북미의 전기자동차 전지 전해액 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

North America Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636474

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

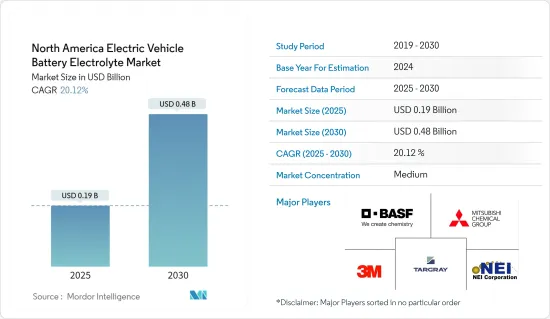

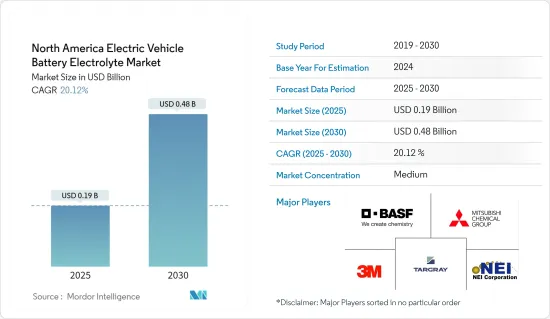

북미의 전기자동차 전지 전해액 시장 규모는 2025년에 1억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 20.12%로, 2030년에는 4억 8,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 동지역 전체에서 전기자동차의 보급과 전지 기술의 진보가 진행되고 있어 예측 기간 중 전기차용 전지 전해액 시장 수요를 견인할 것으로 예상됩니다.

한편, 고체 전해질의 기술적 과제는 전기자동차 전지 전해질 시장의 성장을 크게 억제할 수 있습니다.

전지 성능, 안전성 및 수명을 향상시키는 전해액 배합 기술 혁신은 특히 고성능 또는 장거리 EV를 위해 가까운 미래에 전기자동차 전지 전해액 시장에 큰 성장 기회를 창출합니다.

미국은 EV 보급률 상승으로 예측 기간 동안 북미 전기자동차 전지 전해질 시장에서 가장 급성장하는 국가가 될 것으로 예상됩니다.

북미 전기자동차 전지 전해액 시장 동향

리튬 이온 전지 유형이 크게 성장

북미의 전기자동차 전지 전해액 시장, 특히 리튬 이온 전지에 사용되는 전해액 시장은 전기자동차(EV) 부문의 확대와 함께 급성장하고 있습니다. 이 급성장의 주요 요인은 EV 소비자 증가와 온실가스 배출 억제를 목적으로 한 정부의 엄격한 규제입니다.

리튬 이온 전지는 높은 에너지 밀도, 긴 수명 및 최소한의 자가방전율로 EV에 매우 중요합니다. 리튬 이온 전지의 가격 설정은 전기자동차 전체의 비용에 크게 영향을 미치며, 전해액은 이러한 전지 비용의 주요 결정 요인입니다.

예를 들어 Bloomberg NEF의 보고서에 따르면 2023년 전지 가격은 139달러/kWh로 하락하고 전년 대비 13% 하락했습니다. 지속적인 기술 진보와 제조 최적화로 인해 전지 팩 가격은 2025년까지 113달러/kWh로 더 낮아졌고, 2030년에는 80달러/kWh에 이를 것으로 예상됩니다. 제조 효율성 향상, 원료 대량 조달, 공급망의 합리화로 리튬 이온 전지의 생산이 확대됨에 따라 전지 전해질 단위당 비용은 예측 기간 동안 감소할 전망입니다.

게다가 리튬 이온 전지의 연구개발이 진행되고 있으며, 전지의 성능, 안전성, 수명을 높이는 새로운 전해액의 배합이 탄생하고 있습니다. 전국의 주요 연구소는 리튬 이온 EV 전지용 첨단 전해질 솔루션을 개발하고 있습니다.

예를 들어, 2023년 3월, 미국 에너지부 산하의 Argonne National Laboratory의 연구원들은 전기자동차의 주행 거리를 크게 연장하는 리튬 공기 전지를 발표했습니다. 이 혁신적인 전지는 기존의 액체 전해질 접근법과 달리 고체 전해질을 채택합니다. 이 발전으로 인해 표준 리튬 이온 전지와 비교하면 에너지 밀도가 4배로 높아지며 이는 예측 기간 동안 EV에서 이러한 선진 리튬 이온 전지에 대한 수요가 증가할 것을 보여줍니다.

또한 주요 전지 제조업체는 북미에서 생산 능력을 강화하고 있으며 전해액 시장을 더욱 활성화하고 있습니다. 2023년 9월 스웨덴의 유명한 리튬 이온 전지 제조업체인 Northvolt는 캐나다 퀘벡주에 52억 달러의 기가팩토리를 건설할 계획을 발표했습니다. 이 공장은 전지 생산뿐만 아니라 양극 활물질 생산에도 주력할 예정입니다. Northvolt Six 공장 건설은 올해 시작되며 2026년 운영이 예정되어 있습니다. 이러한 노력으로 리튬 이온 전지의 생산이 강화되어 EV용 전해액 수요도 향후 수년간 증가할 전망입니다.

결론적으로 이러한 노력과 기술 혁신은 북미에서 리튬 이온 전지의 생산을 확대하고 예측 기간 동안 EV용 전해액 수요를 급증시킬 것으로 예상됩니다.

상당한 성장을 이루는 미국

미국은 기술 혁신, 제조 및 지원 시책을 중시하며 북미의 EV 전지 전해질 시장에서 매우 중요한 역할을 하고 있습니다. 전해액은 리튬 이온 전지의 중요한 구성 요소로서 음극과 양극 사이의 리튬 이온의 이동을 촉진하고 EV의 에너지 저장 및 방출에 매우 중요합니다.

최근 미국에서는 소비자 수요, 환경 의식 증가, 세액 공제 및 리베이트와 같은 정부 우대 정책으로 EV 판매가 현저하게 증가하고 있습니다. EV 보급의 급증은 리튬 이온 전지, 나아가 고품질 전지 전해액 수요에 직접 박차를 가하고 있습니다.

예를 들어 국제에너지기구(IEA)의 보고에 따르면 2023년 전지식 전기차 판매량은 110만대에 이르며 2022년부터 37.5% 증가, 2019년부터는 3.58배라는 경이로운 성장세를 보였습니다. 정부가 EV의 보급을 촉진하는 여러가지 시책을 내세우고 있기 때문에 판매 대수는 향후 수년간 증가할 전망입니다.

또한 미국 정부는 전기 이동성으로의 전환을 지지하고 탄소 배출을 억제하는 조치를 중시하고 있습니다. 이 노력은 최첨단 전지 전해질의 발전과 전개를 뒷받침합니다.

예를 들어, 2024년 3월, 바이덴 정부는 2032년까지 새롭게 판매되는 승용차와 소형 트럭의 대부분을 전기자동차로 만들 것을 의무화하는 미국에서 가장 철저한 기후 변화 규제를 발표 했습니다. 이러한 대담한 움직임은 EV의 생산을 앞당길 뿐만 아니라 EV용 전지 전해액 수요를 향후 수년간 증폭시킬 것입니다.

급증하는 EV 수요에 대응하기 위해 많은 전지 제조업체들이 미국 내에 생산 기지를 설치하거나 확대하고 있습니다. 이 자국 내 생산 전략은 수입품에 대한 의존을 억제할 뿐만 아니라 지역별 전해액의 안정적인 공급을 보장하기 위한 것입니다.

예를 들어 LG에너지솔루션은 2023년 3월 북미에서 EV와 ESS용 전지의 생산을 강화하기 위해 애리조나주에 7조 2,000억원(52억 2,000만 달러)을 투입해 전지 제조 거점을 설립하여 화제가 되었습니다. 이 새로운 시설은 EV용 전지를 생산하게 되어 신뢰성이 높은 전해액 공급의 필요성이 더욱 높아지고 있습니다.

이러한 개발을 통해 위와 같은 투자와 프로젝트가 미국에서 EV 생산을 강화하고 EV 전지용 전해액에 대한 수요를 높이는 것이 확실시됩니다.

북미 전기자동차 전지 전해질 산업 개요

북미의 전기자동차 전지 전해액 시장은 완만합니다. 주요 진입기업(순서부동)은 3M Company, BASF Corporation, Mitsubishi Chemical Group Corporation, Targray Technology International Inc, NEI corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기자동차 보급 확대

전지 기술의 진보

억제요인

고체 전해질의 기술 과제

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지 유형

리튬 이온 전지

납축전지

기타

전해질 유형

액체 전해질

겔 전해질

고체 전해질

지역

미국

캐나다

기타 북미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

3M Company

BASF Corporation

LG Chem Ltd

Mitsubishi Chemical Group

Panasonic Holdings Corporation

Solvay SA

Asahi Kasei America, Inc.

Cabot Corporation

Dongwha Electrolyte Co.,Ltd.

삼성SDI

NEI corporation

Targray Technology International Inc

기타 유력 기업 목록

시장 순위 분석

제7장 시장 기회와 앞으로의 동향

전해질 배합의 혁신

CSM

영문 목차

영문목차

The North America Electric Vehicle Battery Electrolyte Market size is estimated at USD 0.19 billion in 2025, and is expected to reach USD 0.48 billion by 2030, at a CAGR of 20.12% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the growing adoption of electric vehicles and advancements in battery technology across the region are expected to drive the demand for the electric vehicle battery electrolyte market during the forecast period.

On the other hand, the technological challenges in Solid-State electrolytes can significantly restrain the growth of the electric vehicle battery electrolyte market.

Nevertheless, the innovation in electrolyte formulations that improve battery performance, safety, and lifespan, particularly for high-performance or long-range EVs creates significant growth opportunities in the electric vehicle battery electrolyte market in the near future.

The United States is anticipated to be the fastest-growing country in the North American electric vehicle battery electrolyte market during the forecast period due to rising EV adoption.

North America Electric Vehicle Battery Electrolyte Market Trends

Lithium-Ion Batteries Type to Witness Significant Growth

The North American market for EV battery electrolytes, especially those used in lithium-ion batteries, is experiencing rapid growth, paralleling the broader expansion of the electric vehicle (EV) sector. This surge is largely fueled by increasing consumer adoption of EVs and stringent government regulations aimed at curbing greenhouse gas emissions.

Lithium-ion batteries are pivotal to the EV landscape, celebrated for their high energy density, extended cycle life, and minimal self-discharge rate. The pricing of lithium-ion batteries significantly influences the overall cost of electric vehicles, with electrolytes being a key determinant of these battery costs.

For example, a Bloomberg NEF report highlighted that in 2023, battery prices fell to USD 139/kWh, marking a 13% drop from the prior year. With ongoing technological advancements and manufacturing optimizations, projections suggest battery pack prices will further decline to USD 113/kWh by 2025 and reach USD 80/kWh by 2030. As lithium-ion battery production ramps up, driven by enhanced manufacturing efficiencies, bulk raw material procurement, and streamlined supply chains, the cost per unit of battery electrolytes is set to decrease during the forecast period.

Moreover, ongoing R&D in lithium-ion batteries is birthing new electrolyte formulations that boost battery performance, safety, and lifespan. Leading research labs nationwide are pioneering advanced electrolyte solutions for lithium-ion EV batteries.

For instance, in March 2023, researchers from Argonne National Laboratory, under the US Department of Energy, unveiled a lithium-air battery poised to significantly extend electric vehicles' driving range. This innovative battery employs a solid electrolyte, diverging from the conventional liquid electrolyte approach. When compared to standard Li-ion batteries, this advancement could potentially quadruple energy density, signaling a heightened demand for such advanced lithium-ion batteries in EVs during the forecast period.

Additionally, major battery manufacturers are ramping up production capacities in North America, further energizing the electrolyte market. In September 2023, Northvolt, a prominent Swedish lithium-ion battery manufacturer, unveiled plans for a USD 5.2 billion gigafactory in Quebec, Canada. This facility will not only produce batteries but also focus on cathode active material production. Construction of the Northvolt Six factory is set to kick off this year, with operations slated for 2026. Such initiatives are poised to bolster lithium-ion battery production and, consequently, the demand for EV battery electrolytes in the coming years.

In conclusion, these initiatives and innovations are set to amplify lithium-ion battery production in North America, driving a corresponding surge in demand for EV battery electrolytes during the forecast period.

United States to Witness Significant Growth

The United States plays a pivotal role in the North American EV battery electrolyte market, emphasizing innovation, manufacturing, and supportive policies. Electrolytes, as vital components of lithium-ion batteries, facilitate the movement of lithium ions between the anode and cathode, crucial for energy storage and release in EVs.

In recent years, the United States has seen a notable uptick in EV sales, driven by consumer demand, heightened environmental consciousness, and government incentives like tax credits and rebates. This surge in EV adoption has directly spurred demand for lithium-ion batteries and, by extension, high-quality battery electrolytes.

For instance, the International Energy Agency reported that in 2023, battery electric vehicle sales hit 1.1 million units, marking a 37.5% rise from 2022 and a staggering 3.58-fold increase since 2019. With the government rolling out several pro-EV adoption policies, sales are poised to climb in the coming years.

Furthermore, the U.S. government is championing the shift to electric mobility, emphasizing policies that curb carbon emissions. This commitment is propelling the advancement and deployment of cutting-edge battery electrolytes.

For instance, in March 2024, the Biden administration unveiled the nation's most sweeping climate regulations, mandating that by 2032, a significant majority of newly sold passenger cars and light trucks will be all-electric. Such bold moves are set to not only hasten EV production but also amplify the demand for EV battery electrolytes in the coming years.

In response to the surging EV demand, numerous battery manufacturers are either setting up or expanding their production bases in the U.S. This domestic manufacturing strategy not only curtails dependence on imports but also guarantees a consistent supply of region-specific electrolytes.

For instance, in March 2023, LG Energy Solution made headlines with a KRW 7.2 trillion (USD 5.22 billion) investment to establish a battery manufacturing hub in Arizona, aiming to bolster EV and ESS battery production in North America. This new facility is set to churn out EV batteries, further amplifying the need for a reliable electrolyte supply.

Given these developments, it's evident that such investments and projects are set to bolster EV production in the United States, subsequently driving up the demand for EV battery electrolytes.

North America Electric Vehicle Battery Electrolyte Industry Overview

The North America Electric Vehicle Battery Electrolyte market is moderated. Some of the key players (not in particular order) are 3M Company, BASF Corporation, Mitsubishi Chemical Group, Targray Technology International Inc, NEI corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Adoption of Electric Vehicles

4.5.1.2 Advancements in Battery Technology

4.5.2 Restraints

4.5.2.1 Technological Challenges in Solid-State Electrolytes

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion Batteries

5.1.2 Lead-Acid Batteries

5.1.3 Others

5.2 Electrolyte Type

5.2.1 Liquid Electrolyte

5.2.2 Gel Electrolyte

5.2.3 Solid Electrolyte

5.3 Geography

5.3.1 United States

5.3.2 Canada

5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements