중국의 전기자동차 배터리 전해액 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

China Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636489

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

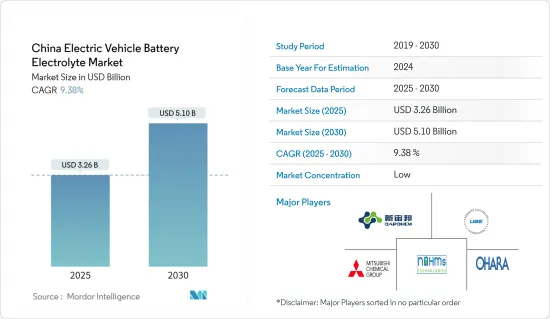

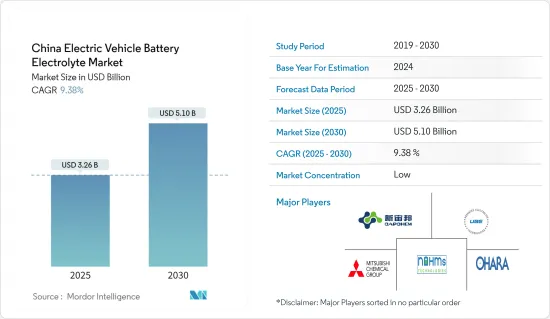

중국의 전기자동차 배터리 전해액 시장 규모는 2025년에 32억 6,000만 달러, 2030년에는 51억 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 9.38%에 달할 것으로 예측됩니다.

주요 하이라이트

장기적으로 중국에서 BEV, PHEV, HEV를 포함한 전기차 이용 증가와 전기차 이용을 촉진하기 위한 유리한 정부 보조금(면세 정책 등)이 시장 성장을 가속할 것으로 예측됩니다.

반대로, 배터리 제조를 위한 원료 매장량 부족은 전기자동차용 배터리 전해질 시장에 부정적인 영향을 미칠 것으로 예상됩니다.

그럼에도 불구하고, 중국의 배터리 시험소(IE China Automotive Battery Research Institute, SGS China)에서 진행 중인 전해질 재료의 조사와 진보는 시장 성장 기회를 제공할 수 있습니다.

중국 전기자동차 배터리 전해액 시장 동향

리튬이온 배터리가 시장을 독점할 전망

리튬 이온 배터리는 수명이 길기 때문에 전기자동차(EV)의 전원으로 사용되며 배터리 교체 빈도가 줄어듭니다. 리튬 이온 배터리는 납이나 카드뮴과 같은 유해 물질을 포함하지 않으므로 다른 배터리와 달리 환경 친화적이고 깨끗하고 안전합니다. 또한, 이러한 배터리는 빠른 가속과 고속 주행이 요구되는 EV에 필수적인 강력한 출력을 제공합니다.

2023년 6월 중국 배터리 제조업체인 Gotion High-Tech는 전기자동차용으로 1회 충전으로 621마일이라는 경이적인 항속 거리를 자랑하는 리튬-망간-철-인산염(LMFP) 배터리를 발표했습니다. 이전에는 이 항속 거리는 주로 고가의 니켈 코발트 배터리로 달성되었습니다. Gotion은 이 회사의 LMFP 배터리가 240Wh/kg에 이르며 킬로와트 시간당 달러 기준으로 표준 LFP 배터리보다 5% 낮은 가격이 될 것으로 예상하고 있습니다.

2023년 현재 중국은 배터리 전기자동차(BEV) 분야에서 압도적인 지위를 차지하고 있으며, 판매 대수는 약 540만대에 이릅니다. 양극과 음극 사이에 양의 리튬 이온을 운반하는 전해액은 매우 중요한 역할을 하고 있기 때문에 EV에 리튬 이온 배터리의 채용이 진행됨에 따라 침투 전해액 수요가 높아질 것으로 예상됩니다.

2024년 7월, 중국 연구팀은 저밀도 및 음극 적합성을 특징으로 하는 비용 효율적인 황화물 고체 전해질을 개발하여 고체 배터리 기술을 비약적으로 발전시켰습니다. 이러한 전고체 배터리는 현재 리튬 이온 배터리가 직면하고 있는 용량과 안전성의 과제에 대처하는 태세를 갖추고 있습니다.

예측에 따르면 2025년까지 중국 배터리 제조업체는 4,800기가와트(GWh)라는 놀라운 배터리를 생산하게 됩니다. 충방전 공정에서 배터리 전해액의 중요한 역할을 감안하면, 이 배터리 생산의 급증은 배터리 전해액 재료 수요를 국가 전체에서 증폭시킬 것입니다.

그 결과, 전기자동차에 리튬 이온 배터리의 채용이 증가하고, 그 가격이 급락하고 있기 때문에 리튬 이온 배터리 분야는 향후 수년간 크게 성장할 전망입니다.

전기차 채용 증가가 시장을 견인할 전망

중국은 플러그인 하이브리드 전기자동차(EV)의 주요 시장이며, 다양한 용도의 배터리를 대량 생산하고 있는 것으로 세계적으로 인정되고 있습니다. 정부가 배기가스가 없는 교통을 향해 강력하게 추진하고 있기 때문에 중국은 향후 수년간 지배적인 지위를 유지할 것으로 보입니다.

플러그인 하이브리드 자동차는 향후 10년간 보급될 전망이며, 해외 자동차 제조업체는 중국 브랜드에 전문 지식을 요구하게 되었습니다. 특히 중국의 대기업 자동차 제조업체인 BYD는 2008년 세계 최초의 플러그인 하이브리드 모델인 F3DM 세단을 발표해 화제가 됐습니다.

중요한 움직임으로 중국 정부는 2024년 5월 전기차(EV)용 차세대 배터리 기술 개척에 약 8억 4,500만 달러를 투자할 계획을 발표했습니다. CATL(세계 최대의 배터리 제조업체)이나 BYD, Geely 등의 대기업 자동차 제조업체를 포함한 6개사가, 전고체 배터리(ASSB)를 발전시키기 위해 정부의 지원을 받게 되었습니다.

중국 기차공업협회(CAAM)가 2023년 8월에 보고한 바와 같이 중국에서는 905만대의 승용차용 전기자동차가 판매되고, 그 내역은 배터리 전용 전기자동차(BEV)가 626만대, 플러그인 하이브리드차(PHEV)가 279만대가 되고 있습니다. 2023년에는 플러그인 전기자동차(BEV와 PHEV 모두)가 중국의 자동차 총 판매 대수의 37%를 차지하고 시장 점유율은 BEV가 25%, PHEV가 12%입니다.

2024년 6월, 중국 산업 정보화부는 배터리 부문에 대한 새로운 지침을 발표했습니다. 이 지침은 전기자동차용 리튬이온 배터리의 품질과 기술 혁신을 높이는 것을 목적으로 하고 있으며, 기업에 대해 단순히 생산능력을 확대하는 것, 특히 배터리 전해질 용액의 기술 혁신을 강화하는 것에 축발을 옮기도록 촉구하고 있습니다.

2030년까지 중국에서는 5,000만대의 전기자동차가 보급될 것으로 예상되고 있으며, 전기자동차 충전을 위한 연간 전력 수요는 200TWh에 이릅니다. 이러한 급증하는 수요는 중국 내 전기차용 배터리 전해액의 진보 가능성을 강조하고 있습니다.

EV의 급속한 보급과 현재 진행 중인 기술적 진보를 감안할 때, 중국은 당분간 시장의 우위를 유지하는 태세를 정돈하고 있습니다.

중국 전기자동차 배터리 전해액 산업 개요

중국의 전기자동차 배터리 전해액 시장은 반파편화 상태입니다. 시장에 진입하는 주요 기업(순부동)에는 Advanced Electrolyte Technologies LLC, Mitsubishi Chemical Holdings, Shenzhen Capchem Technology, Nohms Technologies Inc., Ohara Corporation 등이 있습니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측(단위: 달러)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

BEV, PHEV, HEV를 포함한 전기자동차의 이용 증가

전기자동차의 이용을 촉진하는 유리한 정부 정책

억제요인

배터리 재료 공급 체인 격차

공급망 분석

PESTLE 분석

투자 분석

제5장 시장 세분화

배터리 유형

리튬 이온 배터리

납축 배터리

기타 배터리 유형

전해액 유형

액체 전해액

겔 전해액

고체 전해액

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Advanced Electrolyte Technologies LLC

Mitsubishi Chemical Holdings

Shenzhen Capchem Technology Co., Ltd

Nohms Technologies Inc

Ohara Corporation

BASF SE

LG Chem Ltd

Targray Industries Inc.

SGS China

Ningbo Shanshan Co., LTD

시장 랭킹/공유(%) 분석

기타 주요 기업 목록

제7장 시장 기회와 앞으로의 동향

선진 전해액 재료의 연구 개발

JHS

영문 목차

영문목차

The China Electric Vehicle Battery Electrolyte Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 5.10 billion by 2030, at a CAGR of 9.38% during the forecast period (2025-2030).

Key Highlights

Over the long term, the increasing usage of electric vehicles, including BEVs, PHEVs, and HEVs, and favorable government subsidies (i.e. tax exemption policy) to promote the usage of electric vehicles in the China are expected to drive the market's growth.

Conversely, the lack of raw material reserves for battery manufacturing is expected to negatively impact the electric vehicle battery electrolyte market.

Nevertheless, the ongoing research and advancement in electrolyte material in Chinese battery testing labs i.e, China Automotive Battery Research Institute Co., Ltd., SGS China may offer opportunities for market growth.

China Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery is Expected to Dominate the Market

Lithium-ion batteries, favored for their extended lifespan, are the go-to power source for electric vehicles (EVs), leading to less frequent battery replacements. Unlike some other battery types, lithium-ion variants are deemed environmentally friendly, as they steer clear of toxic materials such as lead or cadmium, making them a cleaner and safer option. Furthermore, these batteries deliver a robust power output, essential for EVs that demand swift acceleration and high speeds.

In June 2023, Gotion High-Tech, a Chinese battery manufacturer, introduced a lithium-manganese-iron-phosphate (LMFP) battery, boasting an impressive range of 621 miles per charge for electric vehicles. Previously, this range was predominantly achieved by pricier nickel-cobalt batteries. Gotion anticipates its LMFP battery will reach 240 Wh/kg and be priced 5% lower than the standard LFP battery on a USD per kilowatt-hour basis.

As of 2023, China stands as a dominant player in the battery electric vehicle (BEV) arena, with sales hitting approximately 5.4 million units. The rising adoption of lithium-ion batteries in EVs is set to boost the demand for penetration electrolyte solutions, given the electrolyte's pivotal role in ferrying positive lithium ions between the cathode and anode.

In July 2024, a team of Chinese researchers made strides in solid-state battery technology by crafting a cost-effective sulfide solid electrolyte, characterized by its low density and stellar anode compatibility. These all-solid-state batteries are poised to address the capacity and safety challenges currently faced by lithium-ion batteries.

Forecasts suggest that by 2025, Chinese battery manufacturers will churn out a staggering 4,800 giga-watt hours (GWh) of batteries. Given the critical role of battery electrolytes in the charging and discharging process, this surge in battery production is set to amplify the demand for battery electrolyte materials throughout the nation.

Consequently, with the rising adoption of lithium-ion batteries in electric vehicles and their plummeting prices, the lithium-ion battery segment is poised for substantial growth in the coming years.

Increasing Adoption of Electric Vehicles is expected to Drive the Market

China stands as the leading market for plug-in hybrid electric vehicles (EVs) in the region and is globally recognized for its mass production of batteries across various applications. With the government's strong push towards emission-free transportation, China is set to uphold its dominant position in the coming years.

Plug-in hybrid vehicles are poised to gain traction in the next decade, leading foreign carmakers to seek expertise from Chinese brands. Notably, BYD, a prominent Chinese player, made headlines in 2008 by launching the world's inaugural plug-in hybrid model, the F3DM sedan.

In a significant move, the Chinese government, in May 2024, unveiled plans to invest approximately USD 845 million into pioneering next-generation battery technologies for electric vehicles (EVs). Six companies, including CATL (the globe's largest battery manufacturer) and major automakers like BYD and Geely, have been greenlit for government backing to advance all-solid-state batteries (ASSBs).

As reported by the China Association of Automobile Manufacturers (CAAM) in August 2023, China has seen sales of 9.05 million passenger electric vehicles, breaking down to 6.26 million battery-only EVs (BEVs) and 2.79 million plug-in hybrid electric vehicles (PHEVs). In 2023, plug-in electric vehicles (both BEVs and PHEVs) accounted for 37% of China's total automotive sales, with market shares of 25% for BEVs and 12% for PHEVs.

In June 2024, China's Ministry of Industry and Information Technology rolled out fresh directives for the battery sector. These guidelines aim to elevate the quality and innovation of lithium-ion batteries for electric vehicles, urging firms to pivot from merely expanding production capacity to enhancing technological innovations, especially in battery electrolyte solutions.

Looking ahead, by 2030, China anticipates hosting 50 million electric vehicles, translating to a staggering annual electricity demand of 200 TWh for EV charging. This burgeoning demand underscores the potential for advancements in electric vehicle battery electrolytes within the nation.

Given the surging adoption of EVs and ongoing technological strides, China is poised to retain its market dominance in the foreseeable future.

China Electric Vehicle Battery Electrolyte Industry Overview

The China Electric Vehicle Battery Electrolyte Market is semi-fragmented. Some of the major companies operating in the market (in no particular order) include Advanced Electrolyte Technologies LLC, Mitsubishi Chemical Holdings, Shenzhen Capchem Technology Co., Ltd, Nohms Technologies Inc., and Ohara Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 The Increasing Usage of Electric Vehicles, including BEVs, PHEVs, and HEVs

4.5.1.2 Favorable government policies to promote the usage of electric vehicles

4.5.2 Restraints

4.5.2.1 The Supply chain gap in battery materials

4.6 Supply Chain Analysis

4.7 PESTLE Analysis

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-Ion Batteries

5.1.2 Lead-Acid Batteries

5.1.3 Other type of Batteries

5.2 Electrolyte Type

5.2.1 Liquid Electrolyte

5.2.2 Gel Electrolyte

5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements