전기자동차 배터리 전해액 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636259

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

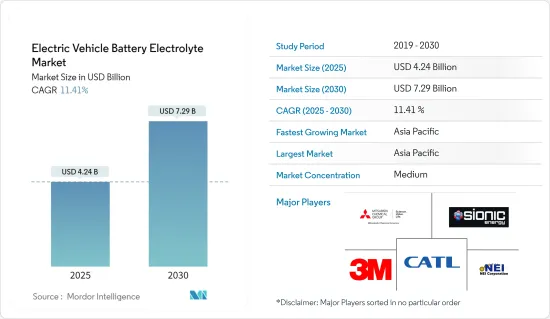

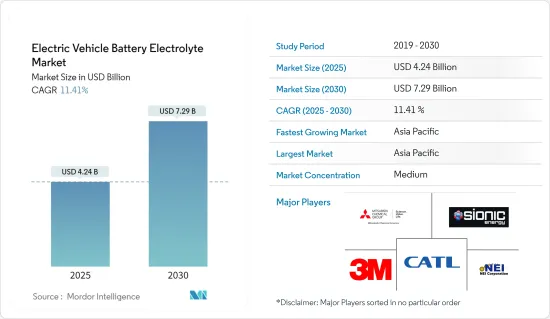

전기자동차 배터리 전해액 시장 규모는 2025년 42억 4,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 11.41%의 CAGR로 2030년에는 72억 9,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

중기적으로는 전기자동차 수요 증가와 정부 지원책 등의 요인이 예측 기간 동안 시장을 견인할 것으로 예상됩니다.

반면, 고급 전해질의 높은 비용과 안전성에 대한 우려는 예측 기간 동안 시장 성장의 걸림돌이 될 것으로 예상됩니다.

그러나 기술 혁신과 신흥 배터리 재료의 확장은 향후 몇 년 동안 시장에 큰 기회를 가져올 것으로 예상됩니다.

아시아태평양은 이 지역의 여러 국가에서 전기자동차 보급률이 높아지면서 시장을 독점할 것으로 추정됩니다.

전기자동차 배터리 전해액 시장 동향

시장을 지배하는 리튬이온 배터리 부문

리튬이온 배터리는 기존에는 주로 휴대폰, 컴퓨터 등 민수용 전자기기에 사용되어 왔습니다. 그러나 최근 들어 환경 부하가 적어 하이브리드 자동차나 완전 전기자동차(EV)의 동력원으로 재설계되는 사례가 늘고 있으며, EV는 CO2, 질소산화물 등 온실가스를 전혀 배출하지 않습니다.

2023년 전기자동차(EV) 배터리 수요는 전년 대비 40% 증가하여 급증했습니다. 중국은 배터리 생산, 특히 대형 배터리 생산에서 계속 선두를 달리고 있으며, 생산량의 약 12%를 수출하고 있습니다. 한편, 유럽은 크게 도약하고 있으며, BloombergNEF의 예측에 따르면 2030년까지 유럽이 세계 배터리 생산에서 차지하는 비중은 31%에 달할 것으로 보입니다.

전 세계적으로 전기자동차에 대한 수요가 증가함에 따라 효과적이고 신뢰할 수 있는 배터리 전해액이 가장 중요해졌고, 전해액 배합과 기술이 크게 발전하고 있습니다.

리튬이온 배터리용 전해액 시장에 영향을 미치는 주요 동향 중 하나는 리튬이온 배터리 가격이 지속적으로 하락하고 있다는 점입니다. 예를 들어, 리튬이온 배터리의 평균 가격은 2023년에 킬로와트시(kWh)당 약 139달러로 하락하여 2013년 이후 82% 이상 크게 하락할 것으로 예상됩니다. 예측에 따르면, 가격은 2025년까지 113달러/kWh 이하로 떨어지고, 2030년에는 80달러/kWh에 도달할 수 있습니다. 이러한 가격 하락 추세는 소비자에게 전기자동차를 더 저렴하게 만들고 제조업체가 새로운 전해질 구성을 탐구하고 기존 전해질 구성을 개선하여 배터리 성능과 수명을 향상시킬 수 있도록 장려합니다.

신흥 시장에서의 전기자동차 보급 확대도 리튬이온 배터리용 전해질 부문의 성장을 견인하고 있습니다. 세계 각국 정부는 전기자동차 보급을 촉진하기 위한 정책 및 인센티브를 시행하고 있습니다.

미국 정부는 2023년, 2030년까지 신차 판매의 50%를 전기자동차로 전환하겠다는 목표를 발표했습니다. 백악관은 또한 EV Acceleration Challenge를 통해 미국의 역사적인 전기자동차로의 전환을 지원하기 위한 민관의 노력을 발표했습니다.

이는 배터리 생산과 전해액 수요의 급격한 증가로 이어집니다. 각국이 온실가스 배출량을 줄이고 청정에너지원으로 전환하는 것을 우선순위로 삼고 있는 가운데, 효율적인 배터리 전해질의 역할은 이러한 지속가능성 목표를 달성하는 데 있어 점점 더 중요해지고 있습니다.

따라서 시장이 발전함에 따라 지속가능성과 대체 기술에 대한 관심이 배터리 전해질 부문의 향후 세계 전망을 형성하고 보다 친환경적인 자동차 산업에 기여할 것으로 예상됩니다.

아시아태평양이 시장을 독점할 것으로 예상

아시아태평양의 전기자동차(EV) 배터리 전해액 시장은 중국의 전기자동차 생산 및 판매의 선도적 지위에 힘입어 괄목할 만한 성장세를 보이고 있습니다. 전 세계 전기자동차 판매량은 2019년 106만 대에서 2023년 810만 대로 650% 이상 급증할 것으로 예상되며, 중국의 배터리 전해액 수요는 이러한 성장에 매우 중요한 역할을 할 것으로 보입니다.

중국 기업들은 배터리 기술 혁신의 최전선에서 리튬이온 배터리의 성능과 효율을 지속적으로 개선하고 있으며, 2024년 3 월에는 전기자동차용 리튬이온 배터리의 충전 속도를 크게 향상시키고 작동 온도 범위를 확장하는 새로운 전해질 설계가 연구를 통해 발표되어 큰 돌파구를 마련했습니다. 획기적인 발전을 가져왔습니다. 이 혁신적인 설계는 상온에서 10분 이내에 완전한 충방전 사이클을 가능하게 하고, -70℃에서 60℃까지 넓은 온도 범위에서 배터리의 가역성을 보장합니다. 이러한 발전은 배터리 효율을 높이고, 안전성을 향상시키며, 전기자동차용 리튬이온 배터리의 신뢰성을 높입니다.

리튬이온 배터리의 대량 생산은 제조 비용의 감소에 기여하여 전기자동차를 소비자에게 보다 친숙하게 다가갈 수 있도록 하고 있습니다. 인건비 하락과 제조업체 간의 경쟁 심화로 인해 전반적인 수익성이 향상되어 더 넓은 시장 진입이 가능해졌습니다. 이러한 비용 효율성은 더 많은 소비자들이 전기자동차로 전환하도록 유도하여 전해액에 대한 수요를 촉진하는 데 매우 중요한 역할을 합니다.

중국 외에도 일본과 한국 등 아시아태평양 국가들도 전기자동차 배터리 전해질 시장에서 큰 진전을 이루고 있습니다. 일본은 고체 배터리와 나트륨 이온 배터리 개발에 주력하고 있으며, 더 낮은 비용으로 더 나은 성능을 제공할 것으로 기대되는 반면, 한국은 배터리 생산과 기술 혁신에 많은 투자를 하고 있습니다.

예를 들어, 2024년 4월 일본 연구진은 고체 리튬이온 배터리의 전해질로 사용하기에 적합한 안정적이고 전도성이 높은 물질을 확인했습니다. 이 신소재는 지금까지 알려진 산화물 고체 전해질을 능가하는 이온 전도도를 자랑하며, 넓은 온도 범위에서 효과적으로 작동합니다.

아시아태평양의 전기자동차 배터리 전해질 시장은 기술 발전, 정부의 강력한 지원, 비용 효율성, 인프라 확대로 인해 지속적인 성장이 예상됩니다. 이러한 요인들이 결합됨에 따라 이 지역은 전기자동차 배터리 전해질 시장에서 우위를 유지하고 지속가능한 운송의 미래를 형성할 것으로 예상됩니다.

전기자동차 배터리 전해액 산업 개요

전기자동차 배터리 전해액 시장은 반통합형입니다. 주요 진출 기업으로는 Mitsubishi Chemical Group, Sionic Energy, 3M, Contemporary Amperex Technology Co.Limited(CATL), NEI Corporation 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의

조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

전기자동차 수요 증가

정부 지원책

성장 억제요인

첨단 전해질의 고비용

공급망 분석

Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 기업 간의 경쟁 관계

투자 분석

제5장 시장 세분화

배터리 유형

리튬이온 배터리

납축배터리

기타 배터리 유형

전해질 유형

액체 전해질

겔 전해질

고체 전해질

지역

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

스페인

북유럽

터키

러시아

기타 유럽

아시아태평양

중국

인도

일본

한국

태국

인도네시아

베트남

말레이시아

기타 아시아태평양

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트

남아프리카공화국

이집트

나이지리아

카타르

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략

기업 개요

Mitsubishi Chemical Group

3M Co.

Contemporary Amperex Technology Co. Limited(CATL)

NEI Corporation

Sionic Energy

BASF SE

Solvay SA

UBE Industries Ltd

LG Chem Ltd

Targray Industries Inc.

시장 순위/점유율 분석

기타 저명한 기업 리스트

제7장 시장 기회와 향후 동향

신흥 배터리 재료 확대

ksm

영문 목차

영문목차

The Electric Vehicle Battery Electrolyte Market size is estimated at USD 4.24 billion in 2025, and is expected to reach USD 7.29 billion by 2030, at a CAGR of 11.41% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as the increasing demand for electric vehicles and supportive government initiatives are expected to drive the market during the forecast period.

On the other hand, high costs of advanced electrolytes and safety concerns are expected to hinder the market growth during the forecast period.

However, technological innovations and expansion in emerging battery materials are expected to provide significant opportunities for the market in the coming years.

Asia-Pacific is estimated to dominate the market due to the increasing adoption rate of electric vehicles across the various countries in the region.

Electric Vehicle Battery Electrolyte Market Trends

The Lithium-ion Batteries Segment to Dominate the Market

Lithium-ion batteries have traditionally been used mainly in consumer electronic devices like mobile phones and personal computers. Still, due to low environmental impact, they are increasingly being redesigned as the power source of choice in hybrid and the complete electric vehicle (EV) range. EVs do not emit any CO2, nitrogen oxides, or other greenhouse gases.

In 2023, the demand for electric vehicle (EV) batteries surged by 40% compared to the previous year, driven by rising EV sales across all markets, particularly in Europe and the United States. China continues to lead in battery production, especially for heavy-duty batteries, with approximately 12% of its production being exported. Meanwhile, Europe is making significant strides, with forecasts from BloombergNEF suggesting that its share of global battery production could reach 31% by 2030.

As the demand for electric vehicles escalates worldwide, effective and reliable battery electrolytes have become paramount, fostering significant advancements in electrolyte formulations and technologies.

One of the primary trends influencing the lithium-ion battery electrolyte market is the continuous decline in the price of lithium-ion batteries. For instance, the average price of lithium-ion batteries fell to around USD 139 per kilowatt-hour (kWh) in 2023, representing a significant decrease of over 82% since 2013. Projections indicate that prices could decline to below USD 113/kWh by 2025 and reach USD 80/kWh by 2030. This downward pricing trend makes electric vehicles more affordable for consumers and encourages manufacturers to explore new electrolyte compositions and improve existing ones, enhancing battery performance and longevity.

The increasing penetration of electric vehicles in emerging markets is also driving the growth of the lithium-ion battery electrolyte segment. Governments worldwide are implementing policies and incentives to promote electric vehicle adoption.

In 2023, the US government announced a goal to have 50% of all new vehicle sales electric by 2030. The White House also announced public and private commitments to support America's historic transition to electric vehicles under the EV Acceleration Challenge.

This leads to a surge in battery production and electrolyte demand. As countries prioritize reducing greenhouse gas emissions and transitioning to cleaner energy sources, the role of efficient battery electrolytes becomes increasingly critical in achieving these sustainability goals.

Hence, as the market evolves, the focus on sustainability and alternative technologies is expected to shape the future landscape of the battery electrolyte segment globally, contributing to a greener automotive industry.

Asia-Pacific is Expected to Dominate the Market

The Asia-Pacific electric vehicle (EV) battery electrolyte market is witnessing remarkable growth, primarily driven by China's leading EV production and sales position. With global electric vehicle sales skyrocketing from 1.06 million in 2019 to 8.1 million in 2023, an increase of over 650%, China's robust demand for battery electrolytes plays a pivotal role in this expansion.

Chinese companies are at the forefront of battery innovation, continually enhancing the performance and efficiency of lithium-ion batteries. A significant breakthrough occurred in March 2024, as researchers unveiled a new electrolyte design that greatly enhances the charging speed and expands the operational temperature range of lithium-ion batteries for electric vehicles. This innovative design allows for full charge and discharge cycles within 10 minutes at room temperature and ensures battery reversibility across a wide temperature span from -70°C to 60°C. Such advancements enhance battery efficiency and improve safety, making lithium-ion batteries more reliable for electric vehicles.

The large-scale production of lithium-ion batteries has contributed to the decline in manufacturing costs, making electric vehicles more accessible to consumers. Lower labor costs and increased competition among manufacturers have enhanced overall profitability, enabling broader market reach. These cost efficiencies are critical in encouraging more consumers to transition to electric vehicles, thereby driving demand for electrolytes.

In addition to China, other countries in Asia-Pacific, such as Japan and South Korea, are making significant strides in the electric vehicle battery electrolyte market. Japan's focus on developing solid-state and sodium-ion batteries promises to deliver better performance at lower costs, while South Korea is investing heavily in battery production and innovation.

For instance, in April 2024, Japanese researchers identified a stable, highly conductive material suitable for use as an electrolyte in solid-state lithium-ion batteries. This new material boasts ionic conductivity surpassing that of any previously known oxide solid electrolytes and operates effectively over a wide temperature range.

The Asia-Pacific electric vehicle battery electrolyte market is poised for continued growth, fueled by technological advancements, strong government support, cost efficiencies, and an expanding infrastructure. As these factors converge, the region is expected to maintain its dominance in the market for EV battery electrolytes, shaping the future of sustainable transportation.

Electric Vehicle Battery Electrolyte Industry Overview

The electric vehicle battery electrolyte market is semi-consolidated. Some of the major players include (not in particular order) Mitsubishi Chemical Group, Sionic Energy, 3M Co., Contemporary Amperex Technology Co. Limited (CATL), and NEI Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Demand of Electric Vehicles

4.5.1.2 Supportive Government Initiatives

4.5.2 Restraints

4.5.2.1 High Costs of Advanced Electrolytes

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion Batteries

5.1.2 Lead-acid Batteries

5.1.3 Other Battery Types

5.2 Electrolyte Type

5.2.1 Liquid Electrolyte

5.2.2 Gel Electrolyte

5.2.3 Solid Electrolyte

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 France

5.3.2.3 United Kingdom

5.3.2.4 Spain

5.3.2.5 NORDIC

5.3.2.6 Turkey

5.3.2.7 Russia

5.3.2.8 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Thailand

5.3.3.6 Indonesia

5.3.3.7 Vietnam

5.3.3.8 Malaysia

5.3.3.9 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 United Arab Emirates

5.3.5.3 South Africa

5.3.5.4 Egypt

5.3.5.5 Nigeria

5.3.5.6 Qatar

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements