아세안 각국의 전기자동차 전지 전해액 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

ASEAN Countries Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636478

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

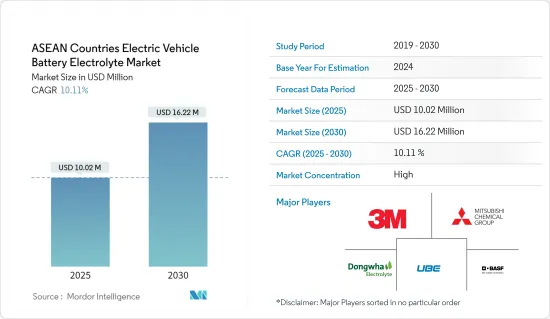

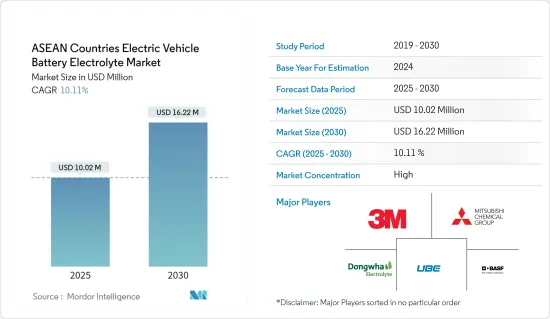

아세안 국가의 전기자동차 전지 전해액 시장 규모는 2025년에 1,002만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 10.11%로, 2030년에는 1,622만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 전기자동차(EV)의 급속한 보급과 정부의 지원책에 힘입어 시장이 성장하고 있습니다.

반대로 공급망 격차가 성장 과제가 될 수 있습니다.

그러나 전해질 배합의 진보는 가까운 미래에 시장에 유리한 기회를 제공합니다.

동지역에서는 싱가포르가 두드러지며, 싱가포르는 EV 생태계를 강화하기 위한 협력적인 노력으로 현저한 성장이 예상됩니다.

아세안 국가의 전기자동차 전지 전해액 시장 동향

리튬 이온 전지 부문이 시장을 독점

리튬 이온 전지 부문은 전기자동차의 급속한 보급과 전지 기술의 혁신에 힘입어 아세안 지역의 전기자동차(EV)용 전지 전해액 시장의 매우 중요한 구성 요소가 되었습니다.

지역정부가 환경친화적인 수송수단을 지지하고 EV에 대한 소비자의 선호도가 높아지는 가운데 효율적이고 고성능인 전지에 대한 수요가 높아지고 있습니다. 전해질은 전지 성능을 높이고 안전성을 확보하며 수명을 연장하는 데 중요한 역할을 합니다.

리튬 이온 전지 부문 확장의 주요 원동력은 전지 비용의 현저한 감소입니다. 예를 들어, 2023년 리튬 이온 전지의 평균 가격은 1킬로와트(kWh)당 약 139달러까지 하락했으며, 2013년 이후 82% 이상의 현저한 하락을 보였습니다. 예측에 따르면 2025년에는 113달러/kWh 미만으로 떨어지며 2030년에는 80달러/kWh에 이를 전망입니다.

이러한 전지 가격의 하락세는 소비자들에게 전기차 구입 용이성을 향상시킬 뿐만 아니라 제조업체가 선진적인 전지 기술과 고급 전해질을 도입하는 계기가 되어 시장 수요를 증폭시킵니다.

게다가, 지속가능성은 리튬 이온 전지 부문에서 매우 중요한 힘으로 부상하고 있습니다. 환경 의식이 증가함에 따라 제조업체는 지속 가능한 재료로 만들어진 친환경 전해질 솔루션으로 전환하고 있습니다. 이러한 녹색 변화는 소비자의 선호를 충족할 뿐만 아니라 전지 생산에서 환경 발자국을 억제하기 위한 규제 의무와도 일치합니다.

2024년 7월 LG에너지솔루션과 현대모터사는 인도네시아에 10GWh 용량의 EV전지 제조시설을 설립했습니다. 2024년 10월 인도네시아는 세계 EV 허브가 되겠다는 야심을 더욱 강화하기 위해 중국의 Contemporary Amperex Technology(CATL)와의 합작 사업을 발표하고 동남아시아에서 리튬 이온 전지 생산을 위해 12억 달러를 기부 했습니다.

결론적으로 투자 증가와 가격 하락에 힘입어 리튬 이온 기술의 채택이 동지역에서 가속화되고 향후 수년간 시장이 크게 성장할 길이 열릴 것으로 전망됩니다.

중요한 역할을 할 것으로 예상되는 싱가포르

싱가포르는 아세안에서 EV 충전 인프라의 최첨단을 달리고 있으며 1,800개 이상의 공공 충전 포인트를 제공하고 있습니다. 싱가포르 정부는 2030년 말까지 추가로 6만 곳의 충전 포인트를 설치할 계획입니다.

2021-2025년에 걸쳐 싱가포르 정부는 EV 보급을 촉진하기 위해 2,200만 달러를 투자했습니다. 이 이니셔티브는 개인 충전기의 수를 늘리고 전체 충전 인프라를 강화하는 것을 목표로 합니다. 동시에 싱가포르는 자국을 EV부문에서 매우 중요한 연구개발 거점으로 자리매김하기 위해 다국적기업과 신흥기업의 투자를 유치하고 현지의 EV 생태계를 육성하고 있습니다.

공해를 억제하기 위해 노력하는 싱가포르 정부는 전기 이동성을 지원하고 이러한 추진으로 EV 판매량이 증가할 것으로 예상됩니다. 특히 싱가포르는 2040년까지 내연 기관에서 보다 깨끗한 에너지 자동차로의 전환을 목표로 하고 있습니다. 그 견인 역할을 하는 곳이 싱가포르의 2040년 그린 에너지 자동차 목표를 향한 대처 방향을 제시하는 신설 국립전기자동차센터(NEVC)입니다. 이 시프트는 가까운 미래에 전지 재료, 특히 전해질에 대한 수요를 높일 것입니다.

육상교통청의 보고에 따르면 싱가포르에서의 EV 판매는 증가세에 있습니다. 2024년 1월부터 7월 사이에 싱가포르에서는 6,019대의 전지 전기자동차가 등록되었습니다. 이는 2023년 동시기 등록 대수 1,892대에서 32.4% 증가한 수치로 대규모 성장을 의미합니다.

EV시장의 급성장은 제로 배출에 의한 대기환경 개선과 온실가스 억제 등 환경에 대한 혜택뿐만 아니라 전지구적인 기후 변화 대처에서도 중요한 역할을 하고 있습니다.

소비자의 선호와 정책적 지원이 일치하기 때문에 싱가포르의 전기자동차 전지 전해액에 대한 수요는 당분간 증가할 것으로 예상됩니다.

아세안 국가의 전기자동차 전지 전해액질 산업 개요

아세안 국가의 전기자동차 전지 전해액 시장은 부분 통합되어 있습니다. 주요 진출기업으로는 Mitsubishi Chemical Group Corporation, 3M, Dongwha Eletrolyte, BASF SE, UBE Corp. 등을 들 수 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기자동차(EV) 보급률 상승

정부 지원책

억제요인

공급망 격차

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지 유형

리튬 이온 전지

납축전지

기타

전해질 유형

액체 전해질

겔 전해질

고체 전해질

지역

말레이시아

태국

인도네시아

싱가포르

기타 아세안 국가

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

Mitsubishi Chemical Group

3M

Dongwha Eletrolyte

UBE Corp.

BASF SE

Hitachi, Ltd.

Cabot Corporation

Umicore NV

시장 순위/점유율 분석

기타 유력 기업 목록

제7장 시장 기회와 앞으로의 동향

전해질 배합 혁신

CSM

영문 목차

영문목차

The ASEAN Countries Electric Vehicle Battery Electrolyte Market size is estimated at USD 10.02 million in 2025, and is expected to reach USD 16.22 million by 2030, at a CAGR of 10.11% during the forecast period (2025-2030).

Key Highlights

In the medium term, the market is poised for growth, fueled by the surging adoption of electric vehicles (EVs) and supportive government initiatives.

Conversely, disruptions in the supply chain may pose challenges to this growth.

However, advancements in electrolyte formulations present lucrative opportunities for the market in the near future.

Within the region, Singapore stands out, anticipating notable growth, thanks to its concerted efforts to bolster the country's EV ecosystem.

ASEAN Countries Electric Vehicle Battery Electrolyte Market Trends

Lithium-Ion Batteries Segment to Dominate the Market

The lithium-ion battery segment stands as a pivotal component of the electric vehicle (EV) battery electrolyte market in the ASEAN region, propelled by the swift uptake of electric vehicles and innovations in battery technology.

With regional governments championing greener transportation and a growing consumer preference for EVs, the appetite for efficient, high-performance batteries is on the rise. Electrolytes play a vital role in boosting battery performance, ensuring safety, and extending longevity.

A key driver behind the lithium-ion battery segment's expansion is the notable drop in battery costs. For example, in 2023, the average price of lithium-ion batteries dipped to approximately USD 139 per kilowatt-hour (kWh), marking a remarkable decline of over 82% since 2013. Forecasts suggest prices might slide below USD 113/kWh by 2025 and could touch USD 80/kWh by 2030.

This downward trajectory in battery prices not only enhances the affordability of electric vehicles for consumers but also spurs manufacturers to delve into advanced battery technologies and premium electrolytes, amplifying market demand.

Moreover, sustainability is emerging as a pivotal force in the lithium-ion battery segment. With a surge in environmental consciousness, manufacturers are pivoting towards eco-friendly electrolyte solutions crafted from sustainable materials. This green shift not only resonates with consumer preferences but also dovetails with regulatory mandates aimed at curbing the environmental footprint of battery production.

In July 2024, LG Energy Solution and Hyundai Motor Corp inaugurated a 10 GWh capacity EV battery manufacturing facility in Indonesia. Furthering its ambition to be a global EV hub, Indonesia, in October 2024, unveiled a joint venture with China's Contemporary Amperex Technology Co Ltd (CATL), committing a substantial USD 1.2 billion towards lithium-ion battery production in the Southeast Asian landscape.

In conclusion, driven by increasing investments and declining prices, the adoption of lithium-ion technology is set to accelerate in the region, paving the way for substantial market growth in the years ahead.

Singapore Expected to Play a Key Role

Singapore has been at the forefront of EV charging infrastructure in ASEAN, with more than 1,800 public charging points available. The Government of Singapore plans to install 60,000 more charging points by the end of 2030.

From 2021 to 2025, the Singapore government has earmarked USD 22 million to boost EV adoption. This initiative aims to bolster the number of chargers on private properties, enhancing the overall charging infrastructure. Concurrently, Singapore has positioned itself as a pivotal R&D hub for the EV sector, attracting investments from multinationals and startups alike, thereby nurturing a robust local EV ecosystem.

With a commitment to curbing pollution, the Singapore government is championing electric mobility. This push is anticipated to drive up EV sales. Notably, Singapore aims to transition from internal combustion engines to cleaner-energy vehicles by 2040. Leading this charge is the newly established National Electric Vehicle Centre (NEVC), steering efforts towards Singapore's 2040 green energy vehicle goal. This shift is poised to elevate the demand for battery materials, particularly electrolytes, in the near future.

As reported by the Land Transport Authority, EV sales in Singapore are on the rise. Between January-July 2024, the country registered 6,019 battery electric vehicles. This marks a significant jump from 1,892 registrations during the same period in 2023, representing an 32.4% increase.

The swift growth of the EV market not only benefits the environment-due to zero emissions improving air quality and curbing greenhouse gases-but also plays a vital role in the global fight against climate change.

Given the alignment of consumer preferences and regulatory support, the demand for electric vehicle battery electrolytes in Singapore is set to rise in the foreseeable future.

ASEAN Countries Electric Vehicle Battery Electrolyte Industry Overview

The ASEAN Countries' electric vehicle battery electrolyte market is semi-consolidated. Some of the major players include (not in particular order) Mitsubishi Chemical Group, 3M, Dongwha Eletrolyte, BASF SE, and UBE Corp. among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Rising Electric Vehicle (EV) Adoption

4.5.1.2 Supportive Government Initiatives

4.5.2 Restraints

4.5.2.1 Supply Chain Disruptions

4.6 Supply Chain Analysis

4.7 Porter's Five Force Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-Ion Batteries

5.1.2 Lead-Acid Batteries

5.1.3 Others

5.2 Electrolyte Type

5.2.1 Liquid Electrolyte

5.2.2 Gel Electrolyte

5.2.3 Solid Electrolyte

5.3 Geography

5.3.1 Malaysia

5.3.2 Thailand

5.3.3 Indonesia

5.3.4 Singapore

5.3.5 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements