ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

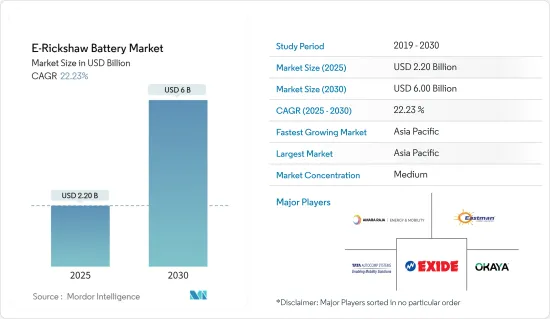

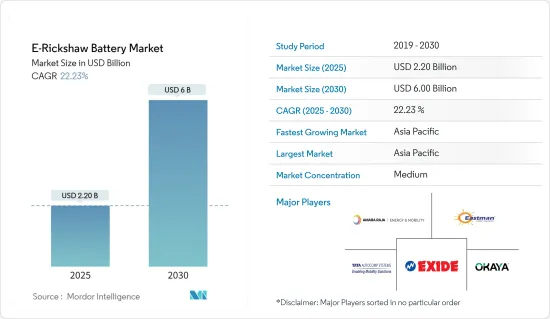

전기 릭샤용 배터리 시장 규모는 2025년 22억 달러로 추정되며, 예측 기간(2025-2030년) 동안 22.23%의 CAGR로 2030년에는 60억 달러에 달할 것으로 예상됩니다.

주요 하이라이트

중기적으로는 정부의 이니셔티브에 의해 E-릭샤의 보급이 확대되고, 기존 화석연료 기반의 E-릭샤에 비해 운행비용과 유지보수 비용이 낮기 때문에 예측 기간 동안 E-릭샤용 배터리 시장이 견인할 것으로 예상됩니다.

반면, 충전 인프라의 미비한 보급과 이용의 어려움, 전기택시의 주행거리가 제한적이라는 점은 예측 기간 동안 전기택시용 배터리 시장의 성장을 저해할 수 있는 요인입니다.

에너지 밀도 향상, 전기택시용 배터리 교체 인프라 도입 등 배터리 기술의 지속적인 발전은 전기택시용 배터리 시장에 큰 기회를 가져다 줄 것으로 보입니다.

아시아태평양은 배터리 구동 차량의 채택이 증가함에 따라 전기 릭샤 시장의 지배적인 지역이 될 것으로 예상됩니다.

전기 릭샤용 배터리 시장 동향

리튬이온 배터리 급성장

다양한 종류의 배터리 기술 중 리튬이온 배터리(LIB)는 예측 기간 동안 가장 빠르게 성장하는 전자 릭샤용 배터리 시장 중 하나가 될 것으로 예상됩니다. 리튬이온 배터리는 용량 대 중량 비율이 우수하여 다른 배터리 유형에 비해 인기가 높아지고 있습니다. 리튬이온 배터리의 보급을 촉진하는 다른 요인으로는 성능 향상(긴 수명, 낮은 유지보수), 저장성 향상, 가격 하락 등이 있습니다.

리튬이온(Li-ion) 배터리는 납축배터리 등 다른 기술에 비해 다양한 기술적 이점을 가지고 있습니다. 평균적으로 리튬이온 배터리는 5,000회 이상의 사이클 수명을 가지며, 납축배터리는 400-500회 정도입니다. 리튬이온 배터리는 납축배터리만큼 자주 유지보수 및 교체가 필요하지 않습니다. 또한, 리튬이온 배터리는 방전 사이클 내내 전압을 유지하므로 전기 부품의 효율을 높이고 더 오래 사용할 수 있습니다.

최근 몇 년 동안 여러 대형 리튬이온 배터리 제조업체들이 규모의 경제를 달성하기 위한 투자와 성능 향상을 위한 연구개발 활동을 진행하면서 경쟁이 치열해져 리튬이온 배터리 가격이 하락하고 있습니다. 예를 들어, 기술 혁신, 제조 개선, 원자재 가격 하락으로 리튬이온 배터리의 체적 가중 평균 가격은 2013년 780달러/kWh에서 2023년 139달러/kWh로 크게 하락했으며, 2025년에는 약 113달러/kWh, 2030년에는 80달러/kWh에 도달할 것으로 예상됩니다. 에 도달할 가능성이 높습니다. 이러한 배터리 비용의 하락 추세는 향후 몇 년 동안 전기 릭샤용 배터리 시장에서 모든 배터리 중에서 리튬이온 배터리가 유리한 선택이 될 가능성이 높습니다.

리튬이온 배터리는 기존에는 휴대폰, 노트북 등 민생용 전자기기에 사용되어 왔습니다. 그러나 최근에는 환경 부하가 적다는 점 등을 이유로 각국의 전기 릭샤를 포함한 전기자동차(BEV)의 전원으로 재설계되는 사례가 늘고 있습니다.

한국 재무부는 2023년 12월, 향후 5년간 리튬 배터리 산업에 38조 원 규모의 정책금융을 지원할 계획을 발표했습니다. 이 정책은 2024년에 정식으로 시행될 예정입니다. 한국은 또한 1조원 규모의 리튬배터리 산업진흥기금을 조성하고, 관련 기술 연구개발에 736억원을 투자할 계획입니다. 동시에 정부는 국내 리튬 배터리 제조에 필요한 핵심 광물 매장량을 늘리고, 배터리 재사용 및 재활용 생태계를 육성하기로 했습니다. 이 모든 것이 리튬이온 배터리 산업을 촉진하고, 궁극적으로 전자 릭샤용 배터리 시장의 성장을 뒷받침할 것으로 예상됩니다.

아시아태평양에서는 리튬이온 배터리 생산이 증가하는 추세입니다. 예를 들어, Panasonic Group은 2024년 3월 Indian Oil Corp(IOCL)과 합작 회사를 설립하여 원통형 리튬이온 배터리를 생산할 것이라고 발표했습니다. 그룹사인 파나소닉 에너지는 IOCL과 원통형 리튬이온 배터리를 제조하는 합작회사 설립의 틀을 마련하기 위해 IOCL과 구속력 있는 계약서에 서명하고 협의를 시작했습니다. 이 구상은 인도 시장에서 이륜차 및 삼륜차 배터리에 대한 수요가 확대될 것으로 예상되기 때문입니다.

2023년 5월, Stellantis는 TotalEnergies, Mercedes-Benz와 함께 프랑스 빌리베르크로 뒤브랑에 Automotive Cells Company(ACC)의 배터리 기가 공장 준공식을 가졌습니다. 초기 생산능력은 13기가와트시(GWh)이며, 2030년까지 40기가와트시(GWh)까지 증가하여 CO2 배출을 최소화한 고성능 리튬이온 배터리를 공급할 것으로 기대됩니다. 이 기가팩토리는 2030년까지 유럽 내 배터리 생산능력을 250GWh까지 끌어올리겠다는 스텔란티스의 목표에 기여하게 될 것입니다.

또한, 에너지효율 및 재생에너지부에 따르면, 정부는 2023년 북미 지역에 전기자동차 배터리 공장을 개발할 것이라고 발표했습니다. 이 지역의 생산능력은 2021년 연간 55기가와트시(GWh/년)에서 2030년 1,000GWh/년으로 증가할 것으로 예상됩니다. 파이프라인에 있는 대부분의 프로젝트는 2025-2030년 사이에 생산을 시작할 것으로 예상됩니다. 이는 차량용 배터리 시장 개척이 순조롭게 진행되고 있음을 의미하며, 향후 몇 년 동안 E-Rickshaw용 배터리 시장을 뒷받침할 것으로 예상됩니다.

2024년 1월, Panasonic Energy는 캔자스주 데소토에 건설 중인 40억 달러 규모의 전기자동차 배터리 공장에 대한 최신 정보를 발표했습니다. 회사 측에 따르면, 이 제조 시설은 초당 66개의 리튬이온 배터리를 생산할 수 있으며, 470만 평방피트 규모의 배터리 공장은 선플라워 육군 탄약 공장 부지에 건설 중이며, 2025년 3월에 생산을 시작할 예정입니다. 이러한 리튬이온 배터리의 개발은 앞으로도 전 세계적으로 지속될 것으로 예상되며, E-Rickshaw용 배터리 시장을 뒷받침할 것으로 보입니다.

리튬이온 배터리의 경량화, 충전 시간 단축, 충전 주기 증가, 비용 절감, 리튬이온 배터리의 발전 등의 특성으로 인해 리튬이온 배터리는 예측 기간 동안 전기 릭샤용 배터리 시장을 포함한 전기자동차에서 가장 빠르게 성장하는 배터리 유형이 될 가능성이 높습니다.

아시아태평양이 시장을 독점할 것으로 예상

아시아태평양은 몇 가지 매력적인 요인으로 인해 예측 기간 동안 전자 릭샤용 배터리 시장을 장악할 것으로 예상됩니다. 예를 들어, 인도, 중국, 방글라데시 등의 국가에서는 인구 밀도가 높고 도시화가 빠르게 진행됨에 따라 효율적이고 저렴한 교통수단에 대한 수요가 증가하고 있으며, 전기 릭샤는 근거리 이동에 적합한 선택이 되고 있습니다. 이러한 높은 수요는 E-Rickshaw용 배터리의 견조한 시장과 직결됩니다.

이 지역의 여러 신흥국에서는 전자 택시의 도입에 대한 정부의 지원이 눈에 띄게 증가하고 있습니다. 특히 인도는 공해 방지 및 화석연료 의존도 감소를 위한 광범위한 노력의 일환으로 전기 릭샤를 포함한 전기자동차의 도입을 촉진하기 위해 지원적인 규제, 보조금, 인센티브를 시행하고 있습니다. 예를 들어, 인도의 FAME(Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) 제도는 전기 릭샤를 포함한 전기자동차 도입에 큰 인센티브를 제공했습니다.

2024년 3월, 인도 중공업부(MHI)는 상업용 이륜차 및 삼륜차 전기자동차의 채택을 촉진하고 인도에서 전기자동차의 개발 및 제조에 필요한 지원을 제공하는 것을 목표로 하는 전기 모빌리티 추진 계획(EMPS)을 시작했습니다.

EMPS-2024는 2024년 4월 1일부터 2024년 7월 31일까지 4개월간 시행됩니다. 예산은 500억 인도 루피로 EV에 보조금을 지급합니다. 이륜차 EV는 1대당 최대 1만 루피, 소형 삼륜차 EV는 최대 2만 5,000루피, 대형 삼륜차 EV는 최대 5만 루피가 지원됩니다. 미쓰비시중공업은 EV 판매 시 보조금과 수요 장려금을 EV 제조업체에 환급하지만, 최종 청구 가격에서 보조금이 차감되기 때문에 EV 구매 가격이 낮아져 소비자에게도 혜택이 돌아갑니다. 이러한 노력으로 국내 전기택시 및 관련 배터리의 도입이 촉진될 것으로 기대됩니다.

인도 도로교통부에 따르면 2023년 인도의 전기 세발자전거 연간 판매량은 58만 1,000대 이상입니다. 국제에너지기구(IEA)의 데이터에 따르면, 2023년 세계 전기 세발자전거 판매량 점유율은 중국과 인도가 66%를 차지할 것으로 예상됩니다. 이는 이들 국가들이 예측 기간 동안에도 엄청난 성장을 지속하고 이를 확인할 가능성이 높다는 것을 강조합니다.

또한, Exide Industries, Amara Raja Batteries, Okaya Power 등 이 지역의 주요 배터리 제조업체들은 최신 배터리 기술 및 혁신에 쉽게 접근할 수 있어 시장 성장을 촉진하고 있습니다. 또한, 이들 기업은 배터리 성능 향상, 비용 절감, 배터리 수명 연장을 위한 연구개발에 지속적으로 투자하고 있으며, 이는 소비자에게 더욱 매력적인 제품으로 거듭나고 있습니다.

아시아태평양은 저렴한 노동력과 원재료로 인해 생산비용이 낮기 때문에 E-릭샤용 배터리의 경쟁력 있는 가격을 책정할 수 있습니다. 이러한 비용 우위는 다양한 사회경제적 계층에 대한 보급을 촉진하여 많은 사람들에게 전기 릭샤가 경제적으로 실행 가능한 솔루션이 될 수 있게 합니다.

또한, 환경 인식의 증가와 지속가능한 도시 교통 솔루션에 대한 필요성이 시장을 발전시키고 있으며, 전기 릭샤는 기존의 자동 전기 릭샤를 대체할 수 있는 친환경적인 대안을 제공하고 많은 아시아태평양 국가의 환경 목표에 부합하는 것으로 나타났습니다. 그 결과, 이 지역은 당분간 세계 전기 릭샤용 배터리 시장에서 선도적인 위치를 유지할 것으로 예상됩니다.

따라서 위의 요인으로 인해 아시아태평양은 예측 기간 동안 전기 릭샤 시장을 장악할 것으로 예상됩니다.

전기 릭샤용 배터리 산업 개요

전기 릭샤용 배터리 시장은 적당히 세분화되어 있습니다. 시장 주요 기업(무순)으로는 Exide Industries Ltd, Eastman Auto & Power Ltd, Amara Raja Energy & Mobility Limited, Okaya Power Private Limited, TATA AutoComp GY. Batteries Pvt. 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의

조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

정부 정책에 의한 전기 릭샤 보급 확대

기존 화석연료 릭샤에 비해 운행·유지 비용이 낮다

성장 억제요인

충전 인프라가 보급되지 않아 접근성이 떨어진다

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협 제품·서비스

경쟁 기업 간의 경쟁 관계

제5장 시장 세분화

배터리 유형

납축배터리

리튬이온 배터리

기타 배터리

차종

승용차

트럭

지역

북미

미국

캐나다

기타 북미

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽

러시아

기타 유럽

아시아태평양

중국

인도

일본

한국

태국

말레이시아

인도네시아

베트남

기타 아시아태평양

중동 및 아프리카

사우디아라비아

아랍에미리트

남아프리카공화국

이집트

나이지리아

카타르

기타 중동 및 아프리카

남미

브라질

아르헨티나

칠레

기타 남미

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략과 SWOT 분석

기업 개요

Exide Industries Ltd

Eastman Auto & Power Ltd

Amara Raja Energy & Mobility Limited

Okaya EV Pvt. Ltd

TATA AutoComp GY Batteries Pvt. Ltd

Microtex Energy Private Limited

Sparco Batteries Pvt. Ltd

Gem Batteries Pvt. Ltd

Alsym Energy Inc.

기타 저명한 기업 리스트(회사명, 본사 소재지, 관련 제품과 서비스, 연락처 등)

시장 순위 분석

제7장 시장 기회와 향후 동향

전기 릭샤용 배터리 교환 인프라의 도입

ksm

영문 목차

영문목차

The E-Rickshaw Battery Market size is estimated at USD 2.20 billion in 2025, and is expected to reach USD 6.00 billion by 2030, at a CAGR of 22.23% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the growing adoption of e-rickshaws aided by government initiatives and the lower operational and maintenance costs compared to traditional fossil fuel-powered rickshaws are expected to drive the e-rickshaw battery market during the forecast period.

On the other hand, the lack of widespread and accessible charging infrastructure and the limited range of e-rickshaws can hinder the growth of the e-rickshaw battery market during the forecast period.

Ongoing advancements in battery technologies, such as increased energy density and the implementation of battery-swapping infrastructure for e-rickshaw, are likely to create vast opportunities for the e-rickshaw battery market.

Asia-Pacific is expected to be a dominant region in the e-rickshaw market due to the increasing adoption of battery-powered vehicles.

E-Rickshaw Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

Among different types of battery technologies, lithium-ion batteries (LIB) are expected to be among the fastest-growing e-rickshaw battery markets during the forecast period. Lithium-ion batteries are gaining more popularity than other battery types due to their favorable capacity-to-weight ratio. Other factors boosting their adoption include better performance (long and low maintenance), better shelf life, and decreasing price.

Lithium-ion (Li-ion) batteries offer various technical advantages over other technologies, such as lead-acid batteries. On average, Li-ion batteries offer cycles over 5,000 times compared to lead-acid batteries that last around 400-500 times. Li-ion batteries do not require as frequent maintenance and replacement as lead-acid batteries. Furthermore, these batteries maintain their voltage throughout the discharge cycle, allowing more significant and longer-lasting efficiency of electrical components.

In recent years, several major lithium-ion battery players have been investing to gain economies of scale and R&D activities to enhance their performance, increasing the competition and declining lithium-ion battery prices. For example, due to the improving technological innovations, manufacturing improvements, and declining raw material costs, the volume-weighted average price of lithium-ion batteries decreased considerably from USD 780/kWh in 2013 to USD 139/kWh in 2023. It is likely to reach around USD 113/kWh in 2025 and USD 80/kWh in 2030. Such declining trends in battery costs are likely to make it a lucrative choice among all batteries for the e-rickshaw battery market in the coming years.

Lithium-ion batteries have traditionally been used in consumer electronic devices like mobile phones, laptops, and others. However, in recent years, they have increasingly been redesigned for use as the power source of choice in electric vehicles (BEVs), including e-rickshaws, in various countries, owing to factors such as low environmental impact.

In December 2023, South Korea's Ministry of Finance announced plans to provide KRW 38 trillion in policy financing to the lithium battery industry over the next five years. This policy will be formally implemented in 2024. South Korea also plans to establish a KRW 1 trillion lithium battery industry promotion fund and invest KRW 73.6 billion in research and development of related technologies. At the same time, the government decided to increase the critical mineral reserves required for domestic lithium battery manufacturing and cultivate a battery reuse and recycling ecosystem. All these are anticipated to boost the lithium-ion battery industry and, in turn, support the growth of the e-rickshaw batteries market.

There has been an increasing trend in lithium-ion battery manufacturing in the Asia-Pacific region. For example, in March 2024, Panasonic Group announced it would form a joint venture with Indian Oil Corporation Ltd (IOCL) to manufacture cylindrical lithium-ion batteries. Panasonic Energy, a group firm, signed a binding term sheet and initiated discussions with IOCL to draw a framework for forming a joint venture to manufacture cylindrical lithium-ion batteries. This initiative is driven by the expected expansion of demand for batteries for two and three-wheel vehicles in the Indian market.

In May 2023, Stellantis, together with TotalEnergies and Mercedes-Benz, celebrated the inauguration of Automotive Cells Company's (ACC) battery gigafactory in Billy-Berclau Douvrin, France, the first of three planned in Europe. With an initial production line capacity of 13 gigawatt-hours (GWh), rising to 40 GWh by 2030, the facility is expected to deliver high-performance lithium-ion batteries with a minimal CO2 footprint. The gigafactory will contribute to Stellantis' goal of increasing battery manufacturing capacity to 250 GWh in Europe by 2030.

Furthermore, as per the Office of Energy Efficiency and Renewable Energy, in 2023, the government announced the development of electric vehicle battery plants in North America. The region is expected to ramp up manufacturing capacity from 55 gigawatts per year (GWh/year) in 2021 to 1000 GWh/year by 2030. Most of the projects in the pipeline are expected to initiate production between the years 2025 to 2030. This indicates a robust battery market development for automotive applications, which is expected to support the e-rickshaw battery market in the coming years.

In January 2024, Panasonic Energy announced an update on their USD 4 billion electric vehicle battery plant, still under construction, in De Soto, Kansas. According to the company, the manufacturing facility will produce 66 lithium-ion batteries per second when operating at full capacity. The 4.7 million-square-foot battery plant is still under construction on the former Sunflower Army Ammunition Plant site, and it is expected to begin production in March 2025. Such developments in lithium-ion batteries are anticipated to continue across the globe and support the e-rickshaw battery market.

Due to properties such as less weight, low charging time, a higher number of charging cycles, declining cost, and the growing progress in lithium-ion batteries, they are likely to be the fastest-growing battery type among electric vehicles, including the e-rickshaw battery market, during the forecast period.

Asia-Pacific Region is Expected to Dominate the Market

The Asia-Pacific region is anticipated to dominate the e-rickshaw battery market during the forecast period due to several compelling factors. For example, the high population density and rapid urbanization in countries such as India, China, and Bangladesh are driving the need for efficient and affordable transportation solutions, positioning e-rickshaws as a preferred option for short-distance travel. This high demand directly translates to a robust market for e-rickshaw batteries.

Various emerging countries in the region are experiencing notable government support for the adoption of e-rickshaws. In particular, countries such as India are implementing supportive regulations, subsidies, and incentives to promote the adoption of electric vehicles, including e-rickshaws, as part of broader efforts to combat pollution and reduce dependency on fossil fuels. For instance, India's Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme significantly incentivized the adoption of electric vehicles, including e-rickshaws.

In March 2024, the Ministry of Heavy Industries (MHI) in India launched the Electric Mobility Promotion Scheme (EMPS) that aims to boost the adoption of two-wheeler and three-wheeler electric vehicles for commercial purposes and provide the necessary support for developing and manufacturing EVs in India.

The EMPS-2024 is being implemented for four months, from 1 April 2024 to 31 July 2024. It has a budget of INR 500 crore and provides subsidies to EVs. Subsidies of up to INR 10,000 will be provided for each two-wheeler EV, up to INR 25,000 for each small three-wheeler EV, and up to INR 50,000 for each large three-wheeler EV. The MHI will reimburse the subsidies or demand incentives to the EV manufacturers upon the sale of a vehicle, which will also benefit the consumers as the subsidy amount will be deducted from the final invoice price, thus reducing the purchase price of the EVs. Such initiatives are anticipated to boost the country's adoption of e-rickshaws and their relevant batteries.

As per the Ministry of Road Transport and Highways in India, the annual sales of electric three-wheelers in India stood at over 581 thousand units in 2023. The data from the International Energy Agency (IEA) revealed that together, China and India accounted for 66% of the world's electric three-wheeler sales share in 2023. This highlights that these countries are likely to continue and witness vast growth during the forecast period.

Moreover, crucial battery manufacturers in the region enhance the market's growth. Companies like Exide Industries, Amara Raja Batteries, and Okaya Power offer easy access to the latest battery technologies and innovations. Besides, these players continuously invest in research and development to improve battery performance, reduce costs, and extend the lifespan of e-rickshaw batteries, making them more attractive to consumers.

The Asia-Pacific region benefits from lower production costs due to cheaper labor and raw materials, enabling competitive pricing of e-rickshaw batteries. This cost advantage helps drive widespread adoption across different socioeconomic segments, making e-rickshaws an economically viable solution for many.

Furthermore, the rising environmental awareness and the need for sustainable urban transport solutions propel the market forward. E-rickshaws offer a greener alternative to traditional auto-rickshaws, aligning with the environmental goals of many Asia-Pacific nations. As a result, the region is expected to maintain its leading position in the global e-rickshaw battery market for the foreseeable future.

Therefore, due to the abovementioned factors, the Asia-Pacific region is expected to dominate the e-rickshaw market during the forecast period.

E-Rickshaw Battery Industry Overview

The e-rickshaw battery market is moderately fragmented. Some key players in the market (not in any particular order) include Exide Industries Ltd, Eastman Auto & Power Ltd, Amara Raja Energy & Mobility Limited, Okaya Power Private Limited, and TATA AutoComp GY Batteries Pvt. Ltd.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Adoption of E-Rickshaws Aided By Government Initiatives

4.5.1.2 Lower Operational and Maintenance Costs Compared to Traditional Fossil Fuel-powered Rickshaws

4.5.2 Restraints

4.5.2.1 Lack of Widespread and Accessible Charging Infrastructure and Limited Range of E-rickshaws

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lead-acid Battery

5.1.2 Lithium-ion Battery

5.1.3 Other Batteries

5.2 Vehicle Type

5.2.1 Passenger Carrier

5.2.2 Goods Carrier

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Nordic

5.3.2.7 Russia

5.3.2.8 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Thailand

5.3.3.6 Malaysia

5.3.3.7 Indonesia

5.3.3.8 Vietnam

5.3.3.9 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 Saudi Arabia

5.3.4.2 United Arab Emirates

5.3.4.3 South Africa

5.3.4.4 Egypt

5.3.4.5 Nigeria

5.3.4.6 Qatar

5.3.4.7 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Chile

5.3.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted & SWOT Analysis for Leading Players

6.3 Company Profiles

6.3.1 Exide Industries Ltd

6.3.2 Eastman Auto & Power Ltd

6.3.3 Amara Raja Energy & Mobility Limited

6.3.4 Okaya EV Pvt. Ltd

6.3.5 TATA AutoComp GY Batteries Pvt. Ltd

6.3.6 Microtex Energy Private Limited

6.3.7 Sparco Batteries Pvt. Ltd

6.3.8 Gem Batteries Pvt. Ltd

6.3.9 Alsym Energy Inc.

6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Implementation of Battery-swapping Infrastructure for E-rickshaws