ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

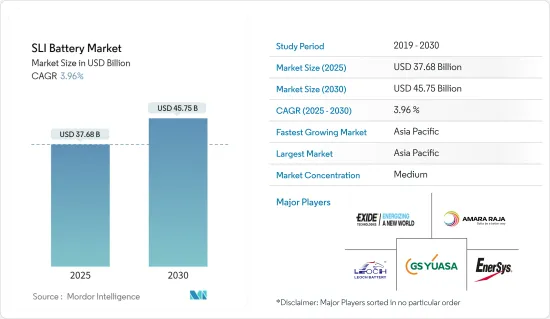

SLI 배터리 시장 규모는 2025년 376억 8,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 3.96%의 CAGR로 2030년에는 457억 5,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

중기적으로는 자동차 보급과 산업 및 농업용 SLI 배터리 수요 증가가 예측 기간 동안 SLI 배터리 시장을 견인할 것으로 예상됩니다.

반면, 대체 배터리의 보급과 엄격한 정부 규제는 예측 기간 동안 시장 성장에 걸림돌이 될 것으로 예상됩니다.

배터리 재활용에 대한 관심이 높아지고 신차 및 애프터마켓 교체 시장에서의 신흥 시장 확대는 SLI 배터리 시장에 기회를 가져다 줄 가능성이 높습니다.

SLI 배터리 시장 동향

자동차 부문이 괄목할만한 성장을 이뤄

자동차 부문 시동, 조명 및 점화(SLI) 배터리 시장은 자동차 산업의 성장과 신뢰할 수 있는 전원 공급 장치에 대한 지속적인 수요로 인해 크게 성장할 것으로 예상되며, SLI 배터리는 자동차에 필수적인 부품으로 엔진 시동, 전기 시스템 작동 및 적절한 점화에 필요한 전력을 공급합니다.

전 세계 자동차 보유량이 지속적으로 증가함에 따라 SLI 배터리에 대한 수요는 계속 증가하고 있습니다. 예를 들어, 국제자동차산업협회(OICA)에 따르면 2023년 세계 자동차 판매량은 약 9,272만 4,000대로 2022년 전년 대비 11.89% 증가할 것으로 예상됩니다.

2023년 세계 자동차 총 판매량 중 승용차는 6,527만 2,000대 이상, 상용차는 2,745만 2,000대 이상이 판매될 것으로 예상됩니다. 이러한 추세는 단기적으로 지속될 것으로 예상되며, 예측 기간 동안 SLI 배터리에 대한 큰 수요를 창출할 것으로 예상됩니다. 또한, 강화형 침수형 배터리(EFB)와 흡수형 글래스 매트(AGM) 배터리 등 SLI 배터리 기술의 발전으로 성능과 내구성이 향상되어 시장 성장을 더욱 촉진하고 있습니다.

SLI 배터리 시장은 전기자동차(EV)의 인기 상승과 지속가능한 에너지 솔루션으로의 전환에 따른 도전에 점차 직면할 것으로 예상되며, EV는 일반적으로 리튬이온 배터리를 사용하기 때문에 장기적으로 기존 SLI 배터리에 대한 수요가 감소할 수 있습니다. 수요가 감소할 수 있습니다.

일부 국가에서는 향후 몇 년 동안 단기적으로 휘발유 및 디젤 자동차의 안정적인 보급이 계속될 것입니다. 예를 들어, 2023년 9월 영국 총리는 계획된 금지 조치가 2030-2035년으로 5년 연기될 것임을 확인했습니다. 영국이 정책 전환을 발표하기 전, 정부는 2030년까지 순수 가솔린 및 디젤 차량의 신차 판매를 금지할 예정이었습니다. 현재는 2035년부터 금지할 계획입니다.

정부에 따르면, 이 금지 조치에 따라 2035년부터는 전기 배터리 차량과 무공해 차량만 신차로 구매할 수 있다고 합니다. 그러나 대부분의 운전자는 중고차를 구매하기 때문에 대부분의 사람들은 이 금지령의 영향을 받지 않을 것으로 보입니다. 영향을 받는 것은 휘발유와 디젤 차량의 신차 판매만 해당되며, 기존 차량에는 영향을 미치지 않습니다. 또한, 금지 조치의 연기로 영국은 EU와 보조를 맞추게 되는데, EU는 2035년까지 가솔린 및 디젤 차량의 신차 판매를 금지할 예정입니다.

전반적으로 SLI 배터리 시장은 완만한 속도로 성장세를 유지할 것으로 예상됩니다. 자동차 인프라에 대한 지속적인 투자와 배터리 설계 및 제조 기술 발전이 시장 성장에 중요한 역할을 할 것으로 예상됩니다. 또한, 친환경 SLI 배터리 개발 및 재활용에 대한 노력은 세계 지속가능성 목표에 부합하며, 진화하는 자동차 환경에서 시장의 관련성을 보장합니다.

아시아태평양이 시장을 독점할 것으로 예상

아시아태평양은 SLI(시동-점화-점화) 배터리 시장에서 큰 성장이 예상됩니다. 이는 급속한 도시화, 자동차 생산량 증가, 자동차에 대한 소비자 수요 증가 등 다양한 요인이 복합적으로 작용할 것으로 예상됩니다. 중국, 인도, 일본, 한국 등의 국가들은 대규모 자동차 시장과 자동차 제조 인프라에 대한 대규모 투자로 이러한 성장에 크게 기여하고 있습니다.

국제자동차공업협회(OICA)에 따르면 2023년 중국의 자동차 생산량은 약 3,016만1,000대, 일본은 899만대 이상, 한국은 424만3,000대, 인도는 585만대 이상입니다. 이 때문에 이 지역은 SLI 배터리의 세계 주요 시장 중 하나가 되었습니다. 또한, 도로를 달리는 자동차의 수가 많기 때문에 SLI 배터리 교체 시장도 상당한 규모를 형성하고 있습니다.

최근 일부 대형 자동차 제조업체들은 이 지역에 가솔린 및 디젤을 연료로 하는 자동차 제조 시설을 개발 및 확장할 계획을 세우고 있습니다. 예를 들어, 일본의 대형 자동차 제조업체인 도요타는 2023년 11월 카르나타카 주정부와 연간 생산능력 10만 대를 증설하는 인도 3번째 제조공장 설립을 위한 양해각서를 체결한 바 있습니다. 이번 공장은 방갈로르 인근 비다디에 건설될 예정이며, 기존 2개 공장에 근접한 곳에 약 330억 인도 루피가 투자될 것으로 예상됩니다.

기존 비다디 공장의 연간 생산량은 총 4,000대 정도이며, 2026년까지 가동될 이 신공장은 Toyota의 생산능력을 약 30% 가량 증대시킬 계획입니다. 이번 발표는 인도에서 25년의 역사를 가진 Toyota 브랜드에 힘을 실어주는 것입니다. 회사 측에 따르면, 신공장은 2026년까지 출시될 예정인 3열 시트 SUV의 주요 생산 기지가 될 것이며, 연간 6만 대를 생산할 계획이라고 합니다. 이러한 자동차 제조의 발전은 향후 몇 년 동안 SLI 배터리의 채택을 촉진할 것으로 예상됩니다.

또한, GS Yuasa Corporation 등 SLI 배터리의 주요 기업 중에는 자회사인 GS Yuasa International Ltd(GS Yuasa)의 지분법 적용 계열사인 인도에 본사를 둔 Tata AutoComp GY Batteries 2005년 10월에 설립된 TGY는 아시아 최대의 이륜차 생산국인 인도에서 점유율 확대를 목표로 연간 840만 개의 이륜차용 축전지 생산능력을 두 배로 늘리겠다고 발표했습니다.

TGY는 2021년 공장 내 신규 증설동에서 생산을 시작했으며, 2022년에는 새로운 생산라인을 증설하여 본격적인 양산에 돌입합니다. 이를 통해 TGY는 생산능력을 지속적으로 확대하여 증설 전 420만 개에서 2배 증가한 연간 840만 개의 이륜차용 축전지를 생산할 수 있는 생산체제를 구축할 계획입니다. 공장 증설로 인해 회사가 생산하는 배터리 모델의 폭이 넓어질 것으로 기대됩니다. 또한 TGY는 자동차용 납축배터리 생산도 강화할 예정이며, 향후 수요 확대가 예상되는 스타트&스톱 차량 등 친환경 차량용 고성능 납축배터리에 집중할 계획입니다.

따라서 위의 요인으로 인해 아시아태평양은 예측 기간 동안 SLI 배터리 시장에서 눈에 띄는 성장을 이룰 것으로 예상됩니다.

SLI 배터리 산업 개요

SLI 배터리 시장은 반분할되어 있습니다. 이 시장의 주요 기업으로는 GS Yuasa International Ltd, Exide Technologies, Amara Raja Energy & Mobility Limited, EnerSys, Leoch International Technology Limited Inc. 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의

조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

자동차 보급 확대

산업·농업 용도에서의 SLI 배터리 수요 확대

성장 억제요인

대체 배터리 보급 확대

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협 제품·서비스

경쟁 기업 간의 경쟁 관계

제5장 시장 세분화

유형

침수형 배터리

VRLA 배터리

EBF 배터리

최종사용자

자동차용

기타

지역

북미

미국

캐나다

기타 북미

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽

러시아

기타 유럽

아시아태평양

중국

인도

일본

한국

태국

말레이시아

인도네시아

베트남

기타 아시아태평양

중동 및 아프리카

사우디아라비아

아랍에미리트

남아프리카공화국

이집트

나이지리아

카타르

기타 중동 및 아프리카

남미

브라질

아르헨티나

칠레

기타 남미

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략과 SWOT 분석

기업 개요

GS Yuasa International Ltd.

Exide Technologies

Amara Raja Energy & Mobility Limited

EnerSys

Leoch International Technology Limited Inc.

East Penn Manufacturing Company

C&D Technologies Inc.

Clarios International Inc.

Trojan Battery Company

Crown Battery Manufacturing Company

기타 저명한 기업 리스트(회사명, 본사 소재지, 관련 제품 및 서비스, 연락처 등)

시장 순위 분석

제7장 시장 기회와 향후 동향

배터리 재활용에 대한 주목 상승

신차 및 애프터마켓용 모두 신흥 시장에서의 확장

ksm

영문 목차

영문목차

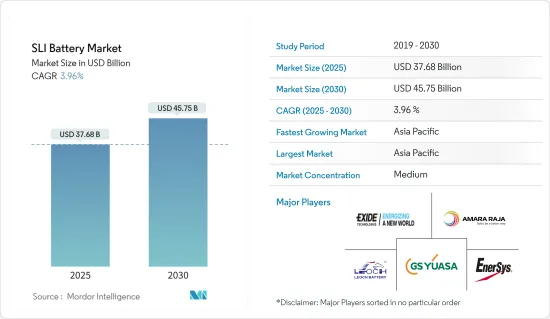

The SLI Battery Market size is estimated at USD 37.68 billion in 2025, and is expected to reach USD 45.75 billion by 2030, at a CAGR of 3.96% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the increasing adoption of motor vehicles and the growing demand for SLI batteries from industrial and agricultural applications are expected to drive the SLI batteries market during the forecast period.

On the other hand, the increasing penetration of alternative battery chemistries and the stringent government regulations are expected to hinder the market's growth during the forecast period.

Nevertheless, the increased focus on battery recycling and the expansion in emerging markets for both new vehicles and after-market replacements will likely create opportunities for the SLI battery market.

SLI Battery Market Trends

Automotive Segment to Witness Significant Growth

The market for starting, lighting, and Ignition (SLI) batteries in the automotive segment is expected to witness notable growth, driven by the expanding automotive industry and the continuous need for reliable power sources. SLI batteries are essential components in motor vehicles, providing the necessary power to start the engine, run electrical systems, and ensure proper ignition.

As the global vehicle fleet continues to grow, the demand for SLI batteries remains robust. For example, as per the International Organization of Motor Vehicle Manufacturers(OICA), the total global motor vehicle sales stood at around 92.724 million in 2023, recording over 11.89% growth compared to the previous years in 2022.

Of the total global motor vehicle sales in 2023, the total passenger vehicles and commercial vehicle sales stood at over 65.272 million and 27.452 million, respectively. Such trends are expected to continue over the short term and create a substantial demand for the SLI battery during the forecast period. In addition, advancements in SLI battery technology, such as enhanced flooded batteries (EFB) and absorbent glass mat (AGM) batteries, are providing improved performance and durability, further propelling market growth.

Despite the positive outlook, the SLI battery market will gradually start facing challenges from the growing popularity of electric vehicles (EVs) and the shift toward more sustainable energy solutions. EVs typically use lithium-ion batteries, which may reduce the demand for traditional SLI batteries in the long term.

Nevertheless, several nations continue to experience a stable adoption of petrol and diesel vehicles over the short term in the coming years. For example, in September 2023, the United Kingdom's Prime Minister confirmed the planned ban was being pushed back five years from 2030 to 2035. Before the United Kingdom announced a shift in policy, the government had planned to ban the sale of new, pure petrol and diesel vehicles by 2030. Now, the plan is for the ban to begin in 2035.

According to the government, under the ban, only electric battery-powered cars and zero-emission vehicles will be able to be bought new from 2035. However, most people will not be impacted by the ban, as most drivers buy vehicles secondhand. Only sales of new petrol and diesel models would be affected, not the existing ones. Moreover, the delay in the ban brings the United Kingdom into line with the European Union, which is also banning sales of new petrol and diesel cars by 2035.

Overall, the SLI battery market is expected to maintain a growth trajectory, albeit at a moderate pace. Continued investments in automotive infrastructure, coupled with technological advancements in battery design and manufacturing, is expected to play a crucial role in market growth. In addition, the development of eco-friendly SLI batteries and recycling initiatives will align with global sustainability goals, ensuring the market's relevance in the evolving automotive landscape.

Asia-Pacific Region is Expected to Dominate the Market

The Asia-Pacific region is expected to witness significant growth in the SLI (Starting, Lighting, and Ignition) battery market. This is likely to be driven by a combination of factors, including rapid urbanization, increasing vehicle production, and growing consumer demand for automobiles. Countries such as China, India, Japan, and South Korea are major contributors to this growth due to their large automotive markets and significant investments in automotive manufacturing infrastructure.

According to the International Organization of Motor Vehicle Manufacturers (OICA), the total number of motor vehicles produced in China stood at around 30.161 million in 2023, Japan produced over 8.99 million, South Korea produced 4.243 million, and India produced over 5.85 million. This makes the region one of the significant markets for SLI batteries worldwide. Moreover, the replacement market for SLI batteries is also substantial due to the high number of vehicles on the road.

Recently, some of the major automobile manufacturers have also planned to develop and expand automobile manufacturing facilities in the region, where the vehicles are fuelled by petrol and diesel. For example, in November 2023, Toyota, one of the largest Japanese automakers, signed a Memorandum of Understanding (MoU) with the government of Karnataka to set up a third manufacturing plant in India, which would increase its production capacity by 1 lakh units per annum. The upcoming plant will also be situated in Bidadi, near Bangalore, near the existing two, and is expected to attract an investment of around INR 3,300 crores.

Toyota's existing plants at Bidadi have a combined output of about 4 lakh units per annum, and this new plant operational by 2026 is planned to add about 30% to Toyota's production capacity. This announcement comes on the back of the brand, which has been completing 25 years in India. According to the company, the new plant will be the primary production base for an upcoming three-row SUV. Toyota is planned to produce 60,000 units annually, with a launch likely by 2026. Such developments in automobile manufacturing are expected to boost the adoption of SLI batteries in the coming years.

Furthermore, some of the leading SLI battery players, such as GS Yuasa Corporation, announced that their India-based company Tata AutoComp GY Batteries Private Ltd (TGY), an equity-method affiliate of subsidiary GS Yuasa International Ltd (GS Yuasa), aims to double its annual production capacity for motorcycle lead-acid batteries to 8.4 million units. TGY, which was established in October 2005, is aiming to boost its market share in India, Asia's largest motorcycle-producing country.

TGY launched production in a newly added wing at its plant in 2021 and began full-fledged mass production with the addition of a new production line in 2022. With this, TGY aims to continue expanding production capacity and establish a production system capable of producing 8.4 million lead-acid motorcycle batteries per year, double its pre-expansion capacity of 4.2 million units. The plant expansion is expected to enable the company to expand the range of battery models it manufactures. In addition, TGY is expected to strengthen its production of automotive lead-acid batteries, with a focus on high-performance lead-acid batteries for environment-friendly vehicles, such as start & stop vehicles, demand for which is expected to continue growing in the coming years.

Therefore, owing to the abovementioned factors, the Asia-Pacific region is anticipated to witness notable growth for the SLI battery market during the forecast period.

SLI Battery Industry Overview

The SLI battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include GS Yuasa International Ltd, Exide Technologies, Amara Raja Energy & Mobility Limited, EnerSys, and Leoch International Technology Limited Inc.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Adoption of Motor Vehicles

4.5.1.2 Growing Demand for SLI Batteries from Industrial and Agricultural Applications

4.5.2 Restraints

4.5.2.1 Increasing Penetration of Alternative Battery Chemistries

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Flooded Battery

5.1.2 VRLA Battery

5.1.3 EBF Battery

5.2 End-User

5.2.1 Automotive

5.2.2 Others

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Nordic

5.3.2.7 Russia

5.3.2.8 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Thailand

5.3.3.6 Malaysia

5.3.3.7 Indonesia

5.3.3.8 Vietnam

5.3.3.9 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 Saudi Arabia

5.3.4.2 United Arab Emirates

5.3.4.3 South Africa

5.3.4.4 Egypt

5.3.4.5 Nigeria

5.3.4.6 Qatar

5.3.4.7 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Chile

5.3.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted & SWOT Analysis for Leading Players

6.3 Company Profiles

6.3.1 GS Yuasa International Ltd.

6.3.2 Exide Technologies

6.3.3 Amara Raja Energy & Mobility Limited

6.3.4 EnerSys

6.3.5 Leoch International Technology Limited? Inc.

6.3.6 East Penn Manufacturing Company

6.3.7 C&D Technologies Inc.?

6.3.8 Clarios International Inc.?

6.3.9 Trojan Battery Company

6.3.10 Crown Battery Manufacturing Company

6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increased Focus on Battery Recycling

7.2 Expansion in Emerging Markets for Both New Vehicles and After-Market Replacements