ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

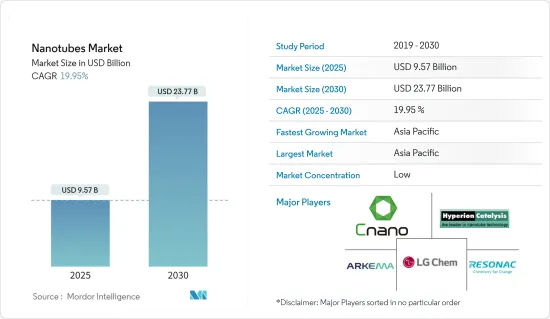

나노튜브 시장 규모는 2025년 95억 7,000만 달러로 추정되며, 2030년에는 237억 7,000만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 19.95%의 CAGR을 기록할 것으로 예상됩니다.

나노튜브 시장은 COVID-19 사태로 인해 생산과 이동이 느려지고 반도체가 부족해지면서 나노튜브 시장에 부정적인 영향을 미쳤습니다. 또한 전자, 에너지, 항공우주 및 기타 산업도 봉쇄 조치와 경제적 혼란으로 인해 생산이 지연되었습니다. 현재 시장은 전염병에서 회복되고 있습니다. 시장은 2022년 팬데믹 이전 수준에 도달할 것으로 예상되며, 앞으로도 안정적인 성장이 예상됩니다.

조사 대상 시장의 성장을 촉진하는 주요 요인은 나노튜브 기술의 발전과 탄소나노튜브의 채택 확대입니다.

반면, 높은 제조 비용과 R&D 비용은 조사 대상 시장의 성장에 주요 장애물이 되고 있습니다.

전자기기 및 저장 장치의 잠재적 응용 분야가 증가함에 따라 예측 기간 동안 조사 대상 시장에 기회를 제공할 가능성이 높습니다.

전자, 에너지, 항공우주, 방위 산업 등 산업분야의 응용과 수요 증가가 나노튜브의 수요를 크게 견인하고 있으며, 아시아태평양이 세계 시장을 주도하고 있습니다.

나노튜브 시장 동향

전자 및 반도체 부문이 시장 수요를 독식

나노튜브는 더 빠르고, 더 효율적이며, 더 내구성이 뛰어난 전자 장치 개발을 위해 전자 산업에서 광범위하게 응용되고 있습니다.

모든 종류의 나노튜브 중에서도 탄소나노튜브는 전자산업에 응용되어 시장 수요를 주도하고 있습니다. 탄소나노튜브 외에도 실리콘 나노 튜브와 무기 나노 튜브도 전자 산업에서 사용되고 있습니다.

탄소나노튜브는 디스플레이, 대면적 표면 전도, 컬러 전계 발광 디스플레이, 센서, 디스플레이 백라이트, 진행파관, 트랜지스터, 태양광발전, 디스플레이 외의 전도성 첨가제, 포토닉스, 무선 주파수 식별(RFID) 태그, 중성자선원, 감마선원, 조명 장치 등에 적용됩니다. 감마선원, 조명장치 등에 응용되고 있습니다.

실리콘 나노튜브는 수소 분자를 함유하고 있어 금속 연료와 같은 역할을 합니다. 따라서 전자 산업에서 반도체 응용 분야에 널리 사용되고 있습니다.

무기 나노 튜브는 또한 반도체 장치, 센서, 바이오 센서, 나노 모터, 평판 디스플레이에 적용하기 위해 전자 산업에서 사용되고 있습니다. 따라서 여러 전자부품에 나노 튜브의 다양한 응용 덕분에 나노 튜브에 대한 수요가 증가할 것으로 예상됩니다.

전기 및 전자 산업에서의 사용량 증가와 응용 분야 확대는 시장 성장을 촉진할 것으로 예상됩니다.

예를 들어, 일본전자정보기술산업협회(JEITA)에 따르면 2021년 세계 전자-IT 산업 생산액은 3조 4,159억 달러, 2022년 3조 4,368억 달러로 전년 대비 1%의 성장률을 기록할 것으로 추정됩니다. 또한 2023년에는 전년 대비 3%의 성장률로 3조 5,266억 달러에 달할 것으로 예상됩니다.

반도체산업협회(SIA)에 따르면 2022년 세계 반도체 산업 매출은 5,741억 달러로 2021년 5,559억 달러에 비해 3.3% 증가할 것으로 예상했습니다.

또한 지역별로는 2022년 미주 시장 매출이 가장 큰 증가율(16.2%)을 기록했습니다. 중국은 여전히 가장 큰 개별 반도체 시장으로 2022년 매출은 2021년 대비 6.2% 감소한 1,804억 달러로 나타났습니다. 또한 유럽(12.8%)과 일본(10.2%)도 2022년 연간 매출이 증가했습니다.

이러한 성장으로 인해 예측 기간 동안 이 지역의 전자 애플리케이션용 나노튜브에 대한 수요가 증가할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

아시아태평양은 전자, 에너지, 헬스케어, 항공우주 및 방위, 자동차 등의 산업에서 수요가 증가하면서 세계 시장 점유율을 독식하고 있습니다.

일본전자정보기술산업협회(JEITA)에 따르면 2022년 일본 전자산업 국내 생산액은 11조 1,243억 엔(851억 9,000만 달러)로 전년 대비 2%의 성장률을 기록할 것으로 추정됩니다. 일본 전자산업의 국내 생산은 2023년 11조 4,029억 엔(873억 2,000만 달러)에 달해 전년 대비 3%의 성장률을 기록할 것으로 보입니다.

또한 전자정보기술부에 따르면 인도 전역의 소비자 전자제품(TV, 액세서리, 오디오) 생산액은 2022년 7,450억 인도 루피(94억 6,000만 달러)를 넘어설 것으로 예상하고 있습니다. 이는 시장 성장을 뒷받침하고 있습니다.

또한 중국민용항공국(CAAC)은 항공 부문의 국내 교통량이 팬데믹 이전의 85% 수준으로 회복될 것으로 예상하고 있습니다. 보잉의 상용 전망 2023-2042에 따르면, 2042년까지 중국에서 약 8,560대의 항공기가 새로 인도될 것이며, 2042년까지 6,750억 달러의 시장 서비스 가치가 발생할 것으로 예상했습니다. 이러한 신규 납품은 항공기 분야에서 나노튜브에 대한 수요를 증가시킬 것으로 보입니다.

또한, 아시아태평양의 자동차 산업 성장으로 인해 시장 성장이 더욱 촉진될 것입니다. 중국, 인도, 일본, 한국 등 신흥국들은 자동차 제조의 수익성을 높이기 위해 제조 기반을 강화하고 효율적인 공급망을 개발하는 데 주력하고 있습니다.

중국 정부의 정책 개발에는 새로운 내연기관차 제조 공장에 대한 투자 제한과 2025년까지 소형 승용차의 평균 연비를 강화하는 제안이 포함됩니다.

또 인도자동차산업협회(SIAM)에 따르면 2022년 인도에서 판매된 승용차는 379만대로 2021년 판매된 승용차 대비 약 23%의 성장률을 기록했습니다.

또한 중국민용항공국(CAAC)은 항공 부문의 국내 교통량이 팬데믹 이전의 85% 수준으로 회복될 것으로 예상하고 있습니다. Boeing Commercial Outlook 2023-2042에 따르면, 2042년까지 중국에서는 약 8,560대의 항공기가 새로 인도될 것이며, 2042년까지 시장 서비스 금액은 6,750억 달러에 달할 것으로 예상됩니다.

따라서, 상기 동향은 예측 기간 동안 이 지역의 나노튜브 수요를 촉진할 것으로 예상됩니다.

나노튜브 산업 개요

나노튜브 시장은 세분화되어 있습니다. 조사 대상 시장의 주요 기업으로는 Arkema, Hyperion Catalysis International, Jiangsu Cnano Technology, Resonac Holdings Corporation, LG Chem 등이 있습니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

나노튜브 기술의 진보

탄소나노튜브 채용 확대

기타 촉진요인

성장 억제요인

높은 제조 비용과 연구개발 비용

기타 저해요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

구매자의 교섭력

대체품의 위협

신규 참여업체의 위협

경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

종류별

탄소나노튜브

실리콘 나노튜브

무기 나노튜브

기타 유형(멤브레인 나노튜브 등)

구조 유형별

비폴리머 유기 나노재료

고분자 나노재료

용도별

수소 저장 디바이스

센서

고분자 바이오소재

리튬이온 배터리

발광 표시 디바이스

바이오센서

나노 전극

정수 필터

반도체 소자

전도성 플라스틱

최종 이용 산업별

헬스케어

일렉트로닉스

에너지

자동차

항공우주 및 방위

섬유

기타 최종 이용 산업(화학 재료 등)

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

시장 점유율(%)**/순위 분석

주요 기업의 전략

기업 개요

Arkema

Carbon Solutions Inc.

Cheap Tubes

Hyperion Catalysis International

Jiangsu Cnano Technology Co., Ltd.

Nano-C

Nanocyl SA(Birla Carbon)

NanoIntegris Inc.

Nanoshel LLC

Resonac Holdings Corporation

Thomas Swan & Co. Ltd

LG Chem

제7장 시장 기회와 향후 동향

전자기기나 스토리지 기기의 잠재적 용도 증가

기타 기회

ksm

영문 목차

영문목차

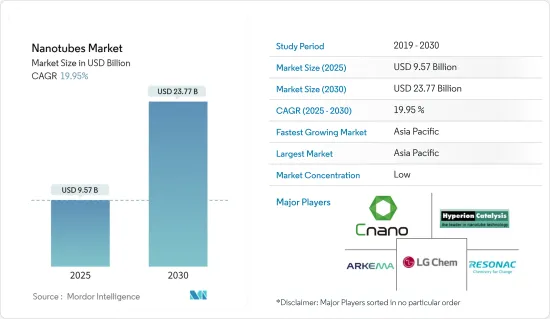

The Nanotubes Market size is estimated at USD 9.57 billion in 2025, and is expected to reach USD 23.77 billion by 2030, at a CAGR of 19.95% during the forecast period (2025-2030).

The nanotubes market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, which caused a shortage of semiconductors, which negatively impacted the market for nanotubes. Also, industries such as electronics, energy, and aerospace were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The major factors driving the growth of the market studied are an advancement in nanotube technologies and the growing adoption of carbon nanotubes.

On the flip side, high manufacturing and R&D costs serve as one of the major stumbling blocks in the growth of the market studied.

Rising potential uses in electronic and storage devices are likely to provide opportunities for the market studied during the forecast period.

Asia-Pacific dominated the global market, as the increasing application and demand from industries such as electronics, energy, aerospace, and defense majorly drive the demand for nanotubes.

Nanotubes Market Trends

Electronics and Semiconductor Segment to Dominate the Market Demand

Nanotubes find extensive application in the electronics industry, for the development of faster, more efficient, and more durable electronic devices.

Among all the types of nanotubes, carbon nanotubes lead the market demand due to their applications in the electronics industry. Apart from carbon nanotubes, silicon nanotubes, and inorganic nanotubes are also used in the electronics industry.

Carbon nanotubes find application in displays, large area surface conduction, color field emission displays, sensors, backlights for displays, traveling wave tubes, transistors, photovoltaics, conductive additives for non-display applications, photonics, radio-frequency identification (RFID) tags, neutron, and gamma-ray sources, and lighting devices.

Silicon nanotubes contain hydrogen molecules and act like metal fuels. Thus, they are widely used for semiconductor applications in the electronics industry.

Inorganic nanotubes are also used in the electronics industry for application in semiconductor devices, sensors, biosensors, nano-motors, and flat panel displays. Hence, owing to the diversified application of nanotubes in several electronic components, the demand for nanotubes is expected to increase.

The increasing usage and widening arena of application in the electrical and electronics industry is expected to drive market growth.

For instance, according to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year on year, compared to USD 3,415.9 billion in 2021. Moreover, the industry is expected to reach USD 3,526.6 billion, with a growth rate of 3% year on year in 2023.

According to the Semiconductor Industry Association (SIA), the global semiconductor industry sales totaled USD 574.1 billion in 2022, registering an increase of 3.3% compared to 2021 with USD 555.9 billion.

Furthermore, on a regional basis, sales into the Americas market saw the largest increase (16.2%) in 2022. China remained the largest individual market for semiconductors, with sales there totaling USD 180.4 billion in 2022, a decrease of 6.2% compared to 2021. Moreover, annual sales also increased in 2022 in Europe (12.8%) and Japan (10.2%).

This growth is expected to increase the demand for nanotubes for electronic applications in the region during the forecast period.

Asia-Pacific Region to Dominate the Market

Asia-Pacific region dominated the global market share due to the increasing demand from industries such as electronics, energy, healthcare, aerospace and defense, and automotive.

Japan is one of the largest producers of electronics; as per the Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry was estimated at JPY 11,124.3 billion (USD 85.19 billion) in 2022, witnessing a growth rate of 2% compared to the previous year. The domestic production by the Japanese electronics industry is likely to reach JPY 11,402.9 billion (USD 87.32 billion) by 2023, registering a growth rate of 3% year-on-year.

Moreover, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022. Thus supporting the growth of the market.

Additionally, The Civil Aviation Administration of China (CAAC) has estimated the aviation sector to recover domestic traffic to around 85% of pre-pandemic levels. According to the Boeing Commercial Outlook 2023-2042, in China, around 8,560 new deliveries will be made by 2042, and the market service value will account for USD 675 billion by 2042. Owing to such new deliveries in the country, the demand for nanotubes in the aircraft sector will likely rise.

Moreover, the market growth is further boosted by the growing automotive industry in the Asia-Pacific region. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability in vehicle manufacturing.

The Chinese government policy developments include the restriction of investments in new ICE-vehicle manufacturing plants and a proposal to tighten the average fuel economy of its light-duty passenger vehicle fleet by 2025.

In addition, according to the Society of Indian Automobile Manufacturers (SIAM), a total of 3.79 million passenger vehicles were sold in India in 2022, witnessing a growth rate of around 23% compared to the passenger vehicles sold in the year 2021.

Additionally, The Civil Aviation Administration of China (CAAC) has estimated the aviation sector to recover domestic traffic to around 85% of pre-pandemic levels. According to the Boeing Commercial Outlook 2023-2042, in China, around 8,560 new deliveries will be made by 2042, and the market service value will account for USD 675 billion by 2042.

Hence, the trends above are expected to drive the demand for nanotubes in the region during the forecast period.

Nanotubes Industry Overview

The nanotubes market is fragmented in nature. The major players in the studied market (not in any particular order) include Arkema, Hyperion Catalysis International, Jiangsu Cnano Technology Co., Ltd, Resonac Holdings Corporation, and LG Chem, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Advancement in Nanotubes Technologies

4.1.2 Growing Adoption of Carbon Nanotubes

4.1.3 Other Drivers

4.2 Restraints

4.2.1 High Manufacturing and R&D Cost

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of Substitute Products and Services

4.4.4 Threat of New Entrants

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Carbon Nanotubes

5.1.2 Silicon Nanotubes

5.1.3 Inorganic Nanotubes

5.1.4 Other Types (Membrane Nanotubes, Etc.)

5.2 Structure Type

5.2.1 Non-polymer Organic Nanomaterials

5.2.2 Polymeric Nanomaterials

5.3 Application

5.3.1 Hydrogen Storage Devices

5.3.2 Sensors

5.3.3 Polymeric Biomaterials

5.3.4 Li-ion Batteries

5.3.5 Luminescent Display Devices

5.3.6 Biosensors

5.3.7 Nanoelectrodes

5.3.8 Water Purification Filters

5.3.9 Semiconductor Devices

5.3.10 Conductive Plastics

5.4 End-user Industry

5.4.1 Healthcare

5.4.2 Electronics

5.4.3 Energy

5.4.4 Automotive

5.4.5 Aerospace and Defense

5.4.6 Textile

5.4.7 Other End-user Industries (Chemical Materials, Etc.)

5.5 Geography

5.5.1 Asia-Pacific

5.5.1.1 China

5.5.1.2 India

5.5.1.3 Japan

5.5.1.4 South Korea

5.5.1.5 Rest of Asia-Pacific

5.5.2 North America

5.5.2.1 United States

5.5.2.2 Canada

5.5.2.3 Mexico

5.5.3 Europe

5.5.3.1 Germany

5.5.3.2 United Kingdom

5.5.3.3 France

5.5.3.4 Italy

5.5.3.5 Rest of Europe

5.5.4 South America

5.5.4.1 Brazil

5.5.4.2 Argentina

5.5.4.3 Rest of South America

5.5.5 Middle-East and Africa

5.5.5.1 Saudi Arabia

5.5.5.2 South Africa

5.5.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Arkema

6.4.2 Carbon Solutions Inc.

6.4.3 Cheap Tubes

6.4.4 Hyperion Catalysis International

6.4.5 Jiangsu Cnano Technology Co., Ltd.

6.4.6 Nano-C

6.4.7 Nanocyl SA (Birla Carbon)

6.4.8 NanoIntegris Inc.

6.4.9 Nanoshel LLC

6.4.10 Resonac Holdings Corporation

6.4.11 Thomas Swan & Co. Ltd

6.4.12 LG Chem

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Rising Potential Uses in Electronic and Storage Devices