HVAC Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1833442

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 185 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

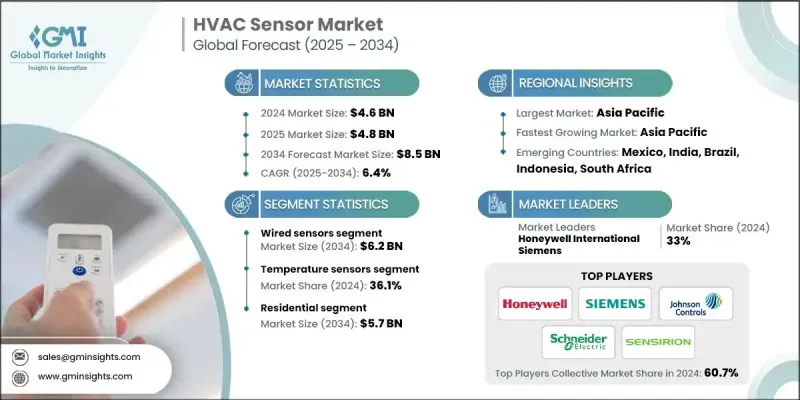

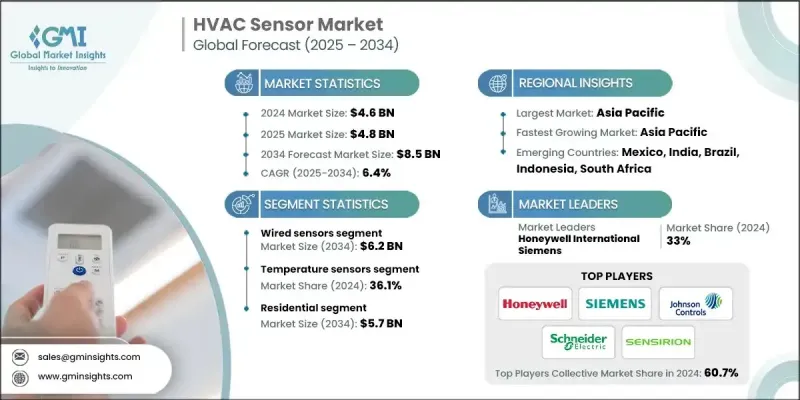

세계의 HVAC 센서 시장은 2024년에는 46억 달러로 평가되었고, CAGR 6.4%로 성장하여 2034년에는 85억 달러에 이를 것으로 추정되고 있습니다.

주거 환경의 HVAC 시스템 설치 증가와 함께 실내 공기질에 대한 관심이 높아지면서 첨단 센서 기술에 대한 수요가 지속적으로 증가하고 있습니다. 온도, 습도, 이산화탄소, 미립자 물질, 휘발성 유기화합물 등을 실시간으로 모니터링하는 다기능 센서 유닛을 채택하는 부동산 소유주 및 시설 운영자가 늘고 있습니다. 이러한 변화는 건강, 편안함, 공기질에 대한 소비자의 인식이 높아지고 환경 안전에 초점을 맞춘 규제 프레임워크에 의해 촉진되고 있습니다. HVAC 시스템이 고도화되고 상호 연결됨에 따라 공기질과 에너지 효율을 보장하는 정밀 센서에 대한 수요는 상업, 산업, 주거 분야에서 증가하고 있습니다.

시장 범위

개시 연도

2024년

예측 연도

2025-2034년

시장 규모

46억 달러

예측 금액

85억 달러

CAGR

6.4%

유선 센서 분야는 신뢰성, 일관된 성능, 데이터 무결성으로 인해 대규모 산업 및 상업 공간에서 우위를 유지하며 2034년까지 62억 달러 규모 시장을 창출할 것으로 예측됩니다. 무선 대안이 인기를 끌고 있지만, 원활한 통신과 최소한의 대기 시간이 중요한 미션 크리티컬한 환경에서는 유선 구성이 여전히 선호되고 있습니다. 제조업체는 현재 설치 편의성을 높이고 유선 센서의 핵심 성능 이점을 손상시키지 않고 유선 센서를 중앙 제어 인프라에 보다 효과적으로 통합하는 데 주력하고 있습니다.

온도 센서 분야는 2024년 36.1%의 점유율을 차지했습니다. 스마트 HVAC 시스템으로의 통합은 더욱 정교해지고 있으며, 종종 습도, CO2, 대기 오염 물질도 감지하는 다기능 장치로 패키지화되어 있습니다. 이러한 첨단 온도 센서는 지능형 기후 조절에 중요한 역할을 하며, 기류와 온도를 실시간으로 조정하여 쾌적함을 개선하고 에너지 사용량을 줄이는 데 중요한 역할을 합니다. 커넥티드 빌딩의 진화에 따라 IoT 프로토콜에 적합한 소형, 고정밀 센서가 제조업체와 최종 사용자들 사이에서 인기를 끌고 있습니다.

북미 HVAC 센서 시장은 2024년 27%의 점유율을 차지할 것으로 예상되며, 2034년까지 연평균 6.6%의 성장률을 보일 것으로 전망됩니다. 이 지역의 강력한 모멘텀은 에너지 효율이 높은 HVAC 설비에 대한 수요 증가와 스마트 빌딩 생태계의 확산에 기인합니다. 북미에서 다중 매개변수 센서의 사용은 주거 및 상업용 건물 전반의 공기 관리 전략을 꾸준히 변화시키고 있으며, 규정 준수와 거주자의 편안함을 향상시키는 자동화된 데이터 기반 HVAC 시스템을 가능하게 하고 있습니다.

HVAC 센서 시장에서 사업을 전개하는 주요 기업으로는 지멘스, 존슨콘트롤스, 하니웰 인터내셔널, 센서리온, 슈나이더 일렉트릭 등이 있습니다. HVAC 센서 업계의 주요 기업들은 실시간 모니터링과 스마트 HVAC 통합에 대한 수요 증가에 대응하는 소형 다기능 센서 솔루션을 개발하여 시장 개척에 나서고 있습니다. 이들 기업은 연구개발에 많은 투자를 통해 온도, 습도, 공기질 감지를 하나의 모듈로 통합한 에너지 효율이 높은 IoT 대응 센서를 개발하고 있습니다. 스마트 빌딩 시스템 공급업체와의 파트너십과 상호운용성 및 데이터 분석에 대한 집중적인 노력은 전체 시스템 성능을 개선하고 배치를 간소화하는 데 도움이 되고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국

기본 추정과 계산

기준연도 계산

시장 예측 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

헬스케어 및 의약품 커스터마이즈 된 HVAC 솔루션 수요 증가

스마트홈과 빌딩 자동화 도입 확대

실내공기질(IAQ) 모니터링에 대한 주목 증가

주택 부문 HVAC 시스템 설치 증가

데이터센터 건설 급증이 냉각 수요를 촉진

업계의 잠재적 리스크&과제

초기 투자와 설치 비용이 높은

기존 HVAC 시스템과의 통합 복잡성

시장 기회

스마트하고 커넥티드건물에 대한 수요 증가

에너지 효율 규제와 기준

기존 HVAC 시스템 개보수와 업그레이드

빌딩 관리 시스템(BMS)과의 통합

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter의 Five Forces 분석

PESTEL 분석

기술 및 혁신 상황

현재 기술 동향

신기술

가격 동향

지역별

제품별

가격 전략

새로운 비즈니스 모델

컴플라이언스 요건

특허 및 지적재산 분석

지정학과 무역 역학

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 기업-경쟁 벤치마킹

재무 실적 비교

매출

이익률

연구개발

제품 포트폴리오 비교

제품 라인 업 넓이

테크놀러지

혁신

지역 존재감 비교

세계 발자국 분석

서비스 네트워크 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더들

과제자들

팔로워

니치 기업

전략적 전망 매트릭스

주요 발전, 2021-2024

인수합병(M&A)

파트너십 및 협업

기술적 진보

확대와 투자 전략

디지털 변혁 대처

신규 기업/스타트업 기업 경쟁 구도

제5장 시장 추산·예측 : 유형별, 2021-2034

주요 동향

온도 센서

습도 센서

압력 센서

연기와 가스 센서

모션 센서

기타

제6장 시장 추산·예측 : 접속 유형별, 2021-2034

주요 동향

유선 센서

무선 센서

제7장 시장 추산·예측 : 최종 용도별, 2021-2034

주요 동향

주택용

상업용

산업

제8장 시장 추산·예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제9장 기업 개요

세계의 주요 기업

Honeywell International

Siemens

Johnson Controls

TE Connectivity

Schneider Electric

지역별 주요 기업

북미

Emerson Electric

Trane

Amphenol

유럽

Belimo Holding

STMicroelectronics

Infineon Technologies

아시아태평양

Omron

Chino

Acal Bfi

니치 기업-/디스럽터

Sensirion

Sensata Technologies

Microchip Technology

Greystone Energy Systems

Texas Instruments

LSH

영문 목차

영문목차

The Global HVAC Sensor Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 8.5 billion by 2034.

Increasing emphasis on indoor air quality, coupled with growing HVAC system installations in residential environments, continues to fuel demand for advanced sensor technologies. A growing number of property owners and facility operators are turning to multi-functional sensor units to monitor temperature, humidity, carbon dioxide levels, particulate matter, and volatile organic compounds in real time. This shift is being driven by heightened consumer awareness around health, comfort, and air quality, as well as regulatory frameworks focused on environmental safety. As HVAC systems become more advanced and interconnected, the demand for precision sensors that ensure air quality and energy efficiency is rising across commercial, industrial, and residential sectors.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$4.6 Billion

Forecast Value

$8.5 Billion

CAGR

6.4%

The wired sensors segment is predicted to generate USD 6.2 billion by 2034, maintaining its dominance in large-scale industrial and commercial spaces due to its reliability, consistent performance, and data integrity. While wireless alternatives are gaining traction, wired configurations continue to be favored in mission-critical environments where seamless communication and minimal latency are key. Manufacturers are now focusing on enhancing installation convenience and integrating wired sensors more effectively into centralized control infrastructures without compromising their core performance advantages.

The temperature sensors segment held a 36.1% share in 2024. Their integration into smart HVAC systems is becoming more sophisticated, often packaged within multi-functional devices that also detect humidity, CO2, and air pollutants. These advanced temperature sensors play a crucial role in intelligent climate regulation, adapting airflow and temperature in real-time to improve comfort and reduce energy usage. As connected buildings evolve, compact, high-accuracy sensors that align with IoT protocols are gaining favor among manufacturers and end-users alike.

North America HVAC Sensor Market held 27% share in 2024 and is projected to grow at a CAGR of 6.6% through 2034. The region's strong momentum is driven by rising demand for energy-efficient HVAC installations and the proliferation of smart building ecosystems. The use of multi-parameter sensors in North America is steadily transforming air management strategies across residential and commercial properties, enabling automated, data-driven HVAC systems that improve compliance and occupant well-being.

Key players operating in the HVAC Sensor Market include Siemens, Johnson Controls, Honeywell International, Sensirion, and Schneider Electric. Leading companies in the HVAC sensor industry are advancing their market position by developing compact, multi-functional sensor solutions that align with the growing need for real-time monitoring and smart HVAC integration. These firms are investing heavily in R&D to create energy-efficient, IoT-compatible sensors that combine temperature, humidity, and air quality detection in a single module. Partnerships with smart building system providers and increased focus on interoperability and data analytics help enhance system-wide performance and simplify deployment.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Type trends

2.2.2 Connectivity type trends

2.2.3 End use trends

2.2.4 Regional trends

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising need for customized HVAC solutions in healthcare and pharmaceuticals

3.2.1.2 Growing adoption of smart homes and building automation

3.2.1.3 Rising focus on indoor air quality (IAQ) monitoring

3.2.1.4 Rising HVAC system installations in residential sector

3.2.1.5 Surge in data center construction driving cooling demand

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment and installation costs

3.2.2.2 Complexity in integration with existing HVAC systems

3.2.3 Market opportunities

3.2.3.1 Rising demand for smart and connected buildings

3.2.3.2 Energy efficiency regulations and standards

3.2.3.3 Retrofit and upgradation of legacy HVAC systems

3.2.3.4 Integration with building management systems (BMS)

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product

3.9 Pricing strategies

3.10 Emerging business models

3.11 Compliance requirements

3.12 Patent and IP analysis

3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million & Million Units)

5.1 Key trends

5.2 Temperature sensors

5.3 Humidity sensors

5.4 Pressure sensors

5.5 Smoke & gas sensors

5.6 Motion sensors

5.7 Others

Chapter 6 Market Estimates and Forecast, By Connectivity Type, 2021 - 2034 (USD Million & Million Units)

6.1 Key trends

6.2 Wired sensors

6.3 Wireless sensors

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Million Units)

7.1 Key trends

7.2 Residential

7.3 Commercial

7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Million Units)