ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

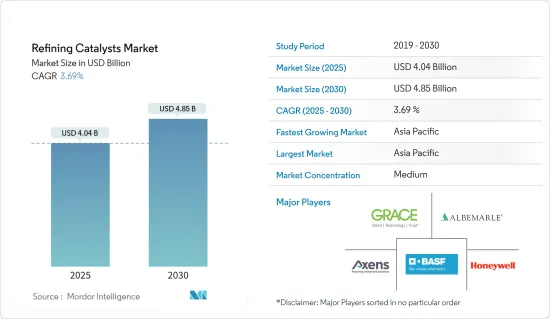

정제 촉매 시장 규모는 2025년에 40억 4,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 3.69%로, 2030년에는 48억 5,000만 달러에 달할 것으로 예측됩니다.

COVID-19의 발생은 석유 정제 제품의 소비 감소로 시장에 부정적인 영향을 미쳤습니다. 그러나 2021년에는 산업이 회복되었고 시장 수요는 회복되었습니다.

주요 하이라이트

단기적으로는 정유소에 대한 투자 증가와 높은 옥탄가 연료에 대한 수요 가속화가 시장을 견인하는 주요 요인입니다.

반면 귀금속 가격 변동은 시장 성장을 방해할 것으로 예상됩니다.

나노촉매에 대한 관심의 변화는 향후 호기성이 될 것으로 예상됩니다.

아시아태평양은 석유 정제 촉매의 최대 시장이며 세계 점유율의 거의 절반을 차지합니다.

정제 촉매 시장 동향

시장을 지배하는 유동 접촉 분해(FCC) 촉매

유동 접촉 분해(FCC) 공정은 원유에서 가벼운 제품을 생산하는 정유 공장에서 중요한 역할을합니다.

FCC 장치는 분해가스유, 경유, 탈아스팔트가스유, 진공/대기압 수지 등 다양한 유형의 원료를 경유, 제트연료, LPG, 등유, 가솔린 등 보다 가볍고 고가치의 제품으로 변환하는 데 도움이 됩니다.

원료는 FCC 장치 내에서 고온·중압으로 가열됩니다. 이와 함께 원료는 촉매와 접촉되어 고비점 탄화수소 액체의 장쇄 분자를 저분자로 분해하고 증기로 회수됩니다.

FCC 공정에서 촉매는 미세 분말로 사용됩니다. 이전에는 비정질 실리카 알루미나와 같은 촉매가 FCC 장치에서 진공 가스 오일을 분해하는 데 사용되었습니다. 그러나 1960년대 초에 제올라이트가 FCC 촉매로서 상업적으로 도입되어 접촉분해의 역사에서 큰 진보를 이루었습니다. 예를 들어, Indian Oil Corp(IOC)는 할리야나 주 파니팟의 정유 공장 확대에 43억 9,000만 달러를 투자할 예정입니다. 이 확대 계획은 2024년 9월까지 완료될 예정이며, 정유소의 생산량을 연간 1,500만 톤에서 2,500만 톤으로 확대합니다.

위와 같은 요인들로부터 FCC 촉매는 예측 기간 동안 정제 촉매 시장 수요를 촉진하는 데 중요합니다.

아시아태평양이 시장을 독점

아시아태평양은 석유 정제용 촉매의 최대 시장이며 세계 점유율의 거의 절반을 차지합니다.

중국은 주요 시장 홀더이며 이 지역의 40% 이상을 차지합니다. 중국의 석유 정화 능력은 세계 정화 능력의 14% 이상을 차지합니다.

또한 인도 최고의 석유 정제 회사 중 하나인 Indian Oil Corp는 향후 5-7년간 기존 브라운필드 정유소를 확대하기 위해 76억 4,000만 달러를 포함한 229억 1,000만 달러의 투자를 계획하고 있습니다.

한국에서는 에틸렌플랜트의 능력 증강과 아시아의 플라스틱 수요 증가로 나프타 사용량은 계속 확대될 것으로 보입니다. 예를 들어 2022년 한국의 연료유 생산량은 약 13억 6,000만 리터로 2021년 대비 28.55% 증가를 보였습니다. 한국의 연료유 생산량은 최근 증가하고 있습니다. 그러므로 이 나라의 연료 생산량 증가는 정제 촉매 시장 수요 증가로 이어질 것으로 예상됩니다.

또한 인도네시아는 수입 석유 제품에 대한 의존도를 최소화하기 위해 석유 정제 능력을 거의 향상시킬 계획을 가속화하고 있습니다. 정부는 2030년까지 국내 석유 생산량을 100만 B/D까지 증가시키려고 합니다. 이를 위해서는 노후화된 유전의 회수 방법을 개선하기 위한 추가 조사와 투자를 촉진해야 합니다.

이상과 같은 요인이 예측기간 동안 이 나라의 석유정제촉매 시장을 견인할 것으로 예상됩니다.

정제 촉매 산업 개요

정제 촉매 시장은 그 특성상 부분적으로 통합되어 있습니다. 이 시장의 주요 기업은 WR Grace & Co.-Conn, Albermarle Corporation, BASF SE, Axens, Honeywell International 등을 포함합니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

고옥탄가 연료 수요 가속화

석유 및 가스 활동 확대

기타 촉진요인

억제요인

귀금속 가격 변동

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(가치 및 수량별 시장 규모)

제품

CoMo

NiMo

알루미나계 귀금속

NiW

제올라이트

기타

프로세스

수소화 처리

가솔린

등유

디젤

진공가스오일

촉매 분해 가솔린

잔류 사료

유체 촉매 분해(FCC)

잔류 유체 촉매 분해(RFCC)

수소화 분해

지역

아시아태평양

중국

인도

일본

한국

아세안 국가

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

러시아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

인수합병, 합작 투자, 협업, 계약

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

Albemarle Corporation

Axens

BASF SE

China Petrochemical Corporation

Exxon Mobil Corporation

Topsoe

Honeywell International

JGC C & C

Johnson Matthey

Royal Dutch Shell PLC

WR Grace & Co.-Conn

Chevron Lummus Global(CLG)

KNT Group

제7장 시장 기회와 앞으로의 동향

OPEC 국가에서의 향후 투자와 생산 능력 증강

기타 기회

KTH

영문 목차

영문목차

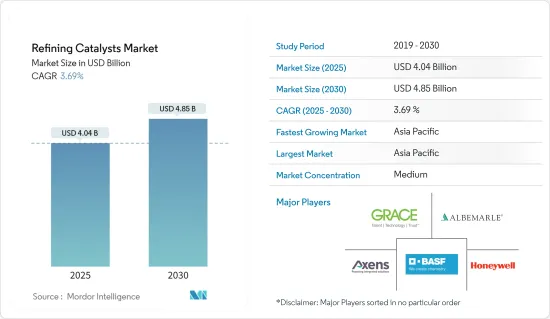

The Refining Catalysts Market size is estimated at USD 4.04 billion in 2025, and is expected to reach USD 4.85 billion by 2030, at a CAGR of 3.69% during the forecast period (2025-2030).

The COVID-19 outbreak negatively impacted the market due to reduced consumption of oil-refined products. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

Over the short term, increasing investment in refineries and the accelerating demand for higher octane fuel are the major factors driving the market studied.

On the flip side, the volatility in precious metal prices is expected to hinder market growth.

The shifting focus toward nanocatalysts will likely act as an opportunity in the future.

Asia-Pacific region accounted for the largest market for refining catalysts, with almost half of the global share, and is also expected to be the fastest-growing market.

Refining Catalysts Market Trends

Fluid Catalytic Cracking (FCC) Catalysts to Dominate the Market

The fluid catalytic cracking (FCC) process plays a crucial role in refineries while producing lighter products from crude oil.

FCC unit helps in converting a variety of feed types, such as cracked gas oil, gas oil, deasphalted gas oils, vacuum/atmospheric resins, and others, into lighter and high-value products, such as diesel oil, jet fuel, LPG, kerosene, and gasoline.

The feedstock is heated at high temperatures and moderate pressure in the FCC unit. Along with this, the feedstock is brought in contact with a catalyst which helps break the long-chain molecules of the high-boiling hydrocarbon liquids into small molecules, which are further collected as vapors.

In the FCC process, the catalysts are used as fine powders. Previously, catalysts, such as amorphous silica-alumina, were used for cracking vacuum gas oils in the FCC unit. However, in the early 1960s, zeolite was commercially introduced as an FCC catalyst, a significant advancement in the history of catalytic cracking. For instance, the Indian Oil Corporation (IOC) intends to spend USD 4.39 billion on expanding its oil refinery in Panipat, Haryana. The extension scheme, which is expected to be completed by September 2024, will expand the refinery's production from 15 million tons annually to 25 million tons annually.

Due to the abovementioned factors, FCC catalysts are important in propelling the market demand for refining catalysts in the forecast period.

Asia-Pacific to Dominate the Market

Asia-Pacific region accounted for the largest market for refining catalysts, with almost half of the global share, and is also expected to be the fastest-growing market.

China is the primary market holder, accounting for more than 40% of the region. China's refinery capacity accounts for over 14% of the world's refining capacity.

Additionally, one of the top oil refiners in India, Indian Oil Corp, plans to invest USD 22.91 billion, including USD 7.64 billion, for expanding its existing brownfield refineries in the next 5 to 7 years.

Naphtha use will likely continue expanding in South Korea due to capacity additions at ethylene plants and the rising demand for plastics in Asia. For instance, in 2022, the production volume of fuel oil in South Korea amounted to around 1.36 billion liters, which shows an increase of 28.55% compared to 2021. Fuel oil production in South Korea has risen in recent years. Therefore, increasing the production volume of fuel in the country is expected to create an upside demand for the refining catalysts market.

Moreover, Indonesia is speeding up plans to nearly increase its oil refining capacity to minimize its reliance on imported petroleum products. By 2030, the government wants to increase domestic petroleum output to 1 million bpd. It seeks to do this by stimulating additional research and investment in improved recovery procedures for aging fields.

All the factors above, in turn, are expected to drive the market for refining catalysts in the country during the forecast period.

Refining Catalysts Industry Overview

The refining catalysts market is partially consolidated in nature. The major players in this market include (not in any particular order) W. R. Grace & Co.-Conn, Albemarle Corporation, BASF SE, Axens, and Honeywell International, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Accelerating Demand for Higher-Octane Fuel

4.1.2 Expansion of Oil and Gas Activities

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Volatility in Precious Metal Prices

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value and Volume)

5.1 Product

5.1.1 CoMo

5.1.2 NiMo

5.1.3 Alumina-based Noble Metal

5.1.4 NiW

5.1.5 Zeolites

5.1.6 Other Products

5.2 Process

5.2.1 Hydrotreating

5.2.1.1 Gasoline

5.2.1.2 Kerosene

5.2.1.3 Diesel

5.2.1.4 Vacuum Gas Oil

5.2.1.5 Catalytic Cracking Gasoline

5.2.1.6 Residual Feed

5.2.2 Fluid Catalytic Cracking (FCC)

5.2.3 Residue Fluid Catalytic Cracking (RFCC)

5.2.4 Hydrocracking

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 ASEAN Countries

5.3.1.6 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 Russia

5.3.3.7 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Albemarle Corporation

6.4.2 Axens

6.4.3 BASF SE

6.4.4 China Petrochemical Corporation

6.4.5 Exxon Mobil Corporation

6.4.6 Topsoe

6.4.7 Honeywell International

6.4.8 JGC C & C

6.4.9 Johnson Matthey

6.4.10 Royal Dutch Shell PLC

6.4.11 W. R. Grace & Co.-Conn

6.4.12 Chevron Lummus Global (CLG)

6.4.13 KNT Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Upcoming Investments and Capacity Additions in OPEC Countries