023.

Given the expanding automotive industry, the demand for metalworking fluids is poised to rise during the forecast period.

Asia-Pacific to Witness the Fastest Growth

Asia-Pacific leads the market, driven by rising demand from the automotive and heavy machinery and equipment sectors. Countries like China, India, and Japan are witnessing a surge in their heavy machinery industry, fueled by industrialization and economic growth.

Metalworking fluids play a crucial role in manufacturing heavy machinery and equipment.

The heavy machinery industry encompasses diverse sub-sectors, including machine tools, heavy electrical equipment, cement machinery, material handling, plastics processing, process plant equipment, and equipment for earth moving, construction, and mining.

China's 14th Five-Year Plan aims to bolster its agricultural and rural transformation, which is directly related to the heightened use of heavy machinery in agriculture and construction.

China's agricultural equipment sector has been on a steady upward trajectory, featuring close to 10,000 farming machinery firms and over 20,000 distribution entities. As highlighted by AgroPages in 2023, amidst 14 foreign trade sub-sectors, agricultural machinery exports showcased a robust 33.5% year-on-year surge, particularly in large and medium-sized tractors.

Moreover, data from the China Construction Machinery Association (CCMA) indicates a 5.31% year-on-year rise in excavator sales, totaling 16,603 units in June 2024. Domestic sales reached 7,661 units, reflecting a strong 25.6% annual growth.

India's agricultural equipment sector holds immense weight in the global arena, with numerous Indian manufacturers catering to both domestic and international markets. The Tractor Manufacturers Association reported a 19.24% dip in tractor sales in December 2023, with figures dropping from 55,390 units in 2022 to 44,735 units. However, overseas exports remained robust at 96,223 units in 2023, albeit down from 131,850 units in 2022.

The Indian construction equipment industry experienced a 26% growth in the fiscal year 2023-24, largely due to the government's infrastructure-driven agenda. According to the Indian Construction Equipment Manufacturers' Association (ICEMA), 2023 sales reached 135,650 units, up from 107,779 units the previous year. Notably, earthmoving equipment sales, the industry's largest segment, rose by 21% to 93,531 units in FY 2023-24, constituting about 70% of the total sales.

Passenger vehicle sales in India jumped 23% in the financial year 2023, as reported by the Federation of Automobile Dealers Associations. Leading manufacturers navigated intermittent supply chain challenges, particularly with semiconductors and electronics. Driven by rising disposable incomes, a wave of new sport-utility vehicles, and attractive loan rates, India's passenger vehicle sales touched 4 million units for the first time in FY 2023.

According to the Society of Indian Automobile Manufacturers (SIAM), in 2023, sales of cars, sedans, and utility vehicles surpassed 4.1 million. This marks an 8.2% rise from the 3.79 million sold in 2022. The surge was predominantly fueled by utility vehicles, making up 57.4% of the total sales.

Given these dynamics, Asia-Pacific is poised to lead the metalworking fluids market in the coming years.

Metal Working Fluids Industry Overview

The metal working fluids market is partially consolidated in nature. The major players (not in any particular order) include Exxon Mobil Corporation, FUCHS, TotalEnergies, BP PLC, and Chevron Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Drivers

4.1.1 Growing Demand from the Automotive Sector

4.1.2 Increasing Demand from the Heavy Machinery Industry

4.1.3 Other Drivers

4.2 Market Restraints

4.2.1 Adoption of Dry Machining Technologies

4.2.2 Stringent Environmental Regulations

4.2.3 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Product Type

5.1.1 Removal Fluids

5.1.2 Forming Fluids

5.1.3 Protection Fluids

5.1.4 Treating Fluids

5.2 By Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 Malaysia

5.2.1.6 Thailand

5.2.1.7 Indonesia

5.2.1.8 Vietnam

5.2.1.9 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 France

5.2.3.4 Italy

5.2.3.5 Spain

5.2.3.6 NORDIC Countries

5.2.3.7 Turkey

5.2.3.8 Russia

5.2.3.9 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Colombia

5.2.4.4 Rest of South America

5.2.5 Middle East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 Qatar

5.2.5.3 United Arab Emirates

5.2.5.4 Nigeria

5.2.5.5 Egypt

5.2.5.6 South Africa

5.2.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share(%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 BP PLC

6.4.2 Carl Bechem Lubricants India Private Limited