인도의 전기자동차 전지 전해액 : 시장 점유율 분석, 산업 동향 & 통계, 성장 예측(2025-2030년)

India Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636488

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

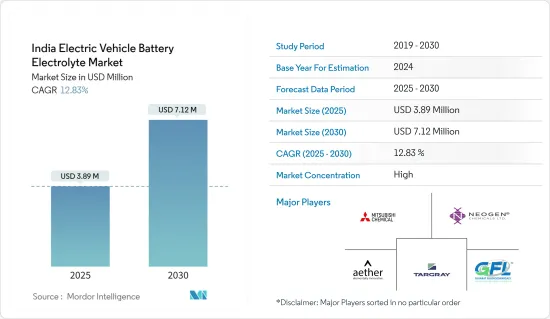

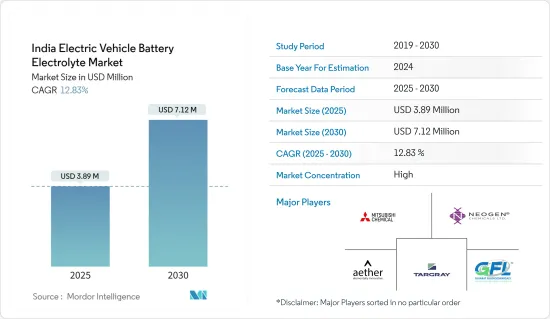

인도의 전기자동차 전지 전해액 시장 규모는 2025년에 389만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 12.83%로, 2030년에는 712만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 전기차의 보급 확대, 정부 시책, 관련 투자가 시장을 견인할 것으로 보입니다.

한편, 원료의 입수성과 공급에 관한 과제는 시장에 부정적인 영향을 미칠 것으로 예상됩니다.

전해질 재료의 지속적인 연구개발은 시장에 미래 성장 기회를 가져올 것으로 예상됩니다.

리튬 이온 전지 유형은 조사 기간 동안 인도의 전기자동차 전지 전해액의 최대 시장이 될 것으로 예상됩니다.

인도 전기자동차 전지 전해액 시장 동향

리튬 이온 전지가 크게 성장

리튬 이온 전지는 전기자동차(EV) 혁명의 최전선에 있으며 뛰어난 에너지 밀도와 긴 수명으로 자동차 산업이 지속 가능한 에너지 솔루션으로 전환하는 데 매우 중요한 역할을 합니다.

2023년 4월, Neogen Chemicals는 일본의 MU Ionic Solutions Corporation과 제휴하여 제조 능력을 강화했습니다. 이 계약을 통해 Neogen은 MUIS의 독자적인 제조 기술을 활용할 수 있게 되었습니다. 이러한 전략적 움직임으로 Neogen은 인도에서 연간 3만 MT의 전해질 용액을 생산할 수 있게 되었고 자국 내 리튬 이온 전지 제조업체 수요 증가에 직접 대응할 수 있게 되었습니다. 이러한 신흥국 시장의 개척은 전기자동차 전지 전해액 시장의 성장을 가속할 것입니다.

마찬가지로 2023년 4월 Gujarat Fluorochemicals(GFL)는 인도에서 전지와 전해조 생산을 위해 3년간 6억 달러의 투자 계획을 발표했습니다. 구자라트 주 다해지에 위치한 동사의 시설은 리튬 이온 전지의 주요 전해질 염인 육불화인산리튬(LiPF6)의 생산을 시작합니다. 연간 1,800톤의 생산능력을 가진 GFL은 리튬 이온 전지의 급증하는 수요에 대응하여 규모를 확대할 계획이며 이는 인도 내 전기차용 전해액 시장의 확대를 뒷받침하고 있습니다.

2023년 12월, Ami Organics는 세계 유명 전해질 기업과 각서를 체결하여 구자라트 주에서 전지 셀과 전해질 생산로를 개척하였습니다. 인도의 '메이크업 인디아' 이니셔티브에 대한 노력을 보여주기 위해 Ami Organics는 전해액 전용 생산 시설에 3,580만 달러를 투자합니다.

최근 몇 년간 리튬 이온 전지 가격이 급락하고 관련 부품에 대한 수요가 높아지고 있습니다. Bloomberg NEF의 보고서에 따르면 2023년 리튬 이온 전지의 평균 가격은 139달러/KWh로 2014년 이후 5배라는 엄청난 가격 인하를 보이고 있습니다. 이러한 가격 하락은 리튬 이온 전지의 채택을 가속화하고 전해질 시장의 밝은 미래를 시사합니다.

앞서 언급한 리튬 이온 전지와 전해액 생산의 동향을 감안하면 인도의 전기자동차 전지 전해액 시장은 향후 수년간 크게 성장할 가능성이 있습니다.

전기차의 보급을 촉진하는 정부 장려책

전기자동차(EV)는 운송부문에서 이산화탄소 배출을 억제하는데 매우 중요한 역할을 하고 있습니다. 인도 정부의 FAME 인도 계획은 전기자동차와 하이브리드 자동차의 채용을 적극적으로 추진하고 2030년까지 전체 수송 수단의 30%를 전기자동차로 대체하는 것을 목표로 하고 있습니다. 이러한 전기차 도입의 급증은 인도의 전기차용 전지 전해질 시장에 이익을 가져올 것으로 예상됩니다.

이와 병행하여 인도의 생산 연계 인센티브(PLI) 제도는 30억 9,000만 달러의 예산이 승인되어 자국 내 전기차 제조를 강화하고 있습니다. PLI 제도는 자동차 제조업체에게 연간 전기자동차 판매액의 13-15%의 정부 보조금을 지급하는 것입니다. 이 우대 정책은 EV 판매 확대를 목표로 할 뿐만 아니라 제조업체가 신기술 투자에 따른 비용을 줄일 수 있도록 지원하고 있습니다. 결과적으로 이 이니셔티브는 인도 전역에서 전기자동차 전지의 전해액 수요에 박차를 가하고 있습니다.

또한 Electric Mobility Promotion Scheme(EMPS)은 인도의 전기자동차 제조 생태계를 육성하는 동시에 전기 이륜차 및 전기 삼륜차의 사용을 장려합니다. EMPS에서는 전지 용량 1킬로와트 당 약 60달러의 보조금이 지급됩니다. 단, 이 보조금은 공장 출하 가격(세금 별도 차량 가격)의 15% 또는 특정 상한(이륜차는 약 120 USD, e-인력거와 e-카트는 약 300 USD, e-오토바이는 약 600 USD)으로 제한됩니다. 이러한 노력으로 인도 전기자동차 전지의 전해질 등의 부품 수요가 높아질 것으로 예상됩니다.

또한, 인도의 전기자동차 시장은 최근 몇 년동안 지속적으로 상승 기조를 보이고 있습니다. 국제에너지기구의 데이터에 따르면 인도의 전기차 판매량은 2023년 8만 2,000대에 달하고, 전년 대비 70% 증가하는 경이로운 성장세를 보였습니다. 이러한 기세를 감안하면 인도에서 전기차 수요가 더욱 늘어날 것으로 예상되고 전해액 시장도 활성화될 것으로 예상됩니다.

이러한 동향과 시장 개척을 고려하면, 인도의 전기자동차 전지 전해질 시장 전망은 유망하다고 생각됩니다.

인도 전기자동차 전지 전해액 산업 개요

인도 전기자동차 전지 전해액 시장은 부분 통합되어 있습니다. 주요 기업(순서부동)에는 Neogen Chemicals, Gujarat Fluorochemicals, Mitsubishi Chemical Group Corporation, Targray Technology International Inc, Aether Industries Limited 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기차 도입을 지원하는 정부 시책

리튬 이온 전지 가격 저하

억제요인

원료 가용성과 공급 제한

공급망 분석

PESTLE 분석

투자 분석

제5장 시장 세분화

전지 유형

납축전지

리튬 이온 전지

기타

전해질 유형

액체 전해질

겔 전해질

고체 전해질

제6장 경쟁 구도

인수합병(M&A), 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

Ami Organics Electrolytes Private Ltd.

Neogen Chemicals

Gujarat Fluorochemicals

3M India

BASF Shanshan Battery Materials Co.

Targray Technology International Inc

Aether Industries Limited

Tatva Chintan Pharma Chem Limited

Mitsubishi Chemical Group

SK Industries

제7장 시장 기회와 앞으로의 동향

전해질 재료 연구개발

CSM

영문 목차

영문목차

The India Electric Vehicle Battery Electrolyte Market size is estimated at USD 3.89 million in 2025, and is expected to reach USD 7.12 million by 2030, at a CAGR of 12.83% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the increasing adoption of electric vehicles, government policies, and associated investments in them are likely to drive the market.

On the other hand, challenges associated with raw material availability and supply is expected to have a negative impact on the market.

Continuous research and development in electrolyte materials is expected to provide future growth opportunities for the market.

The lithium-ion battery type is expected to be the largest market for the India Electric Vehicle Battery Electrolyte during the study period.

India Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery to Grow Significantly

Lithium-ion batteries are at the forefront of the electric vehicle (EV) revolution. Their superior energy density and extended life cycle make them pivotal to the automotive industry's shift toward sustainable energy solutions.

In April 2023, Neogen Chemicals bolstered its manufacturing capabilities through a partnership with Japan's MU Ionic Solutions Corporation. The agreement allows Neogen to leverage MUIS's proprietary manufacturing technology. This strategic move positions Neogen to produce 30,000 MT annually of electrolyte solutions in India, directly addressing the rising demand from domestic lithium-ion cell manufacturers. Such developments are poised to fuel the growth of the electric vehicle battery electrolyte market.

Similarly, in April 2023, Gujarat Fluorochemicals (GFL) announced a USD 600 million investment plan over three years, targeting battery and electrolyzer production in India. Their facility in Dahej, Gujarat, will commence operations with the production of Lithium hexafluorophosphate (LiPF6), a crucial electrolyte salt for lithium-ion batteries. Starting with a production capacity of 1800 tonnes per annum (tpa), GFL plans to scale up in response to the burgeoning demand for lithium-ion batteries, underscoring the expanding electric vehicle battery electrolyte market in India.

In December 2023, Ami Organics entered into a Memorandum of Understanding with a prominent global electrolyte firm, paving the way for battery cell and electrolyte production in Gujarat. Demonstrating its commitment to India's "Make in India" initiative, Ami Organics is investing USD 35.8 million in a dedicated electrolyte production facility.

Over the years, lithium-ion battery prices have plummeted, driving up demand for related components. Bloomberg NEF reports that the average lithium-ion battery price in 2023 was USD 139 USD/KWh, marking a staggering fivefold reduction since 2014. This price drop has accelerated the adoption of lithium-ion batteries, suggesting a bright future for the electrolyte market.

Given the aforementioned trends in lithium-ion batteries and electrolyte production, the electric vehicle battery electrolyte market in India is poised for significant growth in the coming years.

Government Incentives to Raise Adoption of Electric Vehicles

Electric vehicles (EVs) play a pivotal role in curbing carbon emissions from the transportation sector. The Indian government's FAME India scheme actively promotes the adoption of electric and hybrid vehicles, targeting a transition of 30% of total transportation to electric vehicles by 2030. This anticipated surge in electric vehicle adoption is poised to benefit India's electric vehicle battery electrolyte market.

In a parallel effort, India's Production Linked Incentive (PLI) scheme, with an approved budget of USD 3.09 billion, has bolstered domestic electric vehicle manufacturing. The PLI scheme offers automakers a government grant ranging from 13-15% of their annual electric vehicle sales value. This incentive not only aims to amplify EV sales but also assists manufacturers in mitigating the costs associated with new technology investments. Consequently, this initiative has spurred demand for electrolytes in electric vehicle batteries across India.

Furthermore, the Electric Mobility Promotion Scheme (EMPS) champions the use of electric two-wheelers and three-wheelers while simultaneously nurturing India's electric vehicle manufacturing ecosystem. Under the EMPS, a subsidy of approximately USD 60 is granted for each kilowatt hour of battery capacity. However, this subsidy is limited to 15% of the ex-factory cost (the vehicle's price at the factory gate before taxes) or specific caps: around USD 120 for two-wheelers, USD 300 for e-rickshaws and e-carts, and USD 600 for e-autos, whichever is lower for each category. Such initiatives are anticipated to elevate the demand for components like electrolytes in India's electric vehicle batteries.

Additionally, India's electric vehicle market has shown a consistent upward trajectory in recent years. Data from the International Energy Agency reveals that electric car sales in India reached 82,000 units in 2023, marking a staggering 70% surge from the prior year. Given this momentum, the demand for electric vehicles in India is poised for further growth, which in turn is set to invigorate the electrolyte market.

In light of these trends and developments, the outlook for India's Electric Vehicle Battery electrolyte Market appears promising.

India Electric Vehicle Battery Electrolyte Industry Overview

The India electric vehicle battery electrolyte market is semi-consolidated. Some of the major players (not in particular order) include Neogen Chemicals, Gujarat Fluorochemicals, Mitsubishi Chemical Group, Targray Technology International Inc, and Aether Industries Limited.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Government policies supporting adoption of electric vehicles

4.5.1.2 Declining Lithium-ion Battery Prices

4.5.2 Restraints

4.5.2.1 Limited avalibility and supply of raw materials

4.6 Supply Chain Analysis

4.7 PESTLE Analysis

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lead Acid Batteries

5.1.2 Lithium-ion Batteries

5.1.3 Other Battery Types

5.2 Electrolyte Type

5.2.1 Liquid Electrolyte

5.2.2 Gel Electrolyte

5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Ami Organics Electrolytes Private Ltd.

6.3.2 Neogen Chemicals

6.3.3 Gujarat Fluorochemicals

6.3.4 3M India

6.3.5 BASF Shanshan Battery Materials Co.

6.3.6 Targray Technology International Inc

6.3.7 Aether Industries Limited

6.3.8 Tatva Chintan Pharma Chem Limited

6.3.9 Mitsubishi Chemical Group

6.3.10 S K Industries

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Research & Development in electrolyte material