북미의 액체 수소 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

North America Liquid Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636159

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

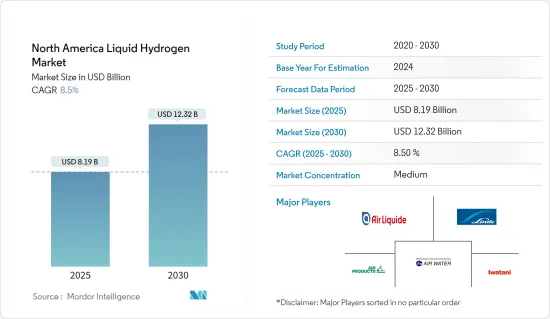

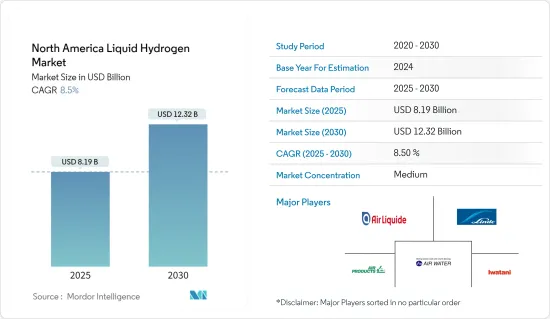

북미의 액체 수소 시장 규모는 2025년 81억 9,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 8.5%의 CAGR로 2030년에는 123억 2,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

중기적으로는 세계 에너지 산업의 탈탄소화에 대한 관심 증가, 자동차 산업 및 기타 최종사용자 산업의 성장과 확장 등의 요인이 예측 기간 동안 북미 액체 수소 시장을 견인할 것으로 예상됩니다.

한편, 액체 수소 운송에 따른 높은 비용이 액체 수소 시장 성장에 큰 걸림돌이 될 것으로 예상됩니다. 액체 수소의 대규모 저장에 따른 복잡성은 이 시장의 성장 범위를 더욱 제한할 것입니다.

해양 연료로서 액체 수소에 대한 관심이 높아지고 항공우주 산업에서 기술 혁신이 진전됨에 따라 북미 액체 수소 시장은 곧 유리한 성장 기회를 맞이할 것으로 예상됩니다.

예측 기간 동안 미국이 북미 액체 수소 시장을 독점할 것으로 예상됩니다. 이는 우주 탐사용 액체 수소에 대한 수요가 증가하고 상용차에 수소 연료전지 채택이 증가하고 있기 때문입니다.

북미의 액체 수소 시장 동향

자동차 부문이 괄목할만한 성장을 이뤄

북미 액체 수소 시장은 자동차 산업에서 청정 연료에 대한 수요가 증가함에 따라 큰 성장이 예상됩니다. 액체 수소는 저장과 운송에 있어 우수한 장점을 가지고 있어 더 큰 이점을 가지고 있습니다.

자동차 응용 분야에서는 고체 고분자 연료전지와 같은 신기술을 사용하여 CO2를 배출하지 않고 액체 수소를 2차 에너지원으로 사용할 수 있습니다.

2022년에는 미국이 북미에서 가장 많은 수소 충전소를 보유하게 될 것입니다. 미국에는 약 54개의 수소 충전소가 운영되고 있으며, 캐나다(9개소)가 그 뒤를 잇고 있습니다. 또한, 미국의 수소경제 로드맵에 따르면, 2030년까지 미국 내 4,300개의 대형 수소 충전소가 건설될 예정입니다. 이는 2019년 현재 운영 중인 대형 수소 충전소 수의 70배에 육박하는 수치입니다.

또한, 미국 연료전지 및 수소에너지협회(FCHEA)에 따르면, 2030년까지 미국에는 4,300개의 대형 수소 충전소가 설치될 것으로 예상됩니다. 그러나 2050년에는 수송용 연료가 미국 수소 수요의 최대 비중을 차지할 것으로 예상됩니다. 화석연료로 구동되는 자동차의 오염은 환경에 직접적으로 배출되어 건강상의 위험을 초래합니다.

예를 들어, Air Liquide는 지난 5월 라스베이거스에 새로운 액체 수소 제조 시설과 물류 센터를 개설하여 모빌리티 부문에서 액체 수소에 대한 새로운 수요를 포착하는 것을 목표로 하고 있습니다. 수소는 전기자동차와 같이 충전을 위한 다운타임이 필요하지 않기 때문에 해운 및 물류 부문에서 연료로 인기를 끌고 있습니다. 새로운 플랜트에서는 천연가스에서 수소를 추출하는 수증기 메탄 개질을 통해 4만 대의 자동차를 연료로 사용할 수 있는 수소를 생산할 수 있습니다. 이러한 프로젝트는 자동차 부문에서 액체 수소에 대한 적극적인 수요를 창출할 가능성이 높습니다.

따라서, 위의 요인에 따라 자동차 부문은 예측 기간 동안 북미 액체 수소 시장에서 큰 수요를 보일 것으로 예상됩니다.

시장을 독점하고 있는 미국

북미의 석유 및 가스 다운스트림 부문의 성장은 예측 기간 동안 수소 수요에 긍정적인 영향을 미칠 것으로 예상되며, 2023년 8월 기준 미국 정유소의 수소 순 공급 능력은 709만 9,000배럴에 달합니다.

미국에서는 셰일 혁명으로 인해 멕시코만 연안을 중심으로 석유 정제 능력이 전례 없이 확대되었습니다. 그 결과, 석유 및 가스 부문에서는 프로젝트 수와 투자 금액이 꾸준히 증가하고 있습니다. 수소는 수력 탈황이라고 불리는 화학적 분리 공정에서 생산된 연료에서 황을 제거하는 데 사용됩니다.

미국 에너지정보청(EIA)은 2021년 정유 부문 수소 순투입량을 8,091만 9,000배럴로 보고했으며, 2021년 대비 5.2%의 성장률을 기록할 것으로 예상했습니다. 수소는 또한 암모니아 및 메탄올 생산, 화학제품 및 산업용 열 공급에도 널리 사용되고 있습니다.

미국은 우주개발 계획에서 시작하여 수송, 고정식 전력, 휴대용 전력 응용 분야에서 상용화를 가능하게 하는 기술에 이르기까지 수소 및 관련 기술 연구 개발의 최전선에 서 있습니다. 수년 동안 미국 에너지부(DOE)는 Spark M. Matsunaga Hydrogen Research, Development, and the Energy Policy Act of 2005(EPACT)를 포함한 여러 법적 권한에 따라 수소 및 관련 기술에 대한 강력한 연구개발 활동을 구축해 왔습니다. 수소 및 관련 기술에 대한 강력한 연구개발 활동을 확립해 왔습니다.

Air Products는 2022년 10월, 약 5억 달러를 투자하여 뉴욕주 마세나의 그린필드에 35톤 규모의 친환경 액체 수소 생산시설과 액체 수소 유통 및 판매 사업을 건설, 소유, 운영할 계획입니다. 이 시설의 상업적 운영은 2026-2027년에 시작될 예정입니다.

2024년 1월, Plug Power는 10억 달러 이상의 정부 자금을 확보했습니다. 조지아 주 공장에서 액체 그린 수소 생산을 시작했습니다. 이러한 신흥국 시장 개척은 예측 기간 동안 북미 액체 수소 시장에 긍정적인 영향을 미칠 것으로 보입니다.

따라서 위의 요인으로 인해 예측 기간 동안 미국이 북미 액체 수소 시장을 독점할 것으로 예상됩니다.

북미의 액체 수소 산업 개요

북미의 액체 수소 시장은 반독점 시장입니다. 주요 기업으로는 Air Liquide S.A., Linde plc, Air Products and Chemicals Inc, Air Water Inc, Iwatani Corporation 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의

조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

세계 에너지 탈탄소화에 대한 주목 상승

자동차 산업 확대

성장 억제요인

액체 수소 운송에 따른 고비용

공급망 분석

Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 기업 간의 경쟁 관계

제5장 시장 세분화

유통

용기

탱크

최종사용자

자동차

화학·석유화학

항공우주

기타

지역

미국

캐나다

기타 북미

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략

기업 개요

Air Liquide S.A.

Air Products and Chemicals, Inc.

AIR WATER INC

Iwatani Corporation

Linde plc

Universal Industrial Gases, Inc.

Messer Group GmbH

Engie SA

Market Player Ranking

제7장 시장 기회와 향후 동향

해양 연료로서의 액체 수소에 대한 주목 상승과 항공우주 산업의 기술 혁신 증가

ksm

영문 목차

영문목차

The North America Liquid Hydrogen Market size is estimated at USD 8.19 billion in 2025, and is expected to reach USD 12.32 billion by 2030, at a CAGR of 8.5% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as increasing focus on the decarbonization of the global energy industry along with growth and expansion of the automobile industry and other end-user verticals are expected to drive the North America liquid hydrogen market during the forecast period.

On the other hand, high costs associated with the transportation of liquid hydrogen is expected to pose a major challenge to the growth of the liquid hydrogen market. Complexities involved in storing liquid hydrogen on a large scale will further restrict the scope of growth for this market.

Nevertheless, rising emphasis on liquid hydrogen as a marine fuel and increasing innovations in the aerospace industry is expected to create lucrative growth opportunities for the liquid hydrogen market in North America soon.

United States is expected to dominate the North America liquid hydrogen market during the forecast period. Owing to the growing demand for liquid hydrogen for space exploration and the increasing adoption of hydrogen fuel cells in commercial vehicles.

North America Liquid Hydrogen Market Trends

Automotive Segment to Witness Significant Growth

North America's liquid hydrogen market is expected to grow significantly due to the rising demand for clean fuel in the automotive industry. Liquid hydrogen offers more significant advantages because of its storage and transportation qualities.

In an automotive application, liquid hydrogen can be used as a secondary energy source without emitting any CO2 using new technologies like Proton Exchange Membrane fuel cells to produce electricity for an electric drive and a direct fuel for ICE (internal combustion engines).

In 2022, United States has the most significant number of hydrogen fueling stations in the North American region. There are about 54 operational hydrogen refueling stations in the country, followed by Canada (9 stations). Furthermore, as per the road map to a US hydrogen economy, 4,300 large hydrogen fueling stations in the United States were expected by 2030. This would be close to 70 times the number of operational large fueling stations in 2019.

Moreover, according to United States Fuel Cell & Hydrogen Energy Association (FCHEA), by the year 2030, the country is expected to have 4,300 large hydrogen fueling stations. However, by 2050, transportation fuels are expected to account for the greatest volume of United States hydrogen demand becuase pollution all around the globe is increasing from vehicles and transportation over time. Pollution from fossil fuel-powered vehicles is emitted directly into the environment, which causes health risks.

For instance, in May 2022, Air Liquide opened a new liquid hydrogen production facility and logistics center in Las Vegas last week, aiming to capitalize on emerging demand for liquid hydrogen as a fuel in the mobility sector. Hydrogen is gaining traction as a fuel within the shipping and logistics arena because it does not require downtime for charging like electric-powered vehicles. The new plant is capable of producing enough hydrogen to fuel 40,000 vehicles, using steam methane reforming, which derives hydrogen from natural gas. Such projects are likely to create positive demand for liquid hydrogen in automotive segment.

Therefore, based on the above-mentioned factors, automotive segment is expected to witness significant demand in the North America liquid hydrogen market during the forecast period.

United States to Dominate the Market

The growth of the oil and gas downstream sector in the North American region is expected to impact the demand for hydrogen during the forecast period positively. As of August 2023, the United States refinery net input of hydrogen capacity stands at 7,099 thousand barrels.

The shale revolution in the United States has resulted in an unprecedented oil refining capacity creation and expansion, primarily along the Gulf Coast. As a result, steady growth in the number of projects and investments has been witnessed in the oil and gas sector. Hydrogen is used to remove the sulfur content from the fuels produced in a chemical separation process called hydro-desulphurization.

Also, the United States Energy Information Administration (EIA) reported the net input of hydrogen in oil refining as 80,919 thousand barrels, recording a growth of 5.2% as compared to 2021 levels. Hydrogen is also used extensively in the generation of ammonia and methanol and in providing industrial heat for chemicals and industrial applications.

The United States has been at the forefront of hydrogen and related technology R&D, from its inception in the space program to enabling technology commercialization in transportation, stationary power, and portable-power applications. Over the years, the Department of Energy (DOE) has established robust R&D activities on hydrogen and related technology aligned with several statutory authorities, including the Spark M. Matsunaga Hydrogen Research, Development, and the Energy Policy Act of 2005 (EPACT).

Air Products, in October 2022, planned to invest about USD 500 million to build, own and operate a 35 tonne/day facility to produce green (renewable) liquid hydrogen at a greenfield site in Massena, New York, as well as liquid hydrogen distribution and dispensing operations. Commercial operation of this facility is expected to commence in 2026-2027.

In January 2024, Plug Power secured over USD one billion in government funding. It commenced producing liquid green hydrogen at its Georgia plant. Such developments are likely to create positive impact on the North America liquid hydrogen market during the forecast period.

Therefore, based on the above-mentioned factors, United States is expected to dominate the liquid hydrogen market in North America during the forecast period.

North America Liquid Hydrogen Industry Overview

The North America liquid hydrogen market is semi consolidated in nature. Some of the major players in the market (in no particular order) include Air Liquide S.A., Linde plc, Air Products and Chemicals Inc., Air Water Inc., and Iwatani Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Focus on the Decarbonization of Global Energy

4.5.1.2 Expansion of Automobile Industry

4.5.2 Restraints

4.5.2.1 High Costs Associated with Transportation of Liquid Hydrogen

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Distribution

5.1.1 Containers

5.1.2 Tanks

5.2 End-User

5.2.1 Automotive

5.2.2 Chemicals and Petrochemicals

5.2.3 Aerospace

5.2.4 Other End-Users

5.3 Geography

5.3.1 United States

5.3.2 Canada

5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Air Liquide S.A.

6.3.2 Air Products and Chemicals, Inc.

6.3.3 AIR WATER INC

6.3.4 Iwatani Corporation

6.3.5 Linde plc

6.3.6 Universal Industrial Gases, Inc.

6.3.7 Messer Group GmbH

6.3.8 Engie SA

6.4 Market Player Ranking

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Rising Emphasis on Liquid Hydrogen as a Marine Fuel and Increasing Innovations in the Aerospace Industry