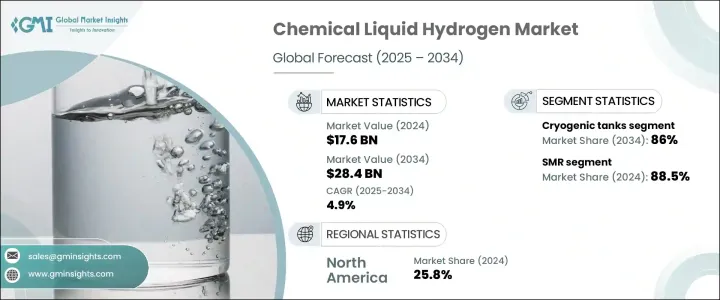

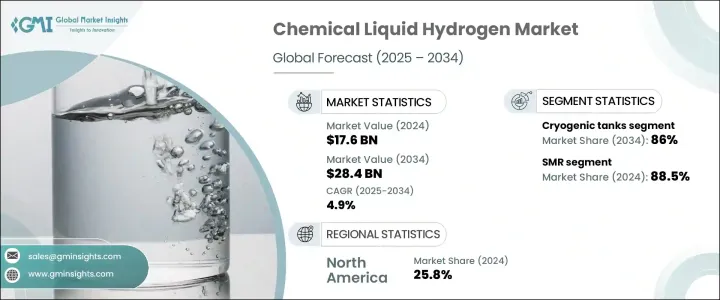

세계의 화학 액체 수소 시장 규모는 2024년 176억 달러로 평가되었고, 화학 제조자가 세계 기후 변화 목표에 맞추어 저배출 가스 원료를 추구하는 가운데 CAGR 4.9%로 성장할 전망이며, 2034년에는 284억 달러에 달할 것으로 예측되고 있습니다.

세계 산업계가 탈탄소 전략에 적극적으로 참여하고 있기 때문에 화학 액체 수소 수요는 가속화되고 있습니다. 정부나 민간 기업은, 넷 제로 목표 달성의 긴급성으로부터, 수소 인프라 대한 고액의 투자를 실시하고 있습니다. 시장은 신재생 에너지 비용의 저하와 기술적 돌파에 힘입어 그린 수소 제조로의 전환을 목격하고 있습니다. 정책 지원, 투자자 신뢰 제고, 전략적 민관 파트너십으로 수소 개발을 위한 활기찬 생태계가 형성되고 있습니다. 전해조의 진보, 탄소 회수 기술, 확장 가능한 액화 시스템에 대한 자금 제공의 증가는 화학 액체 수소를 보다 상업적으로 실현 가능하고 환경적으로 지속 가능한 것으로 만들고 있습니다. 화학, 중공업, 운수 등의 산업 부문이 청정 에너지에 대한 대처를 강화함에 따라 이용하기 쉽고 유연성이 있는 수소 솔루션의 필요성이 더욱 높아지고 있습니다. 이 기세는 앞으로 10년에 걸친 시장의 힘찬 성장의 무대를 갖추어 가고 있습니다.

그린 수소로의 변화가 증가함에 따라 산업 분야에서의 채택을 촉진하고 있습니다. 신재생 에너지, 특히 태양광 발전과 풍력 발전의 비용 절감으로 전해 수소의 상업적 실현성이 높아지고 있습니다. 동시에 전해조 기술과 탄소 회수 시스템의 발전으로 제조 공정의 효율성과 지속가능성이 향상되었습니다. 이러한 혁신으로 산업계는 보다 신속하게 탈탄소화되고 규제 기대에 부응할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 176억 달러 |

| 예측 금액 | 284억 달러 |

| CAGR | 4.9% |

유연한 인프라와 가격 설정 모델의 도입이 진행됨에 따라 수소는 산업용 사용자에게 보다 이용하기 쉬워지고 있습니다. 투명성이 높은 스팟 가격은 장기적인 헌신을 필요로 하지 않는 주문형 공급을 선호하는 구매자에게 새로운 기회를 만들어 분야를 넘어 광범위한 참여를 장려합니다. 이 진전은 투자자의 신뢰를 높이고 클린 수소 이니셔티브에 대한 자금 조달을 가속화합니다. 관민 파트너십은 특히 액체 수소의 저장과 운송을 위한 인프라 정비를 추진하는 데 있어 계속 도움이 되고 있습니다.

수소 유통을 위한 대규모 암모니아 변환 및 액화 시스템의 상업화에 대한 대처가 견인력을 늘리고 있습니다. 이러한 개발은, 장거리 수송의 경제성을 향상시켜, 세계의 수요 증가에 대응하는 것에 일조하고 있습니다. 그러나 수소 관련 기기의 수입 관세를 인상하는 국제 무역 정책이 진행되고 있기 때문에 미래 제조 비용이 상승하고 세계 공급망에 마찰이 발생할 수 있습니다. 또 특히 청정 에너지 인프라가 아직 출범하지 않은 몇몇 지역에서는 기술 혁신이 제한돼 시장 확대가 지연될 수 있습니다.

석탄가스화 분야는 2024년에 11억 달러를 창출했으며, 2034년까지 더욱 성장할 전망입니다. 그 매력은 풍부하게 매장된 석탄을 수소로 변환하고 에너지 다양화 전략을 지원하는 데 있습니다. 에너지 안보가 중시되면서 기존 연료 수입 의존도가 떨어지는 가운데 이 방법에 대한 관심은 여전히 높습니다. 석탄 기반의 수소 제조에 탄소 회수를 포함시킴으로써 프로세스가 보다 깨끗해지고 완전히 재생 가능한 대체 에너지로의 이행의 가교가 됩니다.

유통면에서 파이프라인과 극저온 탱크가 여전히 2대 수송 방법이며, 각각이 이용 사례나 지리적 요구에 근거한 명확한 이점을 제공합니다. 극저온 탱크는 2024년 86%의 점유율을 차지했으며, 화학 생산 환경에서 대량의 액체 수소의 저장과 이동을 가능하게 하는 중요한 역할을 담당하고 있는 것으로 나타났습니다. 이 탱크들은 극저온에 견디도록 설계되어 수소를 액화한 상태로 저장하여 저장 및 수송 중 에너지 손실을 최소화합니다. 이 탱크의 우위성은 진공 단열재와 다층 복합 재료의 기술 혁신에 의해 더욱 뒷받침되고 있으며, 보일 오프율을 대폭 저감하고 전체적인 안전성을 향상시키고 있습니다.

미국의 화학 액체 수소 2024년 시장 규모는 41억 달러로 평가되었고, 관민의 대규모 투자에 지지된 청정 에너지에 대한 적극적인 국가적 뒷받침이 그 원동력이 되고 있습니다. 연방정부의 인센티브, 조성금, 정책 틀에 의해 주요 산업지역 전체에서 수소 제조 및 저장 시설의 급속한 개발이 가능해졌습니다. 화학, 중공업, 운수 등 분야로부터의 관심 고조가, 견고한 수소 공급망의 필요성을 뒷받침하고 있습니다.

Ballard Power Systems, TotalEnergies, Chart Industries, Messer Group, Linde, Plug Power, ENGIE, Air Products and Chemicals, Iwatani Corporation, ENEOS Corporation, Taiyo Nippon Sanso Corporation, Air Liquide, and Nel ASA 등의 기업은 시장 점유율을 확보하기 위해 여러 전략에 주력하고 있습니다. 주된 대처에는, 고효율 제조 기술에의 투자, 에너지·화학 기업과의 전략적 제휴, 모듈식으로 확장성이 높은 수소 플랜트의 건설등이 있습니다. 이들 기업은 공급 감시를 위한 디지털 통합을 우선시하고, 지역의 청정 에너지 정책에 맞추면서 신뢰성 높은 유통을 확보하기 위한 인프라에 투자하고 있습니다.

The Global Chemical Liquid Hydrogen Market was valued at USD 17.6 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 28.4 billion by 2034 as chemical producers pursue low-emission feedstocks to align with global climate targets. Demand for chemical liquid hydrogen is accelerating as industries worldwide move aggressively toward decarbonization strategies. Governments and private players are investing heavily in hydrogen infrastructure, driven by the urgency to meet net-zero goals. The market is witnessing a shift toward green hydrogen production, fueled by lower renewable energy costs and technological breakthroughs. Policy support, growing investor confidence, and strategic public-private partnerships are creating a vibrant ecosystem for hydrogen development. Increasing funding in electrolyzer advancements, carbon capture technologies, and scalable liquefaction systems is making chemical liquid hydrogen more commercially feasible and environmentally sustainable. As industrial sectors such as chemicals, heavy industries, and transportation sectors ramp up their clean energy commitments, the need for accessible and flexible hydrogen solutions is becoming even more critical. This momentum is setting the stage for robust market growth through the next decade.

A growing shift toward green hydrogen is driving adoption across industrial applications. Cost reductions in renewable energy, particularly solar and wind, are making electrolytic hydrogen more commercially viable. Simultaneously, advancements in electrolyzer technology and carbon capture systems are improving the efficiency and sustainability of production processes. These innovations are allowing industries to decarbonize more rapidly and meet regulatory expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.6 Billion |

| Forecast Value | $28.4 Billion |

| CAGR | 4.9% |

The increased deployment of flexible infrastructure and pricing models makes hydrogen more accessible to industrial users. Transparent spot pricing creates new opportunities for buyers who prefer on-demand supply without long-term commitments, encouraging broader participation across sectors. This progress boosts investor confidence, accelerating funding for clean hydrogen initiatives. Public-private partnerships continue to help in advancing infrastructure, particularly for liquid hydrogen storage and transportation.

Efforts to commercialize large-scale ammonia conversion and liquefaction systems for hydrogen distribution are gaining traction. These developments are improving the economic viability of long-distance transport, helping meet rising global demand. However, ongoing international trade policies that raise import tariffs on hydrogen-related equipment may inflate future production costs, creating friction in global supply chains. This may also restrict innovation and slow market expansion in several regions, particularly where clean energy infrastructure is still emerging.

The coal gasification segment generated USD 1.1 billion in 2024 and is poised to grow further by 2034. Its appeal lies in converting abundant coal reserves into hydrogen, supporting energy diversification strategies. As more emphasis is placed on energy security and reducing reliance on traditional fuel imports, interest in this method remains strong. Integrating carbon capture into coal-based hydrogen production makes the process cleaner, helping bridge the transition to fully renewable alternatives.

In terms of distribution, pipelines and cryogenic tanks remain the two primary methods for transporting chemical liquid hydrogen, each offering distinct advantages based on use cases and geographic needs. Cryogenic tanks held an 86% share in 2024, underscoring their critical role in enabling the storage and movement of large volumes of liquid hydrogen within chemical production environments. These tanks are engineered to withstand extreme cold temperatures, preserving hydrogen in its liquefied state and minimizing energy losses during storage and transport. Their dominance is further supported by innovations in vacuum insulation and multilayer composite materials, which significantly reduce boil-off rates and improve overall safety.

U.S. Chemical Liquid Hydrogen Market generated USD 4.1 billion in 2024, fueled by an aggressive national push toward clean energy, backed by significant public and private sector investments. Federal incentives, grants, and policy frameworks have enabled the rapid development of hydrogen production and storage facilities across key industrial regions. Increased interest from sectors such as chemicals, heavy industry, and transportation is driving the need for robust hydrogen supply chains.

Companies like Ballard Power Systems, TotalEnergies, Chart Industries, Messer Group, Linde, Plug Power, ENGIE, Air Products and Chemicals, Iwatani Corporation, ENEOS Corporation, Taiyo Nippon Sanso Corporation, Air Liquide, and Nel ASA are focusing on multiple strategies to secure market share. Key initiatives include investing in high-efficiency production technologies, forming strategic alliances with energy and chemical firms, and building modular, scalable hydrogen plants. These players prioritize digital integration for supply monitoring and investing in infrastructure to ensure reliable distribution while aligning with regional clean energy policies.