Solid-State Electrolytes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1755190

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

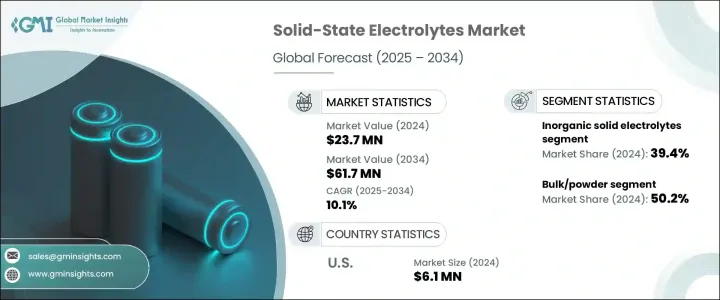

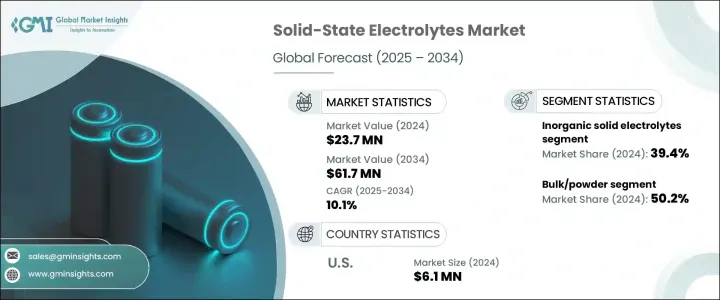

세계의 고체 전해질 시장은 2024년에는 2,370만 달러로 평가되었으며, 보다 높은 에너지 밀도, 강화된 안전성 및 개선된 성능을 제공하는 고급 배터리 솔루션에 대한 수요 증가로 인해 CAGR 10.1%를 나타내 2034년에는 6,170만 달러에 달할 것으로 예측되고 있습니다.

고체 전해질은 리튬 이온 배터리에 사용되는 기존의 액체 또는 겔 기반 전해질을 대체하여 보다 안전하고 효율적인 대안을 제공합니다. 폭주 및 화재 사고의 위험을 줄입니다. 보다 빠른 충전을 지원하고 배터리 수명을 연장 할 수 있기 때문에 전기자동차, 가전제품, 차세대 에너지 저장 시스템에 매우 중요한 기술 혁신이됩니다.

세라믹 및 폴리머 복합 황화물 이온 도체를 중심으로 한 재료의 끊임없는 기술 혁신이 시장을 밀어 올려 이온 전도성과 재료 적합성이 향상되고 있습니다. 특히 EV의 보급과 청정 에너지 기술에 대한 정책 지원에 보다 안전하고 대용량의 배터리에 대한 수요가 높아짐에 따라 고체 배터리는 컨셉에서 상업화로 이행하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

2,370만 달러

예측 금액

6,170만 달러

CAGR

10.1%

무기 고체 전해질 부문은 2024년에 39.4%의 점유율을 차지했습니다. 합성은 에너지 밀도를 높이고 배터리 수명을 연장합니다.

고체 전해질 시장의 벌크 또는 분말형 부문은 2024년에 50.2%의 점유율을 차지했습니다. 효율적인 대량 생산을 지원합니다. 리튬 티오 포스페이트 및 가닛 계 재료와 같은 분말 화합물은 탁월한 이온 전도성과 기계적 강도로 차세대 배터리 시스템의 파일럿 프로젝트에서 점점 더 많이 사용되고 있으며 상업적 스케일링에 가장 적합한 선택입니다.

2024년 미국의 고체 전해질 시장 규모는 610만 달러에 달했습니다. 국내의 전지기술 혁신을 목적으로 한 연방정부의 자금원조와 정책이니셔티브는 이 나라가 시장을 선도하는데 중요한 역할을 하고 있습니다. 프로그램 등의 법률 아래, 보조금, 세액공제, 연구지원을 통해 개발을 가속시키고 있습니다.

고체 전해질 시장의 유력 기업은 삼성 SDI, Toyota Motor, LG Chem, QuantumScape, ProLogium Technology등이 있습니다. 시장에서 프레즌스를 확대하기 위해, 이러한 기업은 고체 전해질 화학을 진보시키고 전지 성능을 향상시키기 위한 연구 개발에 투자하고 있습니다. 연구기관과 정부기관과의 전략적 파트너십은 프로토타입 개발과 스케일링 프로세스를 가속화합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

밸류체인에 영향을 주는 요인

이익률 분석

파괴적 혁신

향후 전망

제조업체

유통업체

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS 코드) 참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

주요 수출국

주요 수입국

영향요인

시장 성장 촉진요인

고에너지 밀도 전지 수요 증가

배터리의 안전성에 대한 관심 증가

전기자동차의 보급 증가

고체 전해질 재료의 진보

시장 성장 억제요인

높은 제조 비용

생산 규모 확대에 있어서의 기술적 과제

인터페이스 안정성 문제

첨단 액체 전해질과의 경쟁

시장 기회

새로운 고체 전해질 재료의 개발

웨어러블 디바이스의 새로운 용도

재생에너지 저장과의 통합

정부의 대처와 자금

시장의 과제

실온에서 높은 이온 전도성을 실현

전극-전해질 계면의 문제에 대처

리튬 덴드라이트의 형성과 성장

대량 생산과 비용 절감

규제 틀과 정부의 대처

배터리 재료의 안전 규제

환경규제

정부의 자금 지원 및 조사 이니셔티브

지역에 의한 규제의 차이

미래 규제 전망

성장 가능성 분석

가격 분석(USD/톤), 2021-2034년

제조 및 생산 공정

고체 상태 합성

솔-젤 처리

기계 화학적 합성

박막 증착 기술

폴리머 처리 방법

확장 가능한 제조 접근 방식

재료 특성 평가 기술

X선 회절 분석

임피던스 분광법

주사형 전자현미경

핵자기 공명

열분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

시장 점유율 분석

전략 틀

합병과 인수

합작투자와 콜라보레이션

신제품 개발

확대 전략

경쟁 벤치마킹

공급업체 상황

경쟁 포지셔닝 매트릭스

전략적 대시보드

특허 분석과 혁신평가

신규 참가자 시장 진출 전략

배전망 분석

제5장 시장 추계·예측 : 재료별(2021-2034년)

주요 동향

무기 고체 전해질

산화물계 전해질

LISICON형

NASICON형

페로브스카이트형

가넷형(LLZO)

기타

황화물계 전해질

티오-리시콘

아르지로이트형

Li2S-P2S5 유리-세라믹

기타

할로겐화물계 전해질

기타

폴리머계 고체 전해질

폴리에틸렌 옥사이드(PEO) 기반

폴리불화비닐리덴(PVDF) 기반

폴리카보네이트 기반

기타

복합 고체 전해질

폴리머-세라믹 복합재료

폴리머-무기염 복합재료

세라믹-세라믹 복합재료

기타

하이브리드 고체 전해질

제6장 시장 추계·예측 : 형태별(2021-2034년)

주요 동향

벌크/분말

박막

시트/멤브레인

기타

제7장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

전기자동차

승용차

상용차

이륜차

가전

스마트폰 및 태블릿

노트북 및 컴퓨터

웨어러블 디바이스

기타

에너지 저장 시스템

주택용

상업용

유틸리티 스케일

의료기기

이식형 의료기기

휴대형 의료기기

기타

항공우주 및 방위

기타

제8장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제9장 기업 프로파일

Ampcera

Cymbet Corporation

Idemitsu Kosan

Ilika

ION Storage Systems

LG Energy

Murata Manufacturing

NEI Corporation

Ohara

ProLogium Technology

QuantumScape

Samsung SDI

Solid Power

TDK Corporation

Toyota Motor Corporation

KTH

영문 목차

영문목차

The Global Solid-State Electrolytes Market was valued at USD 23.7 million in 2024 and is estimated to grow at a CAGR of 10.1% to reach USD 61.7 million by 2034, driven by rising demand for advanced battery solutions that offer higher energy density, enhanced safety, and improved performance. Solid-state electrolytes replace the conventional liquid or gel-based electrolytes used in lithium-ion batteries, providing a safer and more efficient alternative. These materials address major concerns like flammability and leakage, reducing the risks of thermal runaway and fire incidents. Their ability to support faster charging and extend battery lifespan makes them a crucial innovation for electric vehicles, consumer electronics, and next-generation energy storage systems.

Continuous innovation in materials-particularly ceramic and polymer composite sulfide ion conductors-has pushed the market forward, improving ionic conductivity and material compatibility. As demand for safer, high-capacity batteries rises, especially with broader EV adoption and policy support for clean energy technologies, solid-state batteries are moving from concept to commercialization. Supportive regulations, combined with technological advancement, create a strong foundation for market expansion.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$23.7 Million

Forecast Value

$61.7 Million

CAGR

10.1%

The inorganic solid electrolytes segment accounted for a 39.4% share in 2024. These materials are preferred for their excellent ionic conductivity, thermal resilience, and structural integrity, essential in high-stress environments such as electric vehicle batteries and grid-scale energy storage systems. Their stability and compatibility with lithium metal anodes enhance energy density and extend battery life. Inorganic electrolytes-especially sulfide and oxide-based variants-are also non-combustible, eliminating the fire risks associated with traditional liquid systems. Their integration into current production workflows helps streamline manufacturing and accelerates deployment across energy storage applications.

The bulk or powder form segment in the solid-state electrolytes market held a 50.2% share in 2024. The widespread use of powdered electrolytes stems from their versatility and ease of integration with various electrode materials. This form allows for better structural compactness and active material incorporation, supporting efficient mass production for automotive and stationary applications. Powdered compounds such as lithium thiophosphate and garnet-based materials are increasingly used in pilot projects for next-generation battery systems, due to their outstanding ionic conductivity and mechanical strength, making them an optimal choice for commercial scaling.

U.S. Solid-State Electrolytes Market generated USD 6.1 million in 2024. Federal funding and policy initiatives aimed at domestic battery innovation play a key role in the country's market leadership. Major government programs are accelerating development through grants, tax credits, and research support under legislation such as the Inflation Reduction Act and Battery Manufacturing and Recycling Grant Program. These efforts boost innovation in the solid-state battery segment and encourage U.S.-based companies to scale up operations, reduce import dependence, and create robust local supply chains.

Prominent players in the Solid-State Electrolytes Market include Samsung SDI, Toyota Motor Corporation, LG Chem, QuantumScape, and ProLogium Technology. To expand their market presence, these companies invest in R&D to advance solid electrolyte chemistry and enhance battery performance. Collaborations with automotive OEMs and energy storage firms help secure long-term contracts and early adoption opportunities. Strategic partnerships with research institutions and government entities accelerate prototype development and scaling processes. Firms focus on streamlining manufacturing capabilities and deploying pilot production lines to ensure early-mover advantage in commercial solid-state battery deployment.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Base estimates & calculations

1.3 Forecast calculation

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factor affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.2 Trump administration tariffs

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.1.1 Price volatility in key materials

3.2.2.1.2 Supply chain restructuring

3.2.2.1.3 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.2.1 Price transmission to end markets

3.2.2.2.2 Market share dynamics

3.2.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS Code) Note: the above trade statistics will be provided for key countries only.

3.3.1 Major exporting countries

3.3.2 Major importing countries

3.4 Impact forces

3.4.1 Market drivers

3.4.1.1 Growing demand for high-energy density batteries

3.4.1.2 increasing focus on battery safety

3.4.1.3 Rising adoption of electric vehicles

3.4.1.4 Advancements in solid-state electrolyte materials

3.4.2 Market restraints

3.4.2.1 High manufacturing costs

3.4.2.2 technical challenges in scaling production

3.4.2.3 Interface stability issues

3.4.2.4 Competition from advanced liquid electrolytes

3.4.3 Market opportunities

3.4.3.1 Development of new solid electrolyte materials

3.4.3.2 Emerging applications in wearable devices

3.4.3.3 Integration with renewable energy storage

3.4.3.4 Government initiatives and funding

3.4.4 Market challenges

3.4.4.1 Achieving high ionic conductivity at room temperature