ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

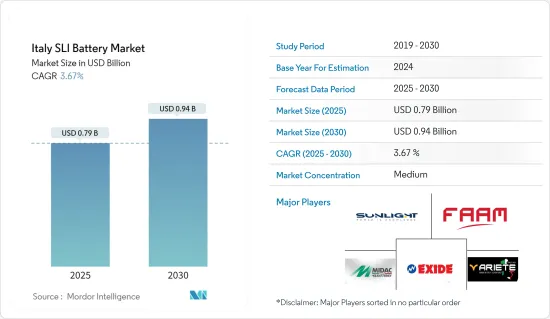

이탈리아의 SLI 배터리 시장 규모는 2025년에 7억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 3.67%로, 2030년에는 9억 4,000만 달러에 도달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 이 지역에서 자동차산업의 성장, 산업용도에서의 SLI 배터리 채용 증가 등의 요인이 예측기간 중 이탈리아의 SLI 배터리 시장의 가장 큰 촉진요인 중 하나가 될 것으로 예상됩니다.

한편, 대체 배터리 화학과의 경쟁이 증가하고 있어 예측기간 동안 시장성장의 위협이 되고 있습니다.

그럼에도 불구하고 SLI 배터리에 대한 연구 개발의 지속적인 노력은 미래에 여러 시장 기회를 창출할 것으로 기대됩니다.

이탈리아의 SLI 배터리 시장 동향

자동차 부문이 큰 성장을 이룰 전망

자동차는 이탈리아 SLI 배터리 시장에서 중요한 최종 사용자 부문입니다. 이 부문에는 승용차, 상용차, 오토바이 등 다양한 차량이 포함되며, 이들 모두 필수 기능을 위해 SLI 배터리에 크게 의존하고 있습니다. 자동차의 전통과 생산으로 유명한 이탈리아에서는 고품질 SLI 배터리에 대한 수요가 지속적으로 강세를 보이고 있습니다.

예를 들어, 국제자동차제조업협회(OICA)의 데이터에 따르면 이탈리아의 차량 생산량이 눈에 띄게 증가했습니다. 이러한 급증은 차량에 대한 수요 증가와 시민들의 가처분 소득 증가에 기인한 것으로 보입니다. 특히 2022년부터 2023년까지 생산량은 연평균 3.3%의 성장률로 10.5% 이상의 괄목할 만한 증가세를 보였습니다. 이러한 성장은 자동차 생산량 증가가 필수 자동차 부품에 대한 수요 증가로 이어지면서 SLI 배터리 시장에도 긍정적인 영향을 미쳤습니다.

승용차 카테고리는 시장을 형성하는 데 있어 지배적인 역할을 합니다. 차량 전기화에 대한 강조가 커지고 하이브리드 및 전기차로의 전환이 점진적으로 이루어지면서 기존 내연기관(ICE) 차량의 SLI 배터리에 대한 요구사항도 계속 진화하고 있습니다.

전기 자동차로의 전환이 진행 중이지만, 이탈리아의 자동차 시장에서는 여전히 내연기관(ICE) 차량이 상당한 비중을 차지하고 있어 SLI 배터리에 대한 수요가 꾸준합니다. 또한 최신 차량에 첨단 기술과 기능이 점점 더 많이 통합됨에 따라 전력 요구 사항이 높아져 이러한 요구를 충족하기 위해 더욱 견고하고 효율적인 SLI 배터리가 개발되고 있습니다.

예를 들어, 2023년 12월, 발레오의 피아네자와 산타나 공장은 차별화된 제품 개발과 생산에 주력하겠다고 발표했습니다. 피아네자는 조명에 특화되어 있으며, 산테나는 인간과 기계 인터페이스에 전념하고 있습니다. 특히 발레오에서는 패널 컨트롤, 터치 스크린, 스위치, 패들 기어 변속기 등 다양한 인간-기계 인터페이스 기술을 개발 및 생산하여 다양한 자동차 브랜드에 공급할 예정입니다. 또한 차량 성능과 신뢰성에 필수적인 SLI 배터리의 개발 및 생산에도 관여하고 있습니다.

전자상거래와 라스트마일 배송 서비스의 성장으로 소형 자동차에 대한 수요가 더욱 증가하면서 안정적인 SLI 배터리에 대한 필요성이 간접적으로 증가하고 있습니다. 또한 이탈리아의 대중교통 인프라를 현대화하고 확장하려는 지속적인 노력으로 인해 중단 없는 서비스와 승객 안전을 보장하기 위해 배터리 신뢰성이 가장 중요한 버스 및 코치 산업에서 SLI 배터리에 대한 수요가 증가했습니다.

따라서 위에서 언급한 요점에 따라 자동차 최종 사용자 부문은 예측 기간 동안 크게 성장할 것으로 예상됩니다.

대체 배터리 기술과의 경쟁이 시장 성장을 억제

시장은 대체 배터리 기술과의 경쟁이 치열 해지고 있으며, 이는 향후 몇 년 동안 성장을 크게 제한 할 것으로 예상됩니다. 이러한 경쟁은 주로 리튬 이온 배터리 기술의 발전과 점진적인 차량 전기화로의 전환에서 비롯됩니다. 자동차 산업이 기존의 내연기관에서 하이브리드 및 전기로 전환하는 전환기를 겪으면서 기존의 납축 SLI 배터리에 대한 수요가 압박을 받고 있습니다.

높은 에너지 밀도, 긴 수명, 빠른 충전 기능으로 잘 알려진 리튬 이온 배터리는 차량 시동 및 보조 전원 기능에 대한 대안으로 점점 더 실용적인 대안이 되고 있습니다. 초기에는 더 비쌌지만, 리튬 이온 기술의 비용 하락과 성능의 장점으로 인해 자동차 제조업체와 소비자 모두에게 매력적인 옵션이 되고 있습니다. 이러한 추세는 특히 고급 배터리 시스템의 추가 비용을 더 쉽게 흡수할 수 있는 프리미엄 및 고급 차량 부문에서 두드러지게 나타납니다.

최근 몇 년 동안 리튬 이온 배터리와 셀 팩의 가격이 하락세를 보이면서 최종 사용자 업계에서는 리튬 이온 배터리를 더욱 매력적으로 여기고 있습니다. 2022년에 약간의 가격 인상을 경험한 배터리 가격은 2023년에 다시 하락했습니다. 리튬 이온 배터리 팩의 가격은 14% 하락하여 사상 최저치인 139달러/kWh를 기록했습니다. 이러한 가격 하락은 원자재 및 부품 가격의 하락과 배터리 가치 사슬 전반의 생산 능력 확대에 기인합니다.

기존 차량에 스타트-스톱 기술의 채택이 증가하면서 이탈리아의 기존 SLI 배터리 시장은 또 다른 도전에 직면했습니다. 차량이 정지하면 자동으로 엔진을 차단하고 필요할 때 다시 시동을 거는 스타트-스톱 시스템은 잦은 시동을 처리하기 위해 더욱 강력한 배터리 성능이 필요합니다.

이러한 요구 사항을 충족하기 위해 강화 침수 배터리(EFB)와 흡수성 유리 매트(AGM) 납축 배터리가 개발되었지만, 우수한 수명 주기와 충전 수용성으로 인해 리튬 이온 배터리가 이 용도에 점점 더 많이 고려되고 있습니다. 엄격한 배기가스 규제와 연비 기준에 따라 다양한 차급에 걸쳐 스타트-스톱 시스템이 널리 보급됨에 따라 기존 SLI 배터리의 시장 점유율이 감소하고 첨단 기술이 선호될 수 있습니다.

차량용 첨단 에너지 저장 시스템의 개발은 리튬 이온 기술보다 더 포괄적입니다. 전고체 배터리, 리튬-황 배터리, 나트륨 이온 배터리와 같은 대체 배터리 화학에 대한 연구가 빠르게 진행되고 있습니다. 이러한 기술이 자동차에 널리 사용되기 위해서는 여전히 상업적으로 실현 가능해야 하지만, 현재의 리튬 이온 배터리에 비해 에너지 밀도, 안전성 및 성능이 더욱 향상될 것으로 기대됩니다.

예를 들어, 2024년 2월, 테벨로라에 본사를 두고 있는 이탈리아 배터리 제조업체 FAAM은 군용 잠수함 프로그램과의 협력 관계를 밝히고, 회사의 LFP 배터리와 최첨단 BMS 기술을 제공했습니다. 이러한 발전은 이탈리아의 최신 잠수함 사업인 U212 NFS에서 중추적인 역할을 합니다. OCCAR에 따르면, 리튬 배터리 시스템의 시험은 운영 효율성 향상, 추진력 강화, 내구성 연장, 유지보수 필요성 감소, 최고 수준의 선상 안전 프로토콜을 강조했습니다.

따라서 위에서 언급했듯이 대체 배터리 기술의 침투는 예측 기간 동안 시장 성장을 억제할 것으로 예상됩니다.

이탈리아의 SLI 배터리 산업 개요

이탈리아의 SLI 배터리 시장은 반분열 상태입니다. 이 시장의 주요 기업(특정한 순서 없음)으로는 Sunlight Group, FAAM, Midac SpA, Accumulatori Ariete SRL, Exide Technologies 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

성장하는 자동차 산업

산업용도에 있어서의 배터리의 채용 확대

억제요인

대체 배터리 화학과의 경쟁

공급망 분석

PESTLE 분석

투자 분석

제5장 시장 세분화

유형별

침수형 배터리

VRLA 배터리

EBF 배터리

최종 사용자별

자동차용

기타

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

Strategies Adopted & SWOT Analysis for Leading Players

기업 프로파일

Sunlight Group

FAAM

Midac SpA

Accumulatori Ariete SRL

Exide Technologies

Johnson Controls

EnerSys

Leoch International Technology Limited Inc.

C&D Technologies Inc.

Trojan Battery Company

기타 저명한 기업 리스트

시장 랭킹, 점유율 분석

제7장 시장 기회와 앞으로의 동향

배터리 기술의 혁신

HBR

영문 목차

영문목차

The Italy SLI Battery Market size is estimated at USD 0.79 billion in 2025, and is expected to reach USD 0.94 billion by 2030, at a CAGR of 3.67% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as the growing automotive industry in the region and the increasing adoption of SLI batteries in industrial applications are expected to be among the most significant drivers for the Italian SLI battery market during the forecast period.

On the other hand, there is increasing competition from alternate battery chemistries that pose a threat to the market's growth during the forecast period.

Nevertheless, continued efforts to conduct research and development regarding SLI batteries are expected to create several future market opportunities.

Italy SLI Battery Market Trends

The Automotive Segment is Expected to Witness Significant Growth

Automotive represents a crucial end-user segment for the Italy SLI battery market. This segment encompasses a wide range of vehicles, including passenger cars, commercial vehicles, and motorcycles, all of which rely heavily on SLI batteries for their essential functions. In Italy, a country renowned for its automotive heritage and production, the demand for high-quality SLI batteries remains consistently strong.

For example, data from the International Organization of Motor Vehicle Manufacturers highlighted a notable upswing in vehicle manufacturing in Italy. This surge could be attributed to the increase in demand for vehicles and increased citizens' disposable incomes. Specifically, between 2022 and 2023, production saw a remarkable uptick of over 10.5%, with an average annual growth rate of 3.3%. This growth positively impacted the market for SLI batteries, as the increased vehicle production led to higher demand for these essential automotive components.

The passenger car category plays a dominant role in shaping the market. With a growing emphasis on vehicle electrification and the gradual shift toward hybrid and electric vehicles, the requirements for SLI batteries in conventional internal combustion engine (ICE) vehicles continue to evolve.

While the transition to electric mobility is underway, ICE vehicles still constitute a significant portion of the Italian automotive market, ensuring a steady demand for SLI batteries. Moreover, the increasing integration of advanced technologies and features in modern vehicles has led to heightened power requirements, prompting the development of more robust and efficient SLI batteries to meet these demands.

For instance, in December 2023, Valeo's Pianezza and Santena sites announced their focus on developing and producing distinctive products. Pianezza specializes in lighting, while Santena is dedicated to human-machine interfaces. Specifically, Valeo will be developing and producing a range of human-machine interface technologies, including panel controls, touch screens, switches, and paddle gear shifts, catering to a wide array of car brands. Additionally, these sites are involved in the development and production of SLI batteries, which are essential for vehicle performance and reliability.

The growth of e-commerce and last-mile delivery services has further bolstered the demand for light commercial vehicles, indirectly driving the need for reliable SLI batteries. Additionally, the ongoing efforts to modernize and expand Italy's public transportation infrastructure have contributed to increased demand for SLI batteries in the bus and coach industry, where battery reliability is paramount for ensuring uninterrupted service and passenger safety.

Therefore, as per the points mentioned above, the automotive end-user segment is expected to witness significant growth during the forecast period.

Competition From Alternative Battery Technology to Restrain Market Growth

The market faces increasing competition from alternative battery technologies, which is expected to significantly restrain its growth in the coming years. This competition primarily stems from advancements in lithium-ion battery technology and the gradual shift toward vehicle electrification. As the automotive industry undergoes a transformative phase, moving away from traditional internal combustion engines toward hybrid and fully electric powertrains, the demand for conventional lead-acid SLI batteries is under pressure.

Lithium-ion batteries, known for their higher energy density, longer lifespan, and faster charging capabilities, are becoming increasingly viable alternatives for vehicle starting and auxiliary power functions. While initially more expensive, the declining costs of lithium-ion technology, coupled with its performance advantages, are making it an attractive option for automakers and consumers alike. This trend is particularly pronounced in the premium and luxury vehicle segments, where the additional cost of advanced battery systems can be more easily absorbed.

In recent years, the price of lithium-ion batteries and cell packs has been on the decline, which has made them more attractive to end-user industries. After experiencing slight price hikes in 2022, battery prices again declined in 2023. The cost of lithium-ion battery packs decreased by 14% to reach a historic low of USD 139/kWh. This reduction can be attributed to decreases in raw material and component prices and an expansion in production capacity throughout the battery value chain.

The rising adoption of start-stop technology in conventional vehicles presents another challenge to the traditional SLI battery market in Italy. Start-stop systems, which automatically shut off the engine when the vehicle is stationary and restart it when needed, require more robust battery performance to handle frequent cycling.

While enhanced flooded batteries (EFB) and absorbent glass mat (AGM) lead-acid batteries have been developed to meet these demands, lithium-ion batteries are increasingly being considered for this application due to their superior cycle life and charge acceptance. As start-stop systems become more prevalent across vehicle classes in response to stringent emissions regulations and fuel efficiency standards, the market share of conventional SLI batteries may decrease in favor of more advanced technologies.

The development of advanced energy storage systems for vehicles is more comprehensive than lithium-ion technology. Research into alternative battery chemistries, such as solid-state batteries, lithium-sulfur batteries, and sodium-ion batteries, is progressing rapidly. While these technologies still need to be commercially viable for widespread automotive use, they hold the promise of even greater energy density, safety, and performance compared to current lithium-ion batteries.

For instance, in February 2024, FAAM, an Italian battery manufacturer headquartered in Teverola, disclosed its collaboration with a military submarine program, offering its LFP batteries and cutting-edge BMS technology. These advancements are pivotal in Italy's latest submarine venture, the U212 NFS. As per OCCAR, the lithium battery system's trials underscored heightened operational efficiency, enhanced propulsion, extended endurance, lowered maintenance needs, and top-tier onboard safety protocols.

Therefore, as mentioned above, the penetration of alternative battery technology is expected to restrain the market's growth during the forecast period.

Italy SLI Battery Industry Overview

The Italian SLI battery market is semi-fragmented. Some of the key players in this market (in no particular order) include Sunlight Group, FAAM, Midac SpA, Accumulatori Ariete S.R.L., and Exide Technologies.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Automotive Industry

4.5.1.2 Growing Adoption of Batteries in the Industrial Applications

4.5.2 Restraints

4.5.2.1 Competition From Alternative Battery Chemistries

4.6 Supply Chain Analysis

4.7 PESTLE Analysis

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Flooded Battery

5.1.2 VRLA Battery

5.1.3 EBF Battery

5.2 End-User

5.2.1 Automotive

5.2.2 Others

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted & SWOT Analysis for Leading Players