납축 배터리 스크랩 시장 전망 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Lead Acid Battery Scrap - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636228

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

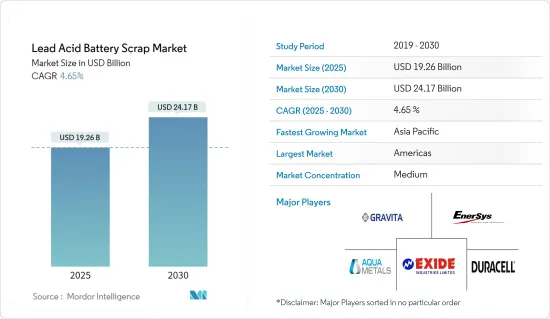

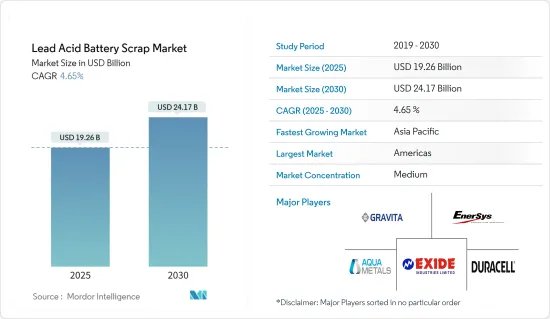

납축 배터리 스크랩 시장 규모는 2025년에 192억 6,000만 달러로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 4.65%로, 2030년에는 241억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 UPS 시스템, 시동 조명, 자동차용 점화 전원과 같은 소규모 전력 저장 장치와 대규모 그리드 규모의 전력 시스템에서 배터리 스크랩으로 생산된 새로운 납축배터리의 사용 증가가 시장 성장을 견인할 것으로 예상됩니다

반면에 높은 비용, 강력한 공급망 부족, 납축 배터리 스크랩과 관련된 낮은 수율은 향후 몇 년간 시장 성장을 저해할 것으로 예상됩니다.

납축 배터리 스크랩 수거의 기술 혁신과 납축 배터리 재활용에 대한 전 세계적인 환경 문제 증가는 시장 성장에 상당한 기회를 제공할 것입니다.

납축 배터리 스크랩 시장 동향

시장을 독점하는 침수 배터리

침수 배터리는 자동차, 고정식(대형) 무정전 전원 공급 장치 및 독립형 에너지 시스템에서 널리 사용됩니다. 통풍식 납축(VLA) 배터리라고도 하는 이 배터리는 상단, 측면의 음극(스펀지 리드) 및 양극 이산화납(PbO2) 단자와 상단의 통풍구 캡으로 구성되어 있습니다.

국제에너지기구 전기차 전망 보고서에 따르면 2023년 전 세계적으로 1,330만 대 이상의 전기차(BEV 및 PHEV)가 판매되었으며, 2024년에는 35% 더 성장하여 1,700만 대에 달할 것으로 예상됩니다. 전체 자동차 시장에서 전기차가 차지하는 비중은 2020년 약 4%에서 2023년 18%로 크게 증가할 것으로 예상됩니다. 전기차의 증가는 새로운 배터리나 다른 제품을 생산하는 데 배터리를 재사용할 수 있기 때문에 범람하는 배터리 스크랩 시장에 활력을 불어넣을 것으로 예상됩니다.

또한, 최근 향상된 침수 배터리(EFB)와 같은 침수 납축 배터리 기술의 발전으로 배터리 무게는 높지만(SLI보다 2-3kg 이상) 비용은 훨씬 낮으면서도 흡수성 유리 매트(AGM) 배터리와 동등한 사이클 수명을 달성할 수 있는 것으로 입증되었습니다. EFB 기술은 납판 제조에 탄소 첨가제를 추가하여 충전 수용 능력을 개선하고 충전 작동 상태(점화용)에서 주기적 내구성을 높입니다.

국제자동차제작자협회(OICA)에 따르면 2023년에 전 세계적으로 9,400만 대의 자동차가 생산될 것으로 예상했습니다. 자동차 판매량이 증가하면 납축 배터리가 필요해지고 시장의 성장을 주도할 것입니다.

따라서 배터리 스크랩 활동을 촉진하기위한 정부의 노력, 배터리 자동차용 납축 배터리 사용 증가 및 에너지 저장 시스템이 예측 기간 동안 침수 배터리 사용을 주도 할 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양 지역에서 중국과 인도와 같은 국가는 자동차 생산 및 판매 측면에서 세계 최대의 자동차 산업 시장입니다. 중국의 전 세계 자동차 생산량 점유율은 10년 넘게 상승세를 이어가고 있습니다. 2023년 중국의 점유율은 2008년에 비해 1.8배 가까이 증가했습니다.

Duracell Inc., CATL, Exide Industries Ltd, Amara Raja Energy와 같은 지역 납축 배터리 업체들은 주로 유지보수가 적은 2-12볼트 배터리 범위 내의 제품을 제공함으로써 태양 에너지 납축 배터리 포트폴리오의 실행 가능성과 효율성을 높이는 데 주력하고 있습니다. 이러한 배터리는 본질적으로 정기적인 딥 사이클 작업에 적합하며 주로 고된 태양 광 발전(SPV) 애플리케이션을 위해 설계되었습니다.

또한 2023년 인도의 총 자동차 생산량은 약 2,593만 대로 전년 대비 증가했습니다. 반면, 총 승용차 판매량은 2,711,457대에서 3,069,499대로 증가했습니다.

또한 인도는 2030년까지 전체 차량 판매량의 30%를 전기자동차로 채우는 것을 목표로 하고 있습니다. 충전소의 성장을 장려하기 위해 인도 정부는 대체 연료 인프라 개발을 장려하기 위해 보조금 및 보조금과 같은 여러 제도를 시행하고 있습니다. 중국 정부는 2030년까지 배기가스 배출량을 최대치에 도달하고 신규 전기차가 도로 주행 차량의 40%를 차지하도록 하는 것을 목표로 하고 있습니다. 중국과 인도에서 배터리 자동차 보급이 증가하면 납축 배터리 사용량이 증가할 것이며, 이러한 배터리는 새 배터리나 다른 제품을 생산하는 데 재사용할 수 있기 때문에 배터리 스크랩 시장의 발전이 촉진될 수 있습니다.

또한, 2024년 1월 인도 환경산림기후변화부(MoEFCC)는 납 스크랩을 사용한 납축 배터리를 재활용하기 위한 표준 운영 절차를 발표했습니다. 이 SOP는 환경 및 건강 위험을 최소화하면서 납 함유 폐기물의 수입, 운송 및 재활용을 규제하는 것을 목표로 합니다.

위의 사항으로 인해 아시아 태평양 지역에서 배터리 자동차에 납축 배터리의 사용이 증가함에 따라 예측 기간 동안 납축 배터리 스크랩 시장이 성장할 수있는 길을 만들 것입니다.

납축 배터리 스크랩 업계 개요

납축 배터리 스크랩 시장은 세분화되어 있습니다. 시장에서 사업을 전개하고 있는 주요 기업(특정한 순서 없음)에는 Gravita India Ltd, Enersys, Exide Industries Ltd, Aqua Metals Inc., Duracell Inc. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

자동차 산업에의 납축 배터리의 이용 확대

환경 문제에 대한 관심 증가

억제요인

비용 상승, 강력한 공급망의 부족

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지 유형별

침수형

밀폐형

배출원별

자동차

무정전 전원 장치

텔레콤 스테이션

전력

지역별

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

스페인

노르딕

터키

러시아

기타 유럽

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

이집트

나이지리아

카타르

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Gravita India Ltd

Enersys

Exide Industries Ltd

Aqua Metals Inc.

Duracell Inc.

AMIDT Group

Engitec Technologies SpA

Ecobat Technologies Ltd

시장 랭킹 분석

기타 유명 기업 일람

제7장 시장 기회와 앞으로의 동향

배터리 폐기에 있어서의 기술 혁신과 조사

HBR

영문 목차

영문목차

The Lead Acid Battery Scrap Market size is estimated at USD 19.26 billion in 2025, and is expected to reach USD 24.17 billion by 2030, at a CAGR of 4.65% during the forecast period (2025-2030).

Key Highlights

Over the medium term, increasing usage of new lead-acid batteries produced from battery scrap in small-scale power storage such as UPS systems, starting lighting, and ignition power sources for automobiles, along with large, grid-scale power systems, are expected to drive the growth of the market.

On the other note, higher costs, lack of a strong supply chain, and low yield related to lead acid battery scrap are expected to hinder market growth in the coming years.

Technological innovations in lead acid battery scrap collection and increasing global environmental concerns for lead acid battery recycling will provide significant opportunities for market growth.

Lead Acid Battery Scrap Market Trends

Flooded Batteries to Dominate the Market

Flooded batteries are widely used in automobiles, stationary (large) uninterrupted power supplies, and stand-alone energy systems. Also known as vented lead-acid (VLA) batteries, they consist of a negative (sponge lead) and a positive lead dioxide (PbO2) terminal on the top/side, along with the covering of vent caps on their top.

According to the International Energy Agency Electric Vehicle Outlook Report, more than 13.3 million electric cars (BEV and PHEV) were sold worldwide in 2023, and sales are expected to grow by another 35% in 2024 to reach 17 million. This significant growth in electric cars' share of the overall car market rose from around 4% in 2020 to 18% in 2023. The rise in electric vehicles is expected to give impetus to the flooded battery scrap market since these batteries can be reused to produce new batteries or other products.

Moreover, recent advancements in flooded lead-acid battery technology, such as enhanced flooded batteries (EFB), have demonstrated to achieve equivalent cycle life as absorbent glass mat (AGM) batteries at a high battery weight (2-3 kg above SLI) but significantly lower cost. EFB technology employs the addition of carbon additives in lead plate manufacturing to improve charged acceptance capability and increase cyclic durability in a reduced state of charge operation (ignition applications).

According to the Organisation Internationale des Constructeurs d'Automobiles, 94 million motor vehicles were produced worldwide in 2023. The increase in automobile sales will, in turn, require lead acid batteries and drive the growth of the market.

Therefore, government initiatives to boost battery scrap activities, growing lead acid battery utilization for electric vehicles, and energy storage systems are anticipated to drive the usage of flooded batteries during the forecast period.

Asia-Pacific to Dominate the Market

In Asia-Pacific, countries like China and India are home to the world's largest market for the automobile industry in terms of automotive production and sales. China's share of global vehicle production has been rising for over a decade. Its share in 2023 increased nearly 1.8 times over 2008.

Regional lead acid battery players such as Duracell Inc., CATL, Exide Industries Ltd, and Amara Raja Energy are focusing on increasing the viability and efficiency of their solar energy lead acid battery portfolios by offering products within the 2-volt to 12-volt battery range, primarily with low maintenance. These batteries are intrinsically suited for regular deep cyclic duty and are primarily designed for arduous solar photovoltaic (SPV) applications.

Moreover, in 2023, the total production volume of vehicles in India was around 25.93 million units, an increase from the previous year. On the other hand, total passenger vehicle sales increased from 2,711,457 to 3,069,499 units.

Also, India aims for 30% of all vehicle sales to be electric by 2030. To encourage the growth of charging stations, the Indian government has launched several schemes, such as subsidies and grants, to incentivize alternative fuel infrastructure development. The Chinese government aims to reach peak emissions by 2030 and have new electric vehicles account for 40% of cars on the road. The growing electric vehicle penetration in China and India will, in turn, create avenues for growth in the usage of lead acid batteries and may facilitate the development of the battery scrap market since these batteries can be reused to produce new batteries or other products.

Also, in January 2024, the Ministry of Environment, Forest and Climate Change (MoEFCC) of India released the standard operating procedure for recycling lead scrap/used lead acid batteries. The SOP aims to regulate the import, transport, and recycling of lead-bearing waste while minimizing environmental and health risks.

Owing to the above points, the growing use of lead acid batteries for electric vehicles in Asia-Pacific will create avenues for the growth of the lead acid battery scrap market during the forecast period.

Lead Acid Battery Scrap Industry Overview

The lead acid battery scrap market is semi-fragmented. Some of the major companies operating in the market (in particular order) include Gravita India Ltd, Enersys, Exide Industries Ltd, Aqua Metals Inc., and Duracell Inc.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Usage of Lead Acid batteries in the Automotive Industry

4.5.1.2 Increasing Environmental Concerns

4.5.2 Restraints

4.5.2.1 Higher Costs, Lack of a Strong Supply Chain

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Flooded

5.1.2 Sealed

5.2 Source

5.2.1 Motor Vehicles

5.2.2 Uninterrupted Power Supply

5.2.3 Telecom Stations

5.2.4 Electric Power

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 France

5.3.2.3 United Kingdom

5.3.2.4 Spain

5.3.2.5 NORDIC

5.3.2.6 Turkey

5.3.2.7 Russia

5.3.2.8 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Malaysia

5.3.3.6 Thailand

5.3.3.7 Indonesia

5.3.3.8 Vietnam

5.3.3.9 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 United Arab Emirates

5.3.5.3 South Africa

5.3.5.4 Egypt

5.3.5.5 Nigeria

5.3.5.6 Qatar

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Gravita India Ltd

6.3.2 Enersys

6.3.3 Exide Industries Ltd

6.3.4 Aqua Metals Inc.

6.3.5 Duracell Inc.

6.3.6 AMIDT Group

6.3.7 Engitec Technologies SpA

6.3.8 Ecobat Technologies Ltd

6.4 Market Ranking Analysis

6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Innovations and Research in Battery Scrapping