도료 및 코팅 첨가제 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

Paints and Coatings Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1640541

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

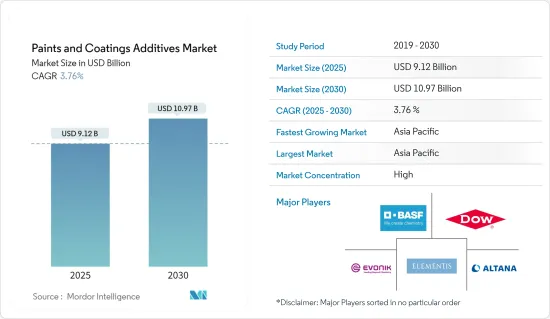

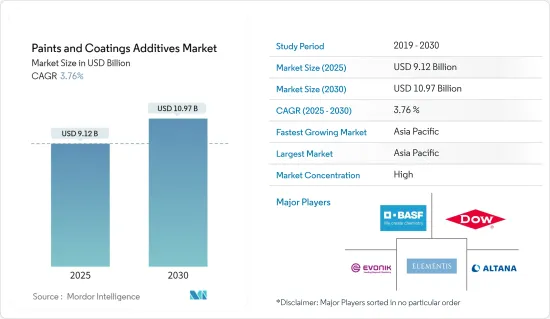

도료 및 코팅 첨가제 시장 규모는 2025년에 91억 2,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 3.76%를 나타낼 전망이며, 2030년에는 109억 7,000만 달러에 도달할 것으로 예측됩니다.

COVID-19는 2020년 도료 및 코팅 첨가제 시장에 부정적인 영향을 미쳤습니다. 그러나 주요 최종 사용자 산업의 작업 재개에 따라 시장은 향후 수년간 안정적으로 성장할 것으로 추정됩니다.

주요 하이라이트

건축용 도료 수요 증가는 시장 조사의 주요 촉진요인입니다.

반대로, 환경 규제 증가는 시장 성장을 방해할 것으로 예상됩니다.

다양한 산업에서 유변학적 개질제 수요 증가가 기회가 될 가능성이 높습니다.

아시아태평양은 세계 시장을 독점하고 중국과 인도에서 소비가 가장 많습니다.

도료 및 코팅 첨가제 시장 동향

건축 부문이 시장을 독점

건축 부문에는 사무실 건물, 창고, 편의점, 쇼핑몰, 주택과 같은 상업용 도료에 사용되는 첨가제가 포함됩니다.

건축용 도료에 사용되는 주요 첨가제에는 유변학적 개질제, 소포제, 분산제, 습윤제 등이 있습니다.

일반적으로 건축 도료에 사용되는 첨가제는 표면 특성 향상, 안료 안정화, 습윤성 향상, 분산성, 소포성 등에 유용합니다.

미국 인구조사국에 따르면 미국의 2022년 12월 신규 건설 생산액은 1조 7,929억 달러였습니다. 2023년 3월 비주택 부문은 9,971억 4,000만 달러로 전년 동기 대비 18.8%의 성장을 기록했습니다.

또한 미국 인구조사국에 따르면 2022년 6월 민간 및 공공건설 비주택지출은 4,926억 8,000만 달러로 2021년 6월 4,842억 6,000만 달러에 비해 1.74% 증가했습니다. 따라서 국내 민간 및 공공 비주택 건설에 대한 지출 증가는 도료 및 코팅 첨가제 시장에 상향 수요를 발생시킬 것으로 예상됩니다.

이 외에도 미국에서는 다양한 상업 건설 프로젝트가 예정되어 있습니다. 노스캐롤라이나주 콩코드에 있는 Red Bull North America의 7억 4,000만 달러 상당의 200만 평방 피트 가공 및 유통 시설, 워싱턴주 파스코 항구에 있는 낙농 협동조합 Dairgold의 5억 달러 상당의 40만 평방 피트 가공 시설(2023년 완성 예정), 텍사스 Biotics Research Corporation의 9백만 달러 상당의 8만 8,000평방피트 규모 창고, 연구소, 오피스 시설(2023년 완성 예정) 등입니다.

사우디아라비아에서는 주택 건설에 대한 투자가 증가하고 있으며, 이는 도료 및 코팅 첨가제 시장 수요를 높일 것으로 예상됩니다. 예를 들어 사우디아라비아에서는 부동산 개발 건수 증가, 주택 수요 증가, 사회 경제 인프라 정비를 위한 정부의 이니셔티브가 도료 및 코팅 첨가제 시장을 견인하고 있습니다. 사우디아라비아 주택부 장관인 Majid Al-Hogail에 따르면, 사우디아라비아는 향후 5년간 30만 호의 주택 건설을 계획하고 있습니다. "비전 2030"에서 사우디아라비아의 중요한 이니셔티브 중 하나가 주택입니다. 향후 수년간 사우디아라비아 건설 부문에서 도료 및 코팅 첨가제 시장에 대한 수요가 창출될 가능성이 높습니다.

정부의 이러한 노력은 건설 업계를 빠르게 활성화시킬 것으로 기대되며 또한 건설 부문의 도료, 나아가서는 코팅 첨가제의 소비를 한층 더 뒷받침하고 있습니다.

따라서 이러한 주택건설에 대한 투자와 프로젝트는 주택건설에 사용되는 도료 및 코팅제의 소비와 함께 이들 국가에서 건설활동을 촉진하고 있습니다.

아시아태평양이 시장을 독점

아시아태평양은 도료 및 코팅 분야 개발을 목표로 하고 있습니다. 주요 원료에 대한 접근성, 기초 분자의 생산, 지역 시장에 대한 접근성을 활용하여 세계의 도료 및 코팅제 공급망의 중심이 되려 합니다.

아시아태평양에는 가장 높고 가장 크고 가장 거대한 구조물을 만들기 위한 끈기있는 노력이 지속되고 있습니다. 아시아태평양의 도료 및 코팅 산업은 향후 몇 년 동안 꾸준한 성장을 기록할 것으로 예상됩니다. 건설 업계는 향후 수년간 견고한 성장을 이루고 이는 도료 첨가제 수요를 증대시킬 것으로 보입니다.

도료 및 코팅 첨가제 시장에서 중국은 아시아태평양에서 가장 큰 점유율을 차지합니다. 중국에서는 투자와 건설 활동이 활발해지고 있기 때문에 도료 및 코팅 첨가제 시장 수요는 예측 기간을 통해 증가할 것으로 예상됩니다. 중국은 지난 몇 년간 세계 인프라에 대한 주요 투자국 중 하나이기 때문에 조사 시장에 큰 기여를 하고 있습니다. 예를 들어 중국국가통계국(NBS)에 따르면 2022년 중국 건설공사 생산액은 31조 2,000억 위안(4,758억 4,000만 달러)에 이르렀으며 2021년에 비해 6.5% 증가했습니다.

또한 중국의 주택 도시 농촌개발부에 따르면 2025년까지 건설업이 GDP에 차지하는 비율은 6%를 유지할 것으로 전망됩니다. 중국에서는 조립식 건축의 동향이 높아지고 있으며, 신축의 30% 이상을 조립식 건축이 차지할 것으로 예상되고 있습니다.

국가개발개혁위원회에 따르면 중국 정부는 26개 인프라 프로젝트를 승인했으며, 그 투자액은 약 1,420억 달러로 추정되며, 2023년까지 완성될 것으로 보입니다. 주택 수요 증가는 공공 부문과 민간 부문의 주택 건설을 촉진할 것으로 예상됩니다. 그러므로 주택건설에 대한 투자가 증가함에 따라 중국 건설 업계에서 도료 및 코팅 첨가제 시장에 대한 수요가 상승할 것으로 예상됩니다.

인도는 아시아태평양의 G20 중 가장 급성장하고 있는 경제국으로 지속될 것으로 예상됩니다. 인도 정부는 3년간(2023-2025년) 3,765억 달러의 인프라 투자 목표를 발표했습니다. 그 내역은 27개의 산업 클러스터 개발에 1,205억 달러, 도로, 철도, 항만 연결 프로젝트에 753억 달러입니다. 이러한 이유로 인도의 건설 산업은 도료 및 코팅 첨가제 수요를 뒷받침할 가능성이 높습니다.

또한 IBEF에 따르면 2022-2023년 연방 예산에서 정부는 인프라 부문 강화에 10조 루피(1,305억 7,000만 달러)를 할당했습니다. 게다가 인도는 향후 5년간 '국가 인프라 파이프라인'을 통해 인프라에 1조 4,000억 달러를 지출할 계획입니다.

또한, 민간항공부 장관은 인도 정부가 2032년까지 100개의 공항을 건설할 계획이라고 발표했습니다.

위와 같은 요인들로 인해 예측 기간 동안 아시아태평양이 세계적으로 우위를 차지할 것으로 예상됩니다.

도료 및 코팅 첨가제 산업 개요

도료 및 코팅 첨가제 시장은 그 특성상 부분적으로 통합되어 있습니다. 이 시장의 주요 기업(순서부동)에는 Dow, BASF SE, Altana Group (BYK), Evonik Industries AG, Elementis PLC가 포함됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

촉진요인

아키텍처 코팅 수요 증가

다양한 산업에서의 유변학적 개질제 수요 증가

기타 촉진요인

억제요인

환경 규제 증가

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 기준 시장 규모)

유형별

살생물제

분산제와 습윤제

소포제 및 탈포제

유변학적 개질제

표면 개질제

안정제

유동 및 레벨링 첨가제

기타 유형

용도별

건축용 도료 및 코팅

목재용 도료

수송용 도료

보호 도료

기타 용도

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)**/순위 분석

주요 기업의 전략

기업 프로파일

AGC Inc.

ALTANA AG

Arkema

Ashland

BASF SE

Cabot Corporation

DAIKIN INDUSTRIES, Ltd.

Dow

Dynea AS

Eastman Chemical Company

ELEMENTIS PLC

Evonik Industries AG

K-TECH(INDIA) LIMITED

Momentive

Nouryon

Solvay

The Lubrizol Corporation

제7장 시장 기회와 앞으로의 동향

워터 코팅으로의 동향 전환

기타 기회

CSM

영문 목차

영문목차

The Paints and Coatings Additives Market size is estimated at USD 9.12 billion in 2025, and is expected to reach USD 10.97 billion by 2030, at a CAGR of 3.76% during the forecast period (2025-2030).

COVID-19 negatively impacted the market for paints and coatings additives in 2020. However, with the resumption of work in major end-user industries, the market is estimated to grow steadily in the coming years.

Key Highlights

The increased demand for architectural coatings is the major factor driving the market studied.

Conversely, rising environmental regulations are expected to hinder market growth.

Increasing demand for rheology modifiers in various industries will likely be an opportunity.

Asia-Pacific dominated the global market, with the largest consumption in China and India.

Paints and Coatings Additives Market Trends

Architectural Segment to Dominate the Market

The architectural segment includes additives used in coatings for commercial purposes, such as office buildings, warehouses, retail convenience stores, shopping malls, and residential buildings.

Some majorly used additives for architectural coatings include rheological modifiers, defoamers, dispersants, and wetting agents.

Generally, the additives used for architectural coatings help to enhance surface properties, stabilizing pigment, enhancing wetting, dispersing, and defoaming properties, etc.

According to the US Census Bureau, the value of new construction output in the United States amounted to USD 1,792.9 billion in December 2022. The non-residential sector accounted for USD 997.14 billion in March 2023, registering a growth of 18.8% compared to the same period of the previous year.

Moreover, according to the US Census Bureau, the private and public construction non-residential spending in June 2022 was 492.68 billion, which showed an increase of 1.74% compared to June 2021, which amounted to USD 484.26 billion. Therefore, increasing spending on private and public non-residential constructions in the country is expected to create an upside demand for the paints and coatings additives market.

Apart from that, there are various construction commercial projects scheduled in the United States Red Bull North America's USD 740 million worth 2 million sq ft processing and distribution facility in Concord, North Carolina, Dairy cooperative DairgoldUSD 500 million worth 400,000 sq ft processing facility in Port of Pasco, Washington (completion scheduled for 2023), Biotics Research Corporation USD 9 million worth 88,000 sq ft warehouse, laboratory, and office facility in Rosenberg, Texas (completion scheduled for 2023).

Increasing investment in residential constructions in Saudi Arabia is expected to boost the demand for the paints and coatings additives market. For instance, in Saudi Arabia, the growing number of real estate developments, increasing demand for residential property, and governmental initiatives to develop socio-economic infrastructure drive the country's paints and coatings additives market. According to Majid Al-Hogail, the Saudi Housing Minister, the Kingdom of Saudi Arabia plans to construct 300,000 extra housing units over the next five years. One of Saudi Arabia's significant initiatives under Vision 2030 is housing. It will likely create demand for the paints and coatings additives market from the country's construction sector in the upcoming years.

Such initiatives by the government are expected to rapidly boost the construction industry. It is also further boosting the consumption of coating and, in turn, coating additives in the construction sector.

Hence, all such residential construction investments and projects are driving construction activities in these countries, along with the consumption of paints and coatings for application in residential construction.

Asia-Pacific to Dominate the Market

Asia-Pacific is aiming for the development of its paints and coatings sector. It is on the way to becoming the center of the global paints and coatings supply chain, leveraging its easy access to key feedstock, production of basic molecules, and access to the regional market.

Asia-Pacific includes a persistent expedition in making some of the tallest, largest, and biggest structures. The paints and coatings industry in the country is expected to register steady growth in the coming years. The construction industry is poised to witness sturdy growth in the forthcoming years, augmenting the demand for coating additives.

China holds the largest Asia-Pacific market share for the paints and coatings additives market. The demand for the paints and coatings additives market is expected to rise throughout the forecast period due to rising investments and construction activity in the country. China is a huge contributor, as it is one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to CNY 31.2 trillion (USD 475.84 billion), an increase of 6.5% compared with 2021.

Moreover, in China, according to the country's Ministry of Housing and Urban-Rural Development, the construction industry will maintain a 6% share of the country's GDP by 2025. There is a growing trend in the country for prefabricated buildings, which is expected to account for more than 30% of the country's new construction.

According to the National Development and Reform Commission, the Chinese government approved 26 infrastructure projects at an estimated investment of about USD 142 billion, estimated to be completed by 2023. The growing demand for housing is expected to drive residential construction in the public and private sectors. Therefore, increasing investments in residential construction is expected to create an upside demand for the paints and coatings additives market from the country's construction industry.

India is anticipated to remain the fastest-growing G20 economy in the Asia-Pacific region. The Indian government announced a target of USD 376.5 billion in infrastructure investment over three years (2023-2025). It includes USD 120.5 billion for developing 27 industrial clusters and USD 75.3 billion for road, railway, and port connectivity projects. Therefore, this will likely create an upside for paints and coatings additives from the country's construction industry.

Moreover, according to IBEF, in Union Budget 2022-2023, the government allocated INR 10 trillion (USD 130.57 billion) to enhance the infrastructure sector. Moreover, India plans to spend USD 1.4 trillion on infrastructure through the 'National Infrastructure Pipeline' in the next five years.

Furthermore, the civil aviation minister announced that the Indian government is also planning to construct 100 airports by 2032, owing to increasing demand for air commutes.

The factors above are expected to make the Asia-Pacific the dominant globally during the forecast period.

Paints and Coatings Additives Industry Overview

The Paints and Coatings Additives Market is partially consolidated in nature. The major players in this market (not in a particular order) include Dow, BASF SE, Altana Group (BYK), Evonik Industries AG, and Elementis PLC.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increased Demand for Architectural Coatings

4.1.2 Increasing Demand for Rheology Modifiers in Various Industries

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Rising Environmental Regulations

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Biocides

5.1.2 Dispersants and Wetting Agents

5.1.3 Defoamers and Deaerators

5.1.4 Rheology Modifiers

5.1.5 Surface Modifiers

5.1.6 Stabilizers

5.1.7 Flow and Leveling Additives

5.1.8 Other Types

5.2 Application

5.2.1 Architectural Paints and Coatings

5.2.2 Wood Paints and Coatings

5.2.3 Transportation Paints and Coatings

5.2.4 Protective Paints and Coatings

5.2.5 Others Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements