ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

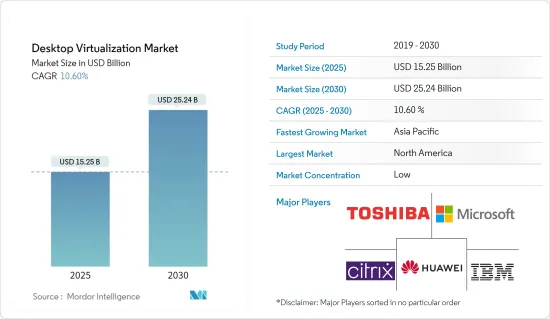

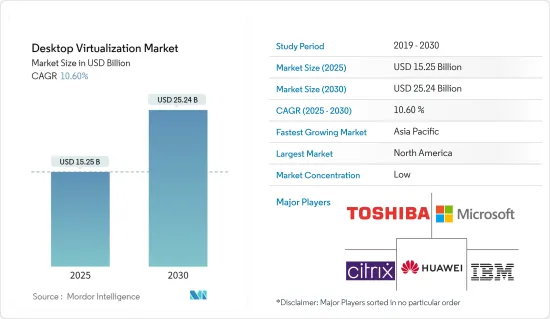

데스크톱 가상화 시장 규모는 2025년에 152억 5,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 10.6%의 연평균 성장률(CAGR)로 2030년에는 252억 4,000만 달러에 달할 것으로 예상됩니다.

데스크톱 가상화는 비용 절감과 완벽하게 동기화되어 있습니다. 따라서 비용 효율성이 시장 성장의 주요 촉진제가 될 것으로 예상됩니다.

주요 하이라이트

데스크톱 가상화는 하드웨어 지출을 줄이고 시스템 관리 및 유지보수 비용을 절감하기 때문에 중소기업에 가치가 있습니다. 우수한 컴퓨팅 경험을 제공하고 몇 가지 복잡한 문제를 해결합니다. 결과적으로 데스크톱 가상화는 운영 비용 절감 및 사용자 만족도 향상과 같은 몇 가지 이점을 제공하여 예측 기간 동안 데스크톱 가상화 시장의 성장을 촉진할 것으로 예상됩니다.

클라우드 컴퓨팅의 도입 확대와 직장에서의 BYOD 수요 증가는 이 시장을 주도하는 중요한 요인입니다. 데스크톱 가상화를 도입함으로써 고용주는 BYOD를 활용하여 원격 근무자와 사무실에 근무하는 직원 모두에게 유연성과 보안을 강화할 수 있습니다. 데스크톱 가상화를 사용하는 직원은 거의 모든 기기에서 거의 모든 위치에서 안전하게 모니터링되는 데스크톱에 액세스할 수 있습니다.

복잡성을 줄이고 다양한 모바일 사용자에게 앱을 제공할 수 있기 때문에 모든 유형의 기업에서 데스크톱 가상화를 도입하고 있습니다. 관리 및 스토리지의 발전으로 인해 보다 현실적인 선택이 되어 전 세계 시장의 보급을 촉진하고 있습니다.

인프라의 제약이 시장 성장을 저해하고 있습니다. 데스크톱 가상화는 Windows 데스크톱과 애플리케이션 제공의 복잡성을 증가시킵니다. 가상 데스크톱이 의도한 대로 작동하려면 여러 계층의 기술이 조화롭게 작동해야 합니다. 새로운 인프라의 필요성과 그에 따른 비용은 데스크톱 가상화 시장의 성장에 큰 제약 요인 중 하나입니다.

COVID-19 이후 많은 기업들이 원격 근무에 눈을 돌리면서 이 시장에 많은 관심이 집중되고 있습니다. 봉쇄 및 사회적 거리두기 지침으로 인해 많은 기업들이 즉시 필요한 조정을 수행하고 원격 근무자를 지원하는 데 필요한 컴퓨터 인프라를 구축해야 했습니다. 기업들은 오랫동안 데스크톱 가상화 솔루션을 사용해 왔습니다.

데스크톱 가상화 시장 동향

클라우드 도입 모드가 큰 성장을 이룰 것으로 전망

다양한 기업들이 클라우드 컴퓨팅을 통해 기업 운영 비용을 절감하고 있습니다. 클라우드 호스팅의 손쉬운 도입, 접근성, 유연성이 기업들의 클라우드 컴퓨팅 도입을 촉진할 것으로 예상됩니다. 클라우드 도입에는 DaaS(Desktop-as-a-Service), Workspace-as-a-Service(Workspace-as-a-Service), SaaS(Application/Software-as-a-Service) 등의 서비스 모델이 있습니다. 데스크톱 가상화는 클라우드 네트워크에서 서비스로 제공되며, 모든 컴퓨팅 및 지원 인프라는 클라우드 전개 방식에서 서비스 제공업체 측에서 호스팅됩니다.

클라우드를 통한 애플리케이션 스트리밍은 업계에서 인기를 얻고 있으며, 많은 기업들이 독립형 애플리케이션 서비스를 선택하고 있습니다. 클라우드는 확장성, 데이터 관리, 비용 절감 등의 이점으로 인해 모든 산업에서 선호되고 있습니다. 플렉셀라 소프트웨어에 따르면, 2023년에는 응답자의 47%가 이미 아마존 웹 서비스(AWS)에서 중요한 워크로드를 실행하고 있는 것으로 나타났습니다.

기업은 실제 PC를 구매하지 않고도 직원을 위해 새로운 데스크톱을 쉽게 만들 수 있습니다. 이러한 리소스가 더 이상 필요하지 않으면 전원을 끌 수 있으며, 그 시점에서 고객은 더 이상 비용을 청구하지 않습니다. 다양한 가격 책정 모델이 있지만, 소비 기반 가격 책정은 클라우드 데스크톱만의 장점입니다.

클라우드를 도입하면 작업 환경 간 데이터 마이그레이션이 용이해집니다. 또한, 기업은 물리적 설치 없이도 요구 사항을 확장하여 컴퓨팅 파워와 데이터를 추가적으로 조달할 수 있습니다. 이러한 DaaS의 유연성은 더 나은 리소스 관리를 가능하게 합니다.

2023년 6월, Cloud Software Group은 Midis Group과의 제휴를 발표하고 동유럽, 중동 및 아프리카의 채널과 소비자에게 서비스를 제공하기 위한 협력을 시작했습니다. 이번 제휴를 통해 클라우드 소프트웨어 그룹은 소비자들이 혁신적 기술 협업을 통해 변화를 가져올 수 있도록 지원하는 데 필요한 현지 리소스와 해당 지역에서의 입지를 확장하는 데 필요한 규모를 제공할 예정입니다.

서비스 제공자 측에서 호스팅되는 서버와 장비는 시스템 유지보수 및 운영에 필요한 기술 인력 및 IT 리소스를 필요로 하지 않습니다. 클라우드에 배포된 데스크톱 가상화 솔루션은 유틸리티와 애플리케이션이 자동으로 업데이트됩니다. 사용자는 업데이트를 '푸시'할 필요가 없습니다. 사용자는 거의 모든 디바이스에서 가상 데스크톱과 프로그램에 액세스할 수 있기 때문에 PC, Mac, Linux, iOS, Android 등 어떤 디바이스를 선택하든 동일한 애플리케이션을 사용할 수 있으며, 필요할 때 언제든지 편리하게 사용할 수 있습니다.

북미가 가장 큰 시장 점유율을 차지할 것으로 예상

북미는 많은 산업 분야에서 세계 허브로 여겨지고 있으며, 그 결과 데스크톱 가상화의 가장 큰 지역 시장으로 자리매김하고 있습니다. 미국은 북미에서 데스크톱 가상화를 가장 많이 사용하는 국가입니다. 미국에는 여러 클라우드 서비스 제공업체가 존재하며, 호스팅 서버의 수가 증가함에 따라 북미 시장의 성장에 기여하고 있습니다.

미국 내 주요 기업의 존재로 인해 선진국에 가까운 캐나다에서도 새로운 작업공간이 설치되고, 환경 친화적이고 에너지 절약적인 방법의 도입이 강조되고 있어 이 지역 전체 시장의 성장을 촉진하고 있습니다.

이 지역의 조직들이 새로운 기술을 빠르게 채택한 것이 세계 우위의 주요 원동력이 되고 있습니다. 이 지역의 클라우드 기반 데스크톱 가상화 구축 성장에는 주요 클라우드 서비스 제공업체들이 큰 역할을 하고 있습니다.

북미 IT 및 통신 산업은 다른 지역 시장 중 가장 큰 규모를 자랑합니다. 은행, 의료, 정부 기관과 같은 산업은 기밀 정보의 대규모 데이터베이스를 다루고 있습니다. 데스크톱 가상화는 지적 재산의 무결성을 유지하면서 사용자에게 유연성을 제공하기 때문에 이들 기업들은 데스크톱 가상화 도입에 큰 기대를 걸고 있습니다.

데스크톱 가상화 업계 개요

데스크톱 가상화 시장은 Citrix Systems Inc, IBM Corporation, Huawei Technologies, Microsoft Corporation, Toshiba Corporation 등 주요 업체들이 존재하며 매우 세분화되어 있습니다. 매우 세분화되어 있습니다. 시장 진입 기업들은 제품 라인업을 강화하고 지속가능한 경쟁 우위를 확보하기 위해 제휴 및 인수 등의 전략을 채택하고 있습니다.

2023년 11월 - Microsft는 새로운 최신 Azure Virtual Desktop 웹 클라이언트 사용자 인터페이스를 일반에 공개한다고 발표했습니다. 이 업데이트를 통해 사용자는 웹 클라이언트 설정을 기본값으로 재설정하고, 라이트 모드와 다크 모드를 전환하고, 리소스를 그리드 또는 목록 형식으로 표시할 수 있습니다.

2023년 7월 - 시트릭스는 고객 인게이지먼트 소프트웨어 분야의 세계 리더인 Twilio와 파트너십을 체결했습니다. 이번 제휴는 Citrix DaaS와 Twilio Flex 환경을 위한 통합된 고성능 솔루션을 제공하기 위한 것입니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

구매자/소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 기업 간의 경쟁 강도

COVID-19가 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

Bring Your Own Device에 대한 수요 증가

클라우드 컴퓨팅 채용 확대

시장 성장 억제요인

인프라 제약

제6장 시장 세분화

데스크톱 제공별

호스트형 가상 데스크톱(HVD)

호스트형 공유 데스크톱(HSD)

기타 데스크톱 제공

전개별

온프레미스

클라우드

최종 이용 업계별

금융 서비스

헬스케어

제조업

IT·통신

기타 업계별

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 개요

Citrix Systems Inc.

IBM Corporation

Huawei Technologies Co. Ltd

Microsoft Corporation

Toshiba Corporation

DELL Technologies Inc.

Parallels International GmbH

Red Hat Inc.

NComputing Co. Ltd.

Ericom Software Inc.

제8장 투자 분석

제9장 시장 기회와 향후 동향

ksm

영문 목차

영문목차

The Desktop Virtualization Market size is estimated at USD 15.25 billion in 2025, and is expected to reach USD 25.24 billion by 2030, at a CAGR of 10.6% during the forecast period (2025-2030).

Desktop Virtualization is completely in sync with cost reduction. Hence, cost-effectiveness is expected to be a key driving factor for the growth of the market.

Key Highlights

Desktop virtualization is valuable for small and medium businesses, as it lowers expenditure on hardware and reduces system administration and maintenance costs. It provides a superior computing experience and solves several complex problems. As a result, desktop virtualization has several benefits, such as a reduction of operational costs and increased user satisfaction, which is expected to fuel the growth of the desktop virtualization market during the forecast period.

The growing adoption of cloud computing and increasing demand for BYOD in the workplace are significant factors driving this market. By implementing desktop virtualization, employers can leverage BYOD to boost the flexibility and security of both a remote workforce and those working in the office. Employees that use desktop virtualization have access to a secure, monitored desktop from almost any location and on any device.

The ability to lower complexity and deliver apps to various mobile users is boosting the adoption of desktop virtualization in all types of businesses. The advancements in management and storage make it a more viable option, which is driving the adoption of the market worldwide.

Infrastructural constraints are hindering the growth of the market. Desktop virtualization increases the complexity of delivering Windows desktops and applications. For virtual desktops to perform as intended, several layers of technology have to work in harmony. The need for new infrastructure, along with the costs associated with it, is one of the major constraints for the growth of the desktop virtualization market.

The market has been brought to focus since COVID-19 because many businesses have turned to remote working. The lockdown and social distancing guidelines forced many businesses to make the necessary adjustments immediately and build the computer infrastructure needed to support their remote workers. Businesses have been using desktop virtualization solutions for a long time.

Desktop Virtualization Market Trends

Cloud Deployment Mode is Expected to Witness Significant Growth

Various organizations are using cloud computing to reduce businesses' operational costs. Easy implementation, accessibility, and flexibility of cloud hosting are expected to drive organizations' adoption of cloud computing. Cloud deployment includes service models, such as Desktop-as-a-Service (DaaS), Workspace-as-a-Service (WaaS), and Application/Software-as-a-Service (SaaS). Desktop virtualization is offered as a service over cloud networks, with all computing and supporting infrastructure hosted on the service provider's end in the cloud deployment mode, which makes the migration of data between working environments easy.

Application streaming over the cloud is gaining popularity in the industry, with many businesses choosing standalone application services. Cloud is preferred across industries, providing better scalability, data management, and cost savings. According to Flexera Software, in 2023, 47 percent of respondents are already running significant workloads on Amazon Web Services (AWS).

Businesses can easily create new desktops for their workforce without needing to purchase physical PCs. When these resources are no longer needed, they can be turned off, at which point the customer is no longer billed. Although there are various pricing models, consumption-based pricing is a unique benefit of cloud desktops.

Cloud deployment makes the migration of data between working environments easy. Also, companies have the option to scale up their requirements and procure additional computing power and data without the need for physical installation. This flexibility of DaaS enables better resource management.

In June 2023, Cloud Software Group announced a partnership with Midis Group, in its collaboration to serve its channel and consumers in Eastern Europe, the Middle East, and Africa. The collaboration offers Cloud Software Group the local resources consumers need to help their transformative technology collaboration and the scale required to expand its presence in these regions.

With servers and equipment hosted on the service provider's side, the need for technical staff and IT resources to maintain and operate systems is eliminated. In cloud-deployed desktop virtualization solutions, utilities and applications are updated automatically. Users do not need to be "pushed" for updates. The fact that users may access their virtual desktop or programs using almost any device means that regardless of whether they prefer PC, Mac, Linux, iOS, or Android, they will see the same applications that work in the same way and have them conveniently available whenever they need them.

North America is Expected to Hold the Largest Market Share

The North American region is considered to be the global hub for many industry verticals, and as a result, it is the largest regional market for desktop virtualization. The United States is the largest consumer of desktop virtualization in North America. The presence of several cloud service providers and an increasing number of hosted servers in the United States have contributed to the growth of the market in North America.

The presence of major companies in the United States has led to the setting up of new workspaces in Canada due to the proximity of its developed counterpart and emphasis on installing eco-friendly and energy-saving practices, thus bolstering the growth of the market across the region.

The early adoption of new technologies by organizations in the region is the primary driving force behind global dominance. Large cloud service providers play a significant role in the growth of cloud-based desktop virtualization deployment in the region.

The North American IT and telecommunications industry is the largest among other regional markets. Industries, such as banking, healthcare, and government organizations, handle large databases of sensitive information. They are looking forward to using desktop virtualization deployments, as they preserve the integrity of the intellectual property and simultaneously provide flexibility to users.

Desktop Virtualization Industry Overview

The Desktop Virtualization market is highly fragmented with the presence of major players like Citrix Systems Inc., IBM Corporation, Huawei Technologies Co. Ltd, Microsoft Corporation, and Toshiba Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

November 2023 - Microsft has announced the General Availability of the latest new Azure Virtual Desktop Web Client User Interface. With this update, Users can Reset web client settings to their defaults, Switch between Light and Dark Mode, and View their resources in a grid or list format.

July 2023 - Citrix has partnered with Twilio, one of the global leaders in customer engagement software. This partnership represents the commitment to provide integrated, high-performance solutions for the Citrix DaaS and Twilio Flex environments.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Defnition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis