일본의 HVAC : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2024-2029년)

Japan HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1550509

리서치사:Mordor Intelligence

발행일:2024년 09월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

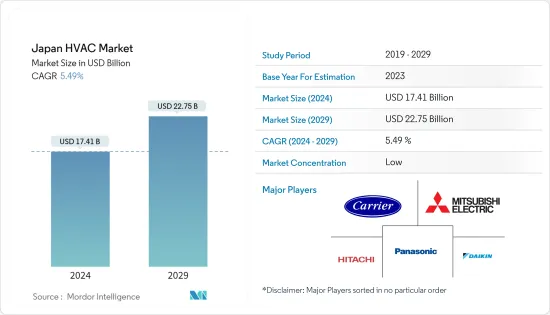

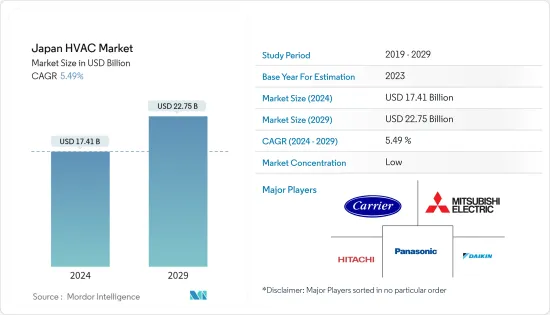

일본의 HVAC 시장 규모는 2024년에 174억 1,000만 달러로 추정되며, 2029년에는 227억 5,000만 달러에 달할 것으로 예측되며, 예측 기간(2024-2029년)의 CAGR은 5.49%로 성장할 것으로 예측됩니다.

주요 하이라이트

HVAC는 아파트, 단독주택, 호텔, 노인 시설과 같은 주거용 주택과 병원과 같은 중대형 산업 및 사무용 건물 등 다양한 환경에서 필수적인 역할을 하고 있으며, HVAC 시스템은 온도와 습도를 조절하고 신선한 외부 공기를 유입시켜 안전하고 건강한 환경을 조성하는 데 도움을 줍니다. 건강한 환경을 조성하는 데 도움을 주고 있습니다.

일본의 HVAC 시장의 성장은 주로 급속한 산업화와 도시화에 의해 촉진되고 있습니다. 산업, 상업 및 주거용 건물 건설이 급증하면서 HVAC 시장에 대한 수요가 크게 증가했습니다.

일본에서는 상당수의 개인이 지방에서 도시로 이주하고 있으며, 그 결과 주택, 상업용 건설 및 산업 인프라에 대한 투자가 증가하고 있습니다. 새로 지어진 건물에 새로운 HVAC 장비를 설치해야 할 필요성이 시장 성장을 더욱 촉진하고 있습니다.

일본에서는 데이터센터 등의 용도로 수냉식 시스템에 대한 수요가 증가하고 있습니다. 일본내 데이터센터의 확장은 HVAC 장비 및 서비스에 대한 수요를 더욱 증가시킬 것으로 보입니다. 예를 들어 아마존 웹 서비스(Amazon Web Services Inc.)는 2024년 1월, 2027년까지 일본에 152억 4,000만 달러를 투자하여 지역 데이터센터 네트워크를 강화할 계획입니다. 이 인프라 확충은 일본의 국내총생산(GDP)에 약 380억 달러의 기여를 할 것이라고 아마존닷컴의 자회사는 밝혔습니다.

HVAC 서비스 시장에는 인력 부족이라는 두드러진 과제가 있습니다. 하지만 이러한 장애물에도 불구하고, 제조업체와 기타 서비스 프로바이더들의 적극적인 조치 덕분에 시장은 번창하고 있습니다.

일본의 HVAC 시장은 단편화되어 있으며, 많은 업체들이 작은 시장 점유율을 차지하고 있습니다. 이 업계에서 사업을 운영하는 업체들은 증가하는 고객 수요에 대응하기 위해 신제품 개발, 전략적 제휴, 인수 및 사업 확장에 주력하고 있으며, 이는 시장 성장을 더욱 촉진하고 있습니다.

예를 들어 2024년 6월 Carrier Corporation은 편안함과 에너지 솔루션을위한 새로운 서비스 기반 모델 출시를 발표했으며, Carrier가 제공하는 Cooling-as-a-Service를 통해 고객은 시스템 및 장비 구매를 위한 초기 자본 지출에 직면하는 대신 확장된 성능과 일관된 지불을 보장할 수 있습니다. 이 혁신적인 금융 접근 방식을 통해 고객은 본연의 업무에 집중할 수 있으며, 캐리어의 종합적인 전문 지식을 활용하여 편안함과 업무 효율성을 보장할 수 있습니다.

또한 일본에서는 공해 수준이 높아지면서 환경 친화적인 건물을 중요시하는 경향이 강해지고 있습니다.

일본의 HVAC 시장은 정부 규제와 에너지 효율이 높은 장비의 채택을 촉진하는 새로운 노력과 같은 거시경제적 요인에 의해 크게 영향을 받고 있습니다. 예를 들어 일본은 2030년까지 온실가스 배출량을 46% 감축하는 것을 목표로 하고 있으며, 더 나아가 50% 감축을 달성하기 위해 노력하고 있습니다.

일본의 HVAC 시장 동향

HVAC 장비가 큰 시장 점유율을 차지

실내외 공기 환경 개선에 대한 요구가 높아지면서 일본내 HVAC 장비가 확대되는 주요 요인이 되고 있습니다. 공기질의 중요성에 대한 인식이 높아지면서 주택 소유주와 사업주들은 실내 공기를 효과적으로 여과하고 정화하며 야외 배기가스를 최소화할 수 있는 HVAC 시스템을 구매하고 있습니다.

공기 처리 장비(AHU)와 같은 환기 시스템은 쇼핑센터와 같이 많은 사람들이 자주 드나드는 넓은 공간에서 자주 사용됩니다. 이러한 시설에서는 공기질 및 CO2 수준에 대한 엄격한 규제를 준수해야 합니다. 에어 핸들링 유닛은 외부 공기를 실내로 유입시켜 대규모 시설에서 일반적으로 사용되는 여러 개의 송풍 팬의 필요성을 효과적으로 줄일 수 있습니다.

히트펌프는 냉동 사이클을 통해 추운 지역에서 더운 지역으로 열을 이동시키는 필수적인 HVAC 장비입니다. 그 결과, 추운 지역은 냉각되고 더운 지역은 따뜻해집니다. 기온이 낮을 때 히트펌프는 외부 환경으로부터 열을 끌어들여 집을 따뜻하게 하고, 기온이 높을 때 집 안의 열을 야외로 배출할 수 있습니다. 히트펌프는 열을 발생시키는 것이 아니라 열을 이동시킬 수 있으므로 주거용 대체 냉난방 시스템보다 에너지 효율이 높은 것으로 알려져 있습니다.

일본 회원국의 보고서는 일본의 히트펌프 발전에도 초점을 맞추고 2050년 넷제로를 목표로 하는 최신 법률에 초점을 맞추었습니다. 정부는 탈탄소를 위한 핵심 기술로 산업용 HP(IHP) 및 상업용 및 가정용 히트펌프 온수기(HPWH)에 대한 구체적인 목표를 설정하고 히트펌프의 사용을 적극적으로 추진하고 있습니다.

에어컨(AC) 시장은 가정용 룸 에어컨의 성장이 예상되지만, 이 목표를 효과적으로 달성하기 위해서는 산업용 HP와 HPWH의 보급을 가속화하는 것이 시급한 과제입니다. 따라서 국내 건설 활동의 활성화는 HVAC 장비의 채택을 촉진할 것으로 보입니다. 국토교통성에 따르면 2023년 일본에서는 약 9,580건의 오피스 건설 프로젝트가 시작될 예정이며, 그 총 연면적은 전년과 동일합니다.

주택 부문이 큰 시장 점유율을 차지하고 있습니다.

지방에서 도심으로 인구 이동이 증가함에 따라 주택 개발이 급증하고 있습니다. 그 결과, HVAC 장비 수요에도 직접적인 영향을 미치고 있습니다. 이러한 건물은 늘어나는 도시 인구를 수용하기 위해 효과적인 냉방 및 공기질 관리 시스템이 필요하기 때문입니다.

국토교통성에 따르면 2023년에는 일본에서 약 81만 9,600채의 주택 건설이 시작될 예정입니다. 민간 부문의 주택 건설 투자는 2023년도에 17조 4,000억 엔으로 증가할 것으로 예측되었습니다. 마찬가지로 일본에서는 2023년도에 약 36만 6,800채의 단독주택이 착공될 예정입니다.

일본의 주택 부문에서 공조 및 환기 시스템에 대한 수요가 증가하고 있습니다. 공조 및 환기 시스템은 여과와 환기를 통해 실내 공기질을 유지하는 데 중요한 역할을 합니다. 대기 오염 수준 증가와 바이러스 확산으로 인해 공기질 개선을 위한 보다 진보된 HVAC 시스템의 필요성이 대두되고 있습니다.

주택 산업에서 HVAC 장비의 정기적 인 정비 및 수리는 HVAC 시스템의 최고 성능을 보장하기 위해 국내 HVAC 서비스에 대한 수요를 증가시킵니다. 정기적 인 HVAC 정비 및 수리의 중요한 이점 중 하나는 시스템의 효율성을 높이는 능력입니다. 적절한 유지보수가 이루어지지 않으면 시스템은 운영상의 문제에 직면하여 에너지 사용량 증가와 장기적인 비용 증가로 이어질 수 있습니다. 주거 분야에서 효율적인 관행에 대한 수요가 증가함에 따라 HVAC 서비스에 대한 요구도 증가할 것으로 예상됩니다.

국내 업체들은 시장 점유율을 높이기 위해 존재감을 확대하는 데 주력하고 있으며, 이는 시장 성장을 더욱 촉진하고 있습니다. 예를 들어 Daikin Industries Ltd는 2023년 8월 이바라키현 츠쿠바미라이시에 새로운 에어컨 제조 시설을 건설하기 위해 토지를 임베디드했다고 발표했습니다. 이 전략적 이전은 현지 생산 능력을 강화하고 일본 시장에서의 입지를 확대하고자 하는 회사의 목표를 지원하기 위한 것입니다.

일본의 HVAC산업 개요

일본의 HVAC 시장은 여러 기업으로 구성된 단편화된 시장입니다. 각 업체들은 신제품 출시, 사업 확장, 전략적 M&A, 제휴, 협업 등을 통해 시장에서의 입지를 강화하기 위해 끊임없이 노력하고 있습니다. 주요 업체로는 Carrier Corporation, Daikin Industries Ltd, Mitsubishi Electric Corporation, Hitachi Ltd, Panasonic Corporation 등이 있습니다.

2024년 5월, Daikin Industries Ltd와 산업용 보일러 제조업체인 Miura는 자본 및 업무 제휴 계획을 밝혔습니다. 전국 공장을 대상으로 난방, 환기, 공조, 증기 보일러, 수처리 시스템 등의 종합적인 솔루션을 제안하는 것을 목표로 합니다.

2024년 5월, Carrier Corporation은 대형 시설용 HVAC 솔루션을 확대하기 위해 터보냉동기 'Carrier AquaEdge 19DV' 시리즈를 일본에 도입했습니다. 이 새로운 AquaEdge 19DV 시리즈는 일본에서 호평을 받고 있는 모듈형 냉각기 Universal Smart X 시리즈에 추가되는 귀중한 제품으로, 일본 상업용 시설 고객의 요구를 충족시키기 위해 설계되었으며, 효율성과 편안함을 모두 보장하는 최첨단 신뢰성 효율성과 편안함을 모두 보장하는 첨단이고 신뢰할 수 있는 시스템을 제공합니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 교섭력

신규 진출업체의 위협

대체품의 위협

경쟁 기업 간 경쟁 강도

업계 밸류체인 분석

COVID-19 부작용과 기타 거시경제 요인이 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

세액공제 프로그램에 의한 에너지 효율 장려를 포함한 정부의 지원 규제

에너지 효율이 높은 기기에 대한 수요의 증가

수요를 지원하는 건설과 개보수 활동의 증가

시장이 해결해야 할 과제

에너지 효율이 높은 시스템의 높은 초기 비용

제6장 시장 세분화

부품 유형별

HVAC 기기

난방 기기

공조·환기 기기

HVAC 서비스

최종사용자 산업별

주택

상업

산업용

제7장 경쟁 구도

기업 개요

Johnson Controls International PLC

Carrier Corporation

Robert Bosch GmbH

Daikin Industries Ltd

Midea Group Co. Ltd

System Air AB

LG Electronics Inc.

Mitsubishi Electric Corporation

Danfoss A/S

Lennox International Inc.

Hitachi Ltd

Panasonic Corporation

제8장 투자 분석

제9장 시장의 미래

KSA

영문 목차

영문목차

The Japan HVAC Market size is estimated at USD 17.41 billion in 2024, and is expected to reach USD 22.75 billion by 2029, growing at a CAGR of 5.49% during the forecast period (2024-2029).

Key Highlights

HVAC plays an essential role in various settings, including residential buildings like apartments, single-family homes, hotels, and senior living facilities, as well as in medium-to-large industrial and office structures such as hospitals. HVAC systems help create safe and healthy environments by controlling temperature and humidity and incorporating fresh outdoor air.

Japan's HVAC market growth is primarily fueled by swift industrialization and urbanization. The surge in industrial, commercial, and residential building construction is leading to a substantial demand for the HVAC market.

In Japan, a significant number of individuals have relocated from rural to urban areas, resulting in increased investments in housing, commercial construction, and industrial infrastructure. The need to install new HVAC equipment in newly constructed buildings further propels the market growth.

Japan has been witnessing a demand for liquid cooling systems for applications such as data centers. The increasing expansion of data centers in the country will further drive the demand for HVAC equipment and services. For instance, in January 2024, Amazon Web Services Inc. plans to invest USD 15.24 billion in Japan by 2027 to enhance its local data center network. The expansion of infrastructure is expected to contribute approximately USD 38 billion to Japan's gross domestic product, as stated by the Amazon.com Inc. subsidiary.

The HVAC services market has seen a notable challenge in the form of a labor shortage. Nevertheless, despite these obstacles, the market has thrived thanks to the proactive measures taken by manufacturers and other service providers.

The HVAC market in Japan is fragmented, with a large number of players occupying a small market share. Vendors operating in the industry are focusing on new product development, strategic partnership, acquisition, and expansion to meet the rising customer demand, further supporting the market growth.

For instance, in June 2024, Carrier Corporation announced the launch of a new service-based model for comfort and energy solutions. Carrier's cooling-as-a-service offering enables customers to secure extended performance and consistent payments instead of facing an initial capital expense for system or equipment acquisitions. This innovative financial approach empowers customers to concentrate on their primary operations, leveraging Carrier's comprehensive expertise to ensure comfort and operational effectiveness.

Additionally, the rising pollution levels in Japan are driving the nation to enhance its emphasis on eco-friendly buildings, potentially opening up numerous opportunities for businesses to invest and grow in the Japanese HVAC market.

The HVAC market in Japan is highly affected by macroeconomic factors such as government regulations and new initiatives to boost the adoption of energy-efficient equipment. For instance, Japan aims to cut its greenhouse gas emissions by 46% by 2030, steadfastly committed to achieving an even more ambitious 50% reduction.

Japan HVAC Market Trends

HVAC Equipment Holds Significant Market Share

The increasing need for better indoor and outdoor air quality is a major factor fueling the expansion of HVAC equipment in Japan. Growing recognition of the crucial role of air quality encourages homeowners and business owners to purchase HVAC systems that can effectively filter and purify indoor air and minimize outdoor emissions.

Ventilation systems, such as air handling units (AHUs), are frequently utilized in spacious establishments that numerous individuals, such as shopping centers, frequently access. These establishments are required to adhere to strict regulations concerning air quality and CO2 levels. By introducing outside air into the rooms, air handling units can effectively decrease the necessity for multiple blower fans typically used in large facilities.

Heat pumps are essential HVAC equipment that moves heat from a colder area to a hotter area through a refrigeration cycle. This results in cooling the colder area and warming the hotter area. During colder temperatures, a heat pump is able to draw heat from the external environment to warm a home, whereas during hotter temperatures, it can expel heat from the house to the outdoors. Heat pumps are considered more energy-efficient than alternative heating or cooling systems for residential use, considering the capability of heat pumps to transfer heat rather than produce it.

The Japan Member Country Report also focused on the advancement of heat pumps in Japan, highlighting the latest legislation targeting 2050 net zero. The government is actively promoting the use of heat pumps by setting specific targets for industrial HPs (IHP) and commercial and household heat pump water heaters (HPWH) as crucial technologies for decarbonization.

Although the air conditioners (AC) market will witness growth in residential room ACs, there is a pressing need for accelerated deployment of industrial HPs and HPWHs to effectively achieve the outlined goals. Thus, the growing construction activities in the country will propel the adoption of HVAC equipment. According to MLIT (Japan), in 2023, Japan initiated approximately 9,580 office construction projects, the total floor area of which remained consistent with the previous year.

The rise in rural populations moving to urban centers has resulted in a surge in the development of residential structures. Consequently, there has been a direct impact on the need for HVAC equipment, as these buildings necessitate effective cooling and air quality management systems to cater to the expanding urban populace.

According to MLIT Japan, in 2023, approximately 819.6 thousand housing units were initiated in Japan. Residential construction investment by the private sector was forecasted to increase to JPY 17.4 trillion in fiscal year 2023. Similarly, in Japan, construction began on approximately 366.8 thousand detached houses in 2023.

The demand for air conditioning and ventilation systems in Japan's residential sector is increasing. AC and ventilation systems play a crucial role in preserving indoor air quality using filtration and ventilation. The rising levels of air pollution and the spread of viruses drive the need for more advanced HVAC systems to deliver improved air quality.

Regular maintenance and repairs of the HVAC equipment in the residential industry guarantee peak performance of HVAC systems, thus increasing demand for HVAC services in the country. One key benefit of routine HVAC upkeep and repairs is the capacity to enhance the system's effectiveness. In the absence of proper maintenance, the system could encounter operational challenges, leading to heightened energy usage and greater expenses over time. With the growing demand for efficient practices in the residential sector, the requirement for HVAC services will also grow.

The players in the country are focusing on expanding their presence to capture a significant market share, further supporting the market growth. For instance, in August 2023, Daikin Industries Ltd announced that it would purchase land in Tsukubamirai City, Ibaraki Prefecture, Japan, to create a new manufacturing facility for air conditioners. This strategic move will enhance the company's local production capabilities and support its goal of expanding its presence in the Japanese market.

Japan HVAC Industry Overview

The Japanese HVAC market is fragmented and consists of several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering strategic mergers and acquisitions, partnerships, and collaborations. Some of the major players include Carrier Corporation, Daikin Industries Ltd, Mitsubishi Electric Corporation, Hitachi Ltd, Panasonic Corporation, and many more.

May 2024: Daikin Industries Ltd and Miura Co. Ltd, an industrial boiler manufacturer, revealed their plans to establish a capital and business alliance. This collaboration aims to offer comprehensive solution proposals encompassing heating, ventilation, air conditioning, steam boilers, and water treatment systems for factories throughout Japan.

May 2024: Carrier Corporation introduced the Carrier AquaEdge 19DV centrifugal chiller series in Japan, expanding its HVAC solutions for large-scale facilities. This new series, AquaEdge 19DV, will be a valuable addition to the popular Universal Smart X series of modular chillers in Japan. The AquaEdge 19DV series is designed to meet the demands of commercial customers in Japan, providing a cutting-edge and reliable system that guarantees both efficiency and comfort.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

5.1.2 Increasing Demand For Energy Efficient Devices

5.1.3 Increased Construction And Retrofit Activity To Aid Demand

5.2 Market Challenges

5.2.1 High Initial Cost of Energy Efficient Systems