ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

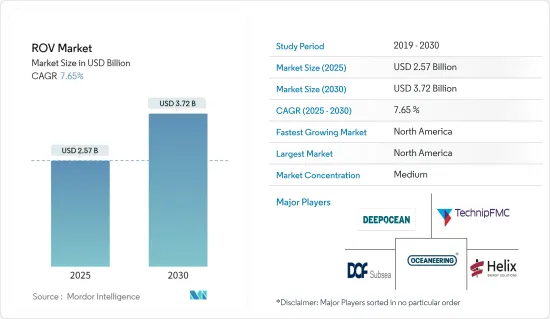

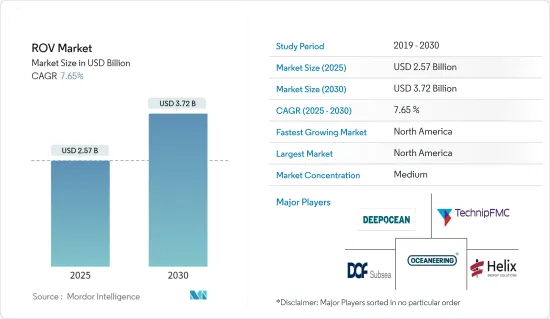

ROV 시장 규모는 2025년에 25억 7,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 7.65%로, 2030년에는 37억 2,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

아메리카, 아시아태평양, 중동, 아프리카에서 해양 석유 및 가스 탐사 활동 증가와 해양 재생 가능 기술의 성장이 예측 기간 동안 ROV 시장을 견인할 것으로 예상됩니다.

한편, 여러 지역에서 해양 탐사 및 생산 활동이 금지되어 있고 이는 시장을 억제할 것으로 예상됩니다.

그러나 현재 진행 중인 심해 및 초심해에서의 석유 및 가스 발견과 셰일 가스 탐사는 예측 기간 동안 ROV 성장의 큰 기회를 만들어낼 것으로 기대되고 있습니다.

북미는 세계 시장을 독점하고 수요의 대부분은 미국과 멕시코에서 발생합니다. 북미는 선진적이고 민첩한 ROV 개발로 세계를 선도하고 있습니다.

ROV 시장 동향

석유 및 가스용도 부문이 시장을 독점할 전망

세계 주요 경제국이 여전히 석유 기반 제품에 크게 의존하고 있기 때문에 석유 및 가스에 대한 의존도는 높게 유지됩니다. 석유 및 가스산업은 국제정치 경제에서 절대적인 영향력을 가지고 있습니다.

Statistical Review of World Energy Data에 따르면 2022년 세계 석유 생산량은 9,987만 7,000배럴/일로 전년대비 11.1% 증가했습니다. 세계 인구 증가는 1차 에너지 소비 증가를 반영하여 2011년 520.90 엑사 줄에서 2022년에는 604.04 엑사 줄이 되었습니다.

석유수출국기구(OPEC)에 따르면 2023년 세계 원유 수요(바이오연료 포함)는 일량 1억 221만 배럴에 달할 전망입니다. 이 보고서는 경제 활동과 관련 석유 수요가 연말까지 회복되어 일량 1억 400만 배럴 이상 증가할 것으로 예측했습니다.

탄화수소산업은 성공적인 석유 및 가스의 발견과 생산을 위해 해저 조건에 적합한 기술을 개발해 왔습니다. 석유 및 가스 드릴링 리그는 최대 수심 2마일로 조업할 수 있습니다. 심해 유정 및 파이프라인 시스템의 대부분은 설치, 검사, 수리 및 유지보수를 무인잠수정에 의존합니다.

지난 몇 년동안 원격 무인잠수정(ROV)은 틈새 응용 분야의 신기술에서 석유 및 가스 부문의 광범위한 응용 분야로 진화했습니다.

해외 산업의 설비 투자도 세계적으로 크게 증가하고 있으며, 특정 활동을 수행하기 위한 다양한 첨단 기술, 도구 및 장비에 대한 수요가 증가하고 있습니다. 이러한 도구에는 바다에서 유지보수 점검 작업을 용이하게 하는 ROV가 포함됩니다. 일부 석유 및 가스 회사는 해저 조사를 지원하기 위해 ROV에 투자하고 있습니다.

예를 들어, 2023년 8월, Energean은 애버딘에 본사를 둔 원격 무인잠수정(ROV)과 서비스의 세계적인 공급업체 ROVOP에 5년간의 ROV 지원 계약을 주문했습니다. 이 회사는 플랫폼 공급선을 개조한 Energian의 현장 지원선 Energian Star에 ROV를 배치합니다.

ROV의 기술적 진보는 운영을 더욱 쉽고 효율적으로 만들어 석유 및 가스 산업에 대한 수요를 끌어올리고 있습니다.

전반적으로 ROV 수요는 빠르게 성장하는 해양 석유 및 가스 에너지 사업으로 인해 예측 기간 동안 증가할 것으로 예상됩니다. 원격 무인잠수정과 관련된 기술은 점점 진보하고 있습니다.

북미가 시장을 독점할 전망

이 지역은 세계적으로 가장 발전한 해양 석유 및 가스 산업 중 하나이며, 주요 중점 지역인 멕시코만과 알래스카 해안 지역에는 막대한 매장량이 존재합니다. 굴착 깊이가 해마다 깊어짐에 따라 기술적으로 회수 가능한 매장량도 대폭 증가하여 보다 많은 투자를 끌고 있습니다.

미국이 석유 및 가스 생산능력 확대에 많은 투자를 했기 때문에 멕시코만은 세계적인 ROV 수요 핫스팟이 되었습니다. 미국 에너지정보국에 따르면 2022년 멕시코만 연방 앞바다의 석유 천연가스 생산량은 미국의 원유 총 생산량의 약 15%를 차지했습니다. 이 지역은 해양 장비의 배치 밀도가 세계에서 가장 높은 지역 중 하나입니다. 이 지역은 생산 굴착 플랫폼, 해양선박, 파이프라인 네트워크 등 기타 석유 및 가스 인프라로 구성되어 있습니다.

미국은 국방예산에 세계 최대 금액을 투입하고 있어 ROV선 연구개발의 선구자입니다. 2023년 5월 미국 해군은 심해를 순찰하고 소형 잠수정과 무인 정찰기를 배치하는 하이테크 선박에 최대 51억 달러를 투자할 계획을 발표했습니다. 이러한 투자는 북미 ROV 시장을 견인할 것으로 예상됩니다.

ROV 기술의 저가격화가 진행되고 있는 가운데, 미국의 석유 및 가스 생산자는 해저 자산이나 지표의 데이터 취득이나 정기 보수 작업을 실시하기 위해서 ROV 서비스에 투자하고 있습니다. ROV는 다이빙 작업자에 비해 초기 비용이 높지만 동일한 양의 작업을 완료하는 데 필요한 시간이 짧기 때문에 전체 프로젝트의 OPEX를 줄일 수 있습니다.

2024년 5월 미국 해양 서비스 회사인 Edison Chouest는 애버딘에 본사를 둔 원격 무인잠수정 제공업체인 ROVOP을 인수했습니다. 이 인수에 의해 동사가 보유한 ROV는 100대 이상, 자율무인잠수정은 6대가 될 전망입니다. 산업에서의 이러한 활동은 비용 절감과 ROV의 신뢰성 향상으로 이어질 것으로 기대됩니다.

따라서 북미 ROV 산업은 매우 발전하고 있으며 해양건설과 석유 및 가스서비스 수요 증가에 따라 이 산업은 예측기간 동안에도 급성장을 계속할 것으로 예상되어 이 지역의 ROV 수요를 견인하고 있습니다.

ROV 산업 개요

ROV 시장은 세분화되어 있습니다. 시장의 주요 기업(순서부동)에는 DeepOcean AS, DOF Subsea AS, Oceaneering International Inc., Helix Energy Solutions Group Inc., TechnipFMC PLC 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

아메리카, 아시아태평양, 중동, 아프리카에서 석유 및 가스 해양 탐사 활동 증가

해외 재생 가능 기술의 성장

억제요인

여러 지역의 해외 탐사 및 생산 활동 금지

공급사슬 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

유형

작업용 ROV

관측용 ROV

용도

석유 및 가스

방어

기타

심해 해양 탐사

활동

측량

점검, 수리, 유지보수

매설과 트렌치 드릴링

기타 활동

지역

북미

미국

캐나다

기타 북미

유럽

독일

덴마크

노르웨이

영국

이탈리아

노르딕

러시아

프랑스

튀르키예

기타 유럽

아시아태평양

중국

인도

일본

호주

태국

말레이시아

인도네시아

베트남

기타 아시아태평양

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

나이지리아

남아프리카

카타르

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

DeepOcean AS

DOF Subsea AS

Helix Energy Solutions Group Inc.

TechnipFMC PLC

Bourbon Corporation SA

Fugro NV

Oceaneering International Inc.

Saab Seaeye Limited

Forum Energy Technologies Inc.

Saipem SpA

Delta SubSea LLC

ROVOP

List of Other Prominent Players

시장 랭킹/공유(%) 분석

제7장 시장 기회와 앞으로의 동향

진행중인 심해 및 초심해 석유 및 가스 탐사

CSM

영문 목차

영문목차

The ROV Market size is estimated at USD 2.57 billion in 2025, and is expected to reach USD 3.72 billion by 2030, at a CAGR of 7.65% during the forecast period (2025-2030).

Key Highlights

Increasing offshore oil and gas exploration activities in the Americas, Asia-Pacific, and Middle East and Africa and growing offshore renewable technologies are expected to drive the ROV market during the forecast period.

On the other hand, the ban on offshore exploration and production activities in multiple regions is expected to restrain the market.

However, the ongoing deepwater and ultra-deepwater oil and gas discoveries and shale gas explorations are expected to create huge opportunities for ROV deployment over the forecast period.

North America dominated the market worldwide, with most of the demand coming from the United States and Mexico. North America is still leading the world with its advanced, highly maneuverable ROV development.

ROV Market Trends

The Oil & Gas Application Segment is Expected to Dominate the Market

The dependence on oil and gas increases as major economies globally still rely heavily on petroleum-based products. The oil and gas industry displays immense influence in international politics and economics.

According to the Statistical Review of World Energy Data, global oil production in 2022 was 99,877 thousand barrels per day, an increase of 11.1% over the previous year. The increase in global population reflected an increase in primary energy consumption, which stood at 604.04 exajoules in 2022, up from 520.90 exajoules in 2011.

According to the Organization of the Petroleum Exporting Countries (OPEC), in 2023, the global demand for crude oil (including biofuels) amounted to 102.21 million barrels per day. The source expects economic activity and related oil demand to pick up by the end of the year, with the projections suggesting an increase of more than 104 million barrels per day.

Many potential global reserves of hydrocarbons lie beneath the sea, and the hydrocarbon industry has developed techniques suited to the conditions found in offshore sites to find and produce oil and gas successfully. Oil and gas drilling rigs may operate in up to two miles of water depth. Many deepwater wells and pipeline systems rely on unmanned underwater vehicles to help perform installations, inspections, repairs, and maintenance.

Over the past few years, remotely operated vehicles (ROV) have evolved from emerging technology with niche uses to extensive applications in the oil and gas sector.

Capital expenditure in the offshore industry is also increasing significantly worldwide, thus boosting the demand for various advanced technologies, tools, and equipment to perform certain activities. These tools include the ROVs, as they ease the maintenance and inspection work in the offshore sector. Several oil and gas companies are investing in ROVs to support subsea surveys.

For instance, in August 2023, Energean awarded a five-year ROV support contract to Aberdeen-based ROVOP, a global supplier of remotely operated vehicles (ROVs) and services. The company will deploy its ROVs onboard Energean's field support vessel, Energean Star, a converted platform supply vessel.

Technological advancements in ROVs make their operations easier and more efficient, thus boosting their demand in the oil and gas industry.

Overall, the demand for ROVs is expected to increase during the forecast period due to the rapidly growing offshore oil, gas, and energy operations. There have been several improvements in the technologies associated with remote-operated offshore vehicles.

North America is Expected to Dominate the Market

The region has one of the most well-developed offshore oil and gas industries globally, with the primary areas of focus being the vast reserves in the Gulf of Mexico and the offshore Alaska region. With the drilling depths increasing over the years, the volume of technically recoverable reserves has also increased significantly, thus attracting more investments.

As the United States invested heavily in expanding its oil and gas production capacity, the Gulf of Mexico has become a global hotspot for ROV demand. According to the US Energy Information Administration, in 2022, oil and natural gas production in the Federal Offshore Gulf of Mexico accounted for about 15% of total US crude oil production. The region has one of the highest global densities of offshore rig deployment. It comprises other oil and gas infrastructure, such as production and drilling platforms, marine vessels, and pipeline networks.

The United States spends the most globally on its defense budget and has pioneered R&D on ROV vessels. In May 2023, the US Navy announced its plans to invest up to USD 5.1 billion in high-tech vessels that would patrol the deepest reaches of the ocean and deploy mini-subs and drones. Such types of investments are expected to drive the ROV market in North America.

As ROV technology has become increasingly affordable, oil and gas producers in the United States are investing in ROV services to obtain data and perform routine maintenance work on subsea assets and surfaces. Despite the higher upfront cost compared to diving crews, ROVs need less time to complete the same amount of work, which reduces overall project OPEX.

In May 2024, Edison Chouest, a US offshore services company, acquired Aberdeen-based remotely operated vehicle provider ROVOP. The deal will likely boost the company's fleet to over 100 ROVs and six autonomous underwater vehicles. Such activities in the industry are expected to reduce costs and increase ROV reliability.

Thus, the ROV industry in North America is highly developed. As demand increases for marine construction and oil and gas services, the industry is expected to keep growing fast during the forecast period, thereby driving the demand for ROVs in the region.

ROV Industry Overview

The ROV market is semi-fragmented. Some of the major players in the market (in no particular order) include DeepOcean AS, DOF Subsea AS, Oceaneering International Inc., Helix Energy Solutions Group Inc., and TechnipFMC PLC.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Offshore Oil & Gas Exploration Activities in the Americas, Asia-Pacific, and Middle East and Africa

4.5.1.2 Growing Offshore Renewable Technologies

4.5.2 Restraints

4.5.2.1 Ban on Offshore Exploration and Production Activities in Multiple Regions

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Work Class ROV

5.1.2 Observatory Class ROV

5.2 Application

5.2.1 Oil and Gas

5.2.2 Defense

5.2.3 Other Applications

5.2.4 Deep Sea Marine Exploration

5.3 Activity

5.3.1 Survey

5.3.2 Inspection, Repair, and Maintenance

5.3.3 Burial and Trenching

5.3.4 Other Activities

5.4 Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Rest of North America

5.4.2 Europe

5.4.2.1 Germany

5.4.2.2 Denmark

5.4.2.3 Norway

5.4.2.4 United Kingdom

5.4.2.5 Italy

5.4.2.6 NORDIC

5.4.2.7 Russia

5.4.2.8 France

5.4.2.9 Turkey

5.4.2.10 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 China

5.4.3.2 India

5.4.3.3 Japan

5.4.3.4 Australia

5.4.3.5 Thailand

5.4.3.6 Malaysia

5.4.3.7 Indonesia

5.4.3.8 Vietnam

5.4.3.9 Rest of Asia-Pacific

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 United Arab Emirates

5.4.5.3 Nigeria

5.4.5.4 South Africa

5.4.5.5 Qatar

5.4.5.6 Egypt

5.4.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 DeepOcean AS

6.3.2 DOF Subsea AS

6.3.3 Helix Energy Solutions Group Inc.

6.3.4 TechnipFMC PLC

6.3.5 Bourbon Corporation SA

6.3.6 Fugro NV

6.3.7 Oceaneering International Inc.

6.3.8 Saab Seaeye Limited

6.3.9 Forum Energy Technologies Inc.

6.3.10 Saipem SpA

6.3.11 Delta SubSea LLC

6.3.12 ROVOP

6.4 List of Other Prominent Players

6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Ongoing Deepwater and Ultra-deepwater Oil and Gas Discoveries